Introduction

Power Purchase Agreement Statistics: A Power Purchase Agreement (PPA) is a contract between a power producer (the seller) and a purchaser (the buyer) outlining the terms for the sale and purchase of electricity over a set period.

It includes key details such as the price of electricity (fixed, variable, or mixed), the quantity to be delivered, and the duration of the agreement, typically ranging from 10 to 30 years.

PPAs provide price certainty for both parties and are commonly used in renewable energy projects to ensure long-term financial stability.

Editor’s Choice

- By 2033, the Global Power Purchase Agreement Market is projected to reach USD 444.3 billion, highlighting strong and sustained growth.

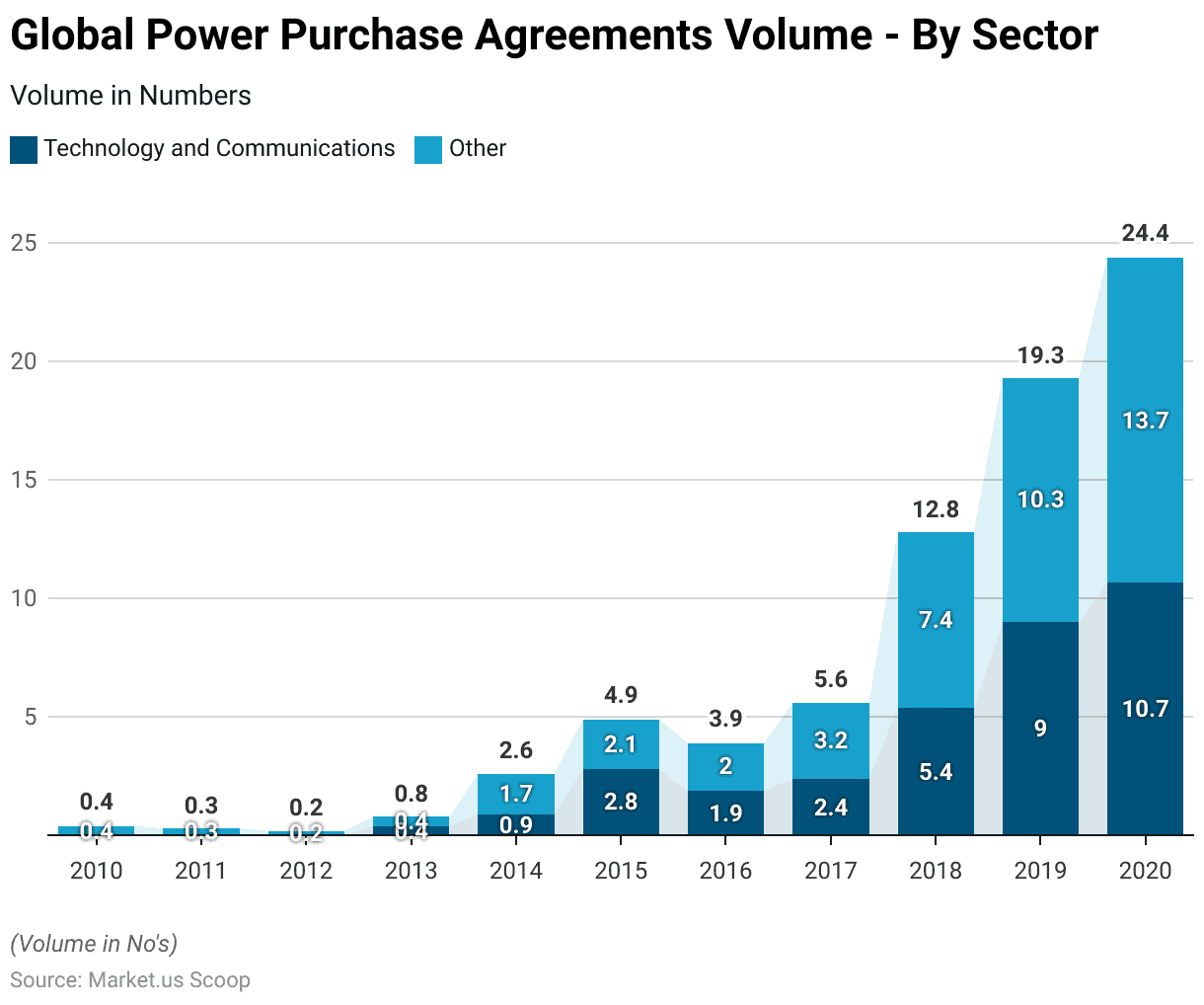

- By 2020, Technology and Communications peaked at 10.7 GW, while the Other sector reached 13.7 GW, reflecting rising corporate interest in renewable energy.

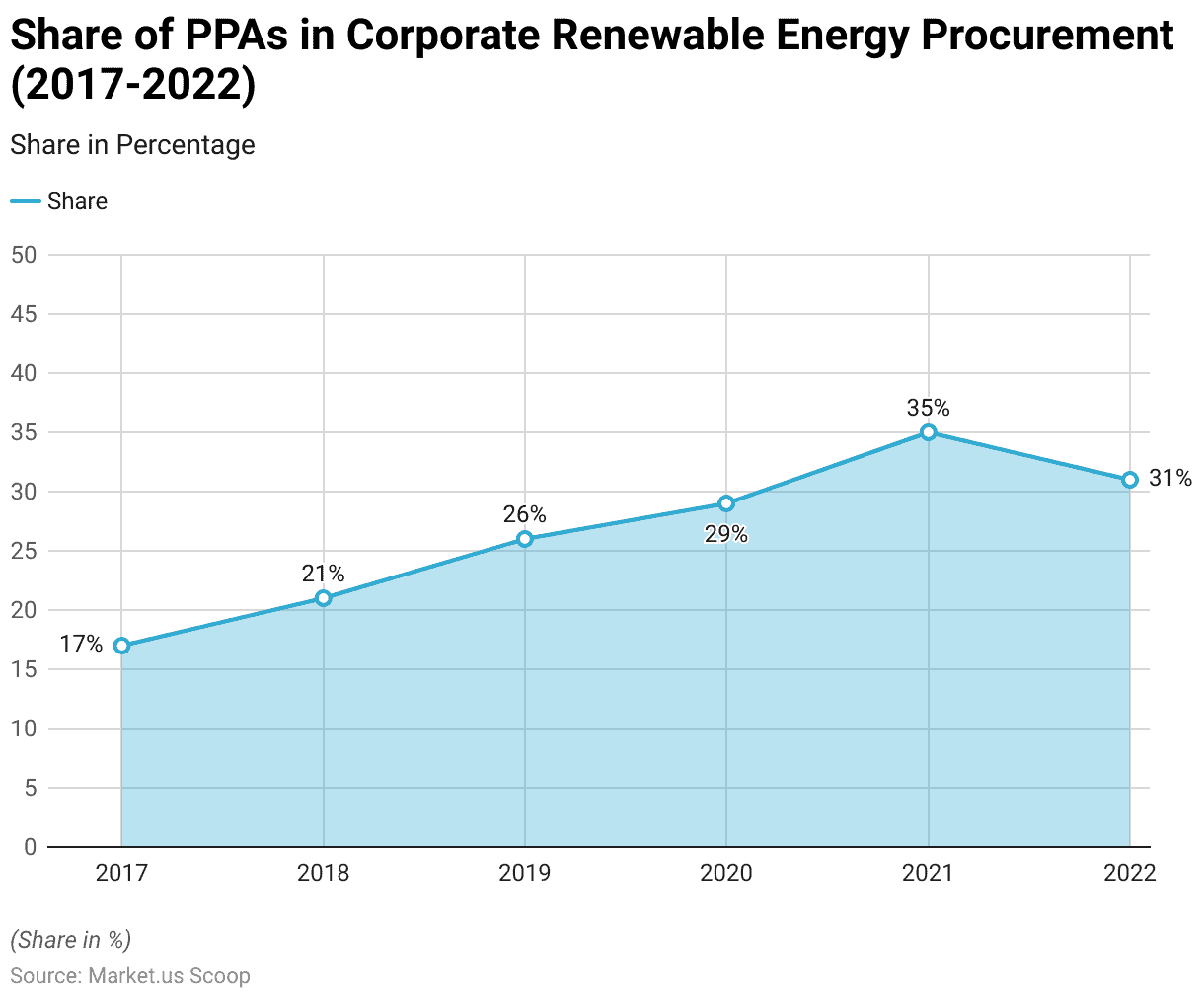

- In 2021, 35% of companies utilized PPAs for renewable energy procurement, demonstrating a strong commitment to clean energy initiatives.

- In 2023, the contracted renewable capacity peaked at 46 GW, underscoring the increasing corporate commitment to renewable energy adoption.

- As of May 2024, Amazon leads globally in cumulative renewable capacity contracted through corporate power purchase agreements (PPAs) with 34 gigawatts (GW), demonstrating its prominent role in advancing renewable energy adoption.

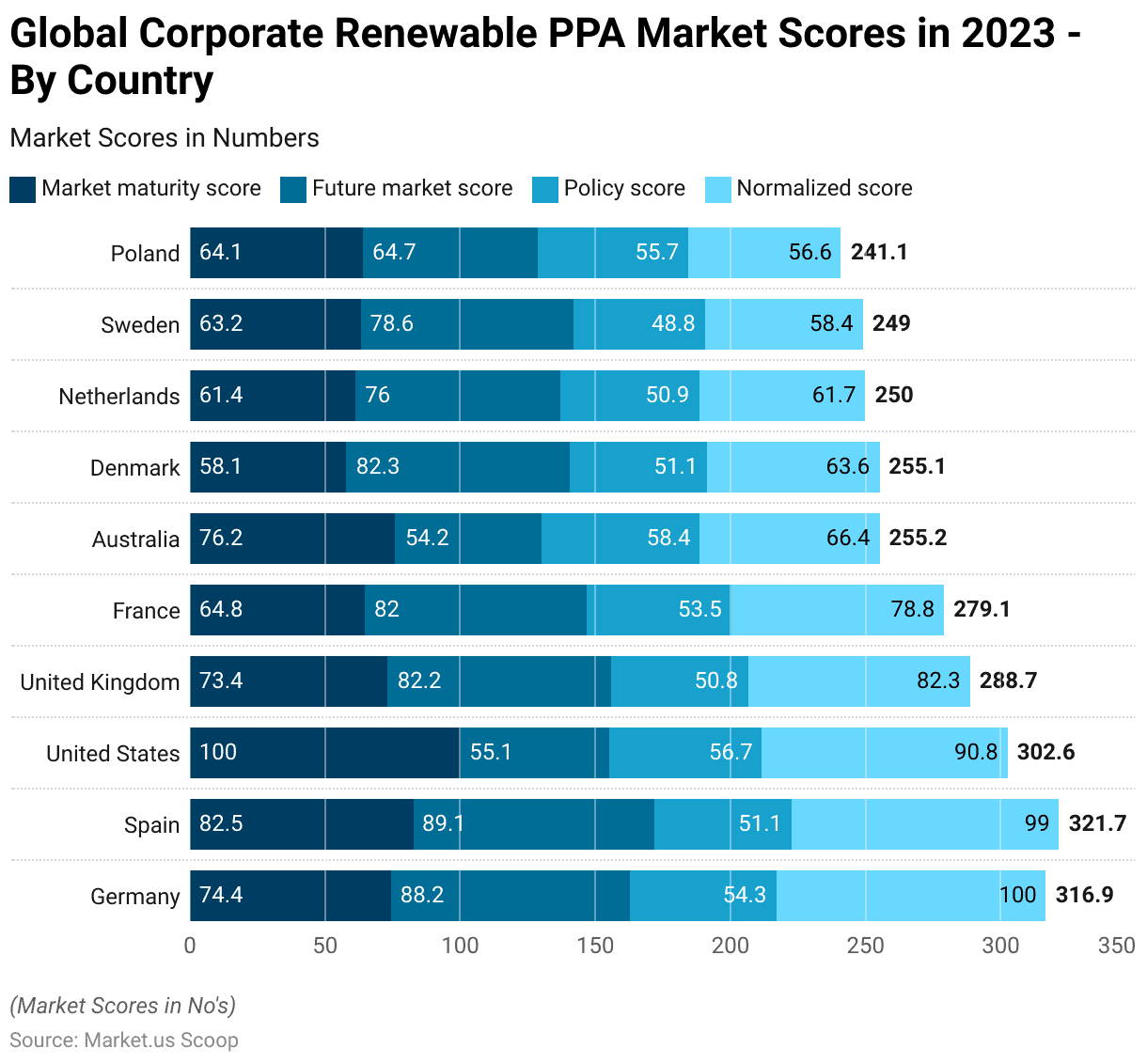

- As of November 2023, Germany led the global renewable corporate PPA market with a normalized score of 100, supported by a market maturity score of 74.4, a future market score of 88.2, and a policy score of 54.3.

- In the European Union, the 2023 reforms proposed by the European Commission aim to stabilize the electricity market by promoting long-term contracts like PPAs, enhancing industry competitiveness, and reducing exposure to volatile energy prices.

Global Power Supply Market Value

- Between 2021 and 2028, the global power supply sector is expected to experience steady growth, highlighting the increasing demand for reliable energy solutions worldwide.

- In 2021, the market value stood at USD 10.24 billion, which rose to USD 10.74 billion in 2022 and further increased to USD 11.29 billion in 2023.

- The upward trend is projected to continue, reaching USD 11.76 billion in 2024 and USD 12.22 billion in 2025.

- By 2026, the market value is expected to grow to USD 12.84 billion, followed by USD 13.48 billion in 2027.

- The forecast indicates a significant rise to USD 14.23 billion by 2028.

- This consistent growth reflects global investments in energy infrastructure, increasing adoption of renewable power sources, and rising demand for efficient energy systems.

- The figures underscore the sector’s critical role in supporting industrial, commercial, and residential energy needs alongside advancing technological solutions for power generation and distribution.

(Source: Statista)

Power Purchase Agreement Market Size Statistics

- The Global Power Purchase Agreement (PPA) Market is projected to experience significant growth over the next decade at a CAGR of 31.7%.

- In 2023, the market size stood at USD 28.3 billion, and it is expected to increase to USD 37.3 billion in 2024.

- By 2025, the market is estimated to reach USD 49.1 billion, and this upward trend continues into 2026 at USD 64.6 billion.

- The market is anticipated to grow further to USD 85.1 billion in 2027, followed by a substantial rise to USD 112.1 billion in 2028.

- In 2029, the market size is projected to hit USD 147.7 billion, while by 2030, it is expected to cross the USD 194.5 billion mark.

- This growth momentum accelerates into the next decade, with the market expanding to USD 256.1 billion by 2031 and USD 337.3 billion in 2032.

- By 2033, the Global Power Purchase Agreement Market is forecasted to reach an impressive USD 444.3 billion, underscoring robust and sustained market expansion.

(Source: market.us)

Power Purchase Agreement Volume Statistics

- From 2010 to 2020, global power purchase agreements (PPAs) volumes by sector, specifically Technology and Communications and Other industries, exhibited significant growth.

- In 2010, only the Other sector recorded a small volume of 0.4 GW, which decreased slightly to 0.3 GW in 2011 and further to 0.2 GW in 2012.

- By 2013, both sectors began reporting activity, with Technology and Communications contributing 0.4 GW and the Other sector maintaining 0.4 GW.

- The trend accelerated in 2014, with Technology and Communications rising to 0.9 GW and the Other sector increasing to 1.7 GW.

- In 2015, the Technology and Communications sector reached 2.8 GW, while the Other sector climbed to 2.1 GW.

- By 2016, volumes slightly dropped in Technology and Communications to 1.9 GW, with the Other sector reaching 2 GW.

- Growth resumed in 2017, with 2.4 GW for Technology and Communications and 3.2 GW for Other.

- In 2018, significant expansion was observed, as Technology and Communications surged to 5.4 GW and Other industries reached 7.4 GW.

- This upward momentum continued into 2019, where Technology and Communications recorded 9 GW, and the Other sector reported 10.3 GW.

- By 2020, both sectors achieved their peak values in this period, with Technology and Communications contributing 10.7 GW and the Other sector reaching 13.7 GW, reflecting the growing corporate interest in renewable energy procurement.

(Source: International Energy Agency)

- The share of corporate renewable energy procurement through power purchase agreements (PPAs) worldwide has shown a steady upward trend between 2017 and 2022, with slight fluctuations in recent years.

- In 2017, only 17% of companies adopted PPAs as a means of securing renewable energy. This share increased to 21% in 2018 and continued to rise to 26% in 2019.

- By 2020, the adoption rate had grown further to 29%, reflecting the increasing corporate focus on sustainability goals.

- The peak was reached in 2021, when 35% of companies utilized PPAs for renewable energy procurement, demonstrating a strong commitment to clean energy initiatives.

- However, in 2022, the share declined slightly to 31%, signaling a potential stabilization or slight shift in procurement strategies.

- Despite this drop, the overall trend remains positive, highlighting the significant role PPAs play in advancing corporate renewable energy targets.

(Source: Statista)

Global Renewable PPA Contracted Capacity Statistics

Global Renewable PPA Contracted Capacity

- The renewable capacity contracted through corporate power purchase agreements (PPAs) worldwide has seen remarkable growth from 2012 to 2023, indicating a strong global shift towards sustainable energy procurement.

- In 2012, the contracted capacity was 0.3 gigawatts (GW), which grew steadily to 1 GW in 2013 and 2.3 GW in 2014.

- By 2015, the figure doubled to 4.7 GW, followed by a slight decline to 4.1 GW in 2016.

- The upward trend resumed in 2017, reaching 6.5 GW, and saw a significant jump to 14.1 GW in 2018.

- This growth accelerated in 2019, with contracted capacity reaching 20.6 GW, followed by 25.6 GW in 2020.

- The market maintained its momentum, recording 31 GW in 2021 and achieving a notable surge to 41 GW in 2022.

- By 2023, the contracted renewable capacity peaked at 46 GW, underscoring the increasing corporate commitment to renewable energy adoption.

(Source: Statista)

Renewable PPA Contracted Capacity Globally – By Region

- The contracted renewable capacity through corporate power purchase agreements (PPAs) worldwide demonstrated regional variations from 2020 to 2023 across the Americas, Europe, the Middle East, and Africa (EMEA), and the Asia Pacific.

- In 2020, the Americas led with 15.4 GW, followed by EMEA at 7.3 GW and the Asia Pacific at 2.9 GW.

- The upward trend continued in 2021, where the Americas increased to 20.4 GW, EMEA reached 8.4 GW, while the Asia Pacific experienced a decline to 2.2 GW.

- In 2022, the Americas remained dominant at 24.1 GW, EMEA recorded a slight growth to 8.8 GW, and the Asia Pacific made a notable recovery to 7.7 GW.

- By 2023, the Americas contracted 20.9 GW, while EMEA surged significantly to 15.4 GW, reflecting growing adoption in the region.

- The Asia Pacific also expanded further, reaching 9.7 GW.

- These trends highlight the regional momentum in renewable energy adoption, with EMEA and Asia Pacific catching up to the Americas’ established dominance.

(Source: Statista)

Renewable PPA Contracted Capacity – By Technology

- As of the end of 2023, the corporate renewable power purchase agreements (PPAs) contracted capacity across European countries showcased diverse adoption by technology, including wind, solar, and renewable portfolios.

- Spain led with the highest total contracted capacity of 8 GW, including 5 GW from solar, 1.7 GW from wind, and smaller contributions from wind and solar combined (0.9 GW) and renewables portfolio (0.4 GW).

- Germany followed with 4.7 GW, driven by 2.9 GW of wind, 1.5 GW of solar, and 0.2 GW from wind and solar combined.

- Sweden recorded a total of 4.1 GW, primarily led by 3.6 GW of wind.

- The United Kingdom reported 2.7 GW, including 1.5 GW of wind, 1 GW of solar, and minor contributions from other sources.

- Norway solely relied on the wind, contributing 2.5 GW.

- France achieved 2.4 GW, with 1.8 GW from solar, 0.2 GW from wind, and a 0.1 GW wind-solar combination.

- Both the Netherlands and Finland recorded 2.1 GW of total capacity, primarily from wind.

- Ireland reached 1.8 GW, including 0.9 GW from wind and solar combined.

- Poland and Denmark each reported 1.4 GW, with Poland’s contributions balanced between solar and wind, while Denmark relied on 1.2 GW of solar.

- Italy registered 0.9 GW, and smaller capacities were observed in Belgium at 0.7 GW and Greece at 0.6 GW.

(Source: Statista)

Global Cumulative Renewable PPA Capacity – By Company

- As of May 2024, Amazon leads globally in cumulative renewable capacity contracted through corporate power purchase agreements (PPAs) with 34 gigawatts (GW), demonstrating its prominent role in advancing renewable energy adoption.

- Microsoft follows with a significant 23.2 GW, while Meta holds the third position with 14.4 GW.

- Google secured 11.1 GW, highlighting its strong efforts toward sustainability.

- Other key contributors include TotalEnergies with 4.4 GW, AT&T with 3.1 GW, and McDonald’s at 2.8 GW.

- Verizon and Rio Tinto each contributed 2.4 GW, while Norsk Hydro recorded 2.1 GW.

- This data underscores the increasing commitment of major corporations to drive renewable energy growth through PPAs.

(Source: Statista)

Corporate Renewable PPA Contracted Capacity – By Power Market

- In the United States, corporate renewable capacity contracted through power purchase agreements (PPAs) varied across electricity system operators between 2022 and 2023.

- ERCOT (Electric Reliability Council of Texas) led in both years, increasing its contracted capacity from 6.9 GW in 2022 to 7.3 GW in 2023.

- PJM saw significant growth, rising from just 0.3 GW in 2022 to 2.3 GW in 2023.

- Conversely, MISO (Midcontinent Independent System Operator) experienced a decline, dropping from 4 GW in 2022 to 2.2 GW in 2023.

- CAISO (California Independent System Operator) also reported a reduction, with capacity falling from 1.2 GW in 2022 to 0.7 GW in 2023.

- Other operators collectively saw a notable decrease from 5 GW in 2022 to 2.8 GW in 2023.

- These trends highlight a shifting landscape in regional renewable energy procurement across the United States.

(Source: Statista)

Global Corporate Renewable PPA Market Scores Statistics

Global Corporate Renewable PPA Market Scores – By Country

- As of November 2023, the leading markets for renewable corporate power purchase agreements (PPAs) worldwide were evaluated based on market maturity score, future market score, policy score, and a normalized score.

- Germany emerged as the top market with a normalized score of 100, supported by a market maturity score of 74.4, a future market score of 88.2, and a policy score of 54.3.

- Spain closely followed with a normalized score of 99, recording a market maturity of 82.5 and a future market score of 89.1.

- The United States secured a normalized score of 90.8, leading in market maturity with a perfect score of 100 but lower future market (55.1) and policy scores (56.7).

- The United Kingdom attained a normalized score of 82.3, with a market maturity of 73.4, a future market of 82.2, and a policy score of 50.8.

- France scored 78.8 (market maturity: 64.8, future market: 82, policy score: 53.5), while Australia had a normalized score of 66.4, supported by a strong policy score of 58.4 but lower future market (54.2).

- Denmark and the Netherlands recorded normalized scores of 63.6 and 61.7, respectively, with strong future market scores (82.3 for Denmark and 76 for the Netherlands).

- Sweden posted a normalized score of 58.4, with lower scores in policy (48.8) and future markets (78.6).

- Finally, Poland achieved a normalized score of 56.6, supported by a strong policy score of 55.7 and a market maturity of 64.1.

(Source: Statista)

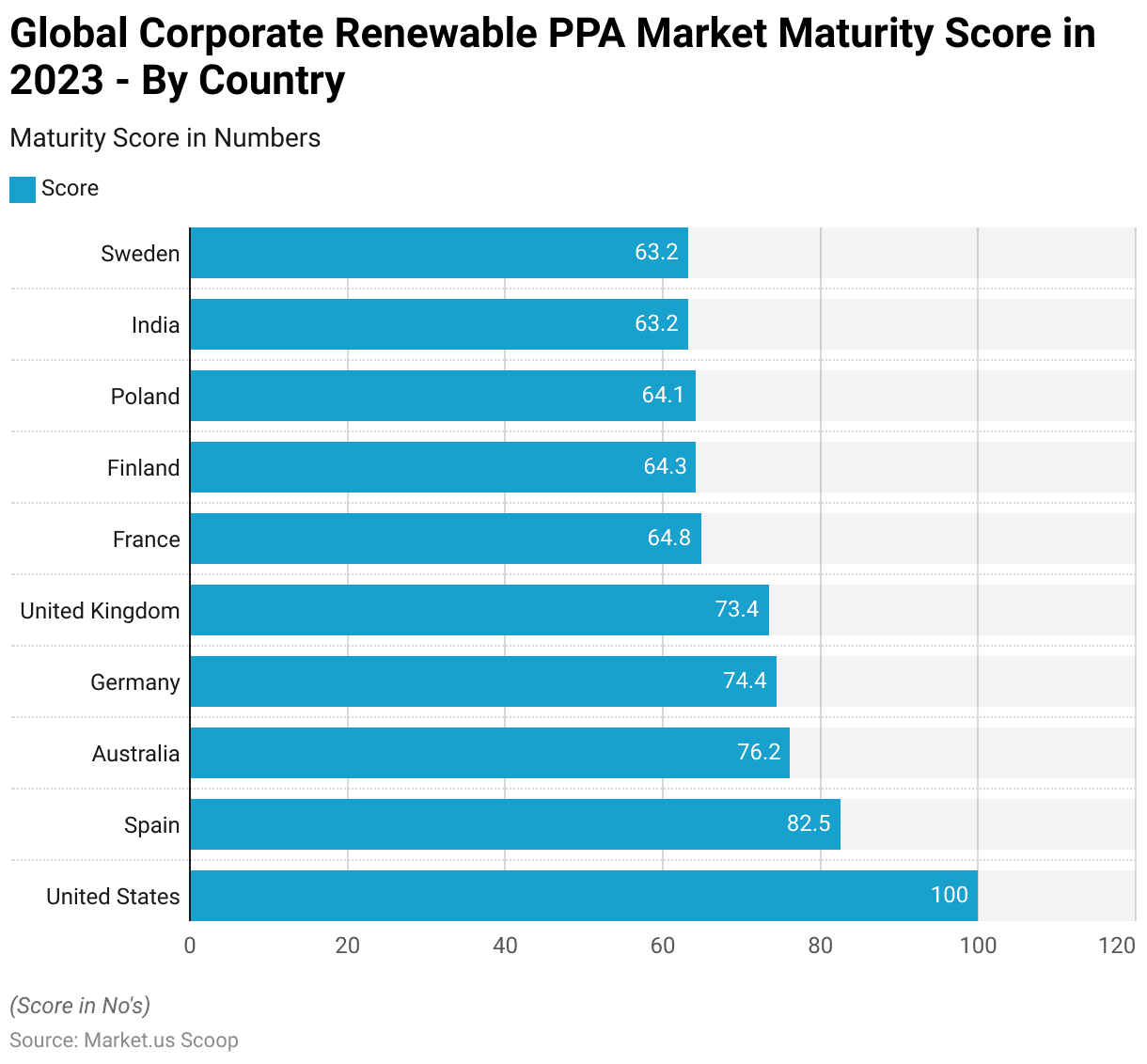

Global Corporate Renewable PPA Market Maturity Score – By Country

- As of November 2023, the most mature countries for renewable corporate power purchase agreements (PPAs) were led by the United States, which achieved the highest market maturity score of 100.

- Spain followed in second place with a score of 82.5, reflecting its strong growth in the renewable PPA market.

- Australia ranked third with a score of 76.2, while Germany and the United Kingdom secured fourth and fifth positions with scores of 74.4 and 73.4, respectively.

- France achieved a market maturity score of 64.8, narrowly surpassing Finland at 64.3 and Poland at 64.1.

- India and Sweden rounded out the top 10 list, each recording a score of 63.2, showcasing their emerging role in the renewable PPA market.

- This ranking highlights the continued global momentum toward renewable energy adoption, with mature markets leading the way.

(Source: Statista)

Power Purchase Agreement Deals Statistics

Renewable Power Purchase Agreement Deals in Europe – By Type Statistics

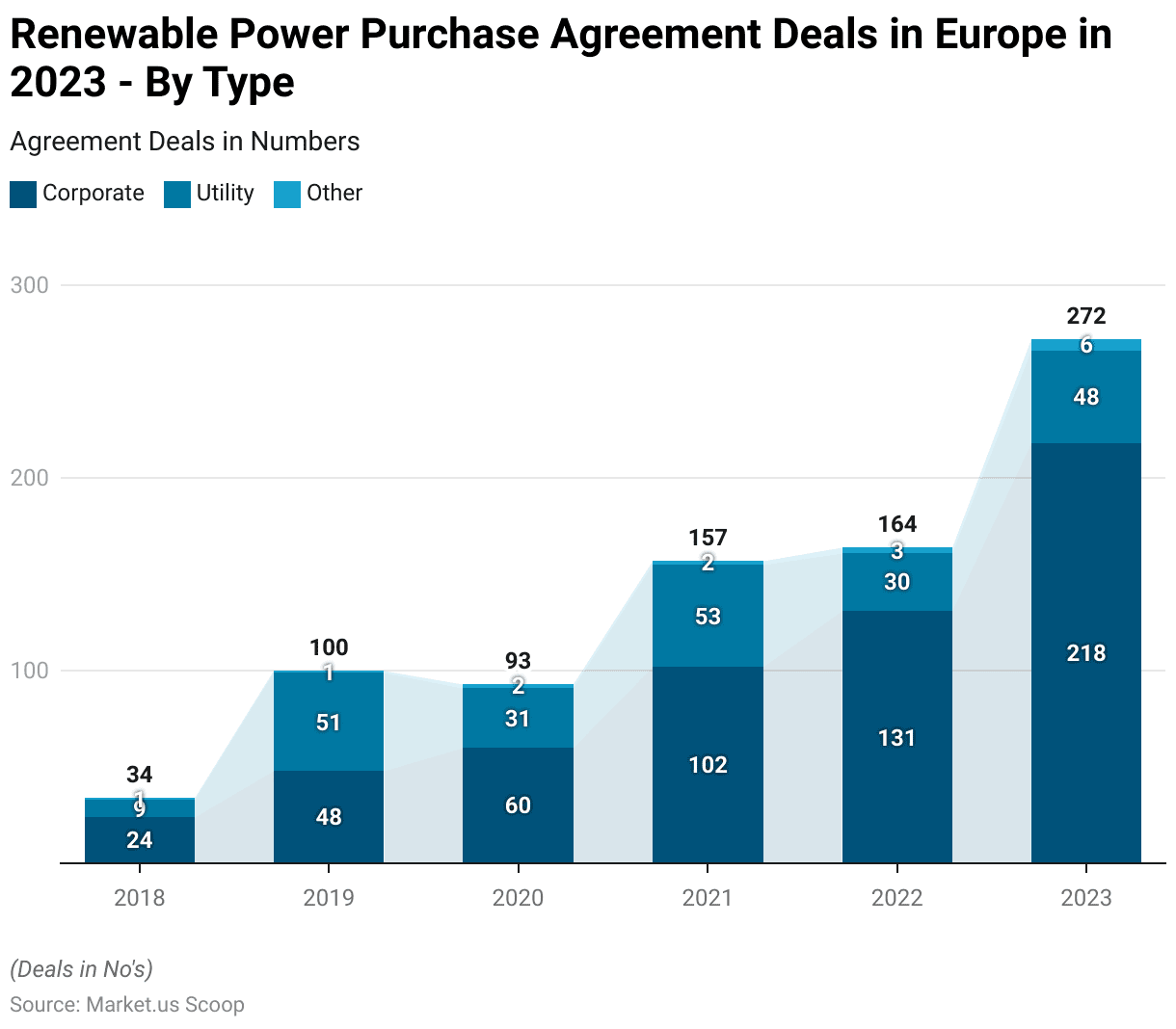

- The number of renewable power purchase agreement (PPA) deals in Europe has grown significantly between 2018 and 2023, reflecting increasing adoption across corporate, utility, and other sectors.

- In 2018, corporate PPAs accounted for 24 deals, while utility PPAs recorded nine deals, and the “other” category registered only one deal.

- By 2019, the market saw substantial growth, with corporate PPAs doubling to 48 deals and utility PPAs surging to 51 deals, while the “other” segment remained at one deal.

- In 2020, corporate PPAs grew to 60 deals, while utility PPAs dropped to 31 deals, and the “other” sector increased slightly to 2 deals.

- The market accelerated in 2021, with corporate PPAs reaching 102 deals, utility deals climbing to 53, and the “other” segment maintaining two deals.

- This growth continued in 2022, when corporate PPAs rose to 131 deals, though utility PPAs declined to 30 deals, and the “other” category expanded to 3 deals.

- The most significant growth occurred in 2023, when corporate PPAs soared to 218 deals, marking a substantial increase, while utility PPAs recovered to 48 deals, and the “other” category further grew to 6 deals.

- This data highlights the dominance of corporate PPAs in driving renewable energy adoption in Europe, particularly in recent years, while utilities and other sectors also play a growing role.

(Source: Statista)

Cumulative Renewable Power Purchase Agreement Deals Signed in Europe – By Country Statistics

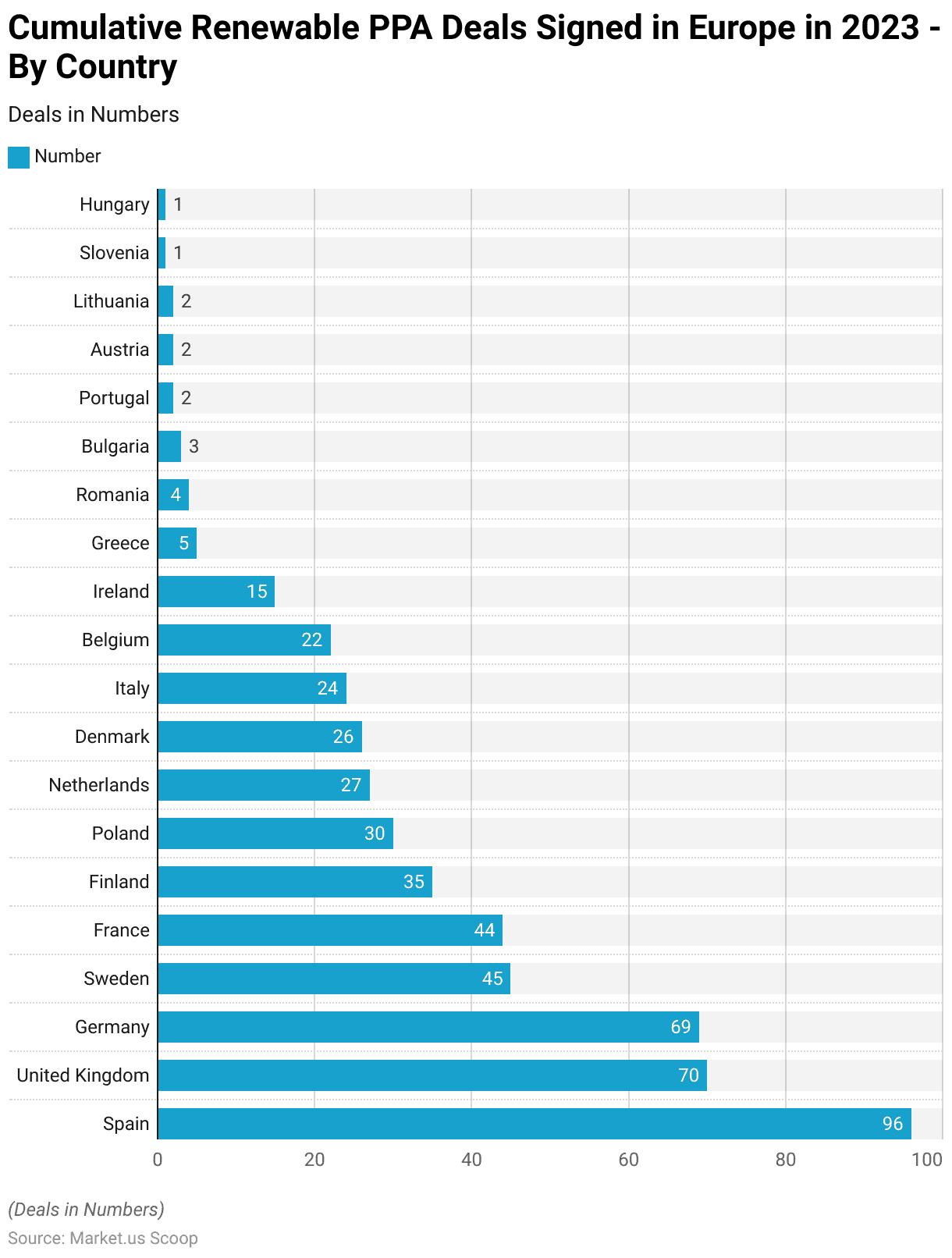

- As of the end of 2023, European countries have collectively demonstrated significant adoption of renewable energy through corporate renewable power purchase agreements (PPAs).

- Spain leads the region with 96 deals, showcasing its strong commitment to clean energy procurement.

- The United Kingdom follows closely with 70 deals, while Germany secures the third position with 69 deals.

- Nordic countries also play a pivotal role, with Sweden signing 45 agreements and Finland finalizing 35 deals.

- France recorded 44 deals, reflecting steady corporate interest, while Poland emerged as a notable player in Eastern Europe with 30 deals.

- Other key contributors include the Netherlands, with 27 deals,

- Denmark with 26, and Italy with 24 agreements. Belgium and Ireland reported 22 and 15 deals, respectively, while Greece secured five deals, and Romania followed with four agreements.

- Bulgaria saw three deals, whereas Portugal, Austria, and Lithuania each recorded two agreements.

- Smaller markets like Slovenia and Hungary reported one deal each, highlighting the gradual penetration of PPAs across the continent.

- This comprehensive distribution highlights a growing commitment to corporate renewable energy adoption, particularly in Western and Northern Europe.

(Source: Statista)

Annual Renewable Power Purchase Agreement Deals Signed in the UK Statistics

- The number of corporate renewable power purchase agreement (PPA) deals signed in the United Kingdom from 2014 to 2023 highlights an evolving trend in renewable energy adoption.

- In 2014, 4 deals were signed, and this figure increased slightly to 5 deals in both 2015 and 2016.

- However, the number dropped to 2 deals in 2017 and further decreased to just one deal in 2018, indicating a slowdown during this period.

- A significant recovery began in 2019, with nine deals signed, showcasing renewed corporate interest in PPAs.

- In 2020, the number of deals fell slightly to 6, followed by a rebound in 2021, where nine deals were once again recorded.

- The market witnessed remarkable growth in 2022, as the number of corporate PPAs surged to 14 deals, and this momentum continued into 2023, reaching its highest point with 16 deals signed.

- This consistent upward trajectory in recent years underlines increasing corporate commitments to renewable energy in the United Kingdom and a growing reliance on PPAs to meet sustainability goals.

(Source: Statista)

Annual Renewable Power Purchase Agreement Deals Signed in Sweden Statistics

- The number of corporate renewable power purchase agreement (PPA) deals signed in Sweden between 2013 and 2023 has shown significant variability, with a noticeable upward trend in recent years.

- In 2013 and 2014, only one deal was signed each year, indicating limited activity in the market.

- The figure increased slightly to 2 deals in 2015, followed by further growth to 4 deals in 2016.

- However, in 2017, the number of deals dropped back to 1, reflecting market fluctuations.

- By 2018, the market recovered slightly, with two deals signed, and a sharp increase followed in 2019, when six deals were finalized.

- The momentum slowed in 2020, with two deals recorded, but strong growth resumed in 2021 as Sweden saw seven corporate PPAs signed.

- The market maintained this momentum with six deals in 2022.

- Finally, in 2023, Sweden reached its highest point in the observed period, recording 11 corporate PPA deals, demonstrating a robust corporate commitment to renewable energy adoption.

(Source: Statista)

Annual Renewable Power Purchase Agreement Deals Signed in Spain Statistics

- The number of corporate renewable power purchase agreement (PPA) deals signed in Spain from 2018 to 2023 highlights a remarkable upward trend, showcasing Spain’s increasing adoption of renewable energy procurement.

- In 2018, Spain recorded five deals, marking the beginning of its steady progress in the renewable energy PPA market.

- This figure slightly increased to 6 deals in 2019, indicating a gradual rise.

- However, the market gained significant momentum in 2020, with the number of deals surging to 14, driven by growing corporate sustainability commitments.

- In 2021, Spain experienced further growth as the number of PPA deals increased to 22, demonstrating strong corporate interest in renewable energy agreements.

- While the market saw a slight decline to 18 deals in 2022, the trend rebounded strongly in 2023, reaching an impressive 30 deals—the highest in the observed period.

- This substantial growth highlights Spain’s leadership in the corporate renewable energy sector and reflects the increasing confidence of businesses in leveraging PPAs to meet their clean energy goals.

(Source: Statista)

Annual Renewable Power Purchase Agreement Deals Signed in Germany Statistics

- From 2018 to 2023, Germany has witnessed a steady and notable rise in the number of corporate renewable power purchase agreement (PPA) deals, reflecting an increasing commitment to renewable energy adoption among corporations.

- In 2018, only two deals were signed, with the same modest number of 2 deals recorded in 2019.

- However, the trend accelerated in 2020, when the number of deals surged to 9, highlighting growing corporate interest in renewable energy initiatives.

- The momentum continued in 2021, with 11 deals finalized, marking further progress in Germany’s renewable energy landscape.

- By 2022, the pace of adoption increased significantly, with 18 deals signed, nearly doubling the figures from two years prior.

- The upward trajectory peaked in 2023, with a record 27 deals signed, showcasing remarkable growth in corporate renewable energy procurement.

- This consistent upward trend underscores Germany’s strong corporate engagement in advancing sustainability goals.

(Source: Statista)

Capacity of Leading Corporate Renewable Energy Deals in the United States

- In 2022, the leading corporate renewable energy deals in the United States showcased a significant commitment toward solar and wind energy adoption.

- Amazon led the market with a substantial 7.1 gigawatts (GW) in solar capacity and 1.3 GW in wind capacity, highlighting its prominent investment in clean energy.

- Meta followed with 1.5 GW of solar capacity and 0.8 GW in wind energy, demonstrating its focus on sustainability.

- Google LLC secured 1.2 GW in solar capacity, further emphasizing its dedication to renewable energy.

- Ford Motor Company contributed 0.7 GW to solar energy initiatives, while McDonald’s, General Motors, and Stellantis each added 0.5 GW to the solar energy sector.

- Ineos reported 0.4 GW in solar capacity, while Comcast and BASF added 0.3 GW and 0.21 GW, respectively.

- These figures underline the growing role of major corporations in advancing renewable energy solutions through substantial investments in solar and wind energy projects.

(Source: Statista)

Power Purchase Agreement Price Statistics

Wind and Solar Power Purchase Agreement Quarterly Prices in Europe Statistics

- Between Q1 2023 and Q1 2024, the prices of solar, wind, and blended power purchase agreements (PPAs) in Europe showed a slight downward trend, reflecting shifts in market dynamics.

- In Q1 2023, solar energy prices were recorded at €73.2 per megawatt-hour (MWh), wind prices stood at €88.88/MWh, and the blended rate reached €106.06/MWh.

- Moving to Q2 2023, solar prices decreased slightly to €72.02/MWh, while wind prices dropped to €85.1/MWh, lowering the blended rate to €98.17/MWh.

- By Q3 2023, solar prices rose marginally to €74.06/MWh, and wind prices increased to €86.94/MWh, raising the blended rate to €99.82/MWh.

- In Q4 2023, solar prices declined to €71.84/MWh, while wind prices settled at €85.38/MWh, resulting in a blended rate of €98.92/MWh.

- By Q1 2024, prices for solar dropped further to €67.63/MWh, and wind prices decreased to €81.13/MWh, bringing the blended rate to €94.63/MWh.

- These trends highlight a gradual reduction in solar, wind, and blended PPA prices over the observed period, indicating increased competitiveness in Europe’s renewable energy market.

(Source: Statista)

Wind and Solar Power Purchase Agreement Quarterly Prices in North America Statistics

- Between Q1 2023 and Q1 2024, the prices of solar, wind, and blended power purchase agreements (PPAs) in North America displayed a gradual upward trend, indicating evolving market conditions.

- In Q1 2023, solar PPAs were priced at $49.52 per megawatt-hour (MWh), while wind PPAs stood at $51.12/MWh, resulting in a blended rate of $50.32/MWh.

- By Q2 2023, solar prices experienced a slight decline to $49.09/MWh, while wind prices climbed to $58/MWh, increasing the blended rate to $53.55/MWh.

- In Q3 2023, solar prices rose to $51.23/MWh, and wind prices marginally decreased to $57.51/MWh, pushing the blended rate to $54.37/MWh.

- The upward momentum continued in Q4 2023, with solar prices reaching $52.69/MWh and wind prices increasing to $60.11/MWh, raising the blended rate to $56.4/MWh.

- In Q1 2024, solar prices settled at $51.52/MWh, while wind prices climbed further to $61.52/MWh, resulting in a blended rate of $56.73/MWh.

- These trends indicate a notable rise in wind energy pricing compared to solar, contributing to the overall increase in blended PPA rates.

(Source: Statista)

Solar PV Power Purchase Agreement Price Forecast in Europe – By Country Statistics

- Between 2025 and 2034, the average forecast price for solar PV power purchase agreements (PPAs) across selected European countries reveals significant regional variations, with Nordic nations leading the list in pricing.

- Sweden is projected to have the highest average PPA price at €141 per megawatt-hour (MWh), followed closely by Norway at €139/MWh and Finland at €138/MWh.

- In contrast, Denmark has a lower projected price of €112/MWh, while Ireland is forecasted at €106/MWh.

- France and Poland report prices of €103/MWh and €100/MWh, respectively, reflecting moderate cost expectations.

- Austria follows with €97/MWh, and the Netherlands is forecasted at €93/MWh. Major economies such as Germany and Great Britain are projected to reach €91/MWh and €89/MWh, respectively.

- Czechia comes close at €88/MWh, while Slovenia and Belgium are forecasted at €86/MWh and €85/MWh.

- Further down the list, Slovakia and Hungary report similar values at €84/MWh and €83/MWh, respectively.

- Southern European nations like Portugal and Spain reflect significantly lower prices at €73/MWh and €70/MWh, showcasing more competitive solar energy markets.

- Italy holds the lowest forecast price at €57/MWh, emphasizing its cost-efficient solar energy outlook.

(Source: Statista)

Quarterly Solar Power Purchase Agreement Prices in the U.S. – By System Operator Statistics

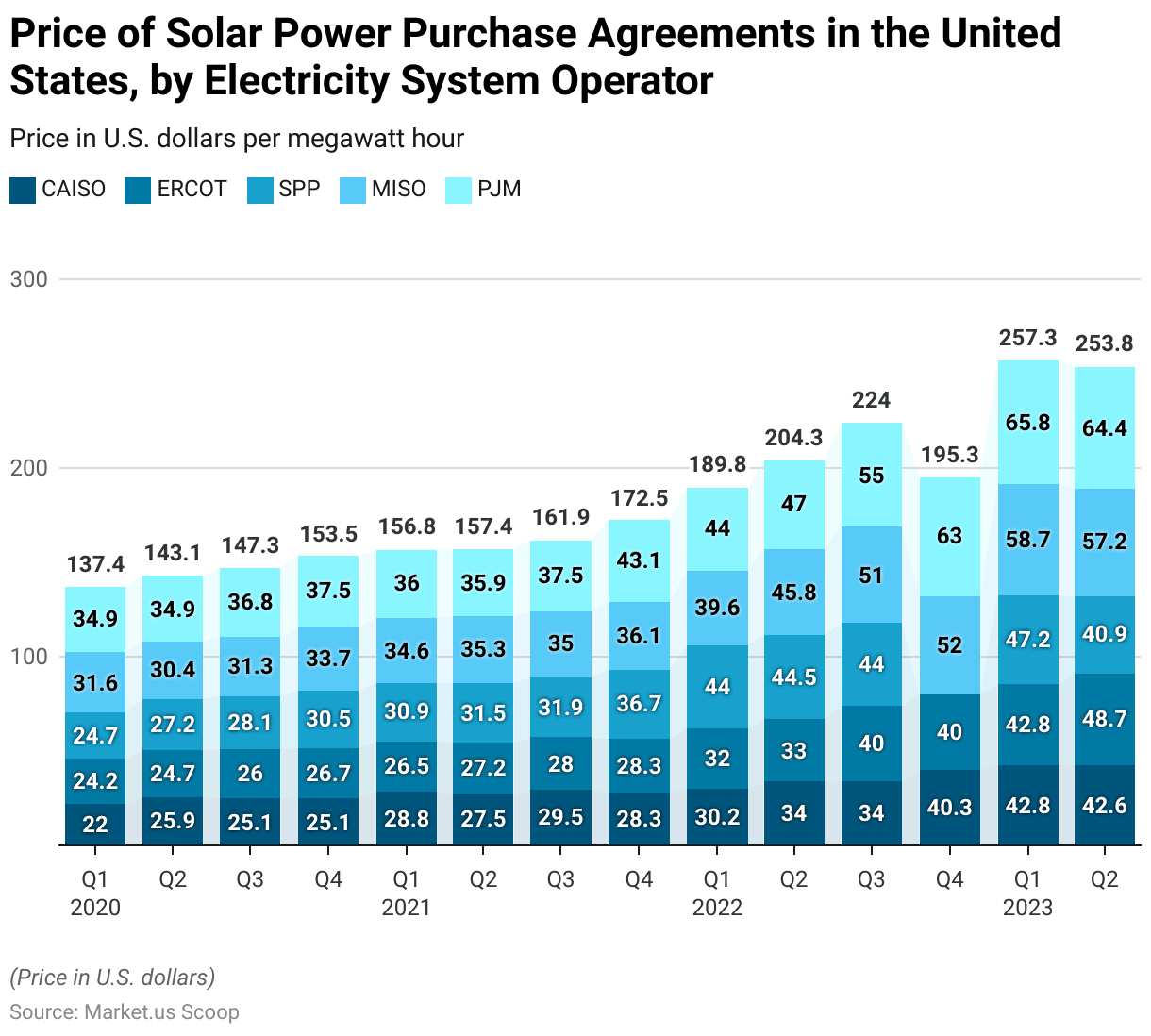

- Between Q1 2020 and Q2 2023, the price of solar power purchase agreements (PPAs) in the United States exhibited an upward trend across major electricity system operators, reflecting changes in market demand and supply conditions.

- In CAISO (California Independent System Operator), prices started at $22/MWh in Q1 2020 and steadily increased to $42.6/MWh by Q2 2023, signaling consistent price growth.

- ERCOT (Electric Reliability Council of Texas) began at $24.2/MWh in Q1 2020 and experienced a sharp increase to $48.7/MWh in Q2 2023, highlighting rising solar PPA costs in Texas.

- In the SPP (Southwest Power Pool) region, prices climbed from $24.7/MWh in Q1 2020 to a peak of $47.2/MWh in Q1 2023 before falling slightly to $40.9/MWh in Q2 2023.

- The MISO (Midcontinent Independent System Operator) region witnessed significant growth, with prices rising from $31.6/MWh in Q1 2020 to $57.2/MWh in Q2 2023, reflecting increased costs for solar PPAs.

- PJM (Pennsylvania-New Jersey-Maryland Interconnection) recorded the highest prices throughout the period, starting at $34.9/MWh in Q1 2020 and reaching $65.8/MWh by Q1 2023, before settling slightly lower at $64.4/MWh in Q2 2023.

- These trends indicate rising costs for solar PPAs across all regions, particularly in ERCOT, MISO, and PJM, driven by higher energy demand and changing market conditions.

- While CAISO experienced relatively moderate price growth, regions like PJM saw significant increases, showcasing variations in regional market dynamics.

(Source: Statista)

Quarterly Wind Power Purchase Agreement Prices in the U.S. – By System Operator Statistics

- Between Q1 2020 and Q4 2023, the price of wind power purchase agreements (PPAs) in the United States exhibited notable variations across major electricity system operators: CAISO, PJM, MISO, ERCOT, and SPP.

- In CAISO (California Independent System Operator), prices began at $48.3 per megawatt-hour (MWh) in Q1 2020 and rose consistently, peaking at $80.5/MWh in Q3 2023, before slightly falling to $75/MWh in Q4 2023.

- PJM (Pennsylvania-New Jersey-Maryland Interconnection) experienced an overall upward trend, starting at $29.1/MWh in Q1 2020, reaching $55.1/MWh in Q1 2022, and culminating at $65/MWh in Q4 2023.

- MISO (Midcontinent Independent System Operator) saw prices rise from $27.4/MWh in Q1 2020 to a peak of $59/MWh in Q3 2023 before settling at $58/MWh in Q4 2023.

- ERCOT (Electric Reliability Council of Texas) reported relatively lower prices initially, at $16/MWh in Q1 2020, but steadily increased to $42/MWh by Q4 2023, reflecting growing demand and market adjustments.

- Meanwhile, SPP (Southwest Power Pool) exhibited fluctuations, starting at $19/MWh in Q1 2020 and peaking at $40/MWh in Q4 2023, with intermittent declines and recoveries.

- Across all regions, the most significant price increases occurred between 2022 and 2023, particularly in CAISO and MISO.

- This upward trend reflects broader market dynamics, including rising costs of materials, higher demand for renewable energy, and regional differences in grid infrastructure.

(Source: Statista)

Key Investments

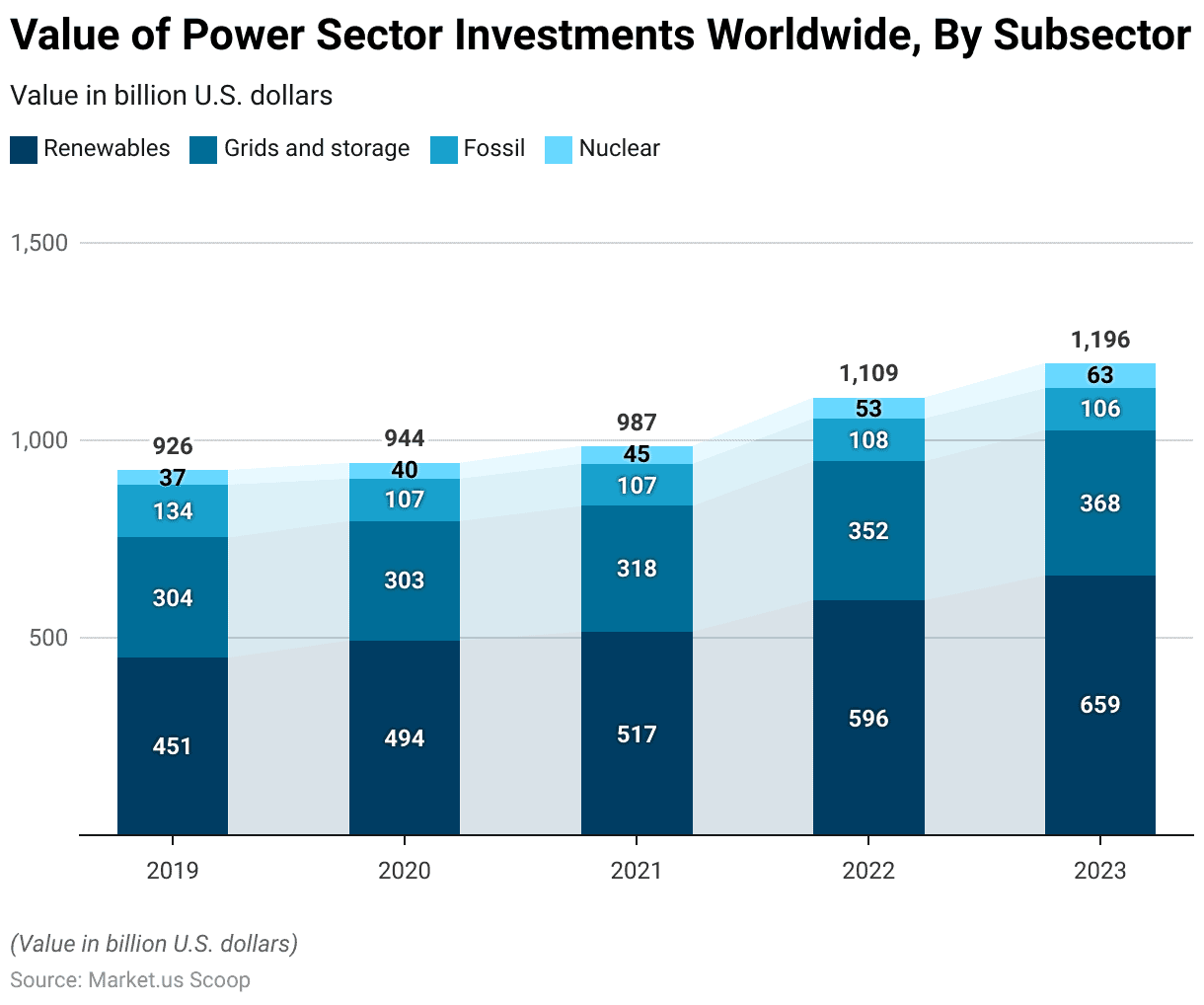

Global Investment in Power Sector – By Subsector

- Between 2019 and 2023, global power sector investments experienced substantial growth across various subsectors, including renewables, grids and storage, fossil fuels, and nuclear energy, measured in 2022 billion U.S. dollars.

- Investment in renewables grew significantly from $451 billion in 2019 to $659 billion in 2023, showcasing a robust and consistent focus on clean energy solutions.

- Meanwhile, investments in grids and storage also exhibited steady growth, increasing from $304 billion in 2019 to $368 billion in 2023, reflecting the need to enhance infrastructure for energy distribution and storage.

- In contrast, investment in fossil fuels declined from $134 billion in 2019 to $106 billion in 2023, highlighting a global shift away from traditional energy sources toward more sustainable alternatives.

- However, nuclear energy saw a notable rise in investment, climbing from $37 billion in 2019 to $63 billion in 2023, indicating renewed interest in nuclear power as a low-emission energy source.

- This data underscores the increasing prioritization of renewable energy and infrastructure improvements, with declining investments in fossil fuels. Simultaneously, nuclear energy investments highlight its growing role in the global energy transition.

(Source: Statista)

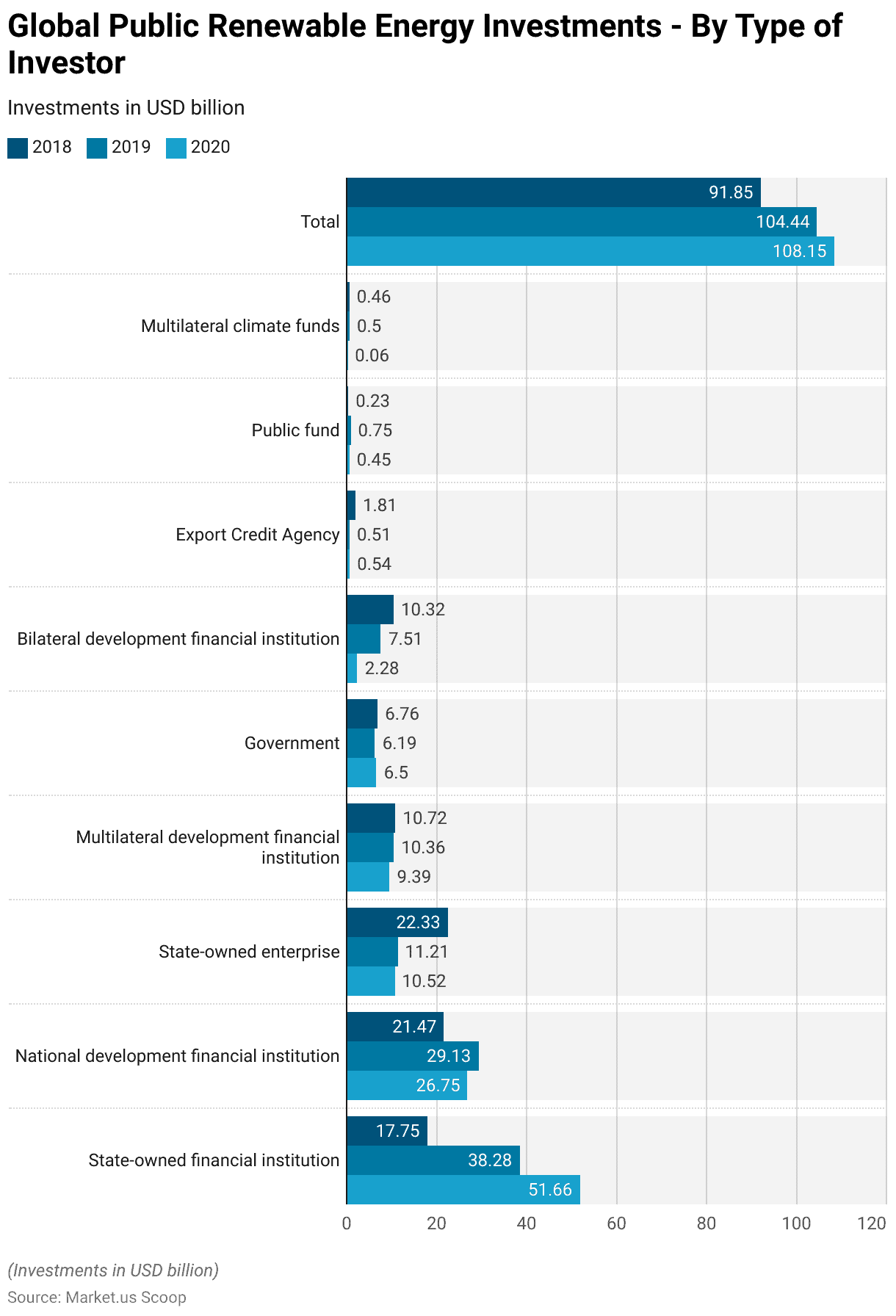

Global Public Renewable Energy Investments – By Type of Investor

- Between 2018 and 2020, public investments in renewable energy worldwide exhibited significant variation across different types of investors, growing from $91.85 billion in 2018 to $108.15 billion in 2020.

- State-owned financial institutions emerged as the leading contributors, increasing their investments dramatically from $17.75 billion in 2018 to $51.66 billion in 2020, underscoring their critical role in advancing renewable energy projects.

- National development financial institutions also played a substantial role, with investments rising from $21.47 billion in 2018 to a peak of $29.13 billion in 2019 before slightly declining to $26.75 billion in 2020.

- Conversely, state-owned enterprises saw a consistent decline in their contributions, falling from $22.33 billion in 2018 to $10.52 billion in 2020. Similarly, investments from multilateral development financial institutions decreased from $10.72 billion in 2018 to $9.39 billion in 2020.

- Government investments remained relatively stable, hovering around $6.76 billion in 2018, $6.19 billion in 2019, and $6.5 billion in 2020.

- Bilateral development financial institutions showed a steep decline, dropping from $10.32 billion in 2018 to just $2.28 billion in 2020. Contributions from export credit agencies remained minimal, fluctuating between $0.51 billion and $0.54 billion.

- Public funds and multilateral climate funds saw negligible contributions, with public funds peaking at $0.75 billion in 2019 and multilateral climate funds decreasing sharply from $0.46 billion in 2018 to just $0.06 billion in 2020.

- This data highlights a significant shift toward state-backed financial institutions as primary investors in renewable energy, while other funding sources, such as bilateral and multilateral funds, experienced noticeable declines.

(Source: Statista)

Power Purchase Agreement Regulations

- Power Purchase Agreements (PPAs) serve as vital tools for managing long-term energy procurement, especially in the renewable sector.

- Across various regions, regulations and developments in PPAs reflect efforts to enhance energy security and economic stability.

- In the European Union, the 2023 reforms proposed by the European Commission aim to stabilize the electricity market by promoting long-term contracts like PPAs, enhancing industry competitiveness, and reducing exposure to volatile energy prices.

- These reforms include adjustments to existing legislation, such as the Electricity Regulation and the Electricity Directive, to support renewable energy integration and better market transparency.

- In Asia-Pacific, countries have tailored PPA regulations to harness their renewable potential and meet sustainability targets.

- For instance, in Vietnam, the regulatory framework supports both physical and virtual PPAs, allowing businesses to negotiate directly with energy producers under the Direct Power Purchase Agreement (DPPA) scheme. This flexibility supports the adoption of renewable energy at varying scales and by different sectors.

- Meanwhile, in Thailand and Singapore, government-driven schemes and competitive bidding processes under regulatory frameworks encourage the use of PPAs, fostering both public and private sector involvement in renewable energy projects.

- Globally, PPAs are recognized for their role in providing revenue stability to power producers and cost predictability to consumers, making them a cornerstone of strategic energy planning and investment in sustainable energy infrastructures.

(Source: Ally Law – We Work Together, TotalEnergies ENEOS, PPP Resource Center)

Recent Developments

Acquisitions and Mergers:

- NextEra Energy Acquires Renewable Energy Projects (2023): In September 2023, NextEra Energy, one of the leading renewable energy companies in the U.S., acquired 1.6 GW of renewable energy projects in a deal valued at $1.2 billion. This acquisition includes both solar and wind PPAs, reinforcing NextEra’s position in the renewable energy market and supporting its goal of reducing carbon emissions by 67% by 2030.

- Engie’s Merger with International Utilities for Global PPA Expansion (2023): Engie merged with international utility company Iberdrola in a strategic move to expand their renewable energy portfolio globally. As part of the merger, the companies jointly signed PPAs worth over $1.8 billion for offshore wind and solar projects across Europe and North America.

Product Launches:

- Tesla Energy’s New Virtual Power Plant Agreement (2023): In 2023, Tesla Energy launched a new Virtual Power Plant (VPP) product for residential energy consumers, allowing homeowners with solar panels and batteries to sell excess energy back to the grid. The product is expected to sign over 200,000 residential PPAs in the next 5 years, contributing to a total capacity of 2 GW of distributed clean energy.

- Siemens Gamesa Unveils Offshore Wind PPA (2023): In November 2023, Siemens Gamesa launched a 1 GW offshore wind project in the North Sea with an agreement to supply power to a major energy buyer via a long-term PPA. The project is expected to reduce carbon emissions by 2.5 million tons annually and provide electricity for approximately 2 million households.

Funding and Investments:

- Renewable PPA Investment Growth (2023): In 2023, investment in Power Purchase Agreements (PPAs) for renewable energy projects surged to $22 billion, reflecting a 15% increase compared to the previous year. This growth was driven by increased corporate demand for clean energy and strong support from financial institutions focused on sustainable investments.

- Brookfield Renewable Partners Secures $500 Million in PPA-Linked Financing (2023): Brookfield Renewable Partners raised $500 million in a green bond offering in 2023 to fund new renewable energy projects linked to Power Purchase Agreements. This funding is expected to help deploy 2 GW of new renewable energy capacity, contributing significantly to decarbonizing power grids in North America and Europe.

Regulatory Developments:

- U.S. Federal PPA Tax Incentives Extended (2023): In December 2023, the U.S. government extended tax incentives for renewable energy PPAs through the Inflation Reduction Act (IRA). This includes an extension of the 30% Investment Tax Credit (ITC) for solar projects, making it more attractive for large corporations to sign PPAs with renewable energy providers.

- EU Green Deal Fuels PPA Growth (2023): The European Union’s Green Deal is expected to accelerate PPA activity in Europe. The EU’s goal to achieve carbon neutrality by 2050 has led to an increase in renewable energy projects, and PPA agreements are playing a central role in financing these initiatives. The total capacity of PPAs in Europe grew by 25% in 2023 compared to the previous year, with over 15 GW of new renewable capacity under long-term contracts.

Conclusion

Power Purchase Agreement Statistics – A Power Purchase Agreement (PPA) is a long-term contract between a power generator and a buyer, ensuring the supply of renewable electricity at a pre-agreed price.

PPAs provide cost stability by protecting buyers from energy price fluctuations and driving investment in renewable energy infrastructure.

Growing corporate commitments to sustainability and falling costs of solar and wind technologies have fueled PPA adoption, particularly in regions like Europe and North America.

By offering financial predictability to buyers and supporting clean energy development, PPAs play a critical role in accelerating the global transition to renewable energy.

FAQs

What is a Power Purchase Agreement (PPA)?

A Power Purchase Agreement (PPA) is a legally binding contract that outlines the terms under which electricity will be generated and sold between a power producer (such as a renewable energy project developer) and a buyer (such as a utility, corporation, or government entity).

Why are PPAs important?

PPAs provide financial certainty for energy producers and buyers. They help secure funding for renewable energy projects by guaranteeing a long-term revenue stream, and they provide buyers with stable pricing for energy.

What is the typical duration of a PPA?

PPAs typically range from 10 to 25 years, depending on the type of project and financing requirements. Longer durations provide more certainty for both parties, especially the seller.

How do PPAs affect energy prices?

PPAs help lock in a fixed price for electricity over the life of the agreement, which can help both buyers and sellers hedge against price volatility in energy markets. This price can be either fixed or variable based on certain conditions or indices.

What is the difference between a PPA and a traditional energy contract?

In traditional contracts, energy prices are typically more volatile and depend on market conditions. PPAs, on the other hand, offer long-term price certainty and often focus on specific energy sources, especially renewable energy.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)