Table of Contents

Introduction

The Global Edge AI Accelerator Market is projected to expand from USD 7.68 billion in 2024 to approximately USD 94.27 billion by 2034, growing at an impressive CAGR of 28.5%. In 2024, North America led the market with a 33% share, generating around USD 2.5 billion in revenue.

The United States alone contributed nearly USD 2.4 billion, expected to grow at a 27.6% CAGR to reach USD 27.5 billion by 2034. The CPU segment dominated with a 38% market share due to its wide adoption for edge inference tasks, while Smartphones captured over 34% share among device types, reflecting increasing integration of edge AI technologies.

US Tariff Impact on Market

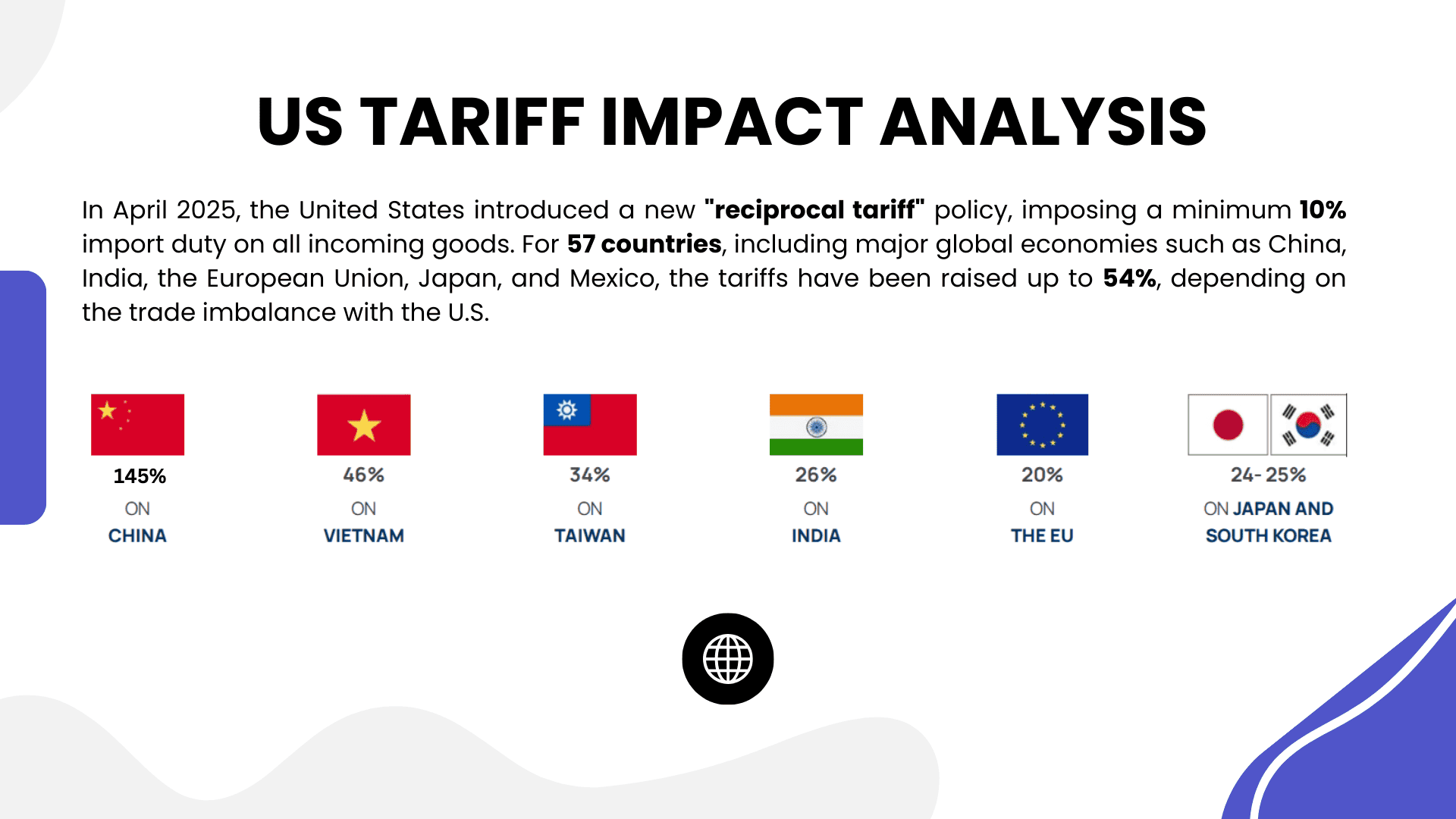

The U.S. tariffs on semiconductors, microprocessors, and AI hardware components have moderately affected the Edge AI Accelerator Market. In 2024, tariffs on critical components rose by 15%–25%, according to USTR and PIIE data. This led to increased hardware manufacturing costs, impacting pricing strategies for AI accelerators in smartphones, IoT devices, and industrial applications.

Companies with strong domestic supply chains and partnerships navigated the cost hikes more effectively, sustaining growth momentum. Despite these challenges, continued investment in domestic semiconductor fabrication and AI R&D initiatives helped offset some tariff pressures.

➤➤➤ Experience the power of actionable insights – get a sample here @ https://market.us/report/edge-ai-accelerator-market/free-sample/

The U.S. government’s push for localized chip manufacturing through initiatives like the CHIPS Act further supports market expansion. Overall, while short-term cost pressures persist, the strong underlying demand for real-time, device-level processing ensures a highly positive long-term growth trajectory for the Edge AI Accelerator Market.

Economic Impact

- Tariff-induced cost hikes slightly elevated AI accelerator pricing.

- Domestic manufacturing investments partially mitigated import dependency.

- The market remains resilient, driven by industries’ urgent need for real-time, decentralized data processing.

Geographical Impact

- North America leads, supported by strong government initiatives and R&D funding.

- Asia-Pacific sees the fastest growth due to expanding smartphone and IoT industries.

- Europe maintains steady progress, emphasizing data privacy and localized edge AI deployments.

Business Impact

- Tariffs encouraged supply chain diversification and localized production.

- Companies invest heavily in edge-specific AI chip innovations.

- Demand for cost-effective, power-efficient accelerators across mobile, automotive, and manufacturing sectors continues to rise.

Key Takeaways

- Market to grow from USD 7.68 billion (2024) to USD 94.27 billion (2034).

- North America holds over 33% market share in 2024.

- CPU segment leads with 38% market share.

- Smartphones dominate device type with 34% share.

- The manufacturing sector leads among end-users at 22%.

Analyst Viewpoint

Currently, the Edge AI Accelerator Market is thriving despite moderate cost increases due to tariffs. Growing demand for real-time data processing across devices like smartphones, IoT gadgets, and industrial machinery fuels expansion. Investments in domestic chip manufacturing further stabilize supply chains and support continuous innovation.

Looking forward, accelerated adoption of 5G, smart manufacturing, autonomous vehicles, and AI-enabled consumer electronics will significantly boost edge AI deployment. Edge AI accelerators are poised to become essential across industries, enhancing performance, security, and energy efficiency. The market outlook remains overwhelmingly positive, underpinned by technological advancements and expanding end-user adoption across global sectors.

➤➤➤ Attention!!! Grab Limited Period Offer Now @ https://market.us/purchase-report/?report_id=147031

Regional Analysis

North America dominates the Edge AI Accelerator Market, with the U.S. leading due to early edge AI adoption, robust R&D investments, and favorable government policies supporting semiconductor innovation. Asia-Pacific is rapidly gaining ground, driven by booming smartphone, automotive, and IoT sectors, especially in China, South Korea, and Japan.

Europe shows consistent growth, emphasizing data sovereignty, privacy regulations, and industrial automation initiatives. Latin America and the Middle East, though smaller markets, are seeing rising investments in smart city projects and IoT infrastructure, offering long-term potential. Regional dynamics reflect a global push toward smarter, faster, and more efficient device-level AI computing.

Business Opportunities

The Edge AI Accelerator Market presents significant opportunities across diverse industries. Manufacturers can capitalize on developing low-power, high-performance AI accelerators for smartphones, automotive applications, and wearable devices. The rising adoption of Industry 4.0 presents opportunities for deploying AI accelerators in predictive maintenance and factory automation.

Healthcare offers potential through AI-enabled diagnostic tools and remote patient monitoring solutions. Emerging demand for privacy-preserving edge AI solutions also opens new niches. Startups focusing on specialized, vertical-specific accelerators, such as those optimized for drones, smart cameras, and autonomous robots, can gain competitive advantages. Collaborations with telecom firms deploying 5G networks further boost expansion opportunities.

➤ U.S. tariffs: What’s changing in these markets?

- Humanoid Robots for Customer Service Market

- Financial Predictive Analytics Market

- Digital Manufacturing Market

- Game Publisher Market

Key Segmentation

The Edge AI Accelerator Market is segmented by component, device type, end-user, and geography.

- By Component: Central Processing Unit (CPU), Graphics Processing Unit (GPU), Application-Specific Integrated Circuit (ASIC), and Field-Programmable Gate Arrays (FPGAs), with CPUs dominating at 38% share.

- By Device Type: Smartphones lead with over 34% share, followed by Industrial IoT Devices, Automotive Devices, and Consumer Electronics.

- By End-User: Manufacturing holds the top position with 22% share, followed by Automotive, Consumer Electronics, and Healthcare.

This segmentation highlights the market’s broad adoption across industries, driven by the need for real-time, localized AI processing at the edge.

Key Player Analysis

Leading players in the Edge AI Accelerator Market focus on technological innovation, targeting reduced latency, energy efficiency, and high-performance capabilities. Companies invest heavily in R&D for developing specialized AI chips tailored for edge applications across smartphones, industrial IoT, and automotive devices.

Strategic partnerships with cloud service providers and telecom firms strengthen their ecosystem positions. Emphasis is also placed on developing AI accelerators that support multiple frameworks (e.g., TensorFlow Lite, ONNX) for developer flexibility.

Firms increasingly prioritize edge security features to comply with stringent data protection regulations. Regional manufacturing expansion and collaboration with OEMs further fuel competitive advantages in the evolving market.

Top Key Players in the Market

- Apple Inc.

- EdgeCortix Inc.

- Hailo Technologies Ltd.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- Intel Corporation

- Google LLC

- NVIDIA Corporation

- Qualcomm Technologies, Inc.

- Rapidus Corporation

- Others

Recent Developments

In 2024, several players launched ultra-low-power edge AI chips optimized for IoT and automotive applications. Partnerships between AI hardware firms and telecom operators accelerated the deployment of 5G-enabled edge AI solutions. Major investments in domestic chip manufacturing facilities were announced to reduce supply chain vulnerabilities caused by ongoing tariff pressures.

Conclusion

The Global Edge AI Accelerator Market is on a dynamic growth trajectory, driven by real-time data processing needs across industries. While tariffs present moderate short-term cost challenges, innovations, government support, and expanding application fields ensure strong long-term prospects. Companies investing in specialized, efficient edge AI solutions will shape the future market landscape.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)