Table of Contents

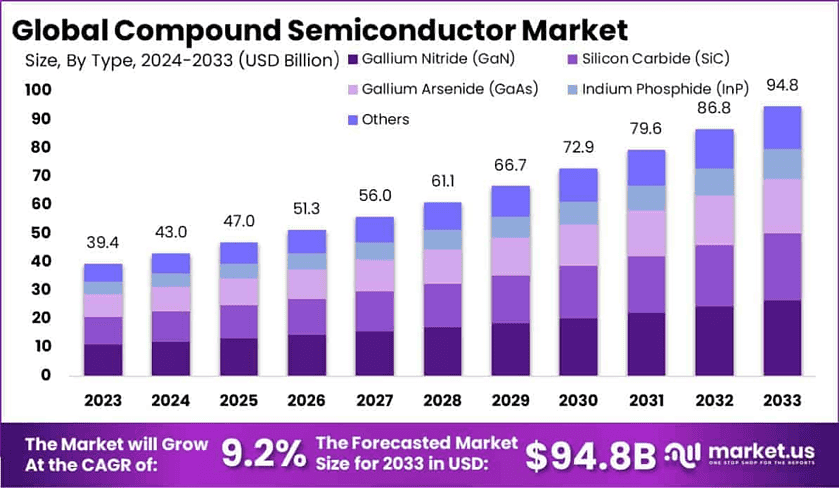

The Global Compound Semiconductor Market is expected to grow from USD 39.4 billion in 2023 to USD 94.8 billion by 2033, expanding at a CAGR of 9.2% during the forecast period (2024–2033). This growth is driven by increasing demand for high-performance semiconductor materials used in 5G technology, LED lighting, solar cells, and power electronics.

Gallium Nitride (GaN) led the market in 2023, capturing 28% of the market share, primarily due to its superior power efficiency in electronic devices. LED products dominated the product segment with a 35% share, driven by the growing demand for energy-efficient lighting solutions.

The IT and Telecom sector held a 40% share in the application segment in 2023, reflecting the importance of compound semiconductors in 5G communication, data centers, and telecommunications infrastructure. Asia-Pacific led the global market, holding a 55% share in 2023 and generating USD 21.68 billion in revenue.

This region benefits from a strong manufacturing base and rapid technological advancements in the telecom and LED industries. The increasing adoption of electric vehicles and renewable energy technologies further fuels the market, making compound semiconductors essential for the development of advanced power electronics and efficient energy systems.

US Tariff Impact on Market

U.S. tariffs on semiconductor materials and components, especially from Asia-Pacific suppliers, have introduced price inflation in the compound semiconductor market. Tariffs of 10% to 25% on components like Gallium Nitride (GaN) and LED materials have led to a 7-10% increase in production costs. According to USITC and SEMI, this price hike affects the IT and Telecom sectors, which are highly dependent on cost-efficient compound semiconductors for 5G infrastructure and telecom equipment. As a result, U.S. companies are turning toward alternative sourcing and local production to mitigate tariff impacts and maintain competitive pricing.

Economic, Geographical, and Business Impact

- Economic Impact: Tariffs have led to a 7-10% increase in costs for GaN and LED materials, increasing prices in 5G telecom and power electronics sectors.

- Geographical Impact: Asia-Pacific faces reduced exports to the U.S., encouraging companies to explore domestic manufacturing in Mexico and Vietnam to bypass tariffs.

- Business Impact: U.S.-based companies are investing in local semiconductor manufacturing to counteract the tariffs and ensure supply chain resilience. However, smaller firms with fewer resources face margin pressures, while larger firms are adopting automation and R&D investments to reduce long-term dependency on imported materials.

➤ Want to see industry trends in action? Request a sample of our research report @ https://market.us/report/compound-semiconductor-market/free-sample/

Key Takeaways

- Market expected to grow from USD 39.4 Bn (2023) to USD 94.8 Bn (2033) at 9.2% CAGR.

- Gallium Nitride (GaN) leads the type segment with 28% share.

- LED products dominate the product segment with 35% share.

- IT and Telecom hold 40% of the application segment.

- Asia-Pacific holds 55% share, driven by semiconductor manufacturing.

- U.S. tariffs have increased costs by 7–10% for key materials.

Analyst Viewpoint

The compound semiconductor market is on a strong growth path, fueled by increasing demand for high-efficiency materials in 5G telecom, LED lighting, and electric vehicles. While U.S. tariffs have introduced short-term challenges, particularly in GaN and LED segments, these are also driving innovations in local production and supply chain resilience.

Looking ahead, the growing focus on renewable energy and energy-efficient technologies will continue to bolster demand. Asia-Pacific’s leadership in manufacturing and technological advancements will remain key to market growth. The future is bright, driven by advanced semiconductor applications in various industrial sectors.

Regional Analysis

Asia-Pacific leads the compound semiconductor market with a 55% share in 2023, benefiting from strong manufacturing capabilities in China, Japan, and South Korea. The region’s dominance is further fueled by its telecommunications, LED, and power electronics industries, which rely heavily on compound semiconductors.

North America, particularly the U.S., is expanding its semiconductor capabilities, focusing on domestic production to counteract tariff impacts. Europe is growing steadily, particularly in automotive and energy-efficient electronics sectors. Southeast Asia is emerging as a cost-effective manufacturing hub due to favorable labor costs and increasing investment in semiconductor R&D.

➤ 𝐄𝐱𝐩𝐥𝐨𝐫𝐞 𝐈𝐧𝐭𝐞𝐫𝐞𝐬𝐭𝐞𝐝 𝐓𝐨𝐩𝐢𝐜𝐬

- Mobile Payment Market

- Sports Online Live Video Streaming Market

- Digital Accessibility Software Market

- Writing Enhancement Software Market

Business Opportunities

The compound semiconductor market offers substantial opportunities across telecommunications, power electronics, LEDs, and automotive sectors. As 5G adoption accelerates, demand for GaN-based semiconductors in telecom infrastructure and data centers is expected to rise. Additionally, the shift toward electric vehicles and renewable energy creates demand for high-performance semiconductors in power management.

Companies focusing on energy-efficient LED lighting, low-loss power devices, and innovative packaging will benefit from market expansion. Furthermore, the nearshoring trend presents new opportunities for semiconductor manufacturers in North America and Southeast Asia, offering growth potential in emerging markets.

Key Segmentation

The compound semiconductor market is segmented by type, product, application, and region. In 2023, Gallium Nitride (GaN) led the type segment with 28% share, driven by its use in power electronics. LED products dominated the product segment with 35% share. The IT and Telecom sector led applications with 40% share due to 5G and telecommunications demand. Regionally, Asia-Pacific remains dominant with 55% market share, supported by advanced semiconductor manufacturing and strong demand across various industries.

Key Player Analysis

Key players in the compound semiconductor market are focusing on GaN technology, advanced packaging solutions, and high-efficiency LED materials. Companies are investing heavily in research and development to improve semiconductor performance and reduce power consumption.

Strategic partnerships with telecommunications, automotive, and renewable energy firms are key to meeting growing demand. Expansion into low-cost regions like Southeast Asia is also a priority to mitigate tariff impacts, while innovation in sustainable technologies is becoming a key differentiator in the competitive landscape.

Top Key Players in the Market

- NXP Semiconductors

- Qorvo Inc.

- STMicroelectronics

- Wolfspeed Inc.

- Infineon Technologies AG

- Samsung Electronics Co Ltd

- Texas Instruments Inc.

- Nichia Corporation

- Taiwan Semiconductor Manufacturing Company Limited

- Renesas Electronics Corporation

- Other Key Players

Recent Developments

Recent developments include new innovations in GaN technology for 5G applications, expansion of semiconductor fabrication in Southeast Asia to avoid tariffs, and partnerships for LED efficiency improvements. Companies are also exploring eco-friendly semiconductor materials to meet global sustainability goals, while expanding into emerging markets for growth opportunities.

Conclusion

The compound semiconductor market is poised for strong growth, driven by demand in 5G, LEDs, and electric vehicles. Despite tariff-related challenges, innovations in GaN technology, energy efficiency, and local production will continue to propel market expansion. As industries evolve, compound semiconductors will be integral to future technological advancements.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)