Table of Contents

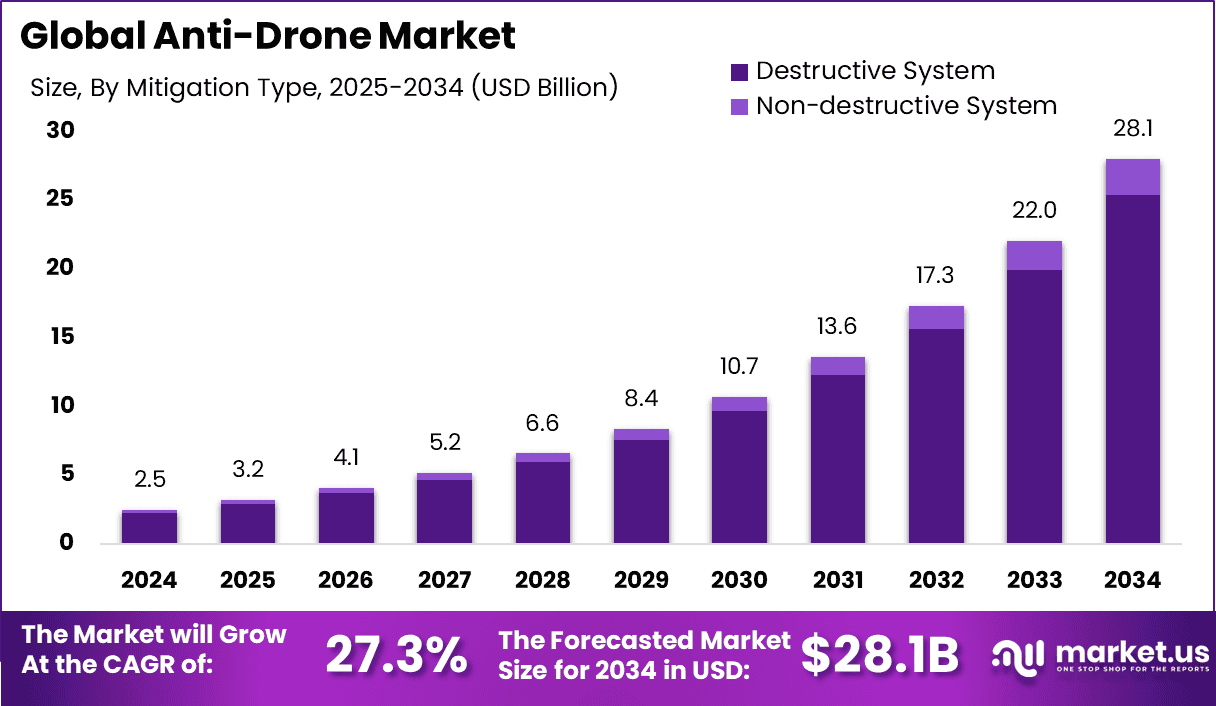

The global anti-drone market is experiencing unprecedented growth, projected to expand from USD 2.5 billion in 2024 to approximately USD 28.1 billion by 2034, registering a CAGR of 27.3%. North America dominated the market in 2024 with a 46.8% share and revenue of USD 1.1 billion, while the U.S. alone contributed USD 0.74 billion, forecasted to grow at 27.5% CAGR.

The destructive system segment accounted for over 90.7% market share, driven by a strong preference for physical neutralization. Radar-based detection topped the detection tech category, while ground-based systems led in deployment, especially in military and defense operations, which secured 58.9% of the end-user market.

US Tariff Impact on the Anti-Drone Market

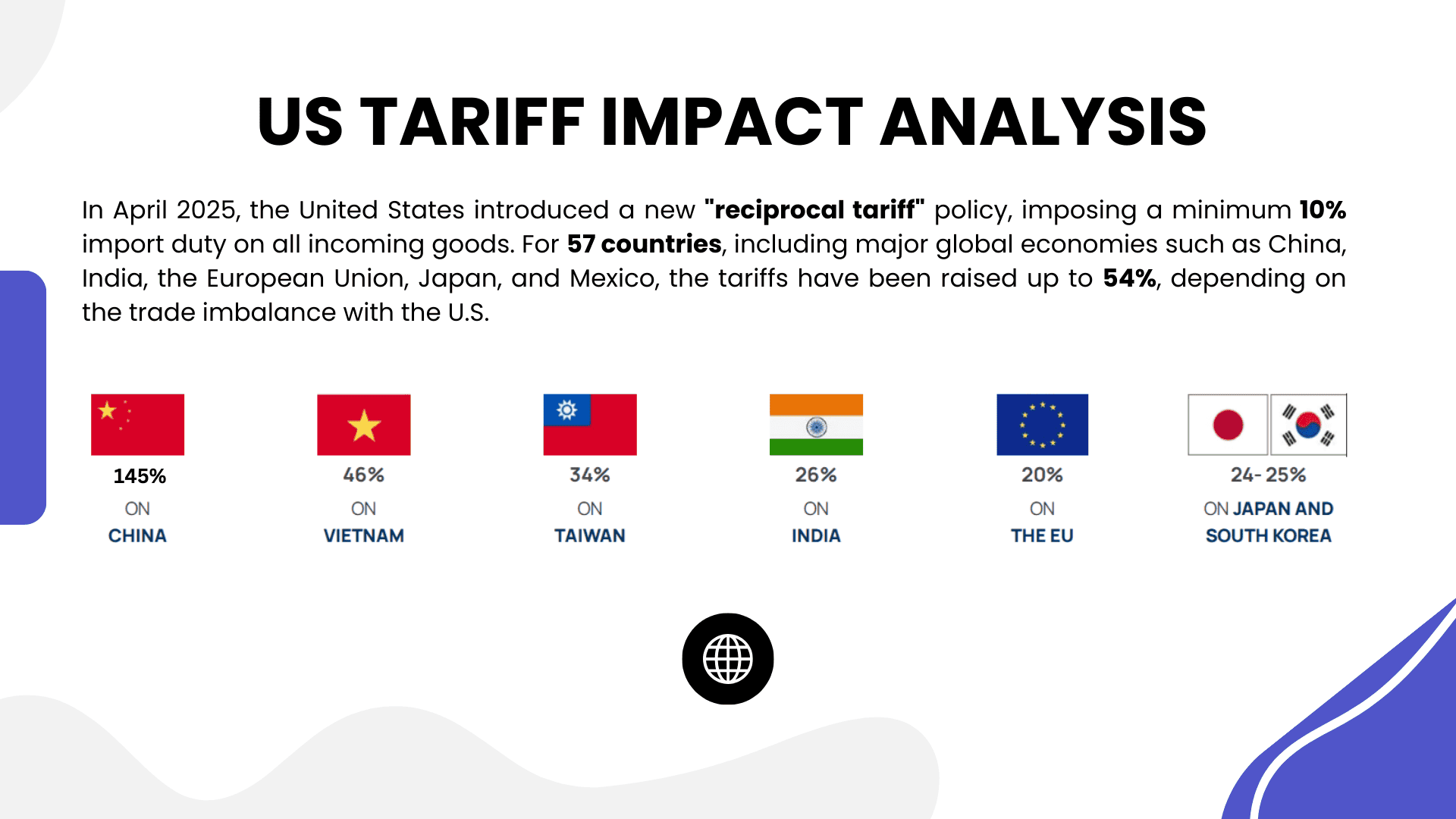

The U.S. tariffs, particularly those imposed on Chinese-made drones and electronic components, have significantly affected the anti-drone market. In 2025, a 170% tariff was applied to Chinese drones, while core components such as processors and RF modules saw increases between 10% to 25%, according to Airsight.com and DefenseNewsallied suppliers, although this transition is costly and time-consuming.

These tariffs have increased acquisition and production costs, directly impacting defense contractors and OEMs dependent on foreign-sourced technologies. This has also led to slower procurement cycles, increased R&D budgets, and delayed project deployments.

➤ Discover how our research uncovers business opportunities @ https://market.us/report/anti-drone-market/free-sample/

Additionally, the uncertainty over future tariff policy has prompted U.S. defense agencies and private firms to shift sourcing to domestic or allied suppliers, although this transition is costly and time-consuming. The market, while rapidly expanding, must now balance growth with new operational cost structures and regulatory pressures introduced by these tariffs.

Economic Impact

- Increased import costs have led to higher procurement prices.

- Tariffs have inflated project budgets for defense and infrastructure agencies.

- The rise in production costs affects commercial adoption and investor sentiment.

Geographical Impact

- North America faces the most direct cost pressures due to high import reliance.

- Asia-Pacific may gain from nearshoring and local manufacturing growth.

- Europe is seeing a moderate impact, with increased interest in domestic drone countermeasure development.

Business Impact

- Tariffs force firms to rethink sourcing and R&D priorities.

- Market entrants face capital strain due to increased component prices.

- Long-term contracts are being re-evaluated to accommodate rising costs and delayed deliveries.

Key Takeaways

- U.S. tariffs raised component costs by up to 25%, with drones seeing 170% hikes.

- North America leads the anti-drone market, but also bears the heaviest tariff burden.

- Destructive systems dominate over non-lethal methods.

- Radar-based detection and ground-based platforms remain the preferred technologies.

- Military and defense continue to drive over 58.9% of demand.

➤ Get Full Access Purchase Now @ https://market.us/purchase-report/?report_id=147337

Analyst Viewpoint

The anti-drone market is accelerating due to escalating global threats and security breaches involving unmanned aerial vehicles (UAVs). While U.S. tariffs have complicated supply chains and raised costs, they’ve also incentivized domestic innovation and manufacturing. Presently, the focus remains on radar detection and destructive countermeasures due to their proven efficiency.

Looking forward, the market will benefit from increased government defense budgets, technological partnerships, and localized production. Players that adapt swiftly by investing in R&D and exploring domestic supply alternatives are well-positioned to lead. Overall, long-term market fundamentals remain strong despite short-term policy and pricing disruptions.

Regional Analysis

In 2024, North America held the largest share at 46.8%, driven by extensive military applications and rising investment in homeland security infrastructure. The U.S. market, valued at USD 0.74 billion, is expected to maintain high momentum, supported by federal contracts and advanced defense ecosystems.

Europe is experiencing steady growth due to regulatory reforms and joint defense initiatives. Meanwhile, Asia-Pacific is emerging as a key growth region, particularly in China, India, and South Korea, where military modernization programs are underway. Latin America and MEA regions show modest growth potential, primarily influenced by increasing border surveillance and internal security threats.

➤ Discover More Latest Research

- Blockchain Security Market

- Post Quantum Computing Market

- AI Consulting Market

- Solar Panel Cleaning Robot Market

Business Opportunities

The rise of unauthorized drone activity across airports, military bases, and urban infrastructure creates vast business opportunities. There’s growing demand for customizable anti-drone systems in critical infrastructure protection, border surveillance, and public event safety. Expansion in ground-based platforms and radar-detection solutions offers scalable commercial potential.

Furthermore, opportunities lie in developing AI-powered autonomous detection tools that minimize false positives and reduce operational complexity. Integrating anti-drone systems with smart city and airport security frameworks also opens new growth avenues. As governments increase defense allocations and private security firms expand portfolios, suppliers of cost-effective and multi-layered anti-drone technologies will gain significant competitive advantages.

Key Segmentation

- By Mitigation Type: Destructive System (Kinetic, Laser-based), Non-Destructive (Jamming, Interception).

- By Defense Type: Detection Only, Detection & Disruption Systems.

- By Technology: Electronic Systems (Signal Disruption, Jamming), Kinetic, Laser, Radar-based, RF.

- By Platform: Ground-Based, Handheld, UAV-Based.

- By End-User: Military & Defense, Homeland Security, Commercial Entities (Airports, Stadiums, Data Centers).

- By Region: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa.

Ground-based radar systems dominate due to effectiveness in long-range surveillance. Destructive methods remain prevalent, especially in military settings, with commercial sectors gradually adopting non-lethal countermeasures for urban use.

Key Player Analysis

Key market players are focused on defense-grade innovation, integrating radar, RF jamming, and kinetic response systems into modular, scalable platforms. Many companies are diversifying through strategic collaborations with aerospace firms and military contractors to offer interoperable solutions. Firms also invest heavily in AI, machine learning, and autonomous threat response capabilities.

The competition is further intensified by the need to balance system effectiveness with cost-efficiency. As global drone incidents surge, vendors prioritizing compact, rapid-deployment systems and regulatory compliance are seeing strong adoption. Expansion into emerging markets and development of portable systems for civil and urban applications are notable strategies gaining traction.

List of Anti-Drone Market Companies

- Airbus Group SE

- Blighter Surveillance Systems

- Dedrone

- Advanced Radar Technologies S.A.

- DeTect, Inc.

- Drone shield LLC

- Enterprise Control Systems

- Israel Aerospace Industries Ltd. (IAI)

- Lit eye Systems, Inc.

- Lockheed Martin Corporation

- Orelia

- Prime Consulting and technologies

- Raytheon Company

- Saab Ab

- Selex Es Inc.

- Thales Group

- The Boeing Company

Recent Developments

In Q1 2025, several companies launched multi-modal detection systems combining radar, optical, and RF technologies to counter next-gen UAV threats. U.S. defense agencies announced expanded anti-drone trials with NATO allies. Furthermore, private security providers began integrating portable jamming units in high-risk urban zones for temporary protection during public events.

Conclusion

The anti-drone market is entering a hypergrowth phase, propelled by evolving threats and robust defense investments. Despite short-term tariff-induced cost pressures, demand remains resilient. Continued innovation, adaptive sourcing strategies, and cross-border collaboration will be pivotal in shaping a secure airspace ecosystem and driving market success across both public and private sectors.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)