Table of Contents

- Introduction

- Editor’s Choice

- Cellular IoT Market Overview

- Technical Specifications of Cellular IoT Statistics

- IoT Connections Worldwide

- Active IoT Devices Statistics

- Cellular IoT Connections Worldwide Statistics

- Global Cellular IoT Module Statistics

- Global Cellular IoT Device Shipments Statistics

- Regulations for Cellular IoT

- Recent Developments

- Conclusion

- FAQs

Introduction

Cellular IoT Statistics: Cellular IoT utilizes standard cellular networks like 4G LTE, NB-IoT, and LTE-M to connect a diverse range of devices beyond traditional smartphones and computers.

It offers robust connectivity over long distances and in remote areas where other networks may be unavailable. making it ideal for applications requiring broad geographical coverage.

With options designed for low power consumption, such as NB-IoT and LTE-M, Cellular IoT supports devices that can operate for extended periods on minimal battery power.

This technology ensures secure data transmission through built-in encryption and authentication features. Which are essential for protecting sensitive information in various IoT applications across industries like smart cities, healthcare, and agriculture.

Editor’s Choice

- The global cellular IoT market revenue reached USD 2.84 billion in 2023.

- By 2033, the market is expected to achieve a significant total revenue of USD 19.78 billion. With software at USD 6.92 billion and hardware at USD 12.86 billion.

- Significant contributions from several key players characterize the global cellular IoT market. Qualcomm Inc. leads the market with a share of 15%.

- The global cellular IoT market exhibits varied regional market shares, with North America leading at 34.1%.

- The cellular IoT ecosystem includes several key technologies, such as 5G Massive IoT (mMTC), 5G RedCap, and 4G LTE Cat-1bis. These technologies offer various capabilities suitable for different applications.

- The evolution of cellular IoT connections by segment and technology from 2017 to 2029 reveals significant trends in the adoption of various IoT technologies.

- In the United States, the IoT Cybersecurity Improvement Act of 2020 sets security standards for devices used by federal agencies. California’s IoT Security Law requires manufacturers to implement reasonable security features.

Cellular IoT Market Overview

Global Cellular IoT Market Size Statistics

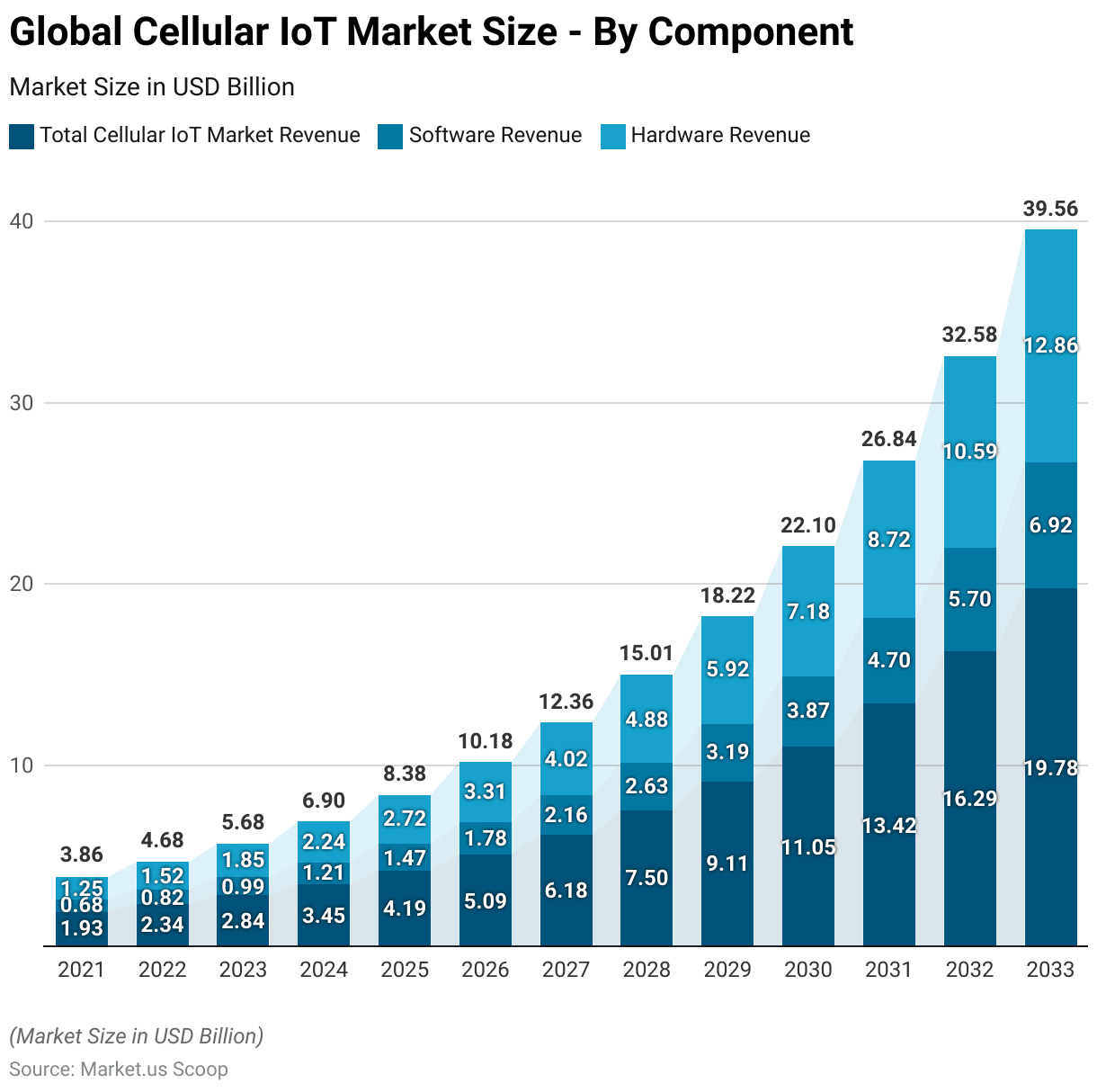

- The global cellular IoT market has exhibited a robust growth trajectory from 2021 to 2033 at a CAGR of 21.4%, underscoring its increasing adoption and expansion.

- In 2021, the market revenue stood at USD 1.93 billion.

- This figure saw a steady rise to USD 2.34 billion in 2022 and further to USD 2.84 billion in 2023.

- The upward trend continued into 2024, reaching USD 3.45 billion, and in 2025, it climbed to USD 4.19 billion.

- By 2026, the market achieved a notable revenue of USD 5.09 billion.

- The growth momentum accelerated, with revenues amounting to USD 6.18 billion in 2027 and USD 7.50 billion in 2028.

- A significant surge was observed in 2029, with revenues hitting USD 9.11 billion.

- The upward trend persisted through the next decade, with the market reaching USD 11.05 billion in 2030, USD 13.42 billion in 2031, USD 16.29 billion in 2032, and an impressive USD 19.78 billion by 2033.

- This substantial growth underscores the increasing reliance on cellular IoT technologies across various sectors globally.

(Source: market.us)

Global Cellular IoT Market Size – By Component Statistics

2021-2027

- The global cellular IoT market has demonstrated substantial growth from 2021 to 2033. With a marked increase in both software and hardware revenues.

- In 2021, the total market revenue was USD 1.93 billion. Comprising USD 0.68 billion from software and USD 1.25 billion from hardware.

- By 2022, the market had grown to USD 2.34 billion. With software revenue at USD 0.82 billion and hardware revenue at USD 1.52 billion.

- In 2023, the total revenue reached USD 2.84 billion. With software contributing USD 0.99 billion and hardware USD 1.85 billion.

- The trend continued upward in 2024, with the market totaling USD 3.45 billion. Including USD 1.21 billion from software and USD 2.24 billion from hardware.

- In 2025, the market expanded to USD 4.19 billion. With software at USD 1.47 billion and hardware at USD 2.72 billion.

- By 2026, revenues climbed to USD 5.09 billion. With software generating USD 1.78 billion and hardware USD 3.31 billion.

- In 2027, the market further grew to USD 6.18 billion. With software and hardware revenues at USD 2.16 billion and USD 4.02 billion, respectively.

2028-2033

- The year 2028 saw the market reach USD 7.50 billion. With software at USD 2.63 billion and hardware at USD 4.88 billion.

- In 2029, the market increased to USD 9.11 billion. Comprising USD 3.19 billion from software and USD 5.92 billion from hardware.

- By 2030, the market revenue was USD 11.05 billion. With software at USD 3.87 billion and hardware at USD 7.18 billion.

- In 2031, total revenue was USD 13.42 billion. With software and hardware revenues at USD 4.70 billion and USD 8.72 billion, respectively.

- The market reached USD 16.29 billion in 2032, with software contributing USD 5.70 billion and hardware USD 10.59 billion.

- Finally, in 2033, the market achieved a significant total revenue of USD 19.78 billion. With software at USD 6.92 billion and hardware at USD 12.86 billion.

- This robust growth reflects the escalating integration and reliance on cellular IoT technologies across diverse industries.

(Source: market.us)

Competitive Landscape of the Global Cellular IoT Market Statistics

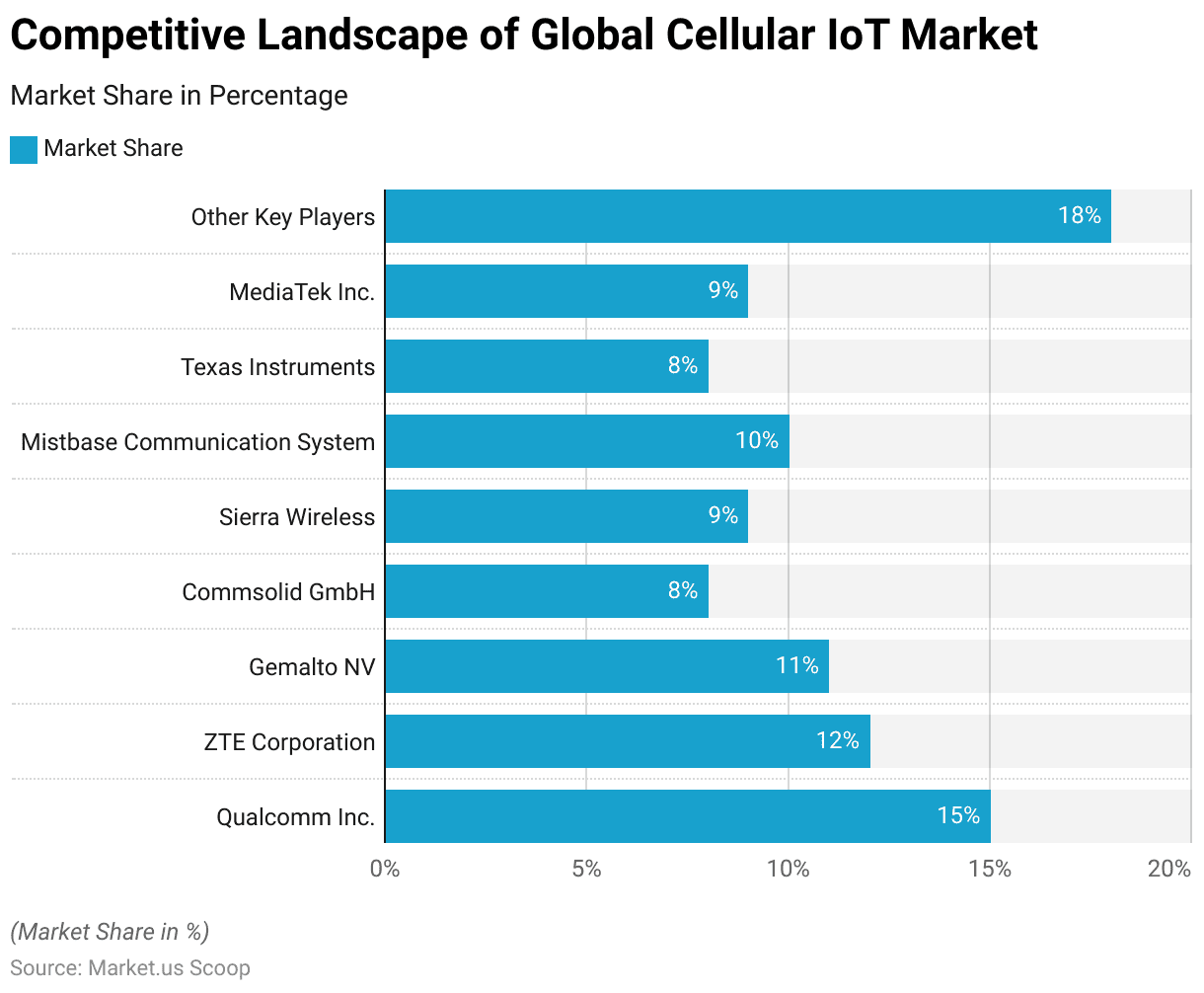

- Significant contributions from several key players characterize the global cellular IoT market.

- Qualcomm Inc. leads the market with a share of 15%, followed closely by ZTE Corporation at 12%.

- Gemalto NV holds 11% of the market, while Mistbase Communication System and MediaTek Inc. each contribute 10% and 9%, respectively.

- Sierra Wireless also commands a 9% market share, and both Commsolid GmbH and Texas Instruments each account for 8%.

- The remaining 18% of the market is distributed among other key players.

- This diverse competitive landscape highlights the broad range of companies driving innovation and growth in the cellular IoT sector.

(Source: market.us)

Regional Analysis of the Global Cellular IoT Market Statistics

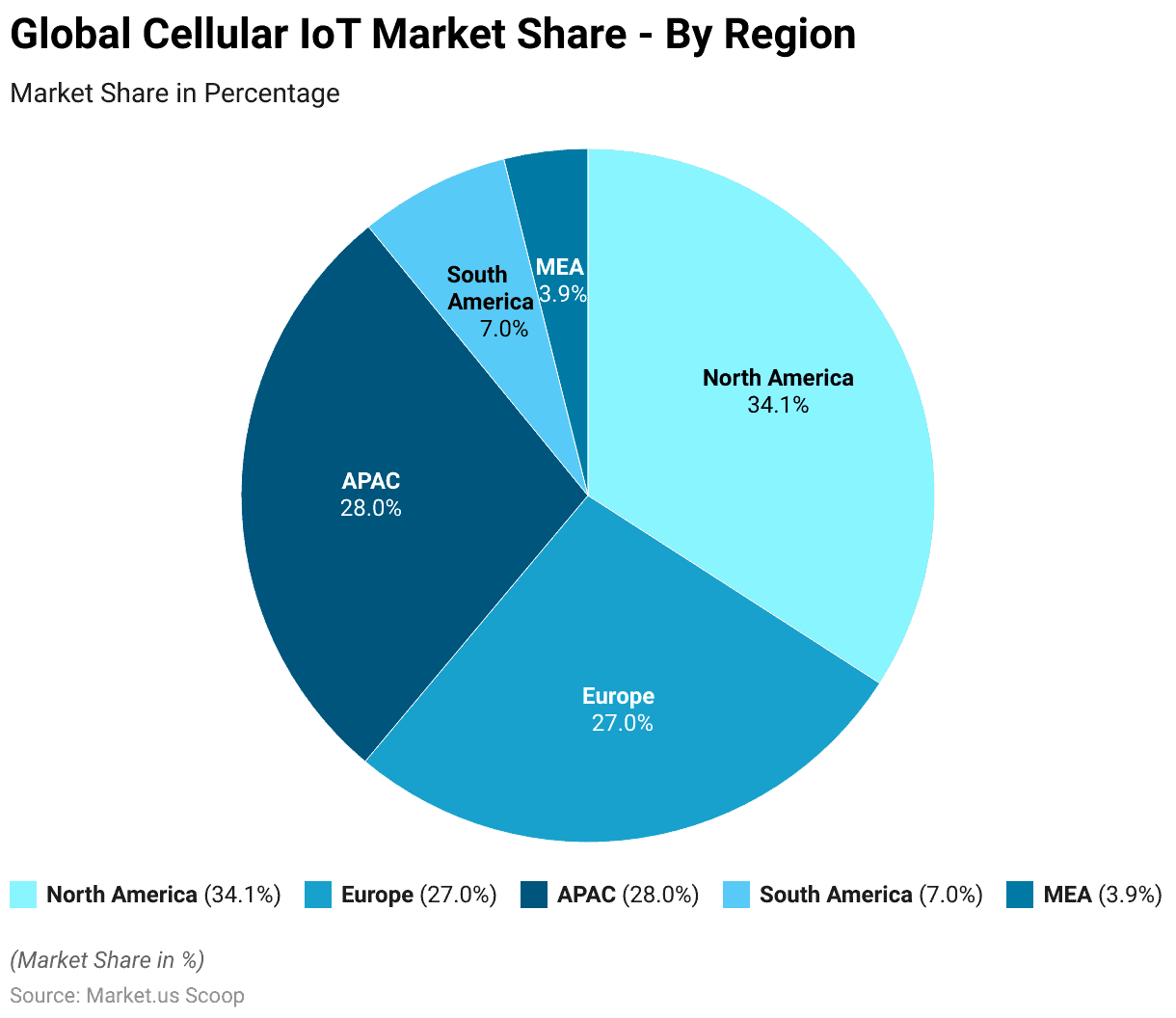

- The global cellular IoT market exhibits varied regional market shares, with North America leading at 34.1%.

- The Asia-Pacific (APAC) region follows closely with a 28.0% share, reflecting its rapid adoption and technological advancements.

- Europe holds a significant portion of the market at 27.0%, driven by strong industrial and consumer IoT applications.

- South America accounts for 7.0% of the market, while the Middle East and Africa (MEA) region represents 3.9%.

- These regional market shares highlight the widespread and growing integration of cellular IoT technologies across the globe.

(Source: market.us)

Technical Specifications of Cellular IoT Statistics

- The technical specifications of cellular IoT are evolving rapidly, driven by advancements in 5G and LTE technologies.

- The cellular IoT ecosystem includes several key technologies, such as 5G Massive IoT (mMTC), 5G RedCap, and 4G LTE Cat-1bis. These technologies offer various capabilities suitable for different applications.

- For instance, LTE Cat 1 provides basic cellular connectivity with data rates of 10 Mbps downlink and 5 Mbps uplink, suitable for low-power, low-cost applications.

- On the other hand, LTE Cat 4 supports higher data rates of 150 Mbps downlink and 50 Mbps uplink, catering to more data-intensive needs.

- 5G technologies are set to dominate the market with 5G Massive IoT supporting extensive device connections with low power consumption and wide coverage.

- The new GSMA eSIM specifications (SGP.31 and SGP.32) enhance remote SIM provisioning. Enabling simplified global connectivity and advanced security features for IoT devices.

- By 2030, the number of cellular IoT connections is projected to reach 5.4 billion. Highlighting the significant transformation and growth in this sector.

(Sources: IoT Business News, IoT for All)

IoT Connections Worldwide

- The projected growth of IoT connections from 2023 to 2029 underscores a significant expansion across various IoT types.

- Wide-area IoT connections are expected to increase from 3.6 billion in 2023 to 7.2 billion in 2029, with a compound annual growth rate (CAGR) of 12%.

- Similarly, cellular IoT connections are projected to grow from 3.4 billion to 6.7 billion over the same period, also reflecting a 12% CAGR.

- Short-range IoT connections are anticipated to see the most substantial growth. Expanding from 12.1 billion in 2023 to 31.6 billion in 2029, with a robust CAGR of 17%.

- Overall, the total number of IoT connections is expected to rise from 15.7 billion in 2023 to 38.8 billion by 2029, achieving a CAGR of 16%.

- This data highlights the rapid proliferation and integration of IoT technologies across various sectors, driving substantial growth in the coming years.

(Source: Ericsson Mobility Report)

Active IoT Devices Statistics

Number of Internet of Things (IoT) Connections Worldwide

- The number of Internet of Things (IoT) connections worldwide is projected to experience substantial growth from 2022 to 2033.

- In 2022, there were 13.8 billion IoT connections globally.

- This number is expected to rise to 15.9 billion in 2023 and further to 18 billion in 2024.

- By 2025, IoT connections are anticipated to reach 20.1 billion. Continuing the upward trend to 22.4 billion in 2026 and 24.7 billion in 2027.

- The growth trajectory remains strong, with projections indicating 27.1 billion connections by 2028, 29.6 billion by 2029, and 32.1 billion by 2030.

- This trend is expected to continue, with IoT connections reaching 34.6 billion in 2031, 37.1 billion in 2032, and ultimately 39.6 billion by 2033.

- This steady increase highlights the rapid and ongoing integration of IoT technologies across various sectors, driving significant connectivity worldwide.

(Source: Statista)

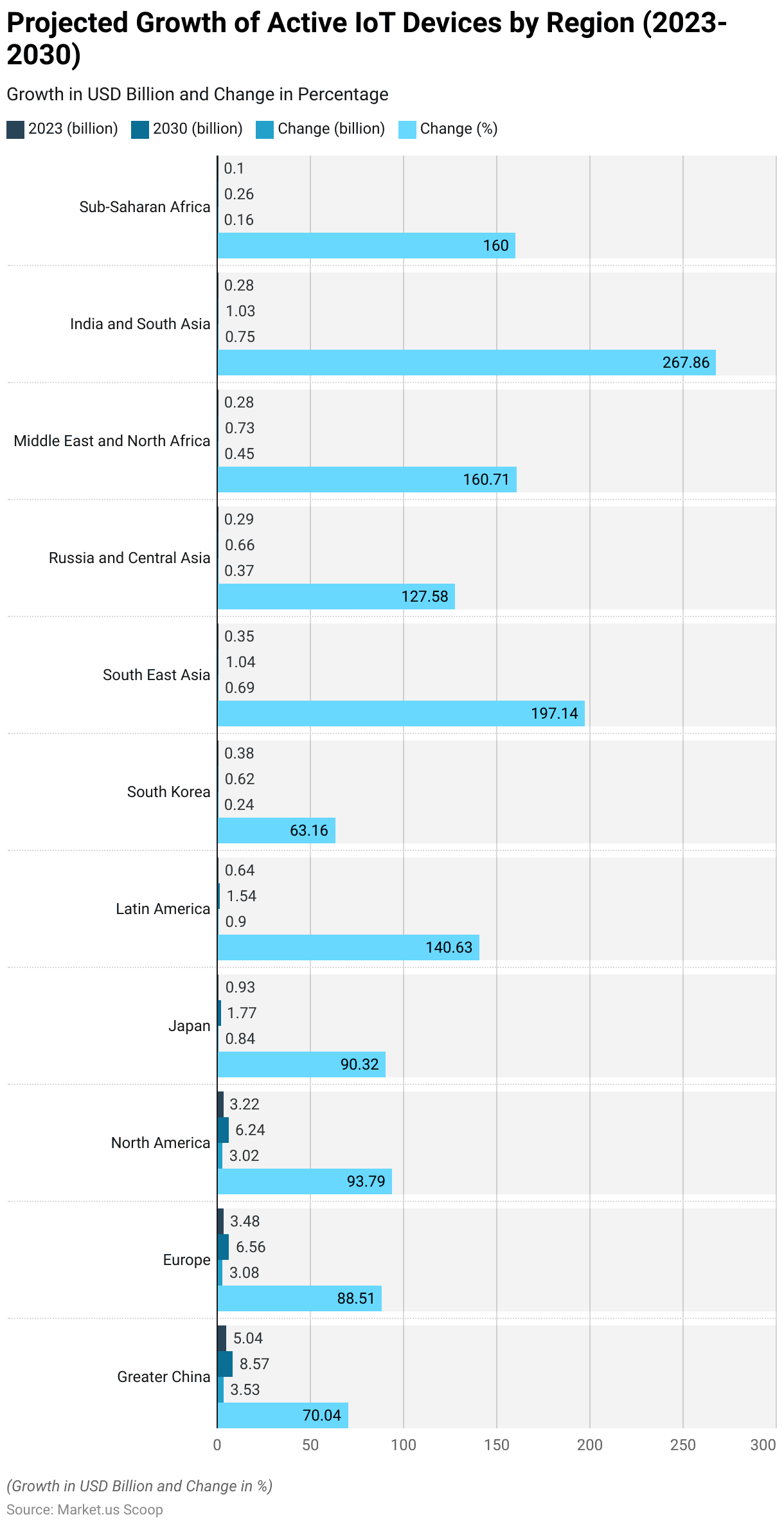

Active IoT Devices- By Region

- The projected growth of active IoT devices from 2023 to 2030 shows substantial increases across various regions.

- Greater China is expected to see its active IoT devices rise from 5.04 billion in 2023 to 8.57 billion by 2030, marking an increase of 3.53 billion devices or 70.04%.

- Europe is projected to grow from 3.48 billion to 6.56 billion devices. A change of 3.08 billion devices or 88.51%.

- North America is anticipated to experience a growth from 3.22 billion to 6.24 billion devices. Reflecting an increase of 3.02 billion devices or 93.79%.

- Japan’s active IoT devices are expected to rise from 0.93 billion to 1.77 billion. An increase of 0.84 billion devices or 90.32%.

- Latin America is projected to grow from 0.64 billion to 1.54 billion devices. An increase of 0.9 billion devices or 140.63%.

- South Korea is expected to see its devices increase from 0.38 billion to 0.62 billion. A growth of 0.24 billion devices or 63.16%.

More Regional Insights

- South East Asia is projected to experience significant growth, with devices increasing from 0.35 billion to 1.04 billion, a change of 0.69 billion devices or 197.14%.

- Russia and Central Asia are expected to grow from 0.29 billion to 0.66 billion devices, an increase of 0.37 billion devices or 127.58%.

- The Middle East and North Africa are projected to rise from 0.28 billion to 0.73 billion devices, a change of 0.45 billion devices or 160.71%.

- India and South Asia are anticipated to see remarkable growth, with devices increasing from 0.28 billion to 1.03 billion, an increase of 0.75 billion devices or 267.86%.

- Finally, Sub-Saharan Africa is projected to grow from 0.1 billion to 0.26 billion devices, reflecting an increase of 0.16 billion devices or 160%.

- This data underscores the widespread and accelerating adoption of IoT technologies globally, with notable growth in both established and emerging markets.

(Source: Transforma Insights)

Cellular IoT Connections Worldwide Statistics

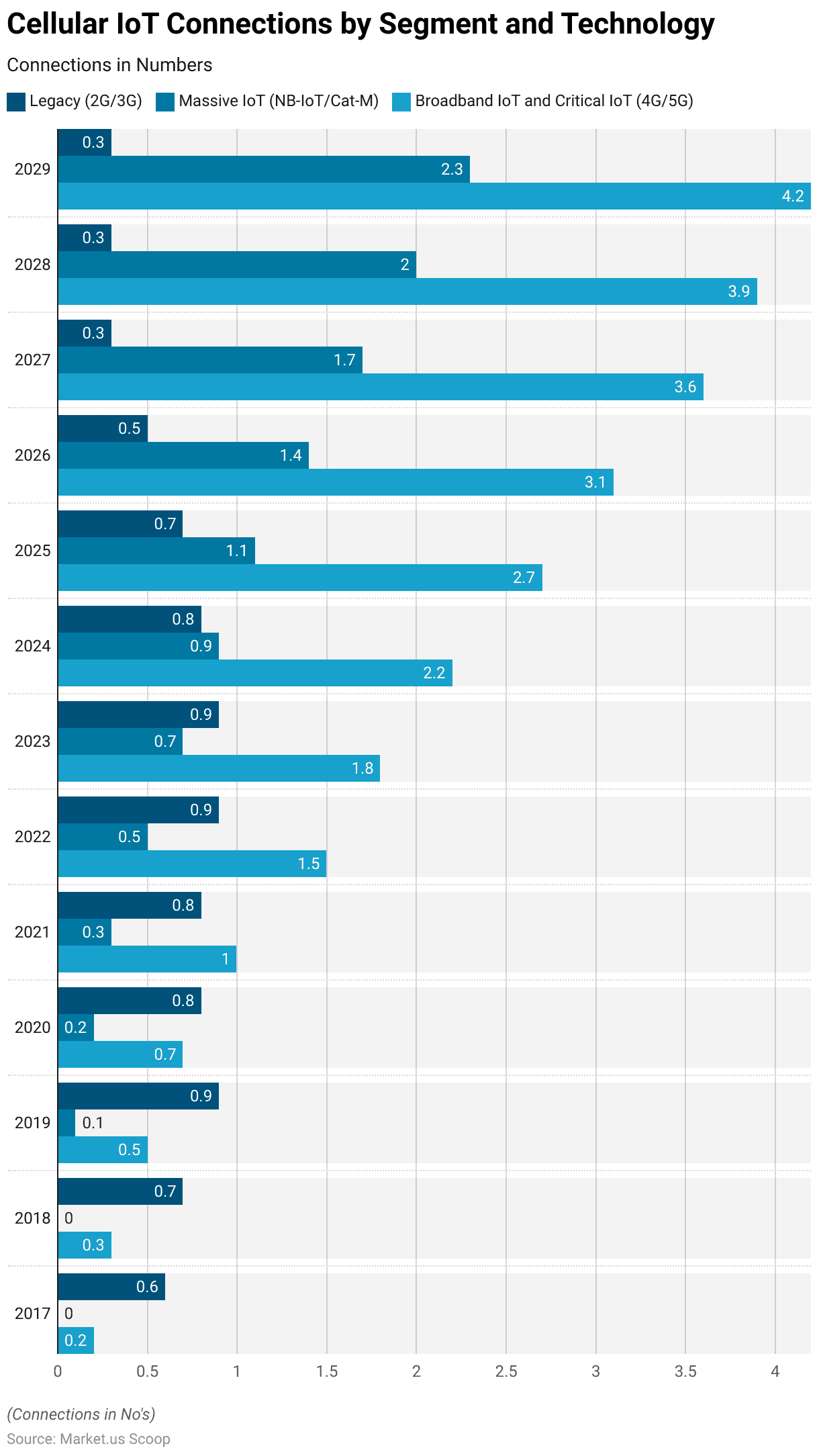

- The evolution of cellular IoT connections by segment and technology from 2017 to 2029 reveals significant trends in the adoption of various IoT technologies.

- Legacy (2G/3G) connections started at 0.6 billion in 2017, reaching a peak of 0.9 billion in 2019 and 2022 before gradually declining to 0.3 billion by 2029.

- In contrast, Massive IoT (NB-IoT/Cat-M) connections began to emerge in 2019 with 0.1 billion connections, showing a consistent increase each year, reaching 2.3 billion by 2029.

- Meanwhile, Broadband IoT and Critical IoT (4G/5G) connections have seen a rapid rise, starting from 0.2 billion in 2017 and growing significantly to 4.2 billion by 2029.

- This data underscores the declining reliance on legacy technologies and the accelerating adoption of advanced IoT technologies, particularly Massive IoT and Broadband/Critical IoT, driven by the increasing deployment of 4G and 5G networks.

(Source: Ericsson Mobility Report)

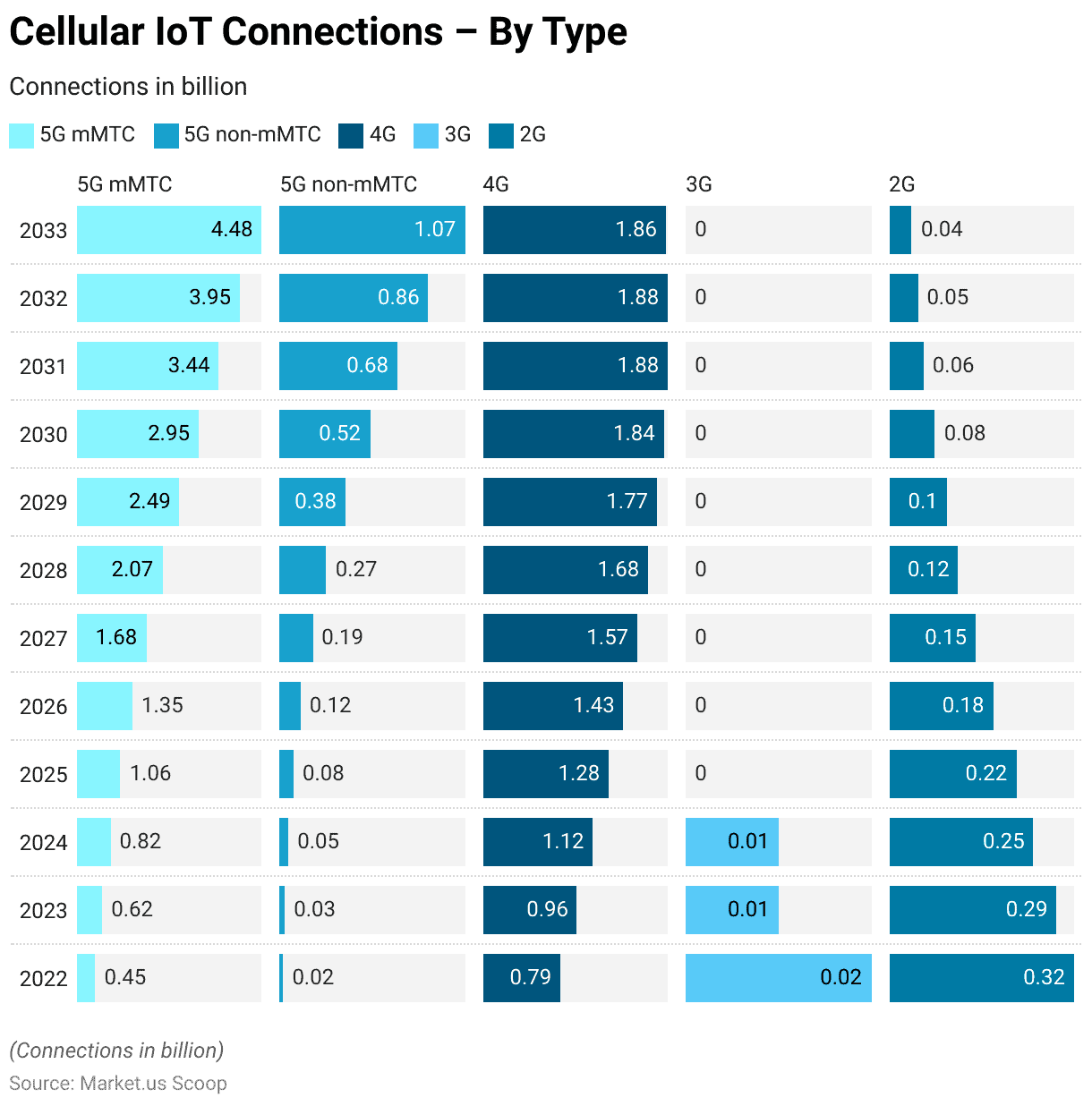

Cellular IoT Connections – By Type Statistics

- The projected growth of cellular IoT connections from 2022 to 2033 highlights the dynamic evolution of various IoT technologies.

- In 2022, 5G mMTC (massive Machine-Type Communications) connections were at 0.45 billion, expected to grow steadily to 4.48 billion by 2033, reflecting a robust adoption rate.

- Similarly, 5G non-mMTC connections, which were at 0.02 billion in 2022, are anticipated to reach 1.07 billion by 2033, indicating significant growth in specialized 5G applications.

- 4G connections, starting at 0.79 billion in 2022, are projected to peak at 1.88 billion by 2031 before slightly declining to 1.86 billion by 2033, suggesting a plateau in 4G adoption as 5G technologies become more prevalent.

- Conversely, 3G connections, which were at 0.02 billion in 2022, are expected to phase out completely by 2025.

- The decline in 2G connections is also notable, from 0.32 billion in 2022 to a mere 0.04 billion by 2033, as newer technologies replace older generations.

- Overall, the data underscores a significant shift towards 5G technologies, both mMTC and non-mMTC, with 4G maintaining a steady presence while 2G and 3G gradually phase out.

(Source: Transforma Insights)

Global Cellular IoT Module Statistics

Cellular IoT Module Shipments Statistics

- In the first quarter of 2022, the global cellular IoT module shipments were predominantly led by Quectel, which held a commanding market share of 38.10%.

- Following Quectel, Fibocom accounted for 8.60% of the market.

- Sunsea and Telit each held shares of 5.70% and 4.60%, respectively, with China Mobile also capturing 4.60%.

- Thales contributed 3.70% to the market, while MEIG and Sierra Wireless each accounted for 3.20%.

- Both Ublox and Foxconn held a share of 2.20% each.

- The remaining 23.90% of the market was distributed among various other vendors.

- This distribution highlights Quectel’s dominant position in the market and the competitive landscape among other significant players.

(Source: Counterpoint Research)

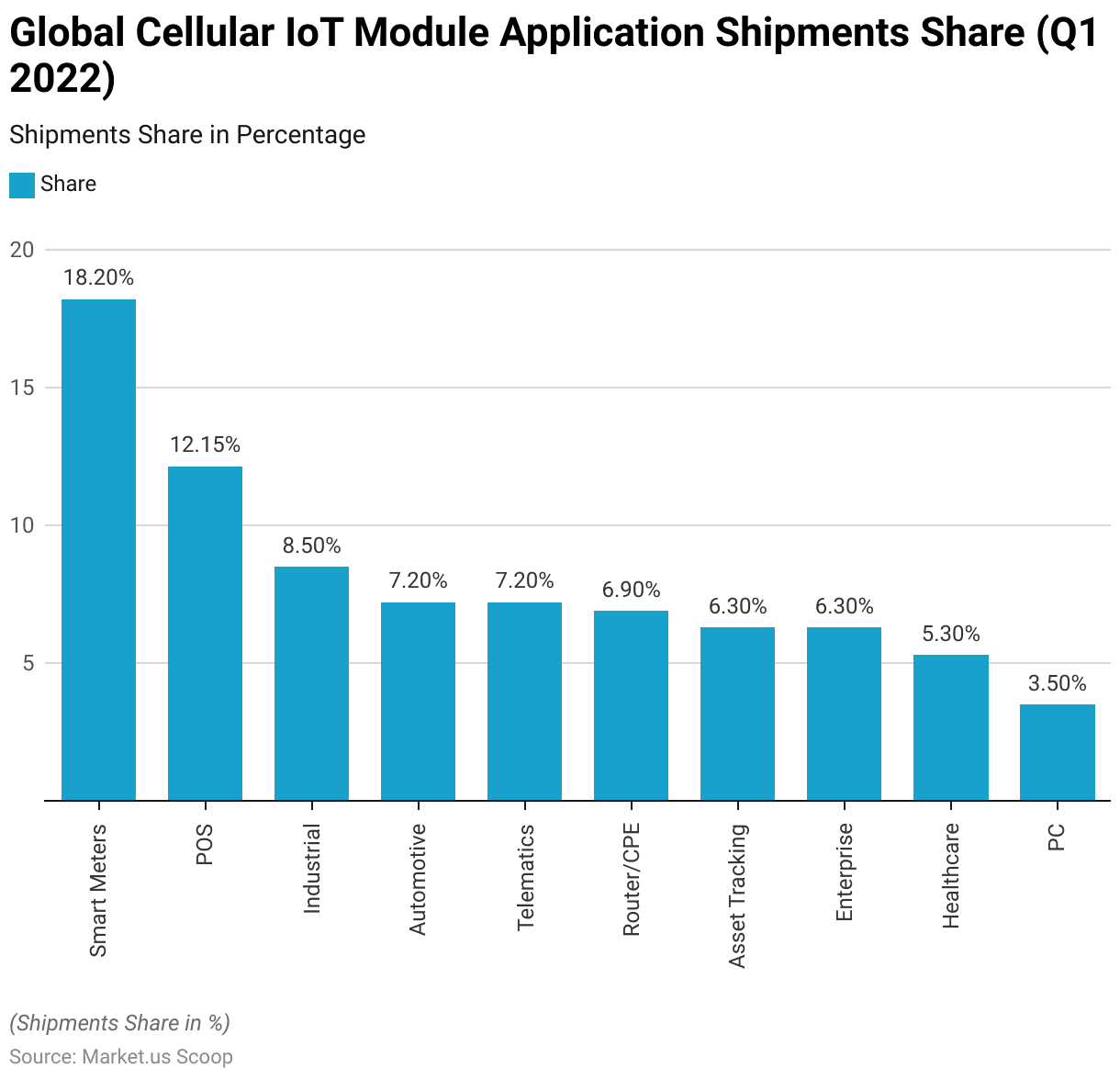

Cellular IoT Module Application Shipments Statistics

- In the first quarter of 2022, the global cellular IoT module application shipments were led by smart meters, which accounted for 18.20% of the market share.

- Point of Sale (POS) systems followed with a 12.15% share.

- The industrial sector captured 8.50% of the market, while both the automotive and telematics segments each held a 7.20% share.

- Router/CPE applications contributed 6.90%, and asset tracking and enterprise applications each accounted for 6.30% of the shipments.

- The healthcare sector had a 5.30% share, while PCs represented 3.50% of the market.

- This distribution highlights the diverse range of applications for cellular IoT modules, with significant adoption across various industries and sectors.

(Source: Counterpoint Research)

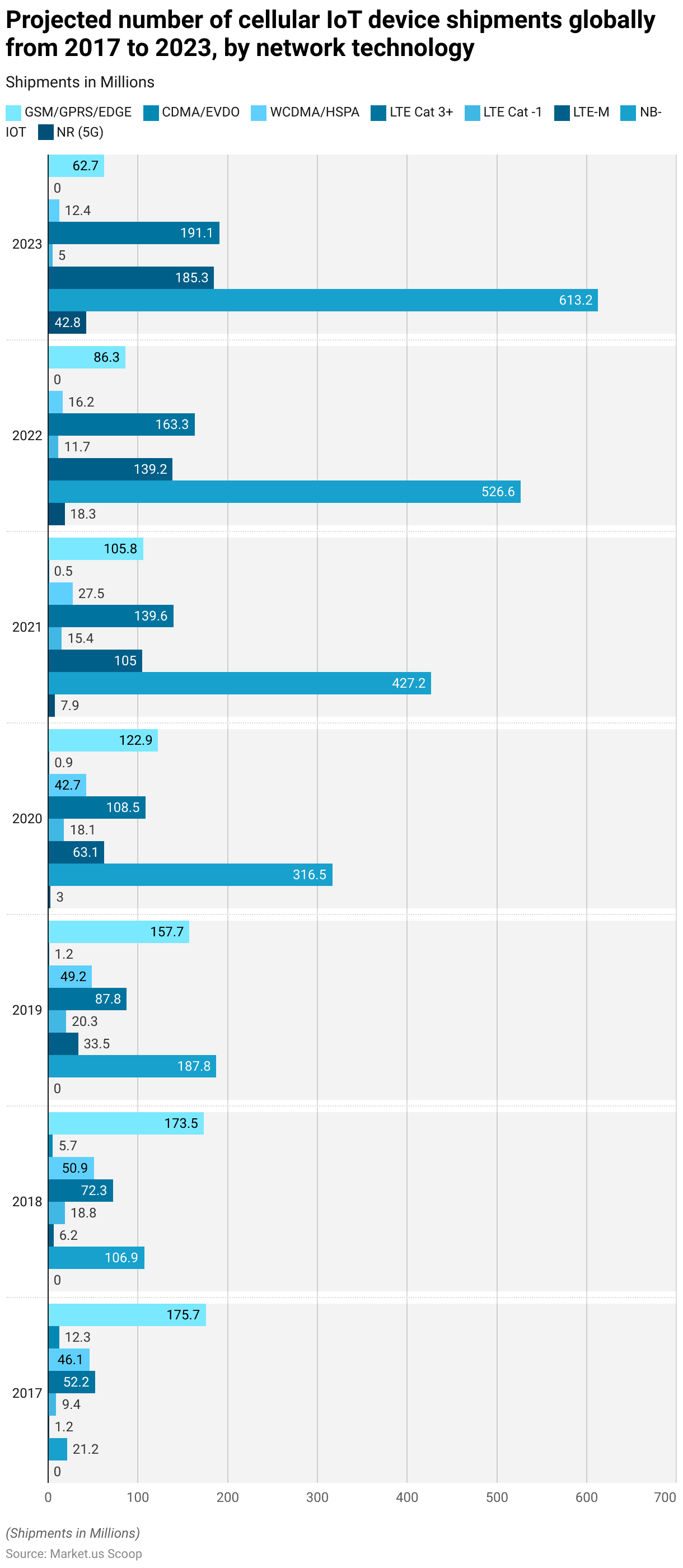

Global Cellular IoT Device Shipments Statistics

- The projected number of cellular IoT device shipments globally from 2017 to 2023, segmented by network technology, reveals significant trends and shifts in adoption.

- In 2017, GSM/GPRS/EDGE technology dominated with 175.7 million shipments, but this number steadily declined to 62.7 million by 2023.

- CDMA/EVDO technology saw a sharp decrease from 12.3 million in 2017 to zero by 2022.

- WCDMA/HSPA shipments also decreased from 46.1 million in 2017 to 12.4 million in 2023.

- Conversely, LTE technologies experienced substantial growth. LTE Cat 3+ shipments increased from 52.2 million in 2017 to 191.1 million by 2023.

- LTE Cat -1 shipments peaked at 20.3 million in 2019 before declining to 5 million in 2023.

- LTE-M technology saw a dramatic rise from 1.2 million shipments in 2017 to 185.3 million in 2023.

- Similarly, NB-IoT technology exhibited exponential growth, from 21.2 million shipments in 2017 to 613.2 million in 2023.

- 5G NR (New Radio) technology, which began shipments in 2020 with 3 million units, is projected to reach 42.8 million shipments by 2023, indicating rapid adoption.

- These trends highlight a clear transition from older network technologies to more advanced LTE and 5G technologies, reflecting the evolving landscape of cellular IoT device connectivity.

(Source: Statista)

Regulations for Cellular IoT

- Regulations for cellular IoT vary significantly by country, addressing cybersecurity, data privacy, and device safety.

- In the European Union, the General Data Protection Regulation (GDPR) mandates stringent data handling procedures to protect personal information. At the same time, the Cybersecurity Act establishes a certification framework to enhance device security. The proposed Cyber Resilience Act aims to embed cybersecurity into the entire lifecycle of IoT products.

- In the United States, the IoT Cybersecurity Improvement Act of 2020 sets security standards for devices used by federal agencies. California’s IoT Security Law requires manufacturers to implement reasonable security features.

- In China, compliance involves several certifications, including the China Compulsory Certificate Mark (CCC) and Network Access License (NAL).

- These diverse regulations reflect the global effort to ensure IoT devices are secure and protect user data across various jurisdictions.

(Sources: Thales Group, IoT for All, IoT Business News, Tellit)

Recent Developments

Acquisitions and Mergers:

- Renesas Electronics acquires Sequans Communications: In August 2023, Renesas agreed to buy Sequans, a France-based cellular IoT chipmaker, for $249 million. The acquisition aims to enhance Renesas’ capabilities in IoT and expand its product offerings in microcontrollers and other devices.

- Renesas completes acquisition of Panthronics AG: In June 2023, Renesas finalized the acquisition of the Austrian fabless semiconductor company specializing in wireless products for approximately $95 million.

New Product Launches:

- 5G and LTE Cat 1 bis modules: The market for 5G modules is experiencing significant growth, with a forecasted 61% increase in revenue for 2024. LTE Cat 1 bis modules are also seeing steady growth, with a 14% revenue increase expected in 2024. These technologies are gaining traction in applications like automotive, smart cities, and asset tracking.

Funding:

- Investment in AI and IoT convergence: There is an increasing trend of integrating AI capabilities with IoT devices, particularly at the edge. This convergence is attracting significant investment and opening new applications in areas like machine vision and predictive maintenance.

Market Dynamics:

- China’s Influence: China accounts for 54% of the global cellular IoT module market, with a 23% revenue growth in Q1 2024. This growth has been pivotal in swinging the overall market revenue back into positive territory, despite declines in other regions.

- Top Companies: The top five companies in the cellular IoT module market by revenue are Quectel, Fibocom, Telit Cinterion, China Mobile, and LG Innotek, accounting for 60% of the market. Quectel leads with a 31% market share and a 19% YoY growth in Q1 2024.

Technological Trends:

- Generative AI in IoT: There is a significant push towards developing generative AI-based solutions for industrial applications, including operational analytics and design automation. This trend is expected to drive further investment and innovation in the IoT space.

- Private 5G Networks: The adoption of private 5G networks is increasing due to their advantages in reliability and cybersecurity over traditional Wi-Fi networks. This trend is driving growth in the deployment of 5G modules.

Regulatory Developments:

- Sustainability Reporting: New regulations, such as the EU’s Corporate Sustainability Reporting Directive (CSRD), require companies to provide detailed reports on environmental and social risks. This is driving the adoption of IoT solutions for monitoring and reporting sustainability metrics (IoT Analytics).

Conclusion

In conclusion, the Cellular IoT market is rapidly expanding, driven by advancements in cellular network technologies such as NB-IoT, LTE-M, and 5G.

These technologies offer extensive coverage, scalability, and robust security features, making them ideal for a wide range of applications, from smart meters and vehicle telematics to health monitoring and smart city infrastructure.

The regulatory landscape for Cellular IoT is complex and varies by region, with significant efforts in the EU, US, and China to enhance cybersecurity and data privacy.

Despite challenges related to security, interoperability, and regulatory compliance, the future outlook remains positive, with projections indicating a substantial increase in the number of cellular IoT connections worldwide, reaching 5.4 billion by 2030.

As the market continues to grow, businesses and regulators must collaborate to address these challenges, ensuring secure, reliable, and efficient IoT deployments.

FAQs

What is Cellular IoT?

Cellular IoT refers to the use of cellular networks to connect IoT devices. These devices leverage existing cellular infrastructure (e.g., 4G LTE, 5G) to communicate data to and from a central server. This connectivity enables a wide range of applications, including smart cities, connected vehicles, and industrial automation.

How does Cellular IoT ensure device interoperability?

Cellular IoT ensures device interoperability through the use of standardized communication protocols and technologies. Organizations such as the 3rd Generation Partnership Project (3GPP) develop these standards, which ensure that devices from different manufacturers can communicate seamlessly within the same network.

What is the role of SIM cards in Cellular IoT?

SIM cards in Cellular IoT devices provide secure authentication and network access. They store the device’s identity and subscription information, enabling it to connect to the cellular network. eSIM (embedded SIM) technology is increasingly being used in IoT devices to offer greater flexibility and ease of management.

Can Cellular IoT be used in remote and rural areas?

Yes, Cellular IoT can be used in remote and rural areas. Technologies like NB-IoT and LTE-M are designed to offer extended coverage, making them suitable for applications such as agricultural monitoring, remote infrastructure management, and wildlife tracking in areas with limited connectivity.

What are the regulatory requirements for Cellular IoT?

Regulatory requirements for Cellular IoT vary by region and include compliance with spectrum allocation, network access regulations, and data protection laws. IoT device manufacturers and service providers must ensure their products comply with local telecommunications regulations and standards.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)