Table of Contents

The Global Cybersecurity in EdTech Market is projected to experience significant growth, reaching USD 243 billion by 2034, up from USD 36 billion in 2024, with a CAGR of 21.2%. North America dominated the market in 2024, holding 40.2% of the share and generating USD 14.4 billion in revenue.

The U.S. market, contributing USD 12.31 billion, is expected to grow at a robust CAGR of 22.3%. In 2024, the hardware segment led the market, accounting for 47.4% of the total share, while endpoint security captured over 35.9%. The K-12 segment emerged as the largest end-user, holding more than 41.5% of the market share.

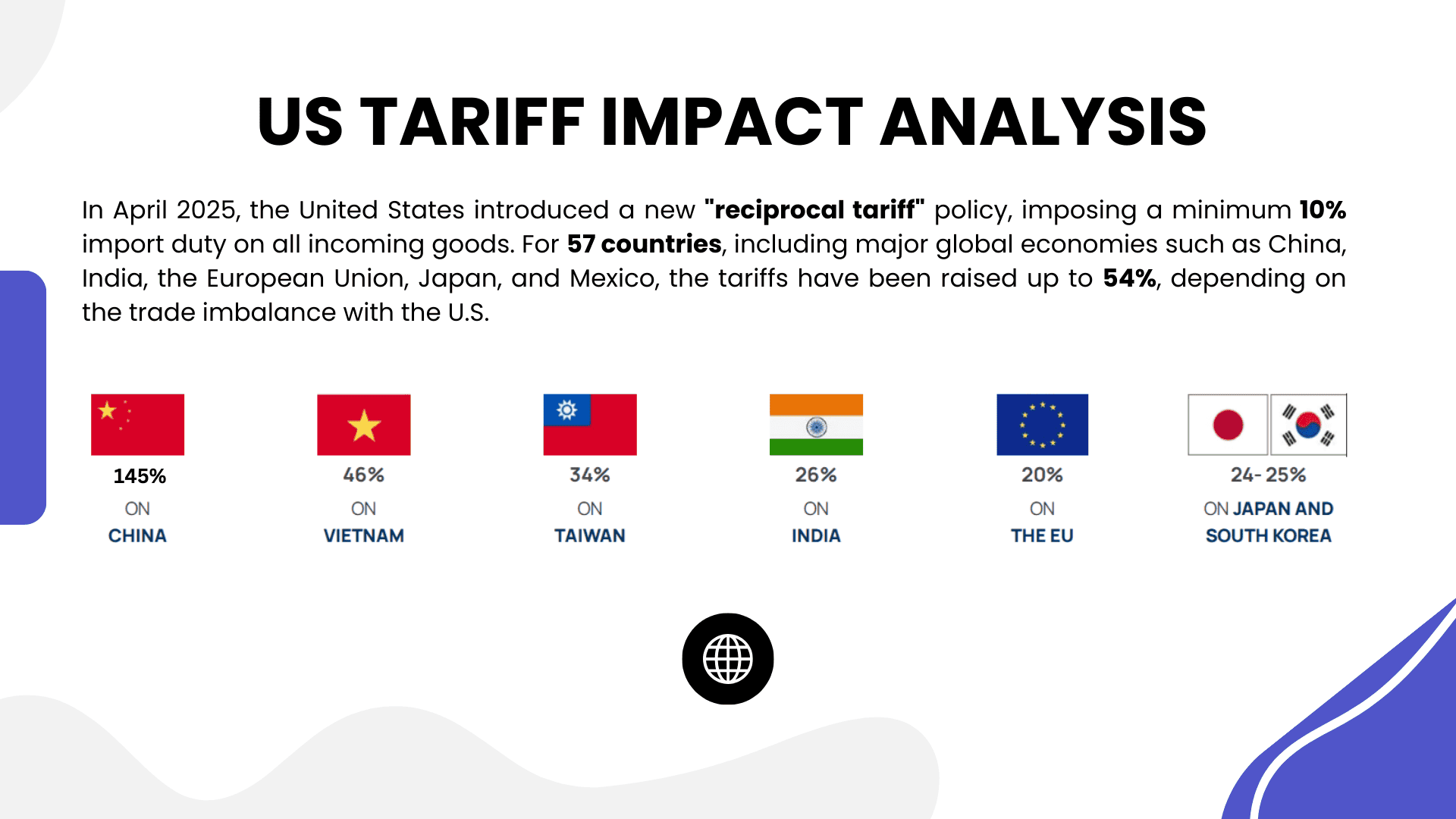

US Tariff Impact on Market

US tariffs on imported hardware components and cybersecurity solutions could drive up the overall cost of EdTech cybersecurity systems. This may affect large enterprises and K-12 institutions, which account for the majority of the market.

The hardware segment, which dominated the global market in 2024 with a 47.4% share, is likely to face increased prices for essential components such as servers, routers, and security devices due to tariffs. As a result, the cost of implementing cybersecurity solutions in educational institutions could rise, potentially slowing down adoption.

However, the growing need for cybersecurity, especially in the K-12 segment, may offset these short-term challenges, as educational institutions remain committed to safeguarding their digital environments. While tariffs may have some impact, the overall market growth driven by increasing demand for cybersecurity in EdTech remains strong.

US Tariff Impact on Sectors

- Hardware: 6%-8%

- Endpoint Security: 4%-6%

- On-premises Deployment: 3%-5%

Economic Impact

Tariffs could lead to increased costs for hardware components and cybersecurity solutions, raising the overall price of cybersecurity systems in EdTech. This may limit affordability for smaller institutions, especially in the K-12 sector, slowing down adoption and affecting market growth in the short term.

Geographical Impact

North America, particularly the U.S., will be significantly impacted by tariffs, as the region relies heavily on imported hardware and software for cybersecurity solutions. Increased costs could slow down the adoption of advanced cybersecurity systems in educational institutions, particularly in the public sector, where budgets are more constrained.

Business Impact

Cybersecurity solution providers in the U.S. may face higher operational costs due to tariffs on imported hardware. This could lead to increased product prices and potentially lower demand for these solutions, especially from smaller educational institutions or those operating under tight budgets, affecting overall business profitability in the short term.

➤➤ Request sample reflecting US tariffs @ https://market.us/report/cybersecurity-in-edtech-market/free-sample/

Key Takeaways

- The global Cybersecurity in EdTech market is expected to reach USD 243 billion by 2034.

- North America holds over 40.2% of the market share, generating USD 14.4 billion in 2024.

- The hardware segment accounted for 47.4% of the total market share in 2024.

- US tariffs could increase the cost of cybersecurity solutions, slowing adoption in the K-12 sector.

Analyst Viewpoint

The EdTech cybersecurity market is poised for strong growth, driven by increasing concerns over data breaches and the need for secure online learning environments. While US tariffs could lead to short-term price increases, long-term demand for robust cybersecurity solutions remains strong.

Educational institutions, particularly in the K-12 segment, will continue to prioritize securing their digital assets, driving the adoption of advanced cybersecurity technologies. With a continued focus on improving cybersecurity infrastructure in schools and universities, the market is likely to see steady growth in the coming years, despite challenges posed by tariffs.

Regional Analysis

North America, particularly the U.S., is the dominant region in the Cybersecurity in EdTech market, accounting for 40.2% of the global market share in 2024, generating USD 14.4 billion in revenue. This growth is driven by the widespread adoption of digital learning platforms and increasing concerns about cyber threats in educational settings.

The K-12 sector in the U.S. continues to be the largest end-user, with institutions investing heavily in cybersecurity solutions to protect student data. Europe and Asia-Pacific are also expected to experience rapid growth, with a focus on strengthening cybersecurity measures as online learning becomes more prevalent in these regions.

Impact of U.S. tariffs on these sectors?

- Over The Top (OTT) Market

- Large Language Model Powered Tools Market

- Network Management System Market

- AI Orchestration Platform Market

Business Opportunities

The Cybersecurity in EdTech market offers significant business opportunities, especially for companies providing advanced cybersecurity solutions tailored for educational institutions. With rising concerns about data privacy, companies can capitalize on the increasing demand for endpoint security, network security, and data protection solutions.

The K-12 segment, representing more than 41.5% of the market, presents a lucrative opportunity for cybersecurity providers, as educational institutions strive to secure their digital platforms. Additionally, the shift towards on-premises deployment models, which accounted for 62.6% of the market share in 2024, provides an opportunity for businesses to offer localized, scalable security solutions for schools and universities.

Key Segmentation

The Cybersecurity in EdTech market is segmented by hardware, security solutions, deployment model, and end-user:

- Hardware Segments: Servers, Routers, Security Devices.

- Security Solutions: Endpoint Security, Network Security, Cloud Security.

- Deployment Models: On-premises, Cloud-based.

- End-Users: K-12, Higher Education, Private Institutions.

In 2024, hardware accounted for 47.4% of the market share, with endpoint security leading at 35.9%. The on-premises deployment model continued to be preferred, representing 62.6% of the market, while the K-12 sector maintained the largest share at over 41.5%. This segmentation highlights the importance of secure, scalable, and localized cybersecurity solutions in the education sector.

Key Player Analysis

Key players in the Cybersecurity in EdTech market are focusing on providing comprehensive security solutions that cater to the unique needs of educational institutions. Companies are enhancing their product offerings with AI-powered security tools, advanced endpoint protection, and integrated solutions for data privacy and compliance.

Many are investing heavily in research and development to create more efficient, cost-effective solutions for the K-12 sector, which is highly sensitive to budget constraints. Partnerships with educational institutions are critical for market penetration, and companies are increasingly focusing on developing user-friendly interfaces that facilitate adoption in schools and universities.

Recent Developments

In 2024, a major cybersecurity provider launched a new cloud-based endpoint security solution specifically designed for educational institutions, offering improved data protection and real-time threat monitoring. This solution is expected to increase security compliance in schools and help mitigate growing cyber risks in the education sector.

Conclusion

The Cybersecurity in EdTech market is set for impressive growth, driven by increasing concerns about the security of digital learning environments. While tariffs may pose short-term challenges, the long-term demand for cybersecurity solutions in educational institutions remains strong. Continued innovations in security technology and increasing adoption in K-12 and higher education will support the market’s expansion.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)