Table of Contents

- Introduction

- Editor’s Choice

- Global Engineering Services Outsourcing (ESO) Market Overview

- Factors Driving the Demand for Engineering Services Outsourcing (ESO) Statistics

- Most Important Factors for Engineering and R&D Executives When Choosing an Outsourcing Provider

- Change in Companies’ Share of Outsourced Engineering and R&D Activities

- Engineering and R&D Spending

- Challenges and Barriers to Engineering Services Outsourcing Statistics

- Regulations for Engineering Services Outsourcing Statistics

- Recent Developments

- Conclusion

- FAQs

Introduction

Engineering Services Outsourcing Statistics: Engineering services outsourcing (ESO) involves delegating engineering tasks to external providers. Offering benefits such as cost savings, access to specialized skills, and enhanced flexibility.

ESO encompasses various mechanical and electrical engineering disciplines, with engagement models ranging from project-based to full-service outsourcing.

Companies can use a global delivery model and technological infrastructure to ensure effective communication and collaboration across distributed teams.

Quality assurance measures and risk management strategies are vital to maintain standards and mitigate inherent risks.

Overall, ESO enables companies to focus on core competencies, and accelerate time-to-market. Which expand their global reach through strategic partnerships and efficient resource utilization.

Editor’s Choice

- The global engineering services outsourcing market revenue is expected to reach USD 5,786.4 billion by 2033.

- In the global engineering services outsourcing market, AKKA holds the largest market share at 16%, showcasing its leading position in the industry.

- The Asia-Pacific (APAC) region dominates with a substantial 42.3% market share, highlighting its major role in the industry.

- When engineering and R&D executives select an outsourcing provider, several critical factors influence their decision-making. The most significant criterion is specific industry expertise, with 325 survey responses highlighting this aspect, representing a 73% share of the top three factors.

- When engineering and R&D executives select an outsourcing provider, several critical factors influence their decision-making. The most significant criterion is specific industry expertise, with 325 survey responses highlighting this aspect, representing a 73% share of the top three factors.

- Global engineering and R&D spending is projected to reach 2.719 billion euros in 2026, marking a 56% increase.

- Perceived barriers to Outsourcing R&D and product engineering (PE) services are varied, with several factors impacting organizations’ decisions. The most significant barrier, cited by 54% of respondents, is the fear of losing control over product development.

Global Engineering Services Outsourcing (ESO) Market Overview

Global Engineering Services Outsourcing (ESO) Market Size Statistics

- The Global Engineering Services Outsourcing Market has demonstrated significant growth over the past few years and is projected to continue on this upward trajectory at a CAGR of 24.1%.

- In 2022, the market revenue was recorded at USD 538.2 billion.

- This figure rose to USD 667.9 billion in 2023 and is anticipated to reach USD 828.8 billion by the end of 2024.

- The growth momentum is expected to accelerate, with the market projected to achieve USD 1,028.6 billion in 2025 and USD 1,276.5 billion in 2026.

- By 2027, the market is forecasted to expand to USD 1,584.1 billion and further to USD 1,965.9 billion in 2028.

- Continuing this robust growth, the market is expected to reach USD 2,439.6 billion by 2029 and USD 3,027.6 billion by 2030.

- Looking ahead, the market is projected to grow to USD 3,757.2 billion in 2031, USD 4,662.7 billion in 2032, and an impressive USD 5,786.4 billion by 2033.

- These figures underscore the rapidly expanding nature of the engineering services outsourcing industry on a global scale.

(Source: market.us)

Competitive Landscape of the Global Engineering Services Outsourcing (ESO) Market Statistics

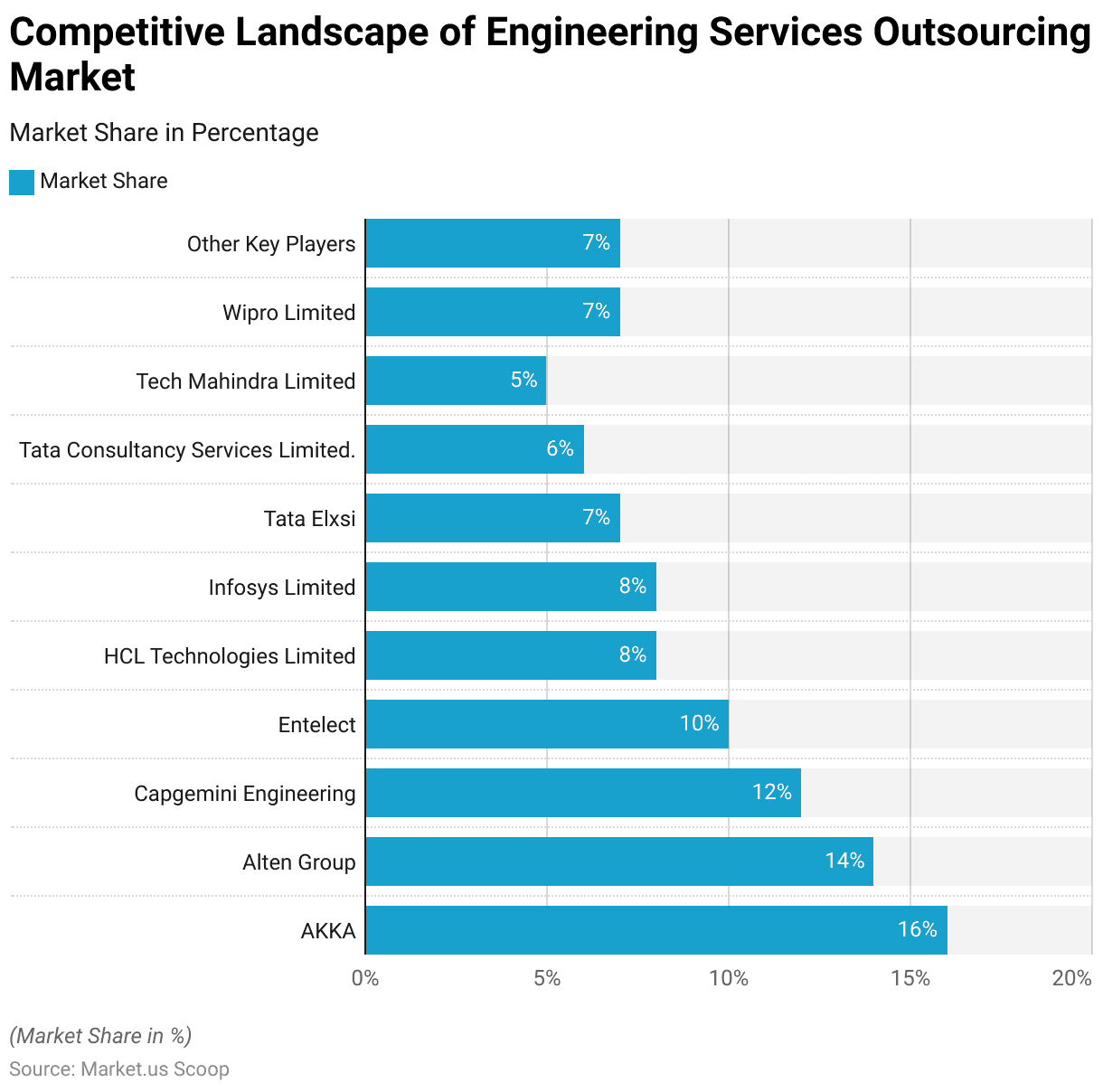

- In the Global Engineering Services Outsourcing Market. AKKA holds the largest market share at 16%, showcasing its leading position in the industry.

- Alten Group follows closely with a 14% market share, indicating its significant influence.

- Capgemini Engineering commands a 12% share, reflecting its substantial presence in the market.

- Entelect, with a 10% share, also demonstrates a strong foothold.

- Both HCL Technologies Limited and Infosys Limited each hold an 8% market share, highlighting their competitive standing.

- Tata Elxsi and Wipro Limited each account for 7% of the market, illustrating their vital roles.

- Tata Consultancy Services Limited and Tech Mahindra Limited have market shares of 6% and 5%, respectively, contributing notably to the market dynamics.

- Other key players collectively hold a 7% share, indicating the diverse range of companies operating within this sector.

(Source: market.us)

Regional Analysis of the Global Engineering Services Outsourcing (ESO) Market Statistics

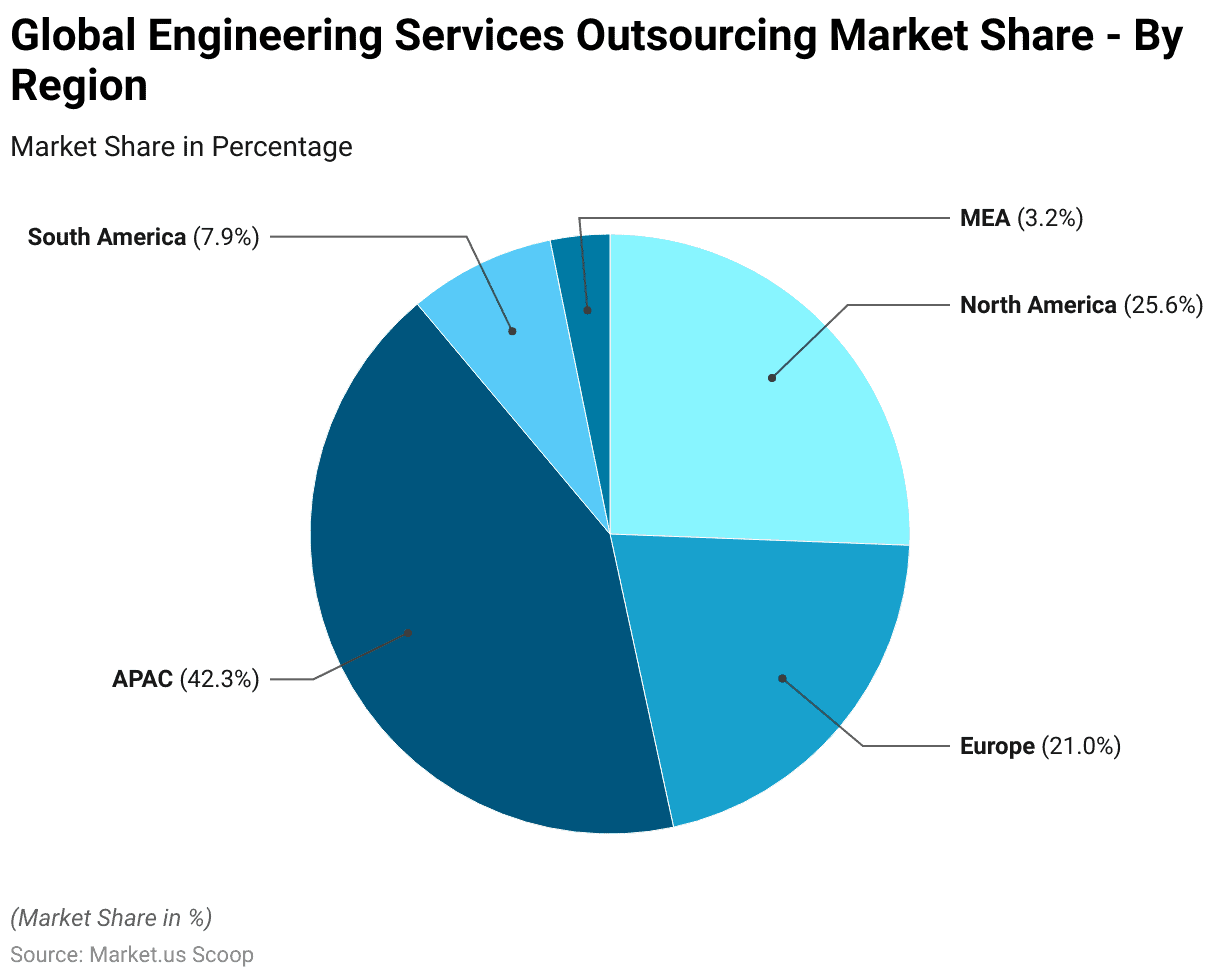

- The regional distribution of the Global Engineering Services Outsourcing Market reveals significant variations in market share.

- The Asia-Pacific (APAC) region dominates with a substantial 42.3% market share, highlighting its major role in the industry.

- North America follows with a 25.6% share, indicating its strong presence.

- Europe holds a 21.0% share, reflecting its considerable participation in the market.

- South America accounts for 7.9% of the market share, showcasing its emerging influence.

- The Middle East and Africa (MEA) region has a 3.2% share. Demonstrating its growing but relatively smaller contribution to the global market landscape.

(Source: Statista)

Factors Driving the Demand for Engineering Services Outsourcing (ESO) Statistics

Lack of Availability of New Engineering Talent

- According to a recent BCG survey, 92% of global company leaders prioritize attracting and retaining talent, especially in engineering.

- The increasing scarcity of engineering talent poses a significant risk to vital industries. It could negatively impact the economy by nearly 40% of the projected GDP impact of all talent shortages in the US by 2030.

- According to the Bureau of Labor Statistics (BLS), there’s a projected growth of approximately 13% in demand for engineering skills from 2023 to 2031.

- Additionally, the American Council of Engineering Companies, representing nearly 6,000 firms, has informed President Biden that a talent shortage in the engineering and design services sector is already hindering crucial projects for the BBBA.

- Countries worldwide are grappling with engineering talent shortages. Japan’s Ministry of Economy forecasts a shortfall of more than 700,000 engineers by 2030. The German Economic Institute highlights a current deficit of 320,000 STEM specialists in Germany as of April 2022.

(Source: Boston Group Consulting, American Council of Engineering Companies, Ministry of Foreign Affairs of Japan, HR Forecast)

Mismatch Between Available and In-Demand Skills

- The gap between new engineering positions and available engineers is significant, currently standing at about 133,000. However, the situation becomes even more concerning when further analysis of the data is needed.

- Over the next decade, the United States is expected to face a shortage of engineers, particularly in software, industrial, civil, and electrical engineering, with an estimated 186,000 job vacancies by 2031.

- Conversely, certain engineering fields like materials, chemical, aerospace, and mechanical engineering, which have historically been popular, are projected to have an oversupply of around 41,000 qualified candidates by the same year. Moreover, the skill requirements for these roles are evolving.

- Even traditional engineering positions will increasingly demand a blend of hard and soft skills. With T-shaped skill profiles encompassing both deep expertise in a specific area and interdisciplinary knowledge.

- Additionally, engineers will need to be familiar with next-generation techniques such as agile methodology, new product development, and test-driven development, which are anticipated to experience the highest growth in demand over the next five years.

(Source: Boston Group Consulting)

Insufficient Reskilling and Upskilling

- Addressing the shortage of next-generation engineering skills requires companies to take proactive measures, as simply hiring their way out of the problem is not feasible due to limited available talent.

- Options include upskilling current employees by promoting them to more senior roles, reskilling them by providing training in less in-demand engineering areas, or hiring candidates with partial fit and enhancing their capabilities.

- While CEOs acknowledge the importance of training, many struggle to establish effective learning and development (L&D) systems, with doubts about their HR teams’ ability to deliver results.

- This challenge extends across industries, with a Harvard Business Review survey revealing that 75% of managers express dissatisfaction with their company’s L&D efforts.

- Industries reliant on engineering, like industrial goods, are particularly lacking in L&D resources, with 10% to 20% fewer training hours per worker compared to other sectors, emphasizing the urgency of addressing this issue.

(Sources: Boston Group Consulting, Harvard Business Review)

Major Leaks in the Engineering Talent Pipeline

- A deficient talent pipeline worsens the engineering shortage, especially in terms of diversity and the lengthy process of talent development from early education.

- BCG analysis reveals that only about 13% of high school students interested in engineering end up completing an engineering degree at university.

- Additionally, less than half of the roughly 200,000 US students graduating with engineering degrees pursue engineering roles.

- The American Society for Engineering Education reports that merely 37% of engineering graduates enter engineering careers.

- Furthermore, despite comprising the majority of college students, only 2% of women graduate with engineering degrees, compared to 10% of men.

- Increasing the number of women pursuing engineering degrees could potentially add up to 40,000 more engineers annually and reduce the US engineering gap by 30%, assuming all women engineers transition into engineering careers.

- Persistence in engineering careers varies, as shown by a 2022 survey by the National Center for Science and Engineering Statistics.

- Initially, male and female engineering graduates exhibit similar retention rates, but over time, women’s retention rates decline significantly compared to men’s.

- For instance, by 2021, only 27% of women who graduated with engineering degrees between 2006 and 2010 remained in engineering roles, whereas 41% of their male peers were still working in engineering.

(Source: Boston Group Consulting, National Science Foundation)

Most Important Factors for Engineering and R&D Executives When Choosing an Outsourcing Provider

- When engineering and R&D executives select an outsourcing provider, several critical factors influence their decision-making.

- The most significant criterion is specific industry expertise, with 325 survey responses highlighting this aspect, representing a 73% share of the top three factors.

- The strongest cost advantage is also highly valued, receiving 261 responses and accounting for 59% of the top three considerations.

- Technology expertise, regardless of industry, is another crucial factor, noted by 257 respondents, equating to 58%.

- Strong intellectual property and thought leadership are important for 181 executives, comprising 41% of the top three criteria.

- Personal connections to the outsourcing provider matter to 135 respondents, making up 30% of the top three factors.

- Lastly, the most reputable brand name is a significant consideration for 104 executives, representing 23% of the top three responses.

- These factors collectively underscore the multifaceted considerations executives weigh when choosing an outsourcing partner.

(Source: Bain and Company)

Change in Companies’ Share of Outsourced Engineering and R&D Activities – By Region

- Survey responses indicate a notable shift in companies’ share of outsourced engineering and R&D activities over the next three years, varying by region.

- Globally, 441 respondents anticipate changes in their outsourcing activities.

- In the Asia-Pacific region, 86 respondents foresee adjustments, reflecting the region’s growing influence in the outsourcing market.

- The Americas have 164 respondents predicting changes, indicating significant potential shifts in their outsourcing strategies.

- Europe, the Middle East, and Africa (EMEA) collectively have 191 respondents expecting alterations in their outsourced engineering and R&D activities, suggesting a dynamic landscape in these regions.

- These responses highlight the global trend towards increasing reliance on outsourced engineering and R&D services.

(Source: Bain and Company)

Change in Companies’ Share of Outsourcing Engineering and R&D Activities – By Engineering Services Statistics

- Survey responses reveal expected changes in companies’ share of outsourced engineering and R&D activities across various engineering services over the next three years.

- Advanced manufacturing and services lead, with 112 respondents anticipating shifts, highlighting the growing trend in outsourcing within this sector.

- The automotive and mobility sector follows with 83 respondents, indicating significant expected changes.

- In the medical devices sector, 44 respondents foresee adjustments in their outsourcing strategies.

- The energy and natural resources sector has 72 respondents predicting changes, reflecting the dynamic nature of this industry. Aerospace and defense see 80 respondents expecting shifts, underlining the evolving landscape in these sectors.

- Lastly, telecommunications has 50 respondents anticipating changes, pointing to ongoing developments in outsourcing within this field.

- These responses underscore the diverse and evolving nature of outsourcing in engineering and R&D activities across different sectors.

(Source: Bain and Company)

Engineering and R&D Spending

Overall Global Spending

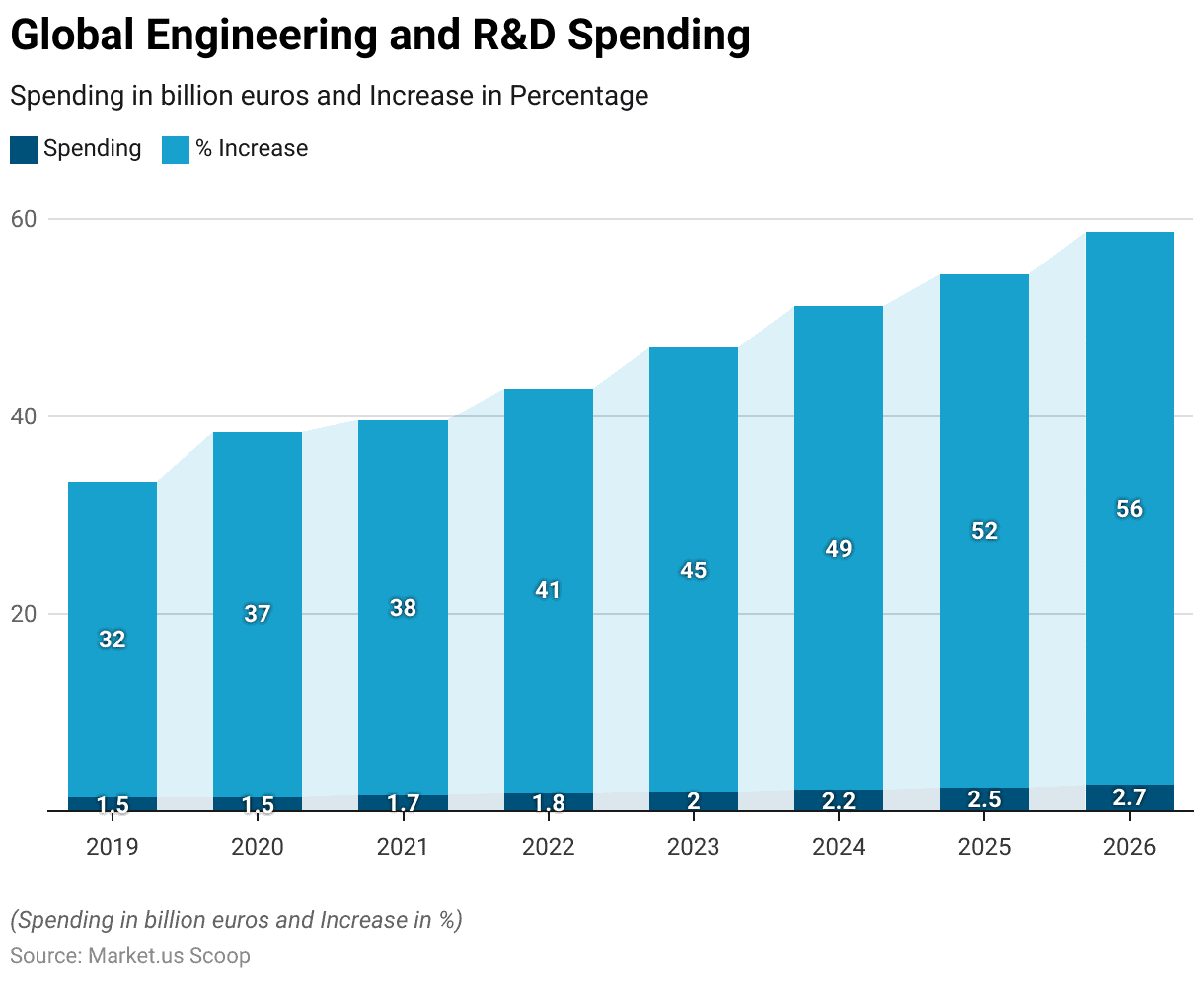

- Global engineering and R&D spending has shown consistent growth from 2019 to 2026, reflecting a strong upward trend.

- In 2019, the spending was recorded at 1.457 billion euros, marking a 32% increase.

- This growth continued into 2020, with spending rising to 1.464 billion euros, representing a 37% increase.

- By 2021, the spending had reached 1.688 billion euros, a 38% increase from the previous year.

- The upward trajectory persisted in 2022, with expenditures climbing to 1.848 billion euros, a 41% increase.

- In 2023, spending further escalated to 2.029 billion euros, showing a 45% increase.

- Projections for 2024 indicate spending will rise to 2.231 billion euros, a 49% increase.

- This growth is expected to continue, reaching 2.460 billion euros in 2025, a 52% increase, and 2.719 billion euros in 2026, marking a 56% increase.

- These figures underscore the robust and accelerating investment in engineering and R&D activities globally.

(Source: Bain and Company)

North America

- Engineering and R&D spending in North America has shown substantial growth from 2021 to 2026.

- In 2021, the spending was recorded at USD 804 billion.

- This figure increased significantly in 2022, reaching USD 903 billion.

- Looking ahead, the spending is projected to escalate further, reaching USD 1,459 billion by 2026.

- These figures illustrate a robust and accelerating investment in engineering and R&D activities within North America over the specified period.

(Source: Zinnov Zones)

Western Europe

- Engineering and R&D spending in Western Europe has experienced notable growth from 2021 to 2026.

- In 2021, the spending was recorded at USD 417 billion.

- This amount increased to USD 443 billion in 2022, reflecting a positive trend.

- Looking forward, the spending is projected to reach USD 573 billion by 2026.

- These figures highlight the increasing investment in engineering and R&D activities in Western Europe over the specified period.

(Source: Zinnov Zones)

Asia-Pacific

- Engineering and R&D spending in the Asia-Pacific region has shown a significant upward trend from 2021 to 2026.

- In 2021, the spending was recorded at USD 411 billion.

- This amount increased to USD 447 billion in 2022, indicating steady growth.

- By 2026, the spending is projected to reach USD 616 billion.

- These figures underscore the expanding investment in engineering and R&D activities within the Asia-Pacific region over the specified period.

(Source: Zinnov Zones)

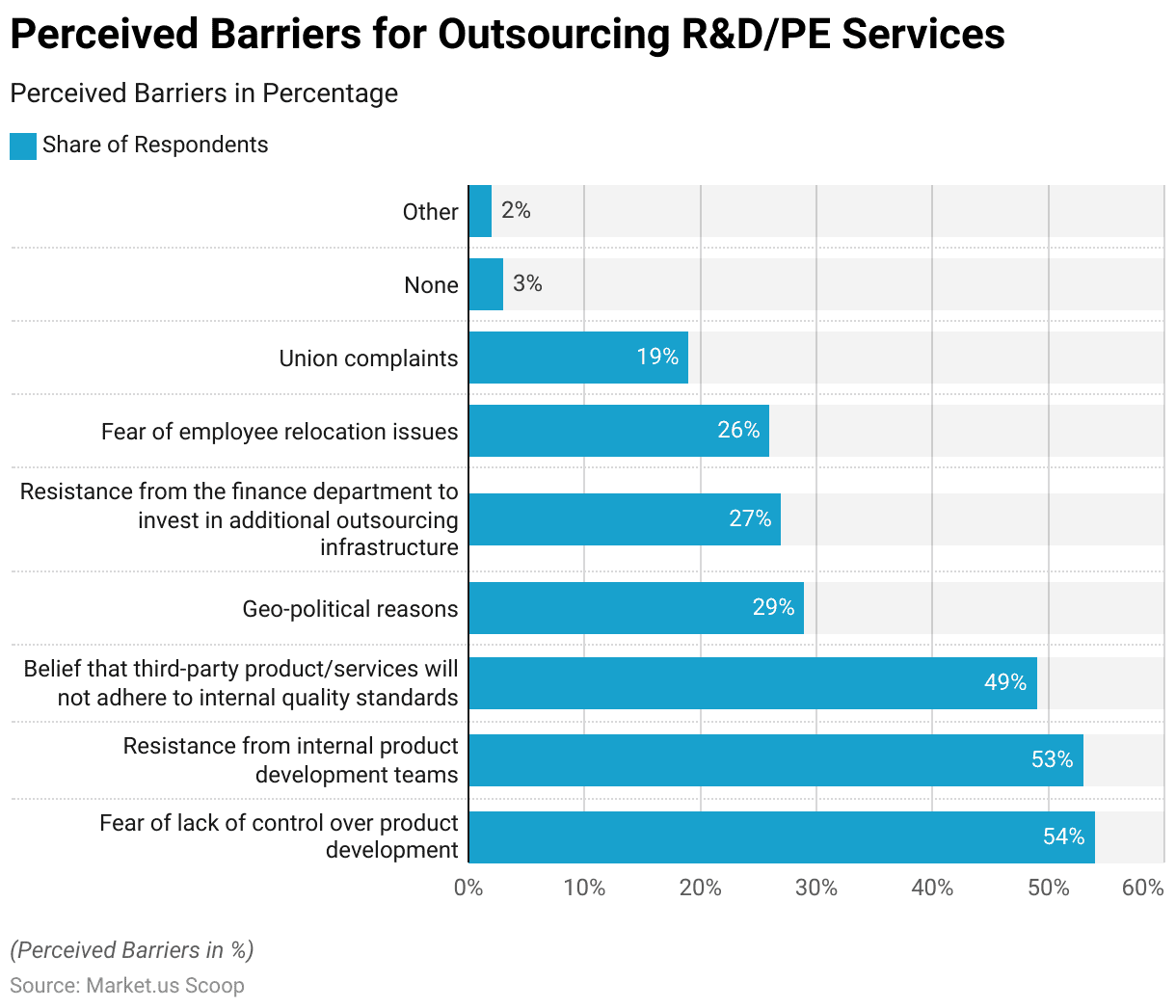

Challenges and Barriers to Engineering Services Outsourcing Statistics

- Perceived barriers to Outsourcing R&D and product engineering (PE) services are varied, with several factors impacting organizations’ decisions.

- The most significant barrier, cited by 54% of respondents, is the fear of losing control over product development.

- This is closely followed by resistance from internal product development teams, reported by 53% of respondents.

- Additionally, 49% of respondents believe that third-party products and services may not adhere to internal quality standards.

- Geo-political reasons are a concern for 29% of respondents, while 27% face resistance from their finance departments regarding investments in additional outsourcing infrastructure.

- Fear of employee relocation issues is a barrier for 26% of respondents, and 19% cite union complaints as a concern.

- Only 3% of respondents reported no perceived barriers, and 2% mentioned other unspecified barriers.

- These insights highlight the complex challenges companies face when considering outsourcing R&D and PE services.

(Source: HCL)

Regulations for Engineering Services Outsourcing Statistics

- Regulations for engineering services outsourcing vary significantly by country, influencing how companies manage their outsourcing operations.

- In the United States, companies must comply with federal laws such as the Export Administration Regulations (EAR) and International Traffic in Arms Regulations (ITAR), which control the export of technology and technical data.

- In Europe, the General Data Protection Regulation (GDPR) affects how personal data is managed during outsourcing.

- The European Union also emphasizes compliance with directives related to intellectual property and cross-border data transfers.

- In India, regulations like the Companies Act 2013 and data protection guidelines set by the Ministry of Electronics and Information Technology are crucial.

- Additionally, countries like China have stringent cybersecurity laws that impact the outsourcing of engineering services.

- These regulations are designed to ensure that outsourcing practices protect national security, intellectual property, and personal data while also promoting fair competition and compliance with international standards.

(Sources: Export Administration Regulations, Legal Information Institute -Cornell Law School, GDPR.EU, Companies Act 2013, KPMG)

Recent Developments

Acquisitions:

- L&T Technology Services’ Acquisition of SWC Business: In 2023, L&T Technology Services Limited announced the acquisition of the Smart World & Communication (SWC) business from L&T. This move aims to enhance its service offerings in the smart city solutions and communication technology sectors.

- Hitachi’s Acquisition of GlobalLogic: Hitachi acquired GlobalLogic Inc., a U.S.-based digital engineering services company, to strengthen its capabilities in digital transformation and advanced technology services.

New Product Launches:

- Tata Consultancy Services (TCS) and Marks & Spencer Partnership: In April 2023, TCS extended its partnership with Marks & Spencer (M&S) to modernize M&S’s core technology stack, aiming to enhance speed, innovation, and resilience in operations.

- Tech Mahindra’s Center of Excellence in Saudi Arabia: In February 2023, Tech Mahindra signed an MoU with the Ministry of Communication and Information Technology (MCIT) of Saudi Arabia to establish a Data & AI and Cloud Center of Excellence in Riyadh. This initiative will support the development of high-tech expertise and create quality jobs in the region.

Funding:

- Investment in Digital Transformation: Companies are heavily investing in R&D to provide advanced engineering solutions. For instance, partnerships with start-ups and increased investments in AI, data analytics, and automation are driving innovation in the ESO market.

- Government Support: Government funding and support are crucial in propelling the growth of the ESO market, especially in regions focusing on digital transformation and technological advancements.

Market Growth:

- Global Market Expansion: The growth is driven by the increasing demand for engineering services in sectors such as automotive, aerospace, and healthcare.

- Regional Insights: North America and Asia-Pacific are leading regions in the ESO market. North America, particularly the U.S., holds a significant market share due to its advanced industrial base and strong demand for technological innovation. Meanwhile, Asia-Pacific is rapidly growing due to cost-effective engineering solutions and a skilled workforce.

Innovation and Trends:

- Onshore vs. Offshore Services: The onshore segment accounted for the highest revenue share in 2022, driven by the need for better communication and collaboration between OEMs and service providers. Offshore services continue to grow due to cost advantages and access to a large talent pool in countries like India, China, and Malaysia.

- Technological Integration: The ESO industry is witnessing increased integration of AI, IoT, and other advanced technologies to enhance service delivery. This trend is expected to drive efficiency and innovation across various engineering disciplines.

Conclusion

Engineering Services Outsourcing Statistics – The global engineering services outsourcing (ESO) market is rapidly growing and fueled by technological advancements and the increasing complexity of engineering projects.

Asia-Pacific leads this growth due to its skilled workforce and cost advantages. Regulatory compliance varies by region, with the U.S. enforcing EAR and ITAR, Europe emphasizing GDPR, and India following the Companies Act 2013 and specific data protection guidelines.

As companies navigate these regulations, the focus remains on quality, intellectual property protection, and cost efficiency through strategic outsourcing. Future growth is expected to be driven by increased investments and technological innovations.

FAQs

What is Engineering Services Outsourcing (ESO)?

Engineering Services Outsourcing (ESO) refers to the practice of contracting specialized engineering tasks and processes to external service providers. These tasks can include design, prototyping, system integration, testing, and more.

Why do companies opt for ESO?

Companies choose ESO to access specialized expertise, reduce costs, improve focus on core activities, accelerate time-to-market, and enhance flexibility and scalability in managing engineering projects.

Which industries commonly use ESO?

Industries that frequently use ESO include automotive, aerospace, telecommunications, medical devices, energy, and consumer electronics. These sectors benefit from outsourced services to handle complex engineering tasks and innovate rapidly.

What are the benefits of ESO?

The benefits of ESO include cost savings, access to a global talent pool, improved efficiency and productivity, faster project turnaround, and the ability to leverage advanced technologies and processes.

What are the potential risks of ESO?

Risks associated with ESO include loss of control over certain processes, potential quality issues, intellectual property concerns, and challenges related to regulatory compliance and data security.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)