Table of Contents

- Introduction

- Editor’s Choice

- Global Greenhouse Gas Emissions

- Carbon Emissions Statistics

- Food System Greenhouse Emissions Worldwide

- Emission Monitoring System (EMS) Market Statistics

- CO₂ Price Trends

- Installation of Continuous Emission Monitoring Systems (CEMS) in Various Industries Statistics

- Design Specifications of Different Components in Continuous Emission Monitoring System Statistics

- Emission Trading System Statistics

- CO₂ Emission Trading Contracts

- Clothing Companies Measuring Their Carbon Footprint

- Companies Setting and Monitoring GHG Emission Targets

- Oil and Gas Industry Methane Detection Spending Statistics

- Key Investments

- Regulations for Emission Monitoring Systems

- Recent Developments

- Conclusion

- FAQs

Introduction

Emission Monitoring System Statistics: An Emission Monitoring System (EMS) is a critical tool used to measure and report the concentration of pollutants, such as CO₂, NOx, SO₂, and particulate matter, from industrial processes.

It consists of sensors, analyzers, sampling probes, and data acquisition systems that continuously or periodically monitor emissions, ensuring compliance with environmental regulations.

EMS data supports both regulatory reporting and operational optimization, helping industries reduce emissions, improve energy efficiency, and maintain air quality standards.

By providing real-time insights and enabling corrective actions, EMS plays a key role in environmental protection, regulatory compliance, and sustainable industrial practices.

Editor’s Choice

- By 2033, the global emission monitoring system market is expected to attain a size of USD 9.7 billion.

- As of the latest data on the installation of Online Continuous Emission Monitoring Systems (OCEMS) in India, a total of 4,247 units were targeted across 17 key industrial categories under the Central Pollution Control Board (CPCB) guidelines.

- In the emission trading system (ETS) market, Germany leads with the highest government income, amounting to USD 12,590 million.

- In 2022, 19% of clothing companies were actively tracking and utilizing their carbon emissions data.

- In 2022, Hungary led Central and Eastern Europe, with 53% of companies setting and monitoring their GHG emissions targets.

- Between 2020 and 2030, emerging markets are expected to offer significant green investment opportunities across key sectors, totaling USD 10.2 trillion.

- In the United States, the Environmental Protection Agency (EPA) mandates continuous emission monitoring systems (CEMS) under various regulations, which include performance specifications for evaluating system acceptability at installation and ongoing quality assurance procedures to ensure data integrity for compliance purposes.

Global Greenhouse Gas Emissions

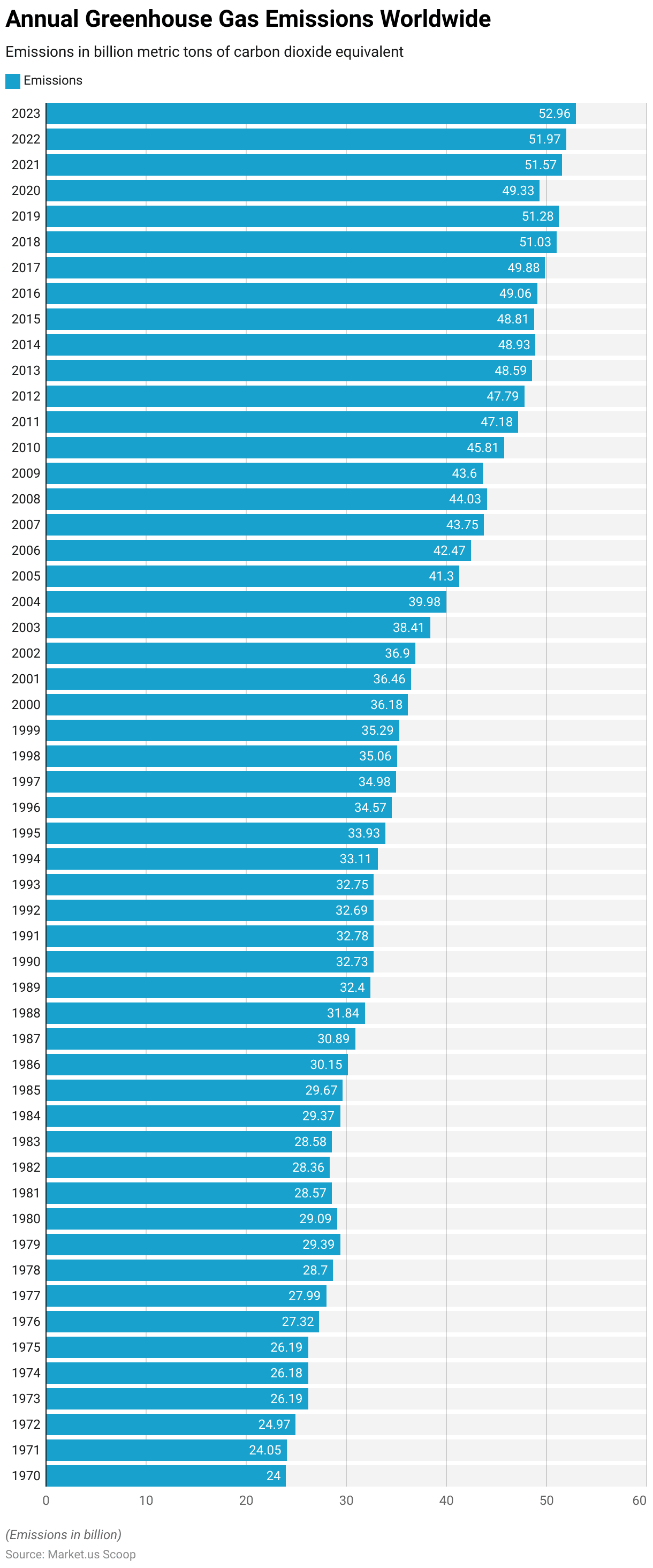

- From 1970 to 2023, global greenhouse gas emissions have steadily increased, reflecting the growing industrialization and population.

- In 1970, emissions were recorded at 24 billion metric tons of CO₂ equivalent.

- This figure rose gradually over the following decades, with emissions reaching 29.39 billion metric tons by 1979.

- The upward trend continued through the 1980s and 1990s, surpassing 32 billion metric tons by 1990 and reaching 34.98 billion metric tons by 1997.

- In the early 2000s, emissions climbed to 36.18 billion metric tons in 2000 and 39.98 billion metric tons by 2004.

- By 2007, emissions peaked at 43.75 billion metric tons, and although there were some fluctuations, the overall growth persisted, reaching 45.81 billion metric tons in 2010.

- In the following decade, emissions continued to rise, reaching 47.18 billion metric tons in 2011 and peaking at 51.28 billion metric tons in 2019.

- The COVID-19 pandemic in 2020 led to a temporary decrease, with emissions dropping to 49.33 billion metric tons.

- However, emissions rebounded in 2021, rising to 51.57 billion metric tons, and further increased to 51.97 billion metric tons in 2022.

- By 2023, global emissions reached 52.96 billion metric tons of CO₂ equivalent, marking the highest level recorded in this period.

- This steady growth highlights the ongoing challenges of mitigating greenhouse gas emissions in the face of expanding global economic activity and energy consumption.

(Source: Statista)

Carbon Emissions Statistics

World’s Biggest CO₂ Emitters

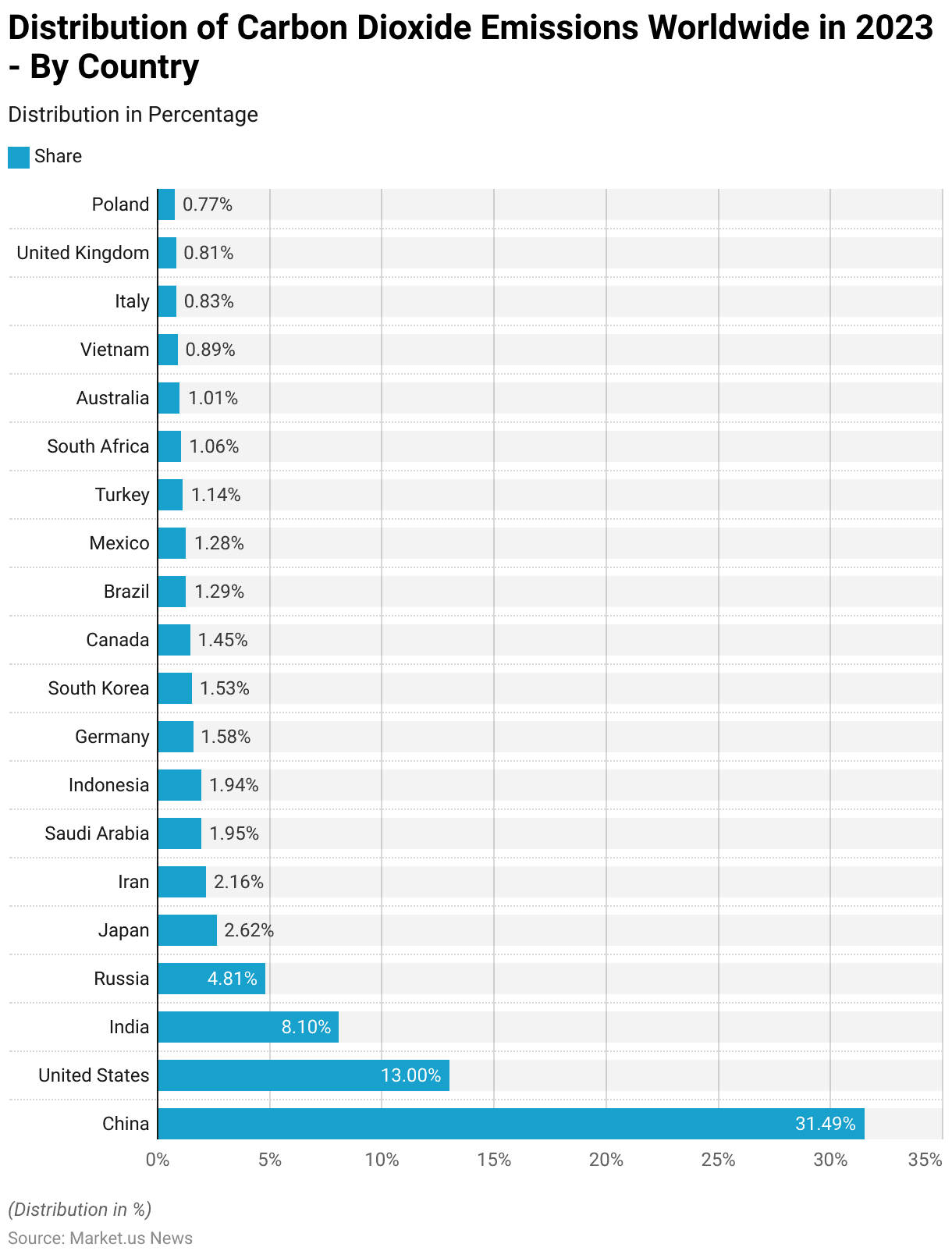

- In 2023, the global distribution of carbon dioxide (CO₂) emissions is dominated by a few key countries.

- China remains the largest emitter, accounting for 31.49% of global CO₂ emissions, followed by the United States with 13%.

- India contributes 8.10% to the global total, while Russia accounts for 4.81%.

- Other significant emitters include Japan (2.62%), Iran (2.16%), and Saudi Arabia (1.95%).

- Indonesia and Germany contribute 1.94% and 1.58%, respectively, while South Korea (1.53%) and Canada (1.45%) also play notable roles in global emissions.

- Additional countries such as Brazil (1.29%), Mexico (1.28%), Turkey (1.14%), and South Africa (1.06%) each account for a smaller yet significant share of global CO₂ emissions.

- Australia, Vietnam, Italy, the United Kingdom, and Poland make up the remaining portions, with shares of 1.01%, 0.89%, 0.83%, 0.81%, and 0.77%, respectively.

- These figures underscore the disproportionate contribution of major industrialized and emerging economies to global CO₂ emissions in 2023.

(Source: Statista)

Global Carbon Dioxide Emissions Per Capita – By Country

- In 2023, countries with the highest per capita carbon dioxide (CO₂) emissions are primarily concentrated in the Middle East and small island nations.

- Qatar leads with an exceptional 42.6 metric tons of CO₂ emissions per capita, followed by Brunei Darussalam at 26.01 metric tons.

- Bahrain and the United Arab Emirates also report high per capita emissions, with 24.59 and 24.1 metric tons, respectively.

- Kuwait and Trinidad and Tobago contribute 23.02 and 22.36 metric tons per capita.

- Saudi Arabia, with 19.93 metric tons, and New Caledonia, with 17.3 metric tons, are also among the top emitters.

- Oman follows closely with 16.9 metric tons per capita, while the Faeroe Islands report 14.97 metric tons.

- Other significant emitters include Australia and the United States, each with per capita emissions of 14.49 and 14.45 metric tons, respectively, and Canada at 14.16 metric tons.

- These figures highlight the disproportionate carbon footprint of smaller, resource-rich nations and industrialized countries in 2023.

(Source: Statista)

Food System Greenhouse Emissions Worldwide

- From 2010 to 2020, global greenhouse gas emissions from the food system have shown a notable increase.

- In 2010, emissions were 18.7 billion metric tons of carbon dioxide equivalent.

- By 2020, this figure had risen to 21.4 billion metric tons.

- Projections indicate a continued upward trajectory, with emissions expected to reach 24.1 billion metric tons by 2030, 26.9 billion metric tons by 2040, and 29.6 billion metric tons by 2050.

- These figures reflect the ongoing growth in emissions from the global food system, driven by factors such as increased demand for food, changes in agricultural practices, and expanding global populations.

(Source: Statista)

Emission Monitoring System (EMS) Market Statistics

Global Emission Monitoring System (EMS) Market Size Statistics

- The global emission monitoring system market is projected to experience steady growth over the next decade at a CAGR of 9.5%.

- Starting at a market size of USD 3.9 billion in 2023, the market is expected to reach USD 4.3 billion in 2024, with a growth trajectory that continues through to USD 4.7 billion in 2025.

- By 2026, the market is forecasted to increase further to USD 5.1 billion, and this upward trend will persist, reaching USD 5.6 billion by 2027.

- The market is anticipated to grow to USD 6.1 billion in 2028, with continued expansion to USD 6.7 billion in 2029.

- Further growth is projected, with the market reaching USD 7.4 billion in 2030, USD 8.1 billion in 2031, and USD 8.8 billion in 2032.

- By 2033, the global emission monitoring system market is expected to attain a size of USD 9.7 billion.

(Source: market.us)

Global Emission Monitoring System (EMS) Market Size – By System Type Statistics

2023-2027

- The global emission monitoring system (EMS) market is expected to witness substantial growth across various system types in the coming years.

- In 2023, the total EMS market was valued at USD 3.9 billion, with Continuous Emission Monitoring Systems (CEMS) accounting for USD 3.17 billion and Predictive Emission Monitoring Systems (PEMS) contributing USD 0.73 billion.

- By 2024, the total market is projected to grow to USD 4.3 billion, with CEMS increasing to USD 3.50 billion and PEMS rising to USD 0.80 billion.

- This trend of growth continues through the forecast period, with the total EMS market reaching USD 4.7 billion in 2025, USD 5.1 billion in 2026, and USD 5.6 billion in 2027.

- CEMS remains the dominant segment, reaching USD 4.55 billion by 2027, while PEMS is expected to grow to USD 1.05 billion by the same year.

2028-2033

- The total EMS market is projected to attain USD 6.1 billion in 2028, USD 6.7 billion in 2029, and USD 7.4 billion by 2030.

- CEMS will continue to drive the majority of the growth, expanding to USD 6.02 billion by 2030, while PEMS will reach USD 1.38 billion.

- By 2031, the EMS market is forecasted to reach USD 8.1 billion, with CEMS at USD 6.59 billion and PEMS at USD 1.51 billion.

- In 2032, the market will grow to USD 8.8 billion, with CEMS valued at USD 7.15 billion and PEMS at USD 1.65 billion.

- By 2033, the EMS market is expected to reach USD 9.7 billion, with CEMS continuing to lead at USD 7.89 billion and PEMS at USD 1.81 billion.

(Source: market.us)

CO₂ Price Trends

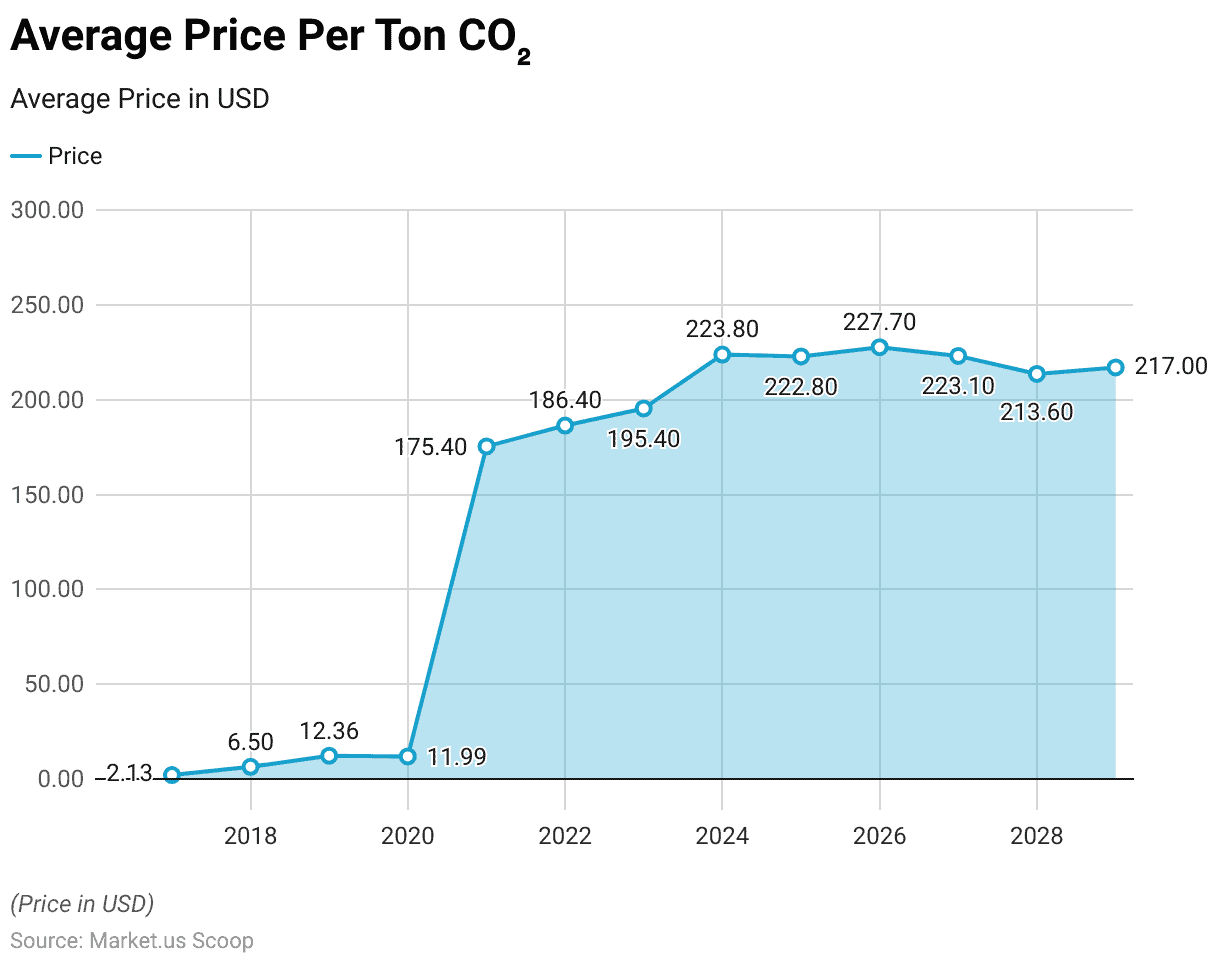

- From 2017 to 2029, the average price per ton of CO₂ has shown significant fluctuations, reflecting market dynamics and policy changes.

- In 2017, the price was relatively low at USD 2.13 per ton.

- However, it began to rise in 2018, reaching USD 6.50, and further increased to USD 12.36 in 2019.

- The price slightly decreased in 2020 to USD 11.99 but saw a dramatic surge in 2021, rising to USD 175.40 per ton.

- This upward trend continued in 2022, with the price reaching USD 186.40, and further increased to USD 195.40 in 2023.

- Projections indicate that the price will continue to rise, reaching USD 223.80 per ton in 2024, followed by a slight decrease to USD 222.80 in 2025.

- In 2026, the price is expected to increase again to USD 227.70 per ton before stabilizing at USD 223.10 in 2027.

- By 2028, the price is anticipated to drop to USD 213.60 per ton, with a slight recovery to USD 217.00 in 2029.

- These fluctuations highlight the evolving nature of carbon pricing, driven by factors such as policy developments, market supply and demand, and environmental regulations.

(Source: Statista)

Installation of Continuous Emission Monitoring Systems (CEMS) in Various Industries Statistics

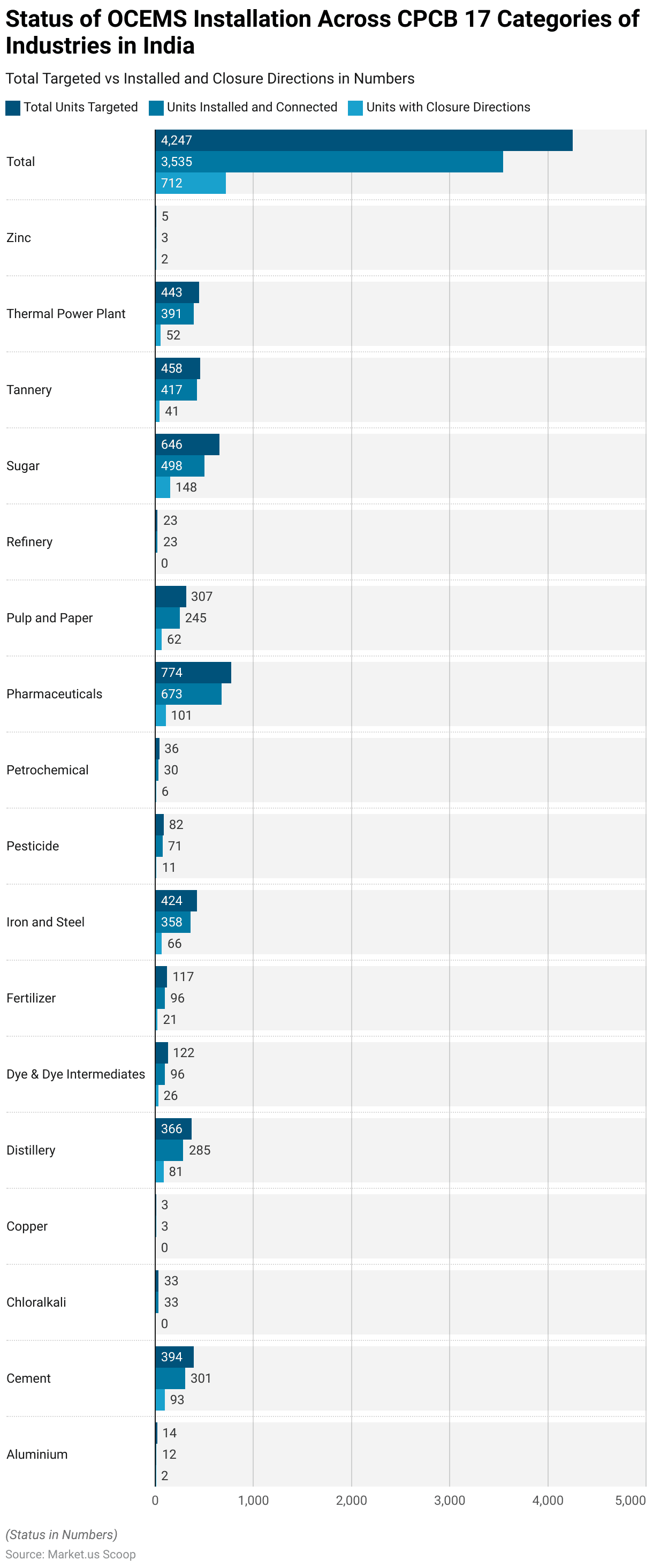

- As of the latest data on the installation of Online Continuous Emission Monitoring Systems (OCEMS) in India, a total of 4,247 units were targeted across 17 key industrial categories under the Central Pollution Control Board (CPCB) guidelines.

- Of these, 3,535 units have been successfully installed and connected, while 712 units have received closure directions due to non-compliance or other regulatory issues.

- In terms of industry-specific performance, sectors such as Chloralkali, Copper, and Refinery have fully installed their targeted units with no closure directions.

- On the other hand, industries like Cement, Distillery, and Sugar have seen significant gaps, with a considerable number of units still pending installation or facing closure directions.

- Notably, the Cement industry has the largest number of targeted units at 394, with 93 units facing closure directions.

- Similarly, the Pharmaceuticals and Iron and Steel sectors have made notable progress, with 673 and 358 units installed, respectively.

- In contrast, industries like Zinc and fertilizers show lower levels of compliance, with fewer units installed compared to targets.

- Overall, while progress has been made in implementing OCEMS across industries, there remain challenges in ensuring full compliance and addressing the closure directions issued by regulatory authorities.

(Source: Uttar Pradesh Climate Change Authority)

Design Specifications of Different Components in Continuous Emission Monitoring System Statistics

Gas Analyzers

- The design specifications for gas analyzers used in Continuous Emission Monitoring (CEM) systems for measuring Sulphur Dioxide (SO₂), Oxides of Nitrogen (NOx), and Carbon Monoxide (CO) are outlined with the following key parameters.

- The lower detection limit for each analyzer is set to be less than 2% of the span, ensuring high sensitivity.

- The interference rejection for all analyzers is required to be within +4% of the span, ensuring minimal cross-sensitivity to other gases.

- The response time for achieving 95% of the final reading is capped at 200 seconds for each gas analyzer.

- The analyzer range is designed to be 1.5 times the approved limit for each gas, providing sufficient capacity for accurate measurements.

- Additionally, the temperature-responsive zero drift must be less than +2% of the span for each analyzer, ensuring stable baseline readings under varying environmental conditions.

- The temperature-responsive span drift is also limited, with a maximum allowable drift of +3% for CO and SO₂ analyzers and +4% for NOx analyzers.

- These specifications ensure the analyzers’ performance remains accurate and reliable across a range of operating conditions.

(Source: Alberta Environmental Protection Environmental Service)

Sulfur Analyzers

- The design specifications for Total Reduced Sulfur (TRS) analyzers include several key performance parameters to ensure accurate and reliable measurements.

- The lower detection limit is specified to be less than 2% of the span, ensuring high sensitivity for detecting low concentrations of sulfur compounds.

- The interference rejection is required to be within +4% of the span, minimizing the impact of potential cross-interference from other gases.

- The response time for reaching 95% of the final reading, as well as the cycle time, is capped at 15 minutes, ensuring timely data collection.

- The analyzer range is set to be 1.5 times the approved limit or 30 parts per million (ppm), whichever is greater, providing sufficient capacity to measure higher concentrations of Total Reduced Sulfur.

- These specifications are designed to ensure the TRS analyzer operates effectively under a range of conditions, providing accurate sulfur measurements for emission monitoring systems.

(Source: Alberta Environmental Protection Environmental Service)

Diluent Monitors

- The design specifications for diluent monitors, specifically for O₂ and CO₂ analyzers, outline key performance parameters to ensure accurate gas measurements.

- For both O₂ and CO₂ analyzers, the lower detection limit is set to be less than 0.5% of the respective gas concentration, providing high sensitivity at low levels.

- Interference rejection for both gases is required to be within +1.0% of the span, ensuring minimal cross-sensitivity from other gases.

- The response time for both analyzers is capped at a maximum of 200 seconds to achieve 95% of the final reading, ensuring timely data acquisition.

- The analyzer range for O₂ is specified as 0 to 21%, while for CO₂, it is 0 to 25%, accommodating typical concentrations found in various monitoring applications.

- Additionally, the temperature-responsive zero drift is limited to less than +0.5% for O₂ and CO₂, ensuring stable baseline readings under varying environmental conditions.

- The temperature-responsive span drift is also constrained to less than +0.5% for both gases, maintaining accuracy across temperature fluctuations.

- These specifications ensure the reliable and precise performance of diluent monitors in emission and air quality monitoring systems.

(Source: Alberta Environmental Protection Environmental Service)

Flow Monitors

- The design specifications for flow monitors focus on ensuring accurate and reliable measurement of flow rates in various systems.

- The lower detection limit is set at 1.0 m/sec, ensuring sensitivity to low-flow conditions.

- The range of the flow monitor is specified to be 1.5 times the expected maximum flow value, providing sufficient capacity for higher flow rates.

- The response time for the monitor to reach 95% of the final reading is capped at a maximum of 10 seconds, ensuring quick and timely data acquisition. The physical design of the flow monitor includes provisions for cleaning the flow element, ensuring long-term accuracy and maintenance ease.

- Additionally, the monitor is designed to prevent interference from moisture, maintaining reliable performance in environments with varying humidity levels.

- These specifications ensure that the flow monitor operates effectively in dynamic conditions, providing precise flow measurements in industrial applications.

(Source: Alberta Environmental Protection Environmental Service)

Temperature Sensors

- The design specifications for temperature sensors focus on ensuring accurate and responsive temperature measurement in various applications.

- The response time for the temperature sensor is set to a maximum of 60 seconds to reach 95% of the final reading, ensuring quick and reliable detection of temperature changes.

- The sensor’s range is designed to be 1.5 times the approved limit, providing sufficient capacity to measure temperatures beyond the typical expected range.

- These specifications ensure that the temperature sensor can operate effectively and provide precise measurements in diverse environments and conditions.

(Source: Alberta Environmental Protection Environmental Service)

Volumetric Flow/Velocity Monitors

- The performance specifications for volumetric flow/velocity monitors are designed to ensure accurate and reliable measurements across a range of flow conditions.

- For velocities greater than three m/sec, the system’s relative accuracy must be within +15% of the reference method, ensuring that the readings are consistent with established measurement standards.

- For velocities below three m/sec, the relative accuracy must be within 0.5 m/sec of the reference method, allowing for precise measurements even at lower flow rates.

- The system’s orientation sensitivity is required to be within +4% of the span, ensuring minimal deviation from accurate readings regardless of the sensor’s orientation.

- In terms of drift, the zero drift over 24 hours must be less than +3% of the span, ensuring stable baseline readings.

- Similarly, the span drift over the same period is limited to less than +3% of the span, maintaining accuracy over time.

- These specifications ensure that volumetric flow and velocity monitors operate effectively, providing precise data for applications in industrial and environmental monitoring.

(Source: Alberta Environmental Protection Environmental Service)

Performance Specifications for Sulphur Dioxide, Oxides of Nitrogen, and Carbon Monoxide Emission Monitoring System Statistics

- The performance specifications for Sulphur Dioxide (SO₂), Oxides of Nitrogen (NOx), and Carbon Monoxide (CO) emission monitoring systems are designed to ensure high accuracy and reliability.

- For all three gases, the analyzer linearity is required to be within +2% of the span from the calibration curve, ensuring precise calibration and measurement across the entire range.

- The relative accuracy for each system must be within +10% of the reference measurement (RM), indicating acceptable deviations from the true values.

- In terms of drift, the zero drift over 24 hours is limited to less than +2% of the span for each system, ensuring stable baseline readings.

- Similarly, the span drift over the same period is restricted to less than +4% of the span for all three gases, minimizing errors in the measurement of gas concentrations over time.

- These specifications are crucial for ensuring that emission monitoring systems provide consistent and accurate data for regulatory compliance and environmental monitoring.

(Source: Alberta Environmental Protection Environmental Service)

Emission Trading System Statistics

Government Income in the Emission Trading System Market

- Government income from the emission trading system (ETS) market has shown significant growth over recent years.

- In 2017, government income was USD 0.11 billion, and it steadily increased to USD 0.44 billion in 2018.

- By 2019, income rose further to USD 0.83 billion, although it slightly declined to USD 0.77 billion in 2020.

- The market saw a dramatic surge in 2021, with government income reaching USD 15.92 billion, followed by USD 16.81 billion in 2022.

- In 2023, government income continued its upward trend, hitting USD 17.7 billion.

- This growth is projected to persist, with expected increases to USD 20.67 billion in 2024, USD 21.49 billion in 2025, and USD 23.32 billion in 2026.

- Although the rate of growth slows slightly, government income is forecasted to stabilize at around USD 23.17 billion in 2027, USD 23.05 billion in 2028, and USD 23.23 billion in 2029, reflecting a steady and sustained upward trajectory over the forecast period.

(Source: Statista)

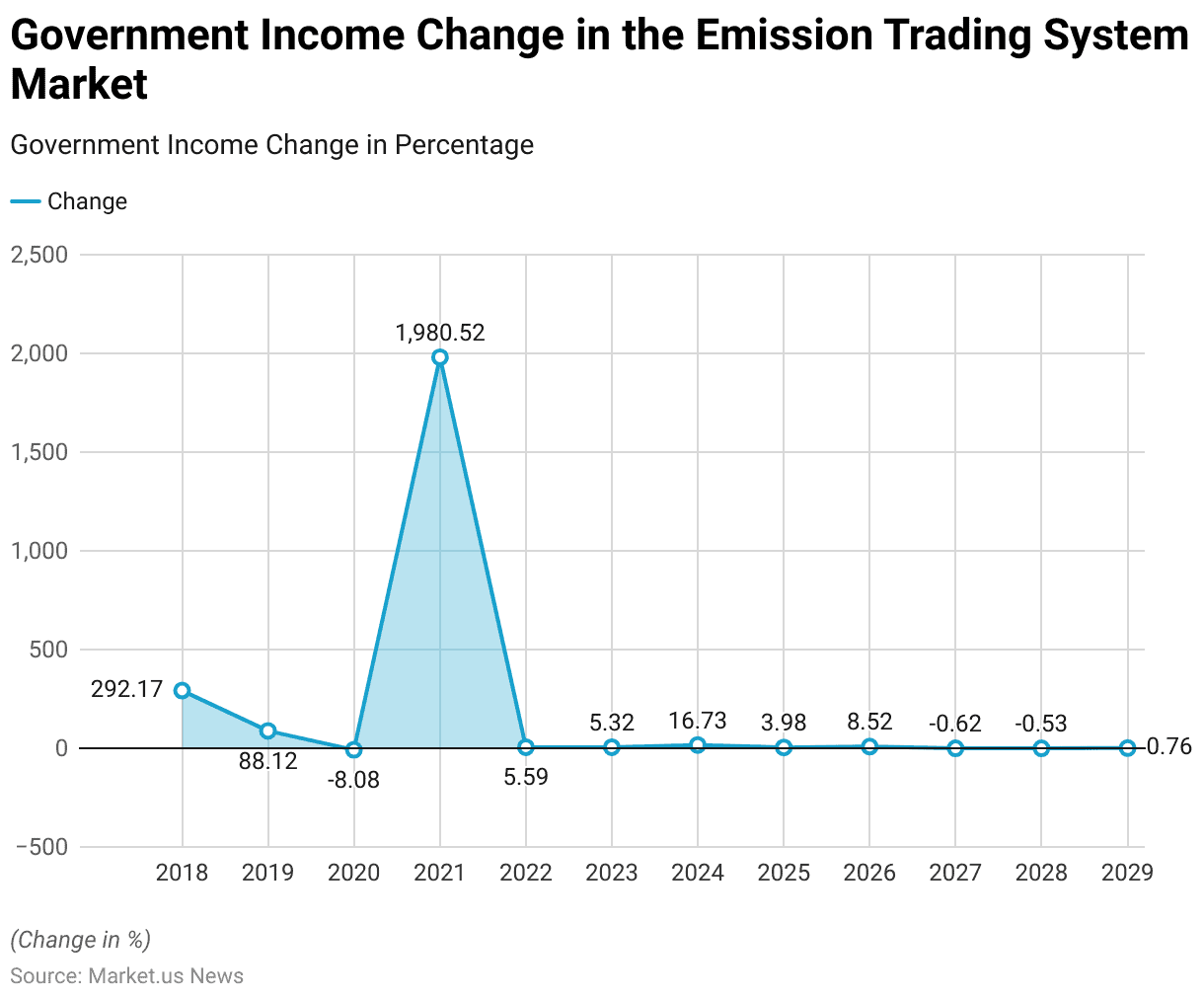

Government Income Change in the Emission Trading System Market

- The change in government income from the emission trading system (ETS) market has experienced substantial fluctuations over the years.

- In 2018, the income change saw a dramatic increase of 292.17%, followed by a continued rise of 88.12% in 2019.

- However, in 2020, there was a slight decline of -8.08%.

- The market then rebounded sharply in 2021, with an extraordinary growth of 1,980.52%. In 2022 and 2023, the growth moderated to 5.59% and 5.32%, respectively.

- Looking ahead, the income change is projected to rise significantly by 16.73% in 2024 before experiencing a more modest increase of 3.98% in 2025.

- Further growth is expected in 2026, with a change of 8.52%.

- However, from 2027 onward, the growth rate is expected to stabilize, with marginal declines of -0.62% in 2027 and –0.53% in 2028, followed by a slight recovery to 0.76% in 2029.

- These trends indicate that while government income from the ETS market will continue to grow, the rate of change may stabilize or experience small fluctuations in the coming years.

(Source: Statista)

By Country Government Income in the Emission Trading System Market

- In the emission trading system (ETS) market, Germany leads with the highest government income, amounting to USD 12,590 million.

- The United Kingdom follows with USD 6,303 million, reflecting its significant participation in the market.

- The United States generates USD 761.6 million, while New Zealand reports a government income of USD 689.6 million.

- South Korea contributes USD 253.7 million to the market.

- These figures highlight the varying levels of government income from the ETS across different countries in 2024, with Germany and the United Kingdom accounting for the largest shares.

(Source: Statista)

CO₂ Emission Trading Contracts

- From 2017 to 2029, the number of CO₂ emission trading contracts has experienced gradual growth, reflecting the expanding global adoption of carbon markets.

- In 2017, there were 53 emission trading contracts, which increased to 68 in 2018.

- The number remained relatively stable in 2019, at 67 contracts, and slightly decreased to 64 in 2020, likely due to the impacts of the COVID-19 pandemic.

- However, the market rebounded in 2021, with the number of contracts rising sharply to 91.

- This upward trend continued through 2022 and 2023, with 90 and 91 contracts, respectively.

- Projections suggest further growth, with the number of contracts expected to increase to 92 in 2024, 96 in 2025, and 102 in 2026.

- By 2027, the number of contracts is forecasted to reach 104, continuing to rise to 108 in 2028 before slightly declining to 107 in 2029.

- This growth reflects the increasing participation in carbon trading schemes as governments and industries seek to meet their climate goals.

(Source: Statista)

Clothing Companies Measuring Their Carbon Footprint

- In 2022, a significant proportion of clothing companies were involved in tracking their carbon footprint, although the level of engagement varied.

- Of the respondents, 19% were actively tracking and utilizing their carbon emissions data in their operations.

- An additional 15% were tracking their carbon footprint but not actively utilizing the data.

- A larger share, 38%, had plans or were in the process of setting up systems to track their carbon emissions.

- Meanwhile, 20% of companies reported that they were not tracking their carbon footprint and had no plans to do so.

- Lastly, 8% of respondents were unsure about their company’s carbon footprint tracking efforts.

- This distribution highlights a growing awareness of environmental impact within the fashion industry, though significant progress is still needed for widespread implementation and active use of carbon tracking data.

(Source: Statista)

Companies Setting and Monitoring GHG Emission Targets

- In 2022, the share of companies setting and monitoring greenhouse gas (GHG) emission targets varied across selected Central and Eastern European countries.

- Hungary led the region, with 53% of firms actively setting and monitoring their GHG emissions targets.

- This was followed by the EU-27 average, where 42% of companies were engaged in such efforts.

- In Poland, 37% of companies reported having GHG emission targets in place, while Slovenia and Czechia both had 34% of firms setting and monitoring their emissions.

- Romania had a slightly lower share at 31%, and Croatia followed closely with 28%.

- Slovakia and Bulgaria had the smallest shares, with 27% and 22% of companies, respectively, setting and monitoring GHG emissions targets.

- These figures reflect varying levels of commitment to environmental sustainability across the region, with Hungary demonstrating the highest engagement in emissions target-setting and monitoring.

(Source: Statista)

Oil and Gas Industry Methane Detection Spending Statistics

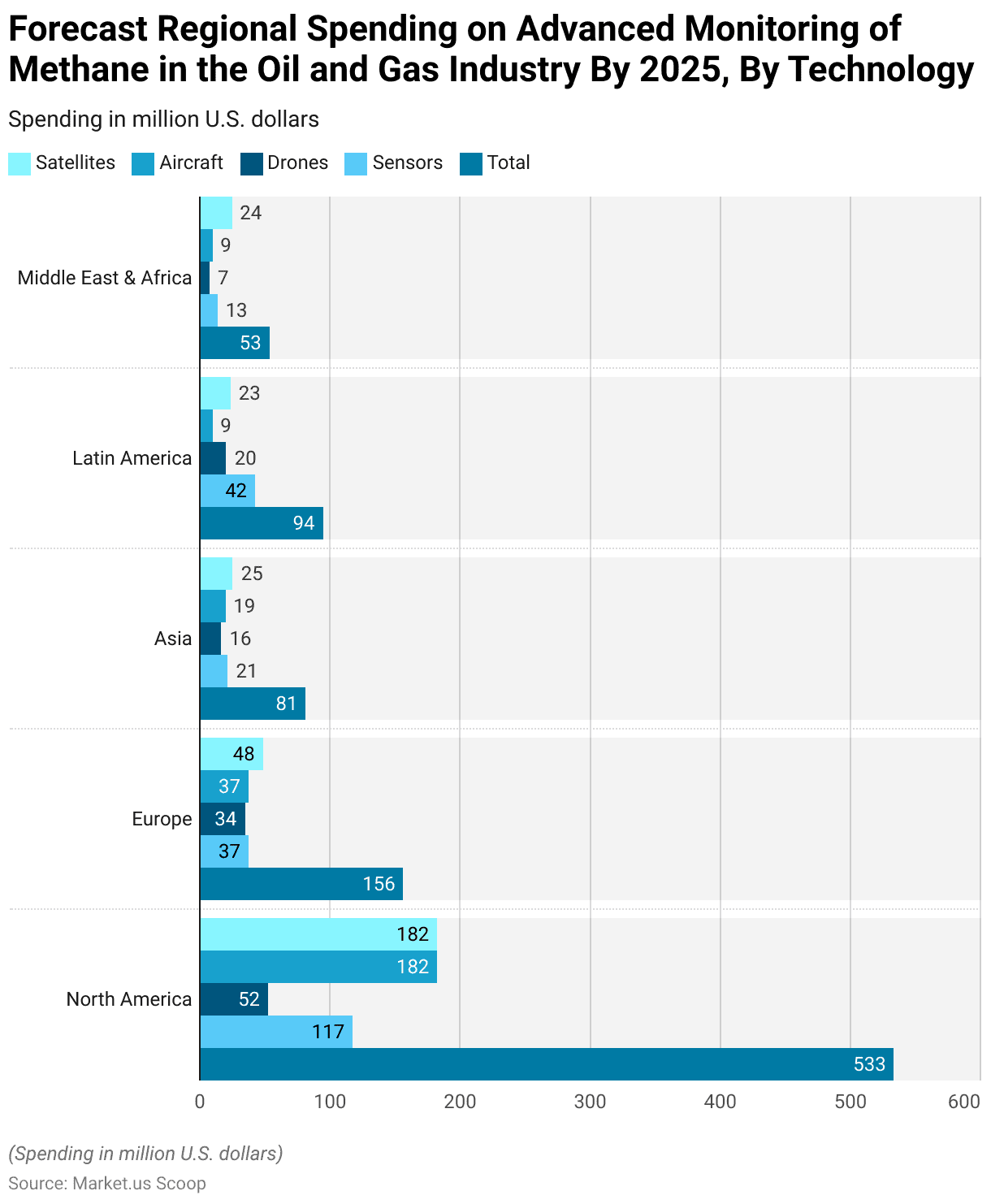

- Forecasted regional spending on advanced methane monitoring technologies in the oil and gas industry by 2025 reveals significant investment across different regions.

- North America is expected to lead, with a total expenditure of USD 533 million, distributed across satellites (USD 182 million), aircraft (USD 182 million), drones (USD 52 million), and sensors (USD 117 million).

- Europe is projected to spend a total of USD 156 million, with satellites accounting for USD 48 million, aircraft for USD 37 million, drones for USD 34 million, and sensors for USD 37 million.

- In Asia, the total spending is forecast to be USD 81 million, with satellites receiving USD 25 million, aircraft USD 19 million, drones USD 16 million, and sensors USD 21 million.

- Latin America is expected to allocate USD 94 million, with significant investment in sensors (USD 42 million), followed by satellites (USD 23 million), drones (USD 20 million), and aircraft (USD 9 million).

- The Middle East & Africa region is projected to spend USD 53 million, with satellites accounting for USD 24 million, aircraft USD 9 million, drones USD 7 million, and sensors USD 13 million.

- This data highlights the varying levels of investment in advanced methane monitoring technologies across different regions, reflecting both regional priorities and the scale of oil and gas operations.

(Source: Statista)

Key Investments

New Investment in Renewable Energy Worldwide

- New investment in renewable energy worldwide has shown consistent growth from 2014 to 2023.

- In 2014, global investments amounted to USD 263 billion, and this figure steadily increased over the following years.

- By 2015, investments rose to USD 293.7 billion, and in 2016, they remained close at USD 290.5 billion.

- The trend continued in 2017 with a rise to USD 317.7 billion, followed by USD 312.5 billion in 2018.

- In 2019, investments reached USD 344.4 billion, and by 2020, they grew further to USD 372 billion.

- The pace of investment accelerated significantly in 2021, reaching USD 459.8 billion, and continued to rise in 2022 with USD 517.7 billion. In 2023, global renewable energy investments peaked at USD 619.1 billion.

- This upward trajectory highlights the increasing global commitment to renewable energy, reflecting growing investments in cleaner, more sustainable energy sources.

(Source: Statista)

Clean Energy Investment – By Region

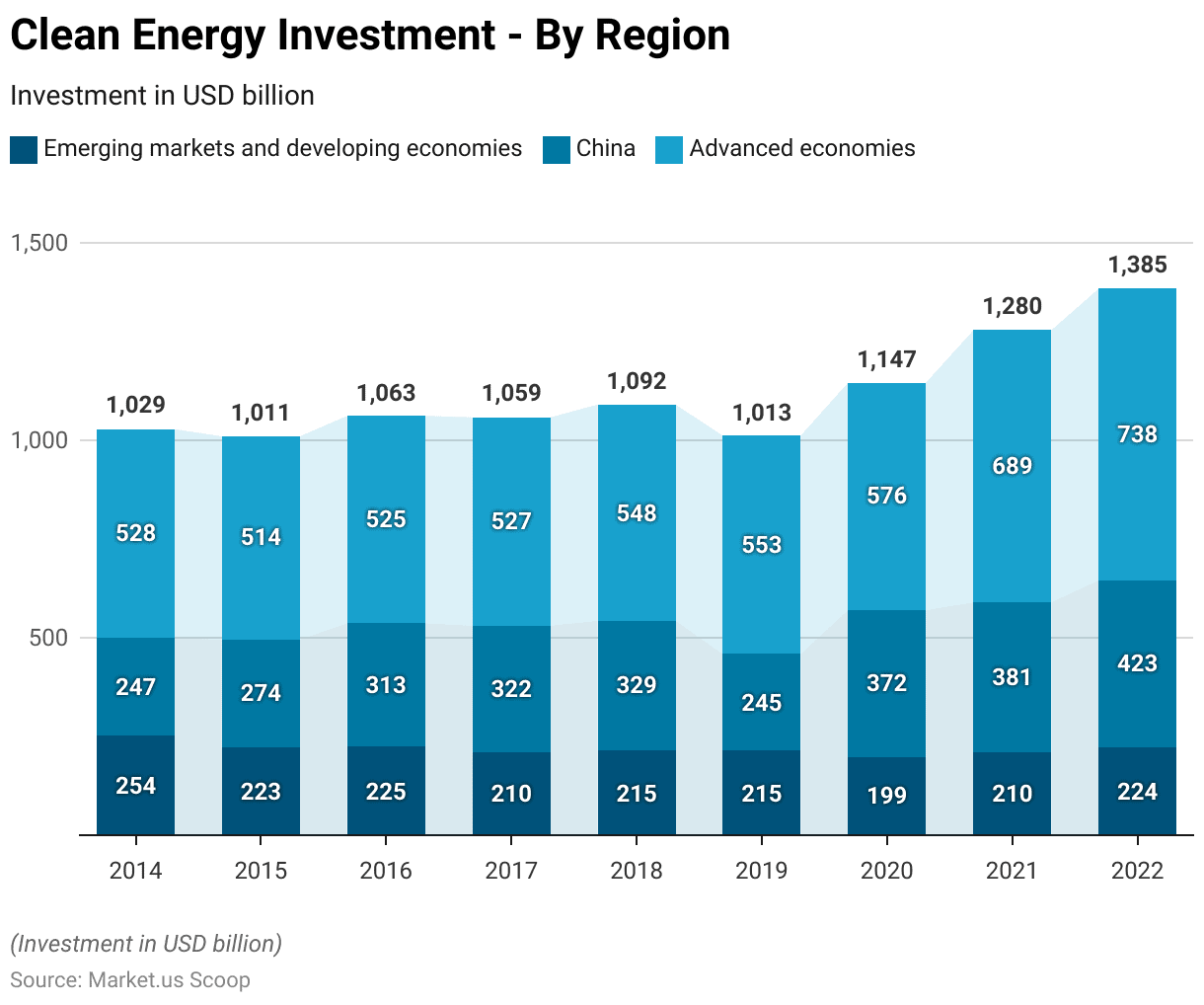

- Clean energy investment by region has varied over the years, with emerging markets, developing economies, China, and advanced economies showing distinct investment patterns from 2014 to 2022.

- In 2014, emerging markets and developing economies saw investments totaling USD 254 billion, while China led with USD 247 billion, and advanced economies accounted for USD 528 billion.

- In 2015, investments in emerging markets dropped to USD 223 billion, while China’s investment increased to USD 274 billion, and advanced economies saw a slight decline to USD 514 billion.

- Throughout the following years, investments continued to fluctuate. In 2016, emerging markets and developing economies invested USD 225 billion, China’s investments grew to USD 313 billion, and advanced economies remained stable at USD 525 billion.

- By 2017, emerging markets saw a decline to USD 210 billion, while China’s investment rose to USD 322 billion, and advanced economies remained strong at USD 527 billion.

Moreover

- In 2018, the trend continued with USD 215 billion in emerging markets, USD 329 billion in China, and USD 548 billion in advanced economies.

- In 2019, emerging markets maintained USD 215 billion, while China’s investment fell to USD 245 billion, and advanced economies increased their investments to USD 553 billion.

- In 2020, a significant shift occurred, with emerging markets investing USD 199 billion, China increasing its share to USD 372 billion, and advanced economies rising to USD 576 billion.

- The trend of growth continued into 2021, with emerging markets and developing economies investing USD 210 billion, China reaching USD 381 billion, and advanced economies investing a record USD 689 billion.

- Finally, in 2022, investment in clean energy reached USD 224 billion in emerging markets, USD 423 billion in China, and USD 738 billion in advanced economies, indicating a continued commitment to clean energy development across all regions.

(Source: International Energy Agency (IEA))

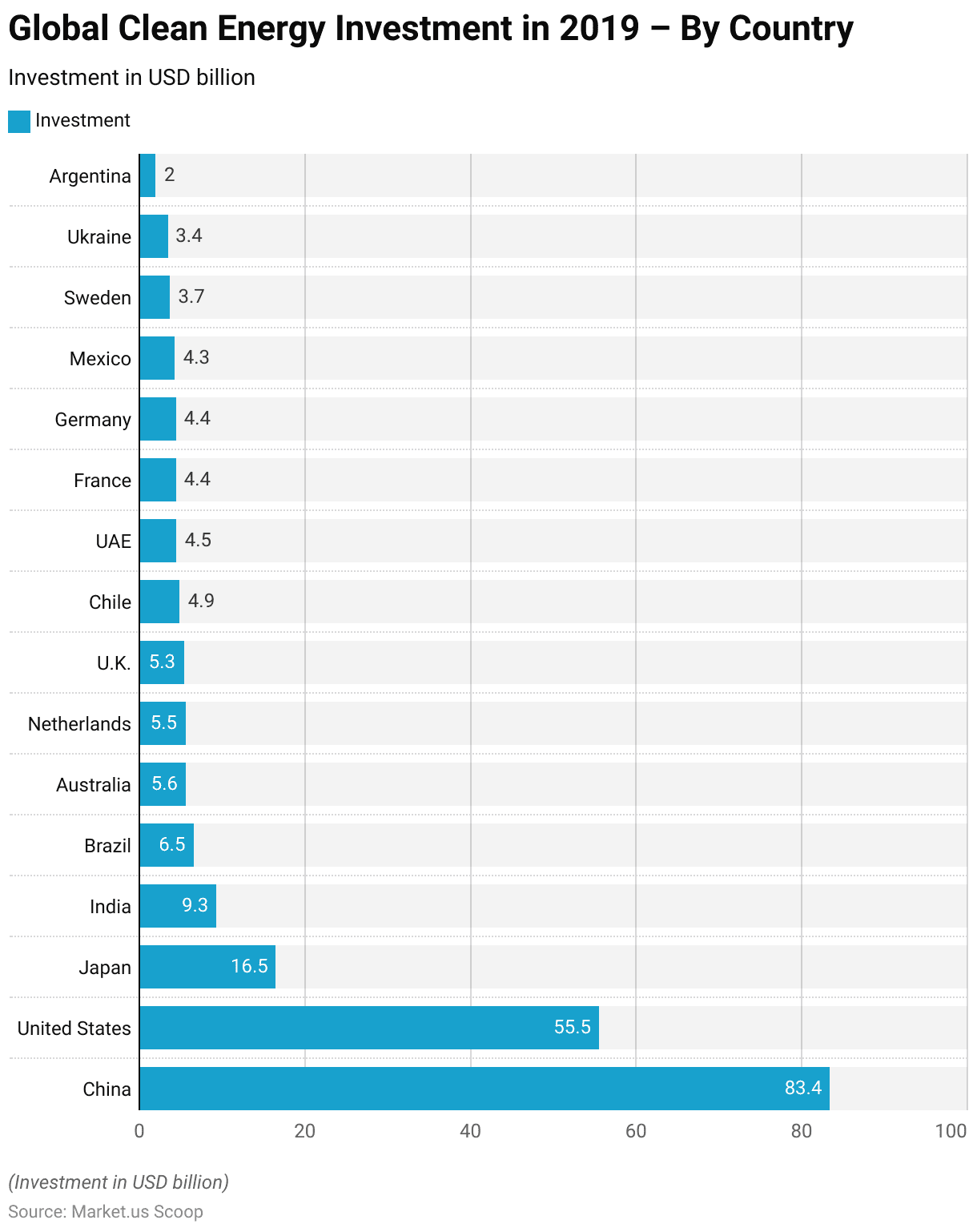

Global Clean Energy Investment – Country

- In 2019, global investment in clean energy was distributed across several key countries, with China leading the way.

- China invested USD 83.4 billion, representing the largest share of global clean energy investment.

- The United States followed with USD 55.5 billion, while Japan invested USD 16.5 billion.

- India also made significant investments, totaling USD 9.3 billion, followed by Brazil with USD 6.5 billion.

- Other notable contributors included Australia with USD 5.6 billion, the Netherlands at USD 5.5 billion, and the United Kingdom with USD 5.3 billion.

- Chile invested USD 4.9 billion, and the UAE contributed USD 4.5 billion.

- France and Germany each invested USD 4.4 billion, while Mexico invested USD 4.3 billion.

- Sweden and Ukraine made investments of USD 3.7 billion and USD 3.4 billion, respectively, and Argentina invested USD 2 billion.

- This distribution of investments highlights the global push for clean energy development, with significant contributions from both developed and emerging economies.

(Source: Statista)

Investment Opportunities Across Key Sectors for Green Recovery – By Region

- Between 2020 and 2030, emerging markets are expected to offer significant green investment opportunities across key sectors, totaling USD 10.2 trillion.

- The largest share of this investment is anticipated to come from East Asia and the Pacific, accounting for USD 5.1 trillion.

- South Asia is projected to attract USD 2.8 trillion in green investments, while Latin America and the Caribbean are expected to contribute USD 1.3 trillion.

- Europe, though smaller in comparison, is still forecast to see USD 0.6 trillion in green investments during the period.

- Sub-Saharan Africa is expected to attract USD 0.3 trillion, and the Middle East and North Africa region is forecast to secure USD 0.2 trillion.

- Further, these figures highlight the growing importance of emerging markets in driving global green investments, with significant contributions from regions like East Asia and South Asia, which are leading the transition to sustainable development.

(Source: Statista)

Gains from Environmental Investment for Small and Medium Enterprises Worldwide

- In 2021, small and medium enterprises (SMEs) worldwide reported various gains from environmental investments.

- The most significant benefit was an increase in product quality, with 19% of companies citing this as a key outcome.

- Access to new markets followed closely, with 17.3% of SMEs highlighting this advantage.

- Additionally, 16.6% of companies experienced increased production as a result of their environmental investments.

- Other opportunities, including improvements in operational efficiency or sustainability practices, were reported by 14% of SMEs.

- Lower input costs were a gain for 10% of businesses, while 7% of companies introduced new products or services as part of their green initiatives.

- Moreover, these findings underscore the diverse and tangible benefits that environmental investments can bring to SMEs, driving both operational improvements and new growth opportunities.

(Source: Statista)

Regulations for Emission Monitoring Systems

- Regulations for emission monitoring systems vary widely by country and are designed to control and reduce harmful emissions from various sources, especially vehicles and industrial processes.

- In the United States, the Environmental Protection Agency (EPA) mandates continuous emission monitoring systems (CEMS) under various regulations, which include performance specifications for evaluating system acceptability at installation and ongoing quality assurance procedures to ensure data integrity for compliance purposes.

- The European Union enforces stringent Euro standards, progressively tightening restrictions on carbon dioxide and nitrogen oxide emissions, influencing global automotive and industrial practices.

- In contrast, emerging economies like Vietnam and Indonesia are developing their regulations, aiming to align with international standards while considering local economic factors.

- Similarly, Australia emphasizes a blend of regulatory mandates and voluntary compliance, promoting a shift toward lower-emission technologies through its Clean Fuel Standard.

- Moreover, updated regulations in the United States aim to substantially reduce greenhouse gases and other pollutants through new vehicle emission standards, offering significant public health benefits and cost savings through improved fuel efficiencies.

- Further, these examples underscore a global trend towards stricter emission standards, with each country tailoring its approach to local needs and technological capabilities, all contributing to a global reduction in environmental pollutants.

(Source: IEA, US EPA, The Insurance Universe)

Recent Developments

Acquisitions and Mergers:

- Emerson Acquires GE Digital’s Gas Turbine Business: In 2023, Emerson Electric Co. completed the acquisition of GE Digital’s gas turbine business for $5 billion. This acquisition strengthens Emerson’s capabilities in industrial automation, including advanced emission monitoring solutions, expanding its market share in environmental monitoring technologies.

- Envirosuite and SafeBridge Merger: In 2023, Envirosuite merged with SafeBridge, expanding its environmental monitoring product suite to include enhanced emission monitoring systems. The merger increases its footprint in global markets, particularly in the mining, oil & gas, and power sectors.

Product Launches

- Horiba’s New Emission Analyzer for Real-Time Monitoring: Horiba launched a new emission analyzer in 2023, designed to provide real-time data on industrial emissions, especially in large-scale power plants and chemical processing facilities. The system promises to improve compliance rates and reduce emissions by 15-20%, contributing to better regulatory adherence and cost savings.

- Thermo Fisher Scientific’s Portable Emission Monitors: In 2023, Thermo Fisher launched a new series of portable emission monitors for field use. These devices are able to detect multiple types of pollutants with high sensitivity, providing industries like manufacturing and energy with precise emission data for compliance and operational efficiency.

Funding and Investments:

- Envirosuite Raises $40 Million in Series C: In 2023, Envirosuite secured $40 million in Series C funding to accelerate the development of its environmental and emissions monitoring platforms. The company plans to use this funding to expand its footprint in North America and Europe, focusing on technology innovations that increase real-time monitoring capabilities.

- Siemens Secures $75 Million for Green Tech Initiatives: Siemens raised $75 million in funding in 2023 to further its green technology initiatives, including emission monitoring systems. This capital will support the development of next-generation sensors for detecting real-time CO2 emissions, enhancing Siemens’ leadership position in industrial environmental monitoring.

Regulatory Developments:

- EU Strengthens Emission Monitoring Requirements: In 2023, the European Union introduced stricter regulations requiring all large industrial plants to implement continuous emissions monitoring systems by 2025. This regulation is expected to drive an 18% increase in the EMS market over the next five years, as companies rush to comply with the new requirements.

- U.S. EPA Expands Emission Reporting to Small Factories: The U.S. Environmental Protection Agency (EPA) introduced new rules in 2023, expanding emission reporting requirements to include small and mid-sized manufacturing facilities. This regulation is anticipated to increase the adoption of affordable emission monitoring systems across a broader range of industries, driving market growth by 12-15% over the next few years.

Conclusion

Emission Monitoring System Statistics: In conclusion, emission monitoring systems (EMS) are essential for ensuring regulatory compliance and reducing industrial impact on air quality.

With advanced technologies such as gas analyzers and remote sensing tools like satellites and drones, these systems provide accurate, real-time data for tracking emissions.

As environmental regulations tighten and green investments rise, the demand for reliable EMS is growing, offering industries the opportunity to improve sustainability.

These systems are key to meeting regulatory standards and supporting global environmental goals, with continuous innovations ensuring more effective and efficient emissions management.

FAQs

What is an Emission Monitoring System (EMS)?

An Emission Monitoring System (EMS) is a set of instruments and technologies used to measure and monitor the release of gases and pollutants from industrial processes into the atmosphere. EMS typically includes gas analyzers, sensors, and software to track emissions in real-time, ensuring compliance with environmental regulations.

Why are Emission Monitoring Systems important?

EMS is crucial for tracking emissions of harmful substances such as sulfur dioxide (SO₂), nitrogen oxides (NOₓ), carbon monoxide (CO), and particulate matter. They help industries meet regulatory standards, improve air quality, and reduce their environmental impact, thus supporting sustainability goals and minimizing fines for non-compliance.

How do Emission Monitoring Systems work?

EMS measures the concentration of gases in exhaust emissions using various technologies like infrared absorption, chemiluminescence, and electrochemical detection. The data is then transmitted to a central system for analysis and reporting, which is essential for compliance with environmental regulations and monitoring performance over time.

What types of gases can Emission Monitoring Systems detect?

EMS can monitor a wide range of gases, including sulfur dioxide (SO₂), nitrogen oxides (NOₓ), carbon monoxide (CO), methane (CH₄), ozone (O₃), and particulate matter (PM). Advanced systems can also measure volatile organic compounds (VOCs) and other hazardous air pollutants (HAPs).

What industries use Emission Monitoring Systems?

EMS is used across various industries, including power generation, cement, chemical manufacturing, petrochemicals, refining, steel production, and transportation. Any industry that produces gaseous emissions is likely to require EMS for regulatory compliance.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)