Table of Contents

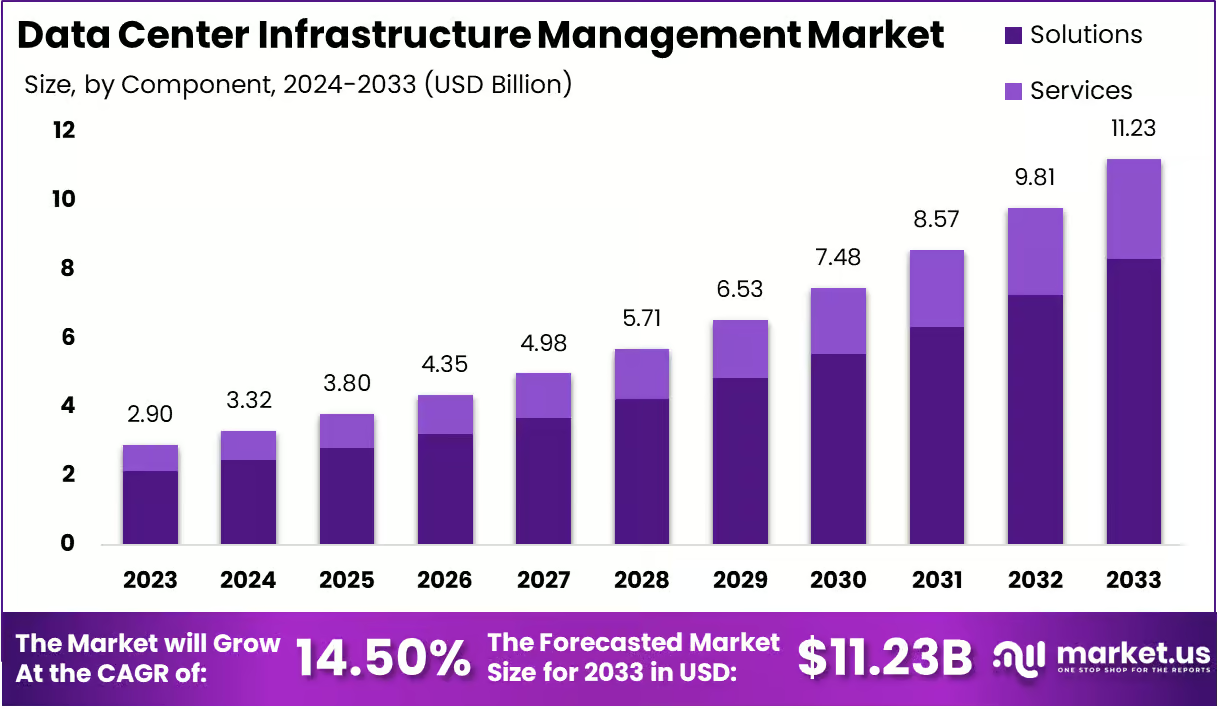

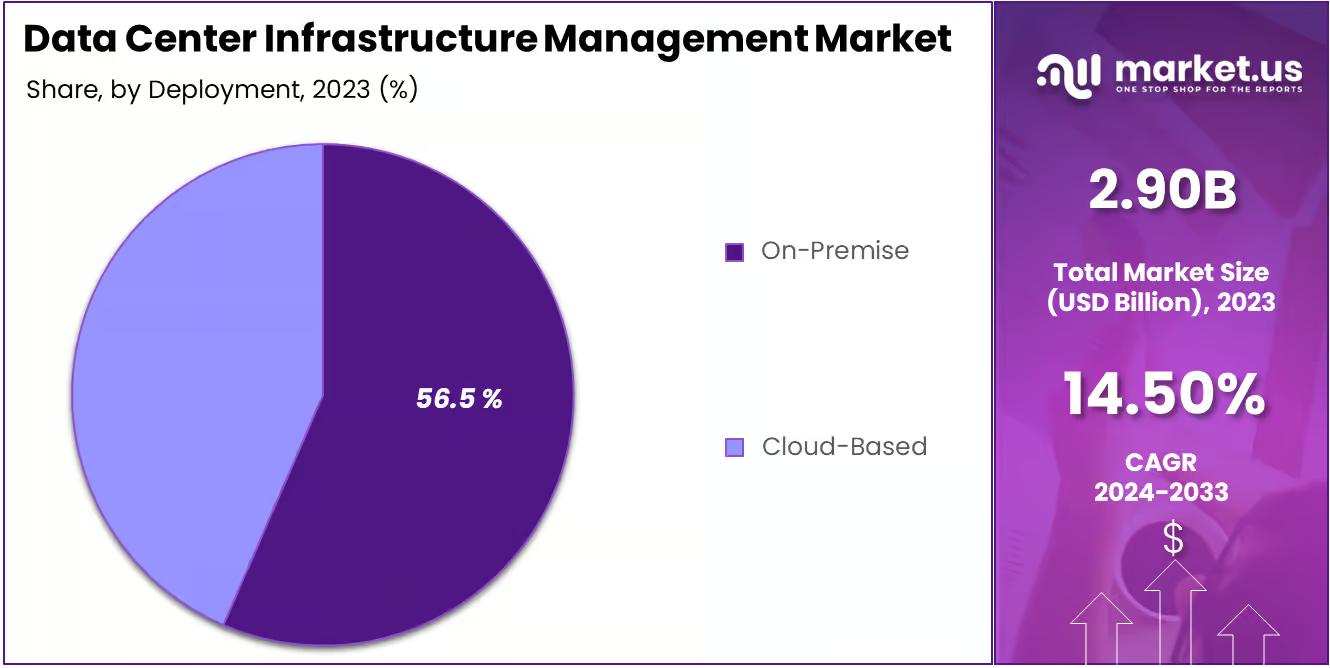

The Global Data Center Infrastructure Management (DCIM) Market is projected to experience substantial growth over the next decade. By 2033, the market is expected to reach approximately USD 11.23 billion, rising from USD 2.9 billion in 2023. This growth represents a compound annual growth rate (CAGR) of 14.50% during the forecast period from 2024 to 2033.

In 2023, North America held a dominant position in the market, accounting for more than 37.2% of the total share and generating approximately USD 1.07 billion in revenue. This strong regional presence underscores the growing adoption of DCIM solutions in the region, driven by increasing investments in data centers, rising demand for cloud computing, and advancements in IT infrastructure.

The significant growth of the DCIM market is attributed to the rising need for efficient data center operations, enhanced energy management, and the integration of AI-powered automation. As enterprises continue to expand their IT infrastructure, the demand for centralized monitoring, real-time analytics, and predictive maintenance solutions is expected to drive market expansion globally.

Key Takeaways

- The global Data Center Infrastructure Management (DCIM) market was valued at USD 2.9 billion in 2023 and is projected to reach USD 11.23 billion by 2033, growing at a CAGR of 14.50%.

- North America led the DCIM market in 2023 with a 37.2% share, achieving USD 1.07 billion in revenue due to its advanced IT infrastructure and the presence of major data center operators.

- The Solution segment captured 74.1% of the market share in 2023, highlighting the demand for comprehensive DCIM solutions that include asset management, energy management, and performance monitoring.

- In deployment preferences, the On-Premise segment led with a 56.5% market share in 2023, reflecting the preference for keeping data management solutions within the enterprise for security and control.

- Large Enterprises dominated the DCIM market with a 65.9% share in 2023, driven by their expansive IT infrastructure needs and the complexity of managing large-scale data centers.

- Asset Management emerged as the leading application in the DCIM market, capturing 34.8% of the market share in 2023, underscoring the importance of tracking and managing both physical and virtual assets.

- The IT and Telecommunications industry was the largest end-use segment with a 30.5% market share in 2023, highlighting the sector’s reliance on efficient DCIM solutions for data center performance and scalability.

- The DCIM market is experiencing growth due to the escalating demand for cloud services, data storage, and high-speed computing, fueled by digital transformation initiatives across multiple industries.

- The push for energy efficiency and sustainability is a significant growth driver, as organizations increasingly rely on DCIM systems to effectively manage energy use and reduce carbon footprints.

- Key players in the DCIM market include ABB Group, Siemens AG, Schneider Electric SE, Eaton Corporation, and Vertiv Group, all contributing to the market’s development through strategic innovations and partnerships.

Key Market Segments

By Component

- Solution

- Services

By Deployment Mode

- Cloud-Based

- On-Premise

By Enterprise Size

- Small and Medium-Sized Enterprises

- Large Enterprises

By Application

- Asset Management

- Power Monitoring

- BI and Analytics

- Capacity Management

- Environmental Monitoring

- Other Applications

By End-Use Industry

- IT and Telecommunications

- BFSI

- Retail

- Manufacturing

- Healthcare

- Government

- Other End-Use Industries

By Component

In 2023, the Solution segment held a dominant position in the DCIM market, accounting for more than 74.1% of the total market share. The increasing demand for integrated, all-in-one solutions that offer a comprehensive approach to data center management has been the primary driver of this growth. These solutions include real-time monitoring, energy management, asset tracking, and resource optimization, all of which are essential for improving operational efficiency and cost reduction.

DCIM solutions enable businesses to centrally manage their physical and virtual infrastructure, monitor power consumption, and ensure system reliability. The integration of multiple management tools into a single, scalable solution makes them highly attractive for large enterprises seeking comprehensive control over their data center operations. The rising adoption of automation and artificial intelligence (AI) in DCIM solutions is further driving demand, as businesses look for advanced technologies to predict and prevent system failures, optimize resource utilization, and manage large, complex infrastructures.

By Deployment Mode

The On-Premise segment dominated the DCIM market in 2023, capturing more than 56.5% of the total market share. The preference for on-premise solutions is driven by the need for enhanced security, control, and customization, particularly among large enterprises and regulated industries, such as finance, healthcare, and government. Organizations operating in these sectors prioritize on-premise deployments to ensure compliance with strict data privacy regulations and to mitigate security risks associated with cloud-based solutions.

On-premise DCIM solutions offer businesses greater autonomy over their IT operations, enabling direct integration with existing infrastructure. These solutions are particularly beneficial for enterprises with multi-facility operations, as they provide the flexibility to customize and tailor data center management according to specific business requirements and security protocols. Additionally, on-premise solutions often offer better data throughput and lower latency than cloud-based alternatives, making them preferable for businesses requiring real-time access to their data.

By Enterprise Size

The Large Enterprises segment led the DCIM market in 2023, capturing more than 65.9% of the total market share. The dominance of large enterprises in this market is driven by their extensive IT infrastructure and the complexity involved in managing large-scale data centers. These organizations often operate multiple data centers and have the resources to invest in advanced DCIM solutions to enhance efficiency, performance, and real-time monitoring.

With high-volume, mission-critical operations, large enterprises require robust systems to manage data center capacity, power usage, cooling, and network performance. Many of these businesses also have dedicated IT teams capable of handling the technical demands of on-premise DCIM solutions. The need for comprehensive, scalable, and flexible solutions has contributed to the sustained growth of DCIM adoption among large enterprises. As organizations expand their global operations, DCIM solutions provide enhanced visibility and control, helping to optimize resource utilization and minimize downtime.

By Application

In 2023, the Asset Management segment held the largest share of the DCIM market, accounting for more than 34.8%. The increasing need for effective tracking, management, and optimization of physical assets, such as servers, storage devices, and networking equipment, has been a significant factor in driving this growth.

As data centers become more complex, businesses require real-time visibility into their hardware and infrastructure to improve operational efficiency and maximize asset utilization. The rise of virtualization and cloud-based infrastructures has further emphasized the need for detailed insights into asset usage, lifecycle, and location. DCIM solutions that incorporate advanced asset management capabilities help organizations prevent downtime, extend hardware lifespan, and optimize IT resources.

Moreover, asset management solutions play a crucial role in regulatory compliance and facilitate better forecasting of future capital expenditures. As hyperscale and colocation data centers expand, managing growing assets across multiple locations has become an increasingly complex task. Effective asset management practices help minimize risks, enhance resource allocation, and reduce costs, making this application a vital component of the DCIM market.

By End-Use Industry

The IT and Telecommunications segment dominated the DCIM market in 2023, securing more than 30.5% of the total market share. The rapid expansion of data centers, driven by the increasing demand for cloud computing, big data analytics, and Internet of Things (IoT) technologies, has significantly contributed to this growth.

The IT and telecommunications sector depends heavily on data centers to support enterprise-level and consumer-facing operations. As the adoption of 5G networks, edge computing, and AI-driven applications continues to rise, data centers must handle massive volumes of data while ensuring uptime, efficiency, and scalability.

DCIM solutions help telecommunications companies and IT service providers optimize data center performance, reduce operational costs, and enhance energy efficiency. These solutions provide real-time asset utilization insights, ensuring that businesses can effectively manage their infrastructure while maintaining service reliability. As cloud computing and edge data centers become more prevalent, organizations in the IT and telecom sector are making significant investments in scalable and automated DCIM solutions to support their growing infrastructure needs.

Top Key Players

- ABB Group

- Siemens AG

- Schneider Electric SE

- Eaton Corporation PLC

- Vertiv Group Corporation

- Cisco Systems, Inc.

- Dell Inc.

- Hewlett Packard Enterprise (HPE)

- Sunbird Software, Inc.

- FNT GmbH

- Other Key Players

Conclusion

The Global Data Center Infrastructure Management (DCIM) Market is set for significant expansion, projected to grow from USD 2.9 billion in 2023 to approximately USD 11.23 billion by 2033, at a CAGR of 14.50% during the forecast period. In 2023, North America held a 37.2% market share with revenue of USD 1.07 billion.

The Solution segment dominated by capturing over 74.1% of the market share, driven by the demand for comprehensive management solutions. The On-Premise deployment led with a 56.5% share due to security and compliance concerns. Large Enterprises accounted for 65.9% of the market, given their complex IT infrastructure needs. The Asset Management segment held the largest share at 34.8%, highlighting the necessity of efficient asset tracking.

The IT and Telecommunications sector dominated the end-use industry, securing 30.5% of the market, fueled by the rising demand for cloud computing, IoT, and 5G networks. The growing reliance on advanced DCIM solutions to enhance operational efficiency, automation, and real-time monitoring is expected to drive continued market growth over the coming years.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)