Table of Contents

The Global Data Center Chip Market is projected to reach USD 57.9 billion by 2033, growing from USD 14.3 billion in 2023 at a CAGR of 15.0%. The GPU segment dominates the chip type segment, accounting for 32.2% in 2023, driven by its key role in accelerating data processing.

Large data centers, representing 64.1% of the market share, are the leading consumers of data center chips, fueled by increasing data demand and processing needs. The BFSI sector, with 23.0% of the market share, continues to be a major contributor due to its high data security and processing requirements. North America holds the largest market share at 38.4%, driven by strong demand for advanced data center infrastructure.

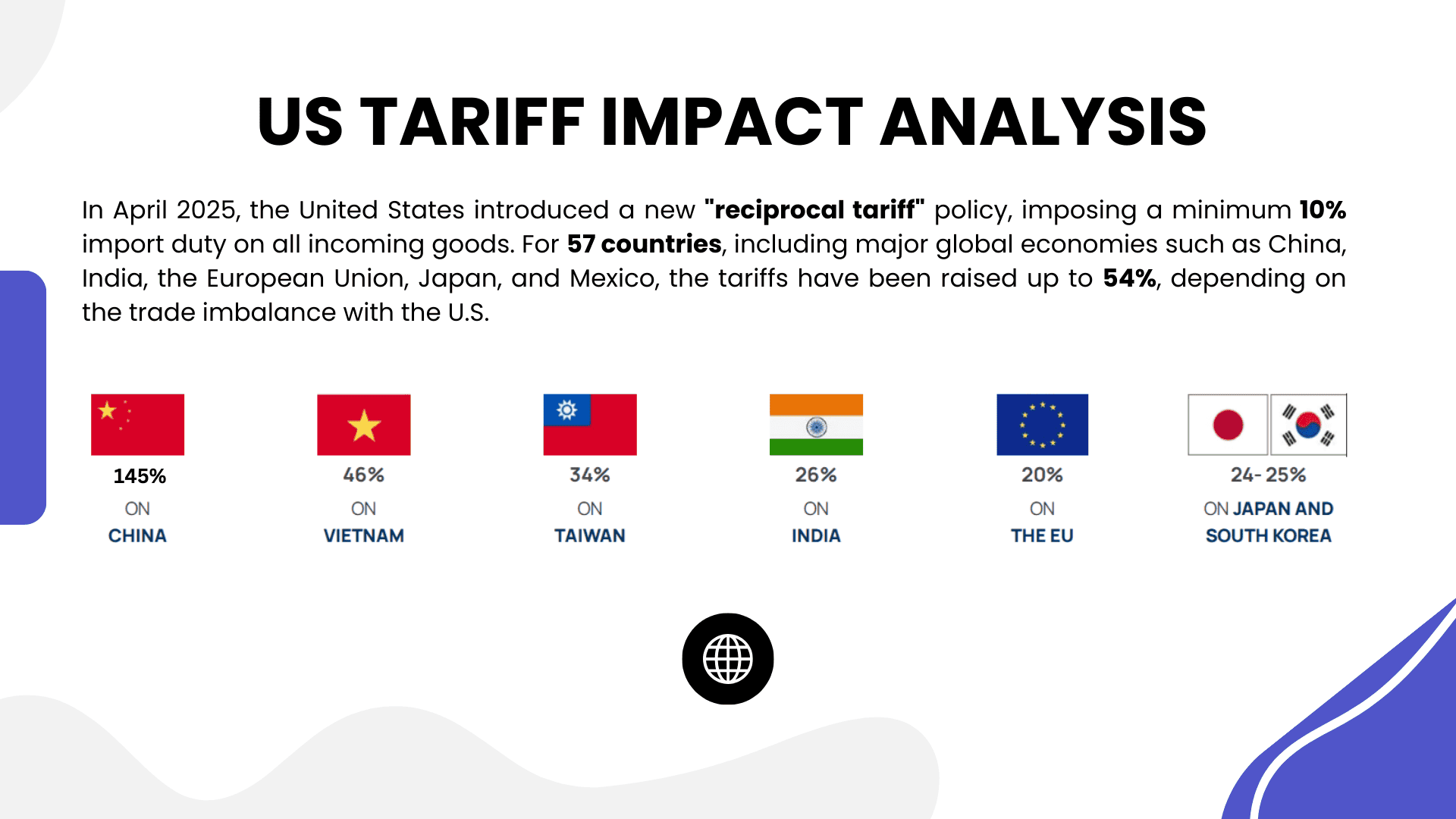

US Tariff Impact on Market

US tariffs on semiconductor components used in data center chips could impact the overall cost of production. As the demand for GPUs and other advanced chips used in data centers grows, tariffs on components such as processors, memory units, and storage chips could raise production costs.

This price increase may be passed onto end consumers, particularly large data centers, which account for 64.1% of the market. Given the growing importance of data processing in sectors like BFSI (which accounts for 23.0% of the market), these tariffs could slow down investments in upgrading existing infrastructure.

While the North American market currently leads, the rising costs could lead to increased competition from global manufacturers, reducing the market share in the U.S. However, as demand for high-performance computing continues, these short-term challenges may be offset by long-term growth driven by the increasing reliance on cloud services and data-intensive applications.

US Tariff Impact on Sectors

- GPU Chips: 4%-6%

- Data Center Chips (General): 5%-7%

- Semiconductor Components: 3%-5%

Economic Impact

Tariffs on semiconductor components could increase production costs for data center chips, raising prices across sectors, particularly in large data centers. This would impact enterprises relying on large-scale data storage and processing, particularly in high-demand sectors like BFSI, potentially slowing the pace of infrastructure upgrades and investments.

Geographical Impact

North America, which currently leads the market with 38.4% share, may face slowed growth due to higher prices caused by tariffs on imported components. The U.S. could experience reduced competitiveness in the global market, as manufacturers in other regions with fewer tariffs could offer more affordable alternatives.

Business Impact

Businesses in the data center chip sector may face lower profit margins due to increased production costs from tariffs. Companies might be forced to pass the increased costs onto customers, which could affect demand, particularly among smaller enterprises or those in price-sensitive industries, potentially slowing market growth.

➤➤ Request sample reflecting US tariffs @ https://market.us/report/data-center-chip-market/free-sample/

Key Takeaways

- The data center chip market is projected to reach USD 57.9 billion by 2033.

- GPU chips dominate with 32.2% market share in 2023, driving data processing.

- Large data centers account for 64.1% of market share, reflecting their critical role in data storage and management.

- US tariffs could increase component costs, potentially slowing the adoption of data center chips, especially in the BFSI sector.

Analyst Viewpoint

The data center chip market is experiencing strong growth, driven by increasing demand for high-performance chips in large data centers and sectors like BFSI. While US tariffs could temporarily raise costs, the long-term outlook remains positive, with continued growth fueled by the rise of cloud computing, AI, and big data applications.

The need for efficient, scalable, and high-performance data center infrastructure will continue to drive the market, even as global competition increases. As the data center industry evolves, innovations in chip design and efficiency will help sustain long-term growth despite short-term challenges posed by tariffs.

Regional Analysis

North America dominated the data center chip market in 2023, accounting for 38.4% of the market share, valued at USD 5.5 billion. The U.S. continues to lead due to its advanced data center infrastructure and growing demand for high-performance chips, particularly for large-scale cloud computing services.

While North America remains the dominant region, growth is also accelerating in Europe and Asia-Pacific, driven by the increasing adoption of data center technology in emerging economies. As the demand for AI, IoT, and big data applications continues to grow, other regions are expected to increase their share in the global market.

➤ Tariff effects on listed markets?

Business Opportunities

The data center chip market offers substantial business opportunities for manufacturers focused on high-performance, energy-efficient solutions. As cloud computing, AI, and edge computing gain traction, the demand for chips with enhanced processing power and low latency will continue to grow.

Companies that specialize in GPUs, memory chips, and storage solutions are well-positioned to benefit from this trend. Additionally, with the increasing shift to hybrid cloud and the expansion of data centers in emerging markets, there is an opportunity to provide cost-effective, scalable chip solutions that meet the evolving needs of modern data centers. Strategic partnerships with cloud service providers will also drive growth.

Key Segmentation

The data center chip market is segmented by chip type, application, and region:

- Chip Types: GPU Chips, CPU Chips, Memory Chips, Storage Chips.

- Application Segments: Large Data Centers, Small Data Centers, Edge Computing.

- Geographical Segments: North America, Europe, Asia-Pacific, Rest of the World.

In 2023, GPU chips dominated the chip type segment with 32.2% market share. Large data centers held a dominant position in the market, capturing 64.1% of the share. The BFSI sector continued to lead the industry vertical segment, with 23.0% market share, as it increasingly relies on secure and high-performance data processing solutions. North America continues to be the largest region, followed by significant growth in Asia-Pacific.

Key Player Analysis

Key players in the data center chip market are focusing on developing high-performance chips designed for large-scale data centers and emerging technologies such as AI and edge computing. Companies are investing in R&D to enhance processing power, reduce energy consumption, and improve chip efficiency to meet the evolving needs of modern data centers.

Partnerships with cloud providers, IT companies, and other industries are crucial for capturing larger market shares. Manufacturers are also exploring new technologies, such as 5G and AI-optimized chips, to stay ahead of market trends. With increasing competition, offering cost-effective, scalable solutions remains a key competitive advantage.

Recent Developments

In 2024, a leading data center chip manufacturer introduced a new GPU designed for AI applications, offering faster processing and lower power consumption. This innovation is expected to increase demand in sectors like AI, machine learning, and cloud computing, helping data centers optimize their operations and reduce energy costs.

Conclusion

The data center chip market is expected to experience strong growth, driven by increasing demand for high-performance chips across industries like cloud computing, AI, and BFSI. While US tariffs could raise component prices and impact short-term market growth, the long-term outlook remains positive, driven by innovation and the need for scalable, energy-efficient solutions in modern data centers.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)