Introduction

Point of Sale Software Statistics: Point of Sale (POS) software is a crucial tool for businesses. Enabling efficient transaction processing, inventory management, and customer relationship tracking.

It integrates payment processing, sales reporting, and employee management into one system, providing real-time data for decision-making.

POS software can be traditional, cloud-based, or mobile, each offering different levels of flexibility and accessibility.

The system often requires hardware such as barcode scanners, receipt printers, and payment terminals. Key benefits include improved transaction speed, inventory accuracy, and enhanced customer experiences.

With trends like omnichannel integration and mobile payment support, POS systems continue to evolve, becoming indispensable for modern businesses.

Editor’s Choice

- The global Point of Sale (POS) software market revenue reached USD 21.1 billion in 2023.

- By 2032, the global POS software market is projected to reach USD 74.7 billion, with on-premise deployments contributing USD 51.09 billion and cloud-based solutions accounting for USD 23.61 billion.

- In 2022, the global Point of Sale (POS) software market was predominantly driven by large enterprises. Which accounted for 60.1% of the total market share.

- As of late 2016, Oracle emerged as the leading provider of Point of Sale (POS) software among retailers in North America, capturing 36% of the market share.

- As of late 2019, 52% of North American retailers planned to upgrade their POS software and 48% of their hardware within the next year, highlighting a focus on system modernization.

- Cloud-based POS software adoption is expanding, with 67% of retailers using it for workforce management and business intelligence and 43% and 41%, respectively, already on cloud platforms.

- In the Philippines, the Bureau of Internal Revenue (BIR) has implemented Revenue Memorandum Order No. 24-2023 to standardize the accreditation of sales machines and software, including POS systems.

Most Used Payment Methods in Physical POS Worldwide

- In 2023, digital wallets, including mobile money, emerged as the most widely used payment method in physical point-of-sale (POS) transactions worldwide. Accounting for an estimated transaction value of $10.8 trillion, or 29.6% of the total transaction value.

- This figure is projected to grow significantly, reaching $19.6 trillion by 2027, capturing 45.9% of the market with a compound annual growth rate (CAGR) of 16.1% from 2023 to 2027.

- Credit cards, which represented $10 trillion in transactions (27.4% share) in 2023, are expected to decline slightly to $9.39 trillion and a 22% share by 2027, reflecting a negative CAGR of -1.6%.

- Similarly, debit card transactions, valued at $8.3 trillion (22.7% share) in 2023, are forecasted to decrease to $7.69 trillion, representing an 18% share by 2027, with a negative CAGR of -1.9%.

- Cash usage continues to decline sharply, with its transaction value expected to drop from $6 trillion (16.4% share) in 2023 to $4.7 trillion (11% share) in 2027, registering a negative CAGR of –5.9%.

- Prepaid cards, on the other hand, are expected to grow modestly from $906 billion (2.5% share) in 2023 to $961 billion (2.3% share) by 2027, with a CAGR of 1.5%.

- POS financing, which accounted for $520 billion or 1.4% of the transaction value in 2023, lacks future projections but remains a relatively small segment.

- These trends underscore a significant shift toward digital and contactless payment methods. Driven by growing consumer preference for convenience and advancements in payment technologies.

(Source: Statista)

Leading Countries in the World with the Highest Number of POS Terminals

- As of 2022, China led the global market in the number of Point of Sale (POS) terminals. With a staggering 46.8 million units deployed.

- The United States followed with 23 million POS terminals, showcasing its robust digital payment infrastructure.

- India ranked third, with 12.6 million terminals, reflecting its growing emphasis on digital transactions.

- Russia and Indonesia recorded 9.6 million and 8.5 million terminals, respectively, highlighting widespread adoption in these markets.

- Pakistan, Egypt, and Brazil had similar figures, with 5.5 million, 5.4 million, and 5.3 million POS terminals, respectively.

- Japan and the Philippines each reported 4.1 million terminals, rounding out the list of the top ten countries.

- These figures underscore the significant role of POS terminals in facilitating cashless transactions across both developed and emerging markets.

(Source: Statista)

POS Terminal Shipments – By Region

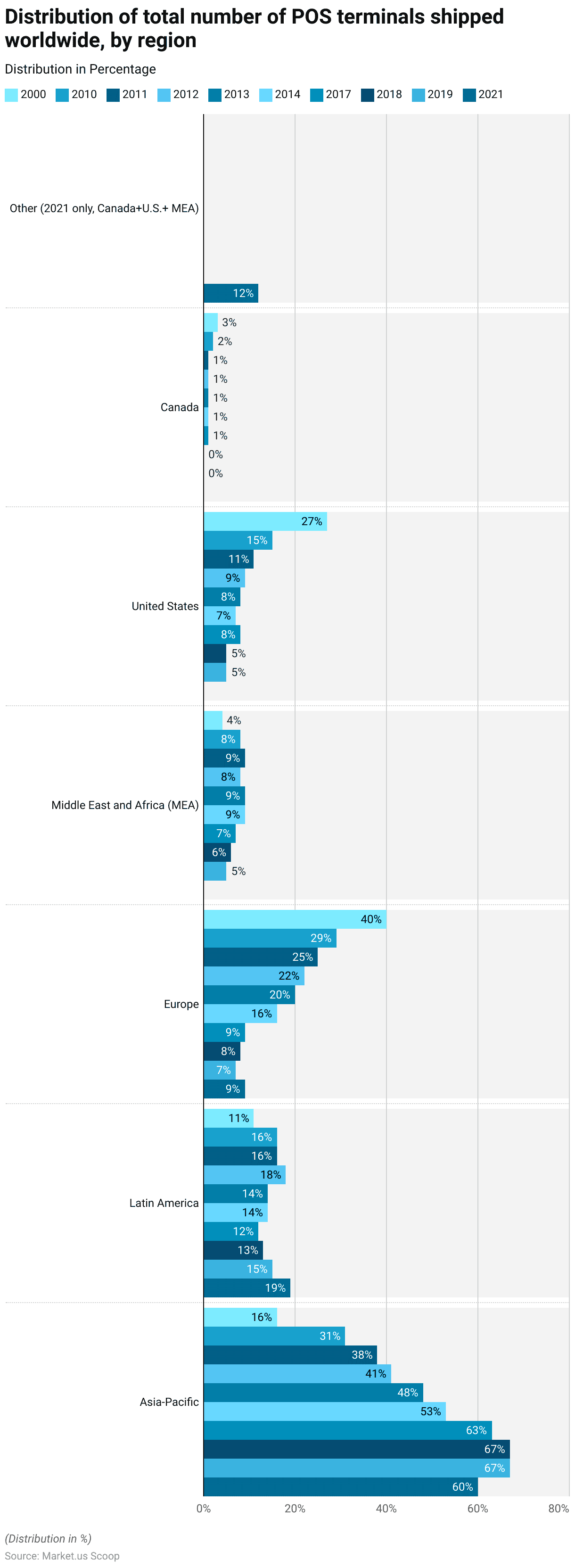

- From 2000 to 2021, the distribution of point-of-sale (POS) terminals shipped worldwide underwent significant regional shifts.

- In 2000, Europe accounted for the largest share at 40%, followed by the United States at 27%, Asia-Pacific at 16%, and Latin America at 11%.

- By 2010, Asia-Pacific had more than doubled its share to 31%. While Europe’s share decreased to 29%, and the United States dropped to 15%. Latin America maintained a steady share of 16%.

- The growth in Asia-Pacific continued, reaching 38% in 2011, 41% in 2012, and 48% in 2013. By 2014, Asia-Pacific had become the dominant region, with 53% of global shipments. While Europe fell to 16% and the U.S. dropped to 7%.

- This trend persisted, with Asia-Pacific capturing 63% of shipments in 2017 and peaking at 67% in both 2018 and 2019, as other regions’ shares declined. Europe, for instance, dropped to 7% in 2019.

- By 2021, Asia-Pacific’s share slightly decreased to 60%. While Latin America rose to 19%, and Europe’s share stabilized at 9%.

- Notably, in 2021, a new category, “Other,” comprising Canada, the U.S., and the Middle East and Africa, accounted for 12% of total shipments.

- These changes highlight Asia-Pacific’s emergence as the leading region for POS terminal shipments. Driven by rapid technological adoption and market growth.

(Source: Statista)

Largest Manufacturers of POS Terminals Worldwide

- From 2009 to 2022, the global Point of Sale (POS) terminal market witnessed significant growth and shifts among key manufacturers based on unit shipments.

- In 2022, Newland Payment Technology (NPT) led with 12.3 million units, up from 2.11 million in 2014.

- Tianyu is closely followed by 11.2 million units, maintaining steady growth since 2014.

- PAX, another major player from China, saw its shipments rise from 0.3 million in 2009 to a peak of 12 million in 2021 before slightly declining to 10.9 million in 2022.

- Centerm also exhibited notable growth, shipping 9.6 million units in 2022.

- New POS and Morefun, both Chinese manufacturers, showed strong performance in 2020, with shipments of 11.6 million and 11.5 million units, respectively. Although New POS’s volume declined to 9 million in 2022.

- Worldline/Ingenico from France consistently performed well, peaking at 14.1 million units in 2021.

- VeriFone, a leading U.S. manufacturer, shipped 8.9 million units in 2020 but saw reduced figures in subsequent years. SZZT and BBPOS, smaller players, also contributed significantly during the early 2010s, with shipments peaking at 3.94 million and 3.05 million units, respectively.

- Other notable contributors included Itron. Which shipped 3.8 million units in 2017, and NEXGO, which reached 3.45 million units in 2016.

- Hypercom, another U.S.-based manufacturer, was active early on, with 1.74 million units in 2009.

- This data underscores the dominance of Chinese manufacturers and the steady growth of European and U.S.-based players in the competitive POS terminal market over the years.

(Source: Statista)

POS Terminals- By Economic Activity

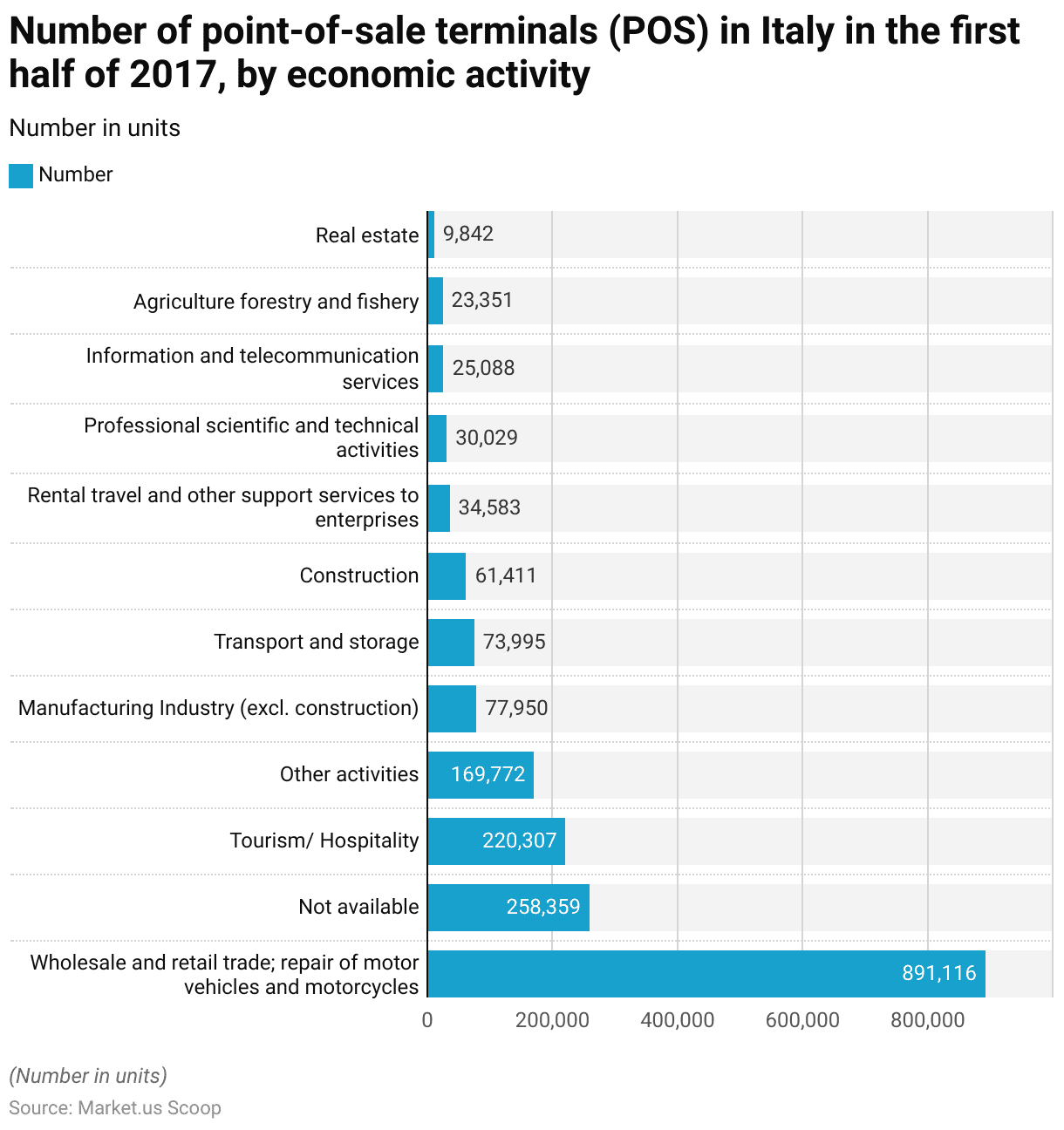

- In the first half of 2017, Italy’s Point of Sale (POS) terminal distribution varied significantly across different economic activities.

- The wholesale and retail trade sector, including the repair of motor vehicles and motorcycles. Accounted for the largest number of POS terminals, with 891,116 units.

- This was followed by sectors with unspecified data at 258,359 units and the tourism and hospitality sector at 220,307 units.

- Other miscellaneous activities utilized 169,772 POS terminals, while the manufacturing industry (excluding construction) had 77,950 units.

- Transport and storage accounted for 73,995 terminals, followed by the construction sector with 61,411 units.

- Rental, travel, and other support services to enterprises operated 34,583 POS terminals. Professional, scientific, and technical activities recorded 30,029 units, while information and telecommunication services accounted for 25,088 units.

- The agriculture, forestry, and fishery sectors used 23,351 POS terminals, and the real estate sector reported the lowest figure at 9,842 units.

- These figures highlight the widespread use of POS terminals across diverse sectors in Italy. Reflecting the nation’s increasing adoption of digital payment solutions.

(Source: Statista)

History and Evolution of Point of Sale Software Statistics

- The history and evolution of Point of Sale (POS) systems depict a significant technological transformation from simple mechanical devices to advanced cloud-based solutions.

- The journey began in 1879 when James Ritty invented the first mechanical cash register. It’s known as “Ritty’s Incorruptible Cashier,” to prevent employee theft by monitoring transactions.

- This device laid the foundational technology for all future developments in POS systems. Over the years, innovations such as electric cash registers in 1906 and electronic versions in the mid-20th century marked progressive milestones in POS technology.

- A breakthrough occurred in 1973 when IBM introduced the first true electronic POS system. Capable of managing multiple tills through a network, marking the dawn of modern POS systems.

- The introduction of graphical user interfaces in the 1980s by Gene Mosher, and later touchscreen capabilities revolutionized the usability and functionality of POS systems.

- The 1990s and early 2000s saw the advent of internet-based POS systems. Which further evolved into today’s cloud-based systems offering real-time data processing and integration with various business operations.

- As technology advanced, POS systems in the 2010s embraced mobile technologies. Allowing for more flexible and efficient customer interactions through mobile and tablet-based systems.

- Today, POS systems are not merely transactional tools but are integral to business operations. Providing critical data analytics, supporting inventory management, and enhancing customer experiences through loyalty programs and personalized service.

- The evolution of POS systems is a testament to the dynamic nature of retail and technological innovation. Reflecting broader trends in global commerce and digital transformation.

(Source: Mobile Transaction, Techradar, Restroworks, Tavolope)

Point of Sale Software Market Statistics

Global Point of Sale Software Market Size Statistics

- The global Point of Sale (POS) software market has exhibited a consistent upward trajectory at a CAGR of 15.1%, with its market size increasing steadily from USD 18.3 billion in 2022 to an estimated USD 74.7 billion by 2032.

- The market is projected to grow at a robust pace. Reaching USD 21.1 billion in 2023 and USD 24.2 billion in 2024.

- The growth continues with an expected market size of USD 27.9 billion in 2025 and USD 32.1 billion in 2026.

- By 2027, the market is anticipated to expand to USD 37.0 billion. Followed by significant growth to USD 42.6 billion in 2028 and USD 49.0 billion in 2029.

- The upward momentum is forecasted to persist, with the market reaching USD 56.4 billion in 2030, USD 64.9 billion in 2031, and culminating in USD 74.7 billion by 2032.

- This data underscores the rapid expansion and increasing adoption of POS software across various industries over the next decade.

(Source: market.us)

Global Point of Sale Software Market Size – By Deployment Mode Statistics

2022-2027

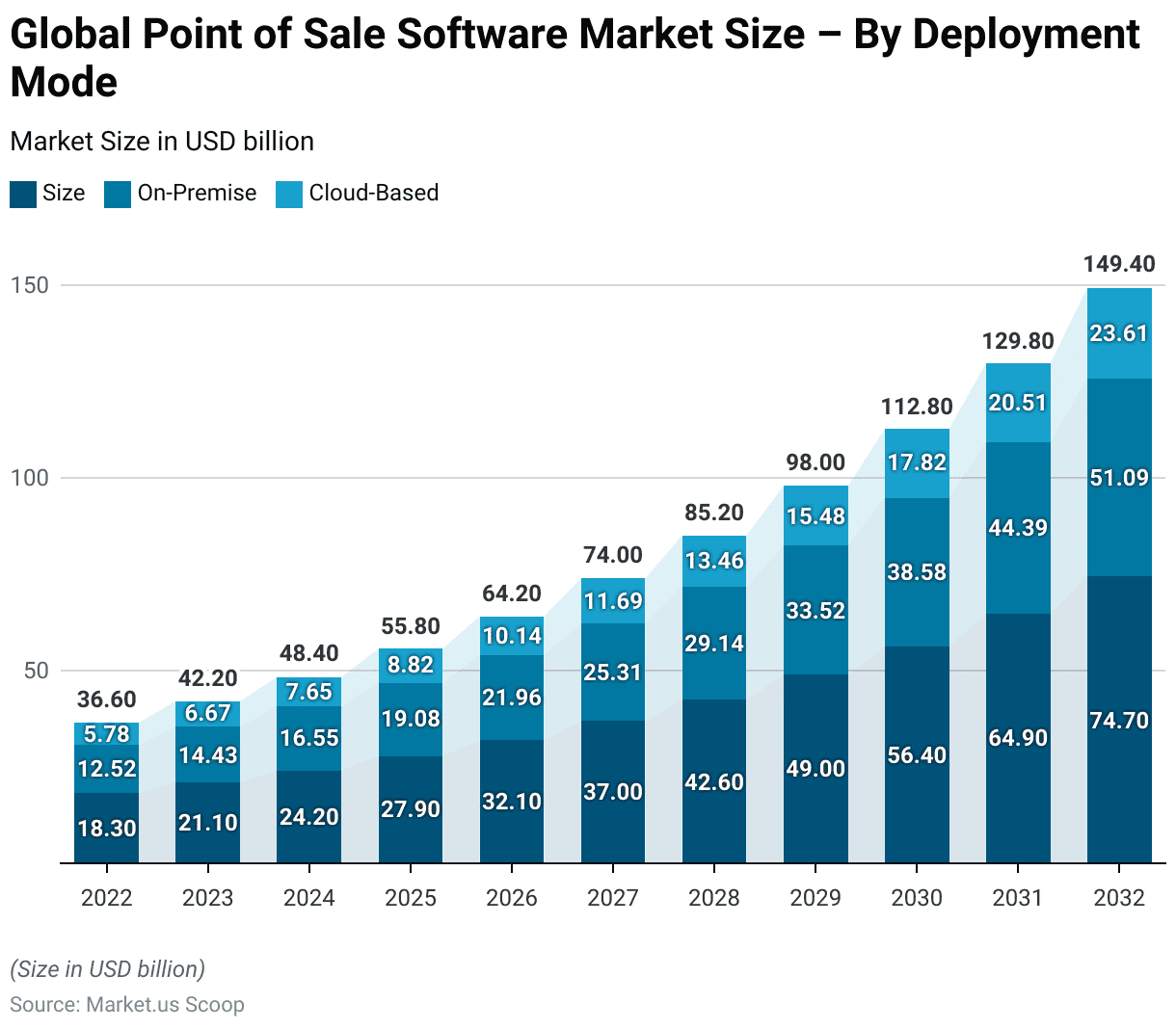

- The global Point of Sale (POS) software market is projected to witness substantial growth across both on-premise and cloud-based deployment modes.

- The market size stood at USD 18.3 billion in 2022. Comprised USD 12.52 billion from on-premise solutions and USD 5.78 billion from cloud-based solutions.

- By 2023, the total market is expected to grow to USD 21.1 billion. With on-premise deployments accounting for USD 14.43 billion and cloud-based solutions reaching USD 6.67 billion.

- This growth trend is forecasted to continue, with the market anticipated to reach USD 24.2 billion in 2024 (USD 16.55 billion on-premise and USD 7.65 billion cloud-based), USD 27.9 billion in 2025 (USD 19.08 billion on-premise, USD 8.82 billion cloud-based), and USD 32.1 billion in 2026 (USD 21.96 billion on-premise, USD 10.14 billion cloud-based).

- By 2027, the market is projected to expand further to USD 37.0 billion, with USD 25.31 billion attributed to on-premise solutions and USD 11.69 billion to cloud-based ones.

2028-2032

- In 2028, the total market size is expected to grow to USD 42.6 billion (USD 29.14 billion on-premise and USD 13.46 billion cloud-based).

- This upward trajectory continues into 2029 with a market size of USD 49.0 billion (USD 33.52 billion on-premise and USD 15.48 billion cloud-based), followed by USD 56.4 billion in 2030 (USD 38.58 billion on-premise, USD 17.82 billion cloud-based), and USD 64.9 billion in 2031 (USD 44.39 billion on-premise, USD 20.51 billion cloud-based).

- Finally, by 2032, the global POS software market is projected to reach USD 74.7 billion. With on-premise deployments contributing USD 51.09 billion and cloud-based solutions accounting for USD 23.61 billion.

- These figures highlight the growing adoption of both deployment models. With cloud-based solutions experiencing particularly rapid growth in response to increasing demand for flexible and scalable software solutions.

(Source: market.us)

Global Point of Sale Software Market Share – By Enterprise Size Statistics

- In 2022, the global Point of Sale (POS) software market was predominantly driven by large enterprises. Which accounted for 60.1% of the total market share.

- Small and Medium-Sized Enterprises (SMEs) contributed the remaining 39.9%.

- This distribution highlights the significant adoption of POS solutions among larger organizations. Which often require advanced and scalable systems to manage complex operations.

- However, the substantial share held by SMEs indicates a growing recognition of the value of POS software in streamlining business processes and enhancing customer experiences across smaller and medium-sized businesses.

(Source: market.us)

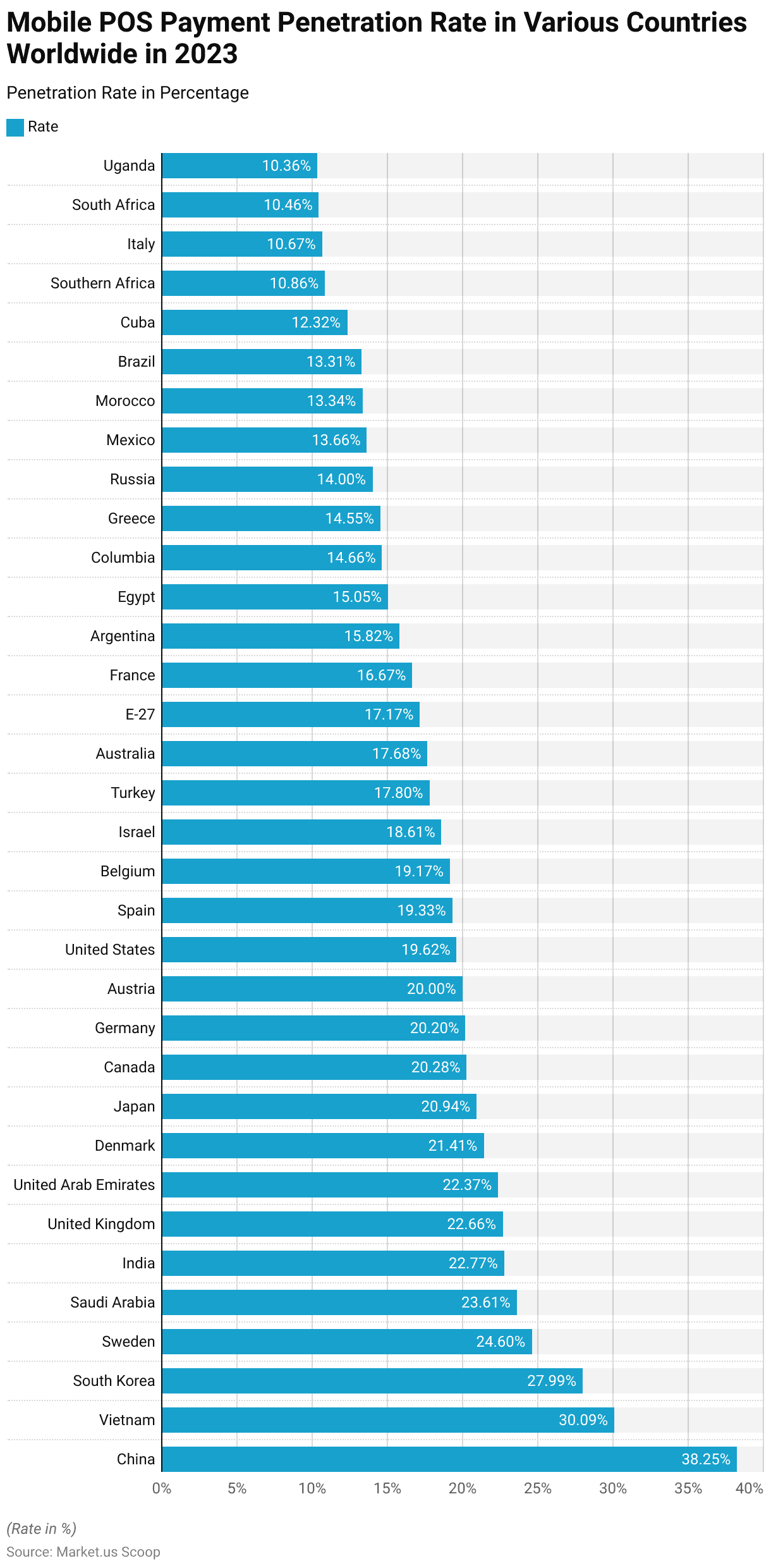

Mobile POS Payment Penetration Rate in Various Countries Worldwide

- In 2023, the penetration rate of mobile Point of Sale (POS) payments varied significantly across 34 countries worldwide.

- China led the market with a penetration rate of 38.25%. Followed by Vietnam at 30.09% and South Korea at 27.99%.

- Sweden recorded a penetration rate of 24.6%. While Saudi Arabia, India, and the United Kingdom posted similar rates of 23.61%, 22.77%, and 22.66%, respectively.

- The United Arab Emirates followed closely at 22.37%, with Denmark (21.41%) and Japan (20.94%) also showing strong adoption.

- Canada and Germany each recorded penetration rates above 20%. With 20.28% and 20.20%, respectively, while Austria reached an even 20%.

- The United States, Spain, and Belgium reported penetration rates of 19.62%, 19.33%, and 19.17%, respectively.

- Israel (18.61%), Turkey (17.80%), and Australia (17.68%) displayed moderate adoption levels. Along with the E-27 countries at 17.17%.

- France, Argentina, and Egypt reported rates of 16.67%, 15.82%, and 15.05%, respectively. While Columbia and Greece had similar figures at 14.66% and 14.55%.

- Russia stood at 14%, followed by Mexico (13.66%), Morocco (13.34%), and Brazil (13.31%).

- Cuba saw a penetration rate of 12.32%, with Southern Africa at 10.86%, Italy at 10.67%, South Africa at 10.46%, and Uganda rounding out the list with a penetration rate of 10.36%.

- These figures highlight the varying levels of adoption of mobile POS payments globally. Driven by differing levels of digital infrastructure and consumer preferences.

(Source: Statista)

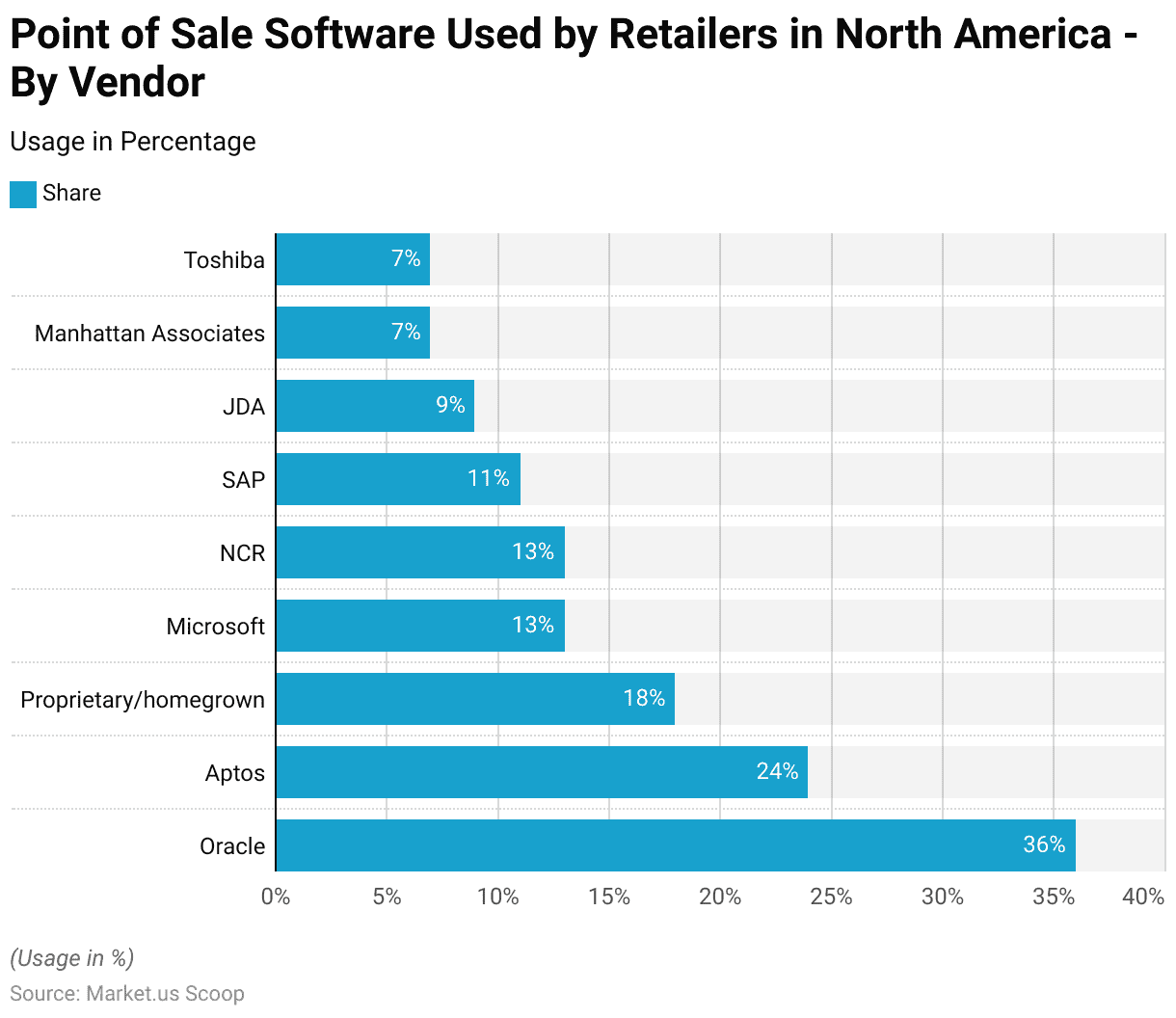

Point of Sale Software Used by Retailers Statistics

- As of late 2016, Oracle emerged as the leading provider of Point of Sale (POS) software among retailers in North America, capturing 36% of the market share.

- Aptos held the second position, with 24% of respondents indicating its use.

- Proprietary or home-grown solutions accounted for 18% of the market, highlighting the continued preference for customized software in certain segments.

- Microsoft and NCR both shared a 13% market presence, followed closely by SAP at 11%.

- JDA accounted for 9% of the market, while Manhattan Associates and Toshiba each held a 7% share.

- This data reflects a diverse competitive landscape in the North American POS software market during that period. With several key players and proprietary systems competing for retailer adoption.

(Source: Statista)

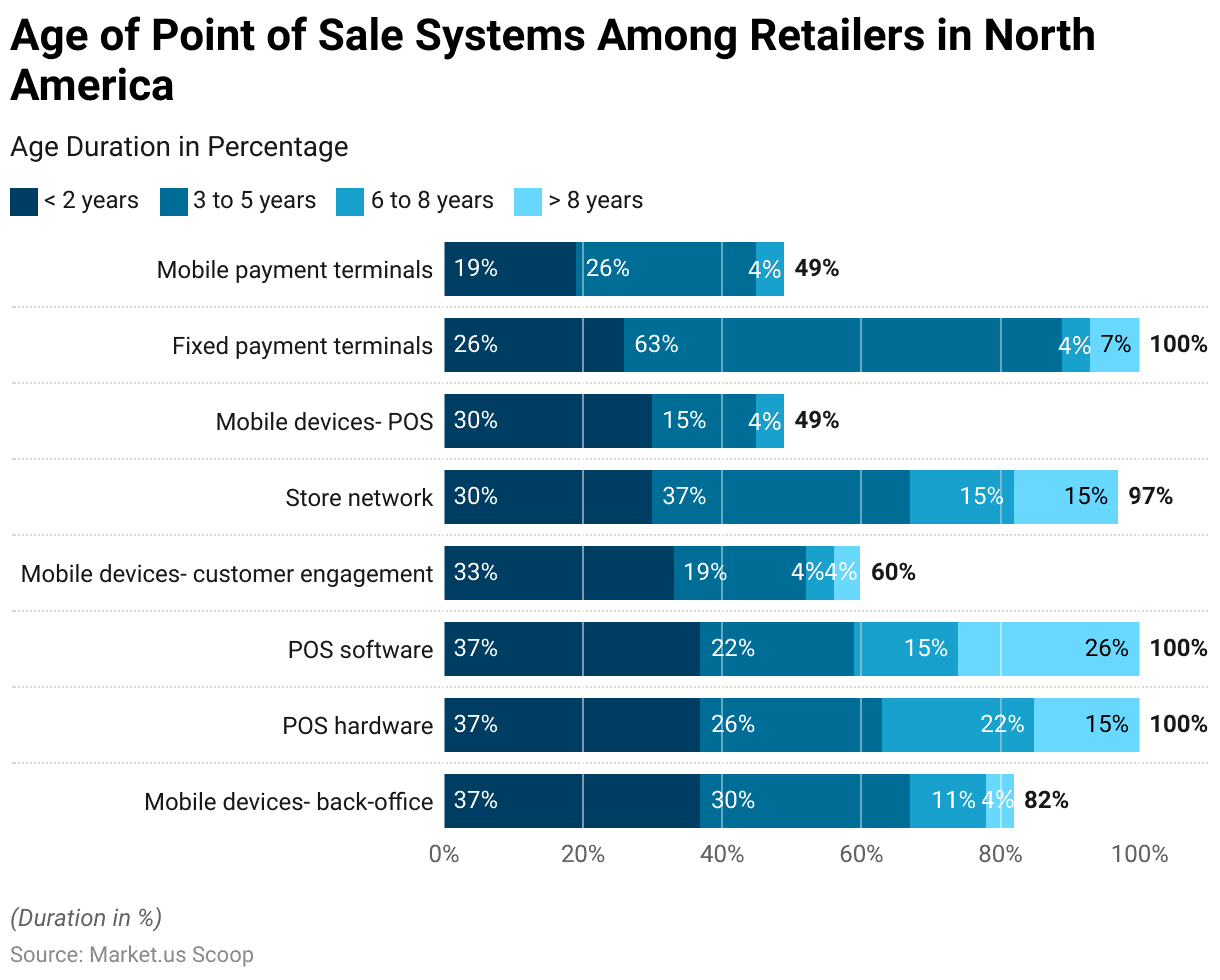

Age of Point of Sale Systems Software Among Retailers Statistics

- As of late 2019, the age of Point of Sale (POS) systems among North American retailers varied significantly across different system types.

- Mobile back-office devices and POS hardware were predominantly newer, with 37% of respondents reporting systems under two years old.

- Similarly, 37% of retailers indicated their POS software was also less than two years old. However, 26% reported using software older than eight years, indicating a notable share of legacy systems.

- Mobile devices for customer engagement showed a somewhat newer profile. With 33% of systems under two years old and only 4% exceeding eight years.

- Store networks demonstrated a broader age distribution, with 30% under two years old, 37% between three to five years old, and 15% each for the six-to-eight and over-eight-year categories.

- For mobile devices used at POS, 30% were less than two years old, with fewer older systems reported.

- Fixed payment terminals exhibited the highest proportion of mid-aged systems. With 63% in the three-to-five-year range, while 26% were newer (under two years).

- Lastly, mobile payment terminals were the newest overall. With 19% under two years and 26% in the three-to-five-year range, but only 4% in older categories.

- This data reflects a mix of modernization efforts and continued reliance on older technologies within the retail sector.

(Source: Statista)

Point of Sale (POS) Service Priorities Among Retailers

- In 2021, the primary Point of Sale (POS) service priorities among North American retailers centered around enhancing operational efficiency and improving customer experience.

- The most significant priority was cited by 67% of respondents. It was the addition or enhancement of Order Management System (OMS) integration.

- Omni-channel capabilities and integration, along with POS software upgrades or replacements, were equally important. With 52% of retailers focusing on these areas to ensure seamless and consistent customer interactions across multiple channels.

- Mobile POS adoption was a priority for 33% of respondents, reflecting the growing demand for flexible, on-the-go payment solutions.

- POS hardware upgrades or replacements and the addition or enhancement of Customer Relationship Management (CRM) capabilities were each a focus for 30% of retailers.

- Meanwhile, 22% of respondents prioritized implementing a unified or single payment platform to streamline payment processes.

- Lastly, improving payment security and ensuring PCI compliance was a priority for 15% of retailers. Emphasizing the need to safeguard sensitive customer data and maintain regulatory compliance.

- These priorities highlight a strategic focus on technology upgrades and integration to drive retail performance and customer satisfaction.

(Source: Statista)

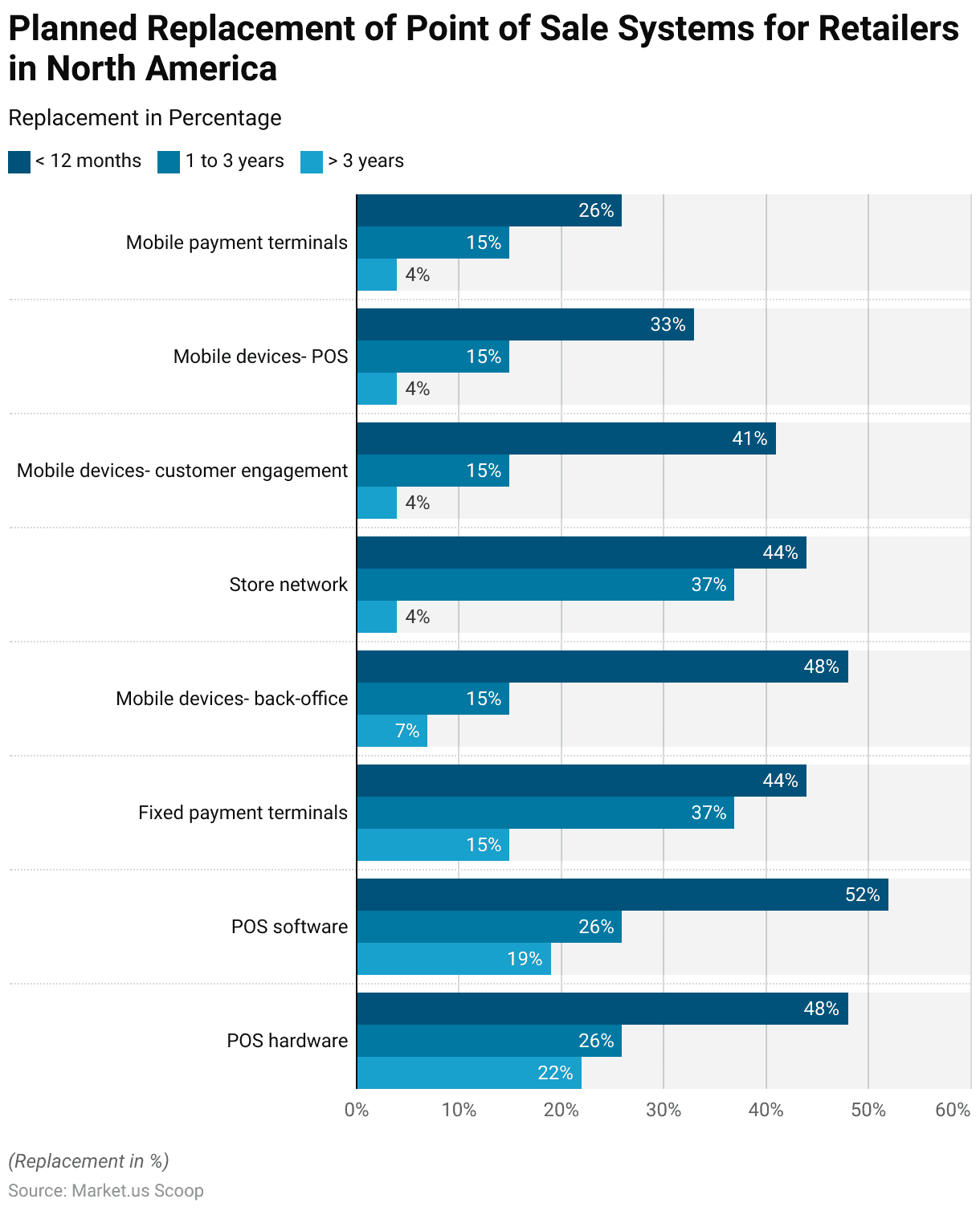

Planned Replacement of Point of Sale Software Systems for Retailers Statistics

- As of late 2019, North American retailers displayed varying timelines for replacing their Point of Sale (POS) systems.

- POS software and hardware upgrades were prioritized, with 52% and 48% of respondents, respectively, planning replacements within the next 12 months.

- For fixed payment terminals and store networks, 44% of retailers intended to replace these systems within a year, with an additional 37% planning to do so within one to three years.

- Mobile devices used for back-office operations showed a similar trend, with 48% scheduled for replacement within 12 months and 15% within one to three years.

- Mobile devices for customer engagement and POS applications followed a more conservative replacement schedule, with 41% and 33%, respectively, planning updates within the next year.

- Mobile payment terminals had the longest replacement timelines, with only 26% of respondents targeting upgrades within 12 months and 15% planning replacements within one to three years.

- Overall, these figures indicate a significant push towards modernizing retail POS systems, particularly in software and hardware components.

(Source: Statista)

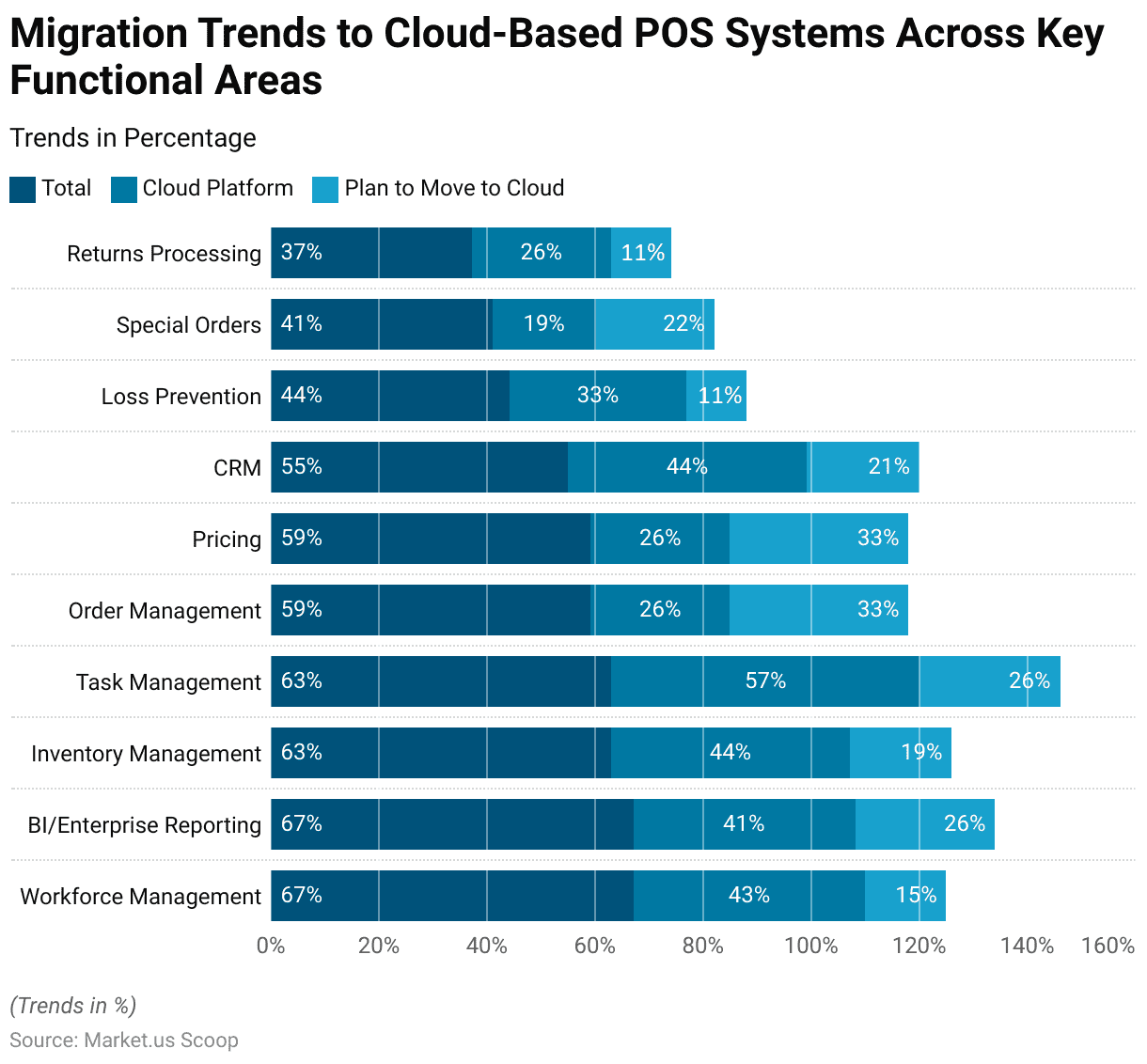

Migration Trends to Cloud-Based POS Systems Across Key Functional Areas

- The adoption of cloud-based Point of Sale (POS) software among retailers is growing across various functional areas.

- Workforce management and business intelligence/enterprise reporting lead the way. With 67% of respondents indicating use and 43% and 41%, respectively, already utilizing cloud platforms.

- Inventory management and task management are closely followed, with 63%, 44%, and 57% of respondents, respectively, having moved these functions to the cloud.

- Meanwhile, 59% of respondents use cloud solutions for order management and pricing. Though only 26% of each currently operate on cloud platforms, 33% planning to migrate in both areas.

- Customer relationship management (CRM) is utilized by 55% of retailers. With 44% already on the cloud and 21% planning to transition.

- Loss prevention systems are in use by 44%, with a smaller cloud adoption rate of 33% and 11% planning to migrate.

- Special orders and returns processing are the least cloud-integrated functions, with 41% and 37% of respondents using these systems, but only 19% and 26% currently operating in the cloud, and 22% and 11% planning to move these functions to the cloud.

- This data highlights the strategic focus on migrating critical retail operations to cloud platforms for improved flexibility and efficiency.

(Source: International Journal of Innovative Research in Computer Science and Technology (IJIRCST))

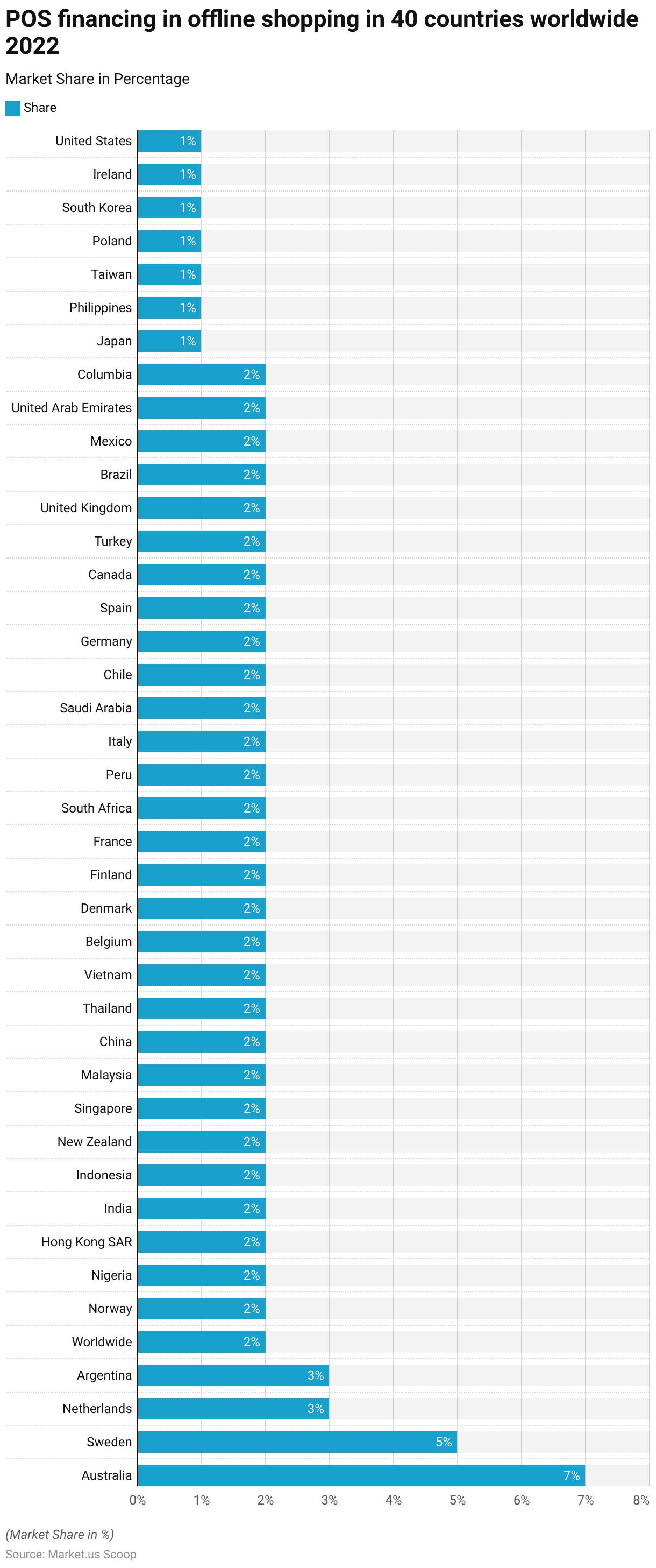

Financing and Investments

- In 2022, the market share of Point-of-Sale (POS) financing, including Buy Now, Pay Later (BNPL) services, in offline retail payments showed notable regional variation across 40 countries and territories.

- Australia led with a 7% market share, followed by Sweden at 5% and the Netherlands and Argentina at 3% each.

- Further, a wide range of countries, including Norway, Nigeria, Hong Kong SAR, India, Indonesia, New Zealand, Singapore, Malaysia, China, Thailand, Vietnam, Belgium, Denmark, Finland, France, South Africa, Peru, Italy, Saudi Arabia, Chile, Germany, Spain, Canada, Turkey, the United Kingdom, Brazil, Mexico, the United Arab Emirates, and Columbia, all recorded a 2% market share.

- Meanwhile, Japan, the Philippines, Taiwan, Poland, South Korea, Ireland, and the United States each held a 1% share in the offline retail POS financing market.

- This data highlights the growing global presence of POS financing and BNPL services. With higher adoption rates in specific regions, particularly in Australia and parts of Europe.

(Source: Statista)

Impact of Demonetization Policy

- The average number of point-of-sale (POS) transactions across India saw a significant increase following the demonetization announcement in November 2016.

- In October 2016, before demonetization, the number of POS transactions stood at 5.08 million.

- However, by November 2016, this figure had surged to 9.81 million. This reflects a dramatic rise in digital transactions as consumers and businesses adapted to the reduced availability of cash.

- This shift highlights the immediate impact of demonetization on payment behavior, with increased reliance on electronic payment methods.

(Source: Statista)

Innovation and Developments in Point of Sale Software Statistics

- In the rapidly evolving retail landscape, point-of-sale (POS) software innovations are pivotal for enhancing customer experience and operational efficiency.

- Moreover, recent developments have seen a significant shift towards cloud-based solutions, which offer the advantages of real-time data accessibility, scalability, and reduced maintenance costs, as noted by companies like ConnectPOS and Shopify POS.

- Alongside this, there is a notable emphasis on integrated payment processing systems, and robust inventory management features that facilitate seamless online and offline sales experiences.

- Advancements in POS hardware also play a critical role, with upgrades focusing on enhancing mobility and incorporating touchless payment technologies, which are increasingly replacing traditional swipe transactions.

- Moreover, the integration of data analytics in POS systems is becoming standard, enabling retailers to harness detailed insights into customer behaviors and sales patterns, thus driving informed decision-making.

- Further innovations include the use of artificial intelligence to personalize customer interactions and optimize store operations and IoT technology to improve the efficiency of in-store shopping experiences, like through the use of beacons for proximity marketing and enhanced customer engagement.

- Such advancements not only streamline operations but also significantly enrich the customer shopping experience, positioning POS systems as essential tools in the modern retail and hospitality sectors.

(Source: Connectpos, Fit Small Business, Hsc)

Regulations for Point of Sale Software Across Various Nations: Statistics

- In conducting market research on the regulations governing Point of Sale (POS) software across various jurisdictions, it becomes evident that the landscape is marked by complex, evolving legal frameworks that significantly impact compliance and operational strategies for businesses globally.

- Moreover, in the Philippines, the Bureau of Internal Revenue (BIR) has implemented Revenue Memorandum Order No. 24-2023 to standardize the accreditation of sales machines and software, including POS systems.

- This order is aligned with the Ease of Paying Taxes law and mandates specific invoicing requirements to avoid penalties.

- In the United States, the scenario is markedly diverse due to the lack of a unified tax system, which results in different sales tax obligations for software and SaaS products across various states.

- This complexity requires businesses to navigate state-specific regulations to ensure compliance carefully.

- Internationally, the trend continues with countries adapting their tax laws to include digital and software products, reflecting the shift towards a more digital global economy.

- This includes regions like the European Union, which uses the VAT MOSS system to tax digital services based on customer location rather than the location of the business.

- Overall, businesses must remain vigilant and adaptable to manage their POS software in line with varying global regulations to ensure both compliance and operational efficiency.

(Source: Grant Thornton Philippines, Paddle)

Recent Developments

Acquisitions and Mergers:

- Shift4’s Acquisition of Revel Systems: In May 2024, Shift4 Payments announced its intention to acquire Revel Systems, a provider of cloud-based POS systems, for $250 million. This strategic move aims to enhance Shift4’s market presence in the restaurant and retail sectors.

- PNC’s Acquisition of Linga: In September 2022, PNC Financial Services Group acquired Linga, a cloud-based restaurant operating system provider, to expand its digital resources and enhance payment solutions for the hospitality industry.

Funding:

- SpotOn’s Series E Funding: In September 2021, SpotOn, a retail and restaurant POS system provider. Raised $300 million in Series E funding, elevating its valuation to $3.15 billion. The funds were allocated for the acquisition of Appetize, a digital and mobile commerce platform, to broaden SpotOn’s service offerings.

Product Launches:

- SumUp’s Expansion into E-commerce: In February 2019, SumUp, a mobile payments company, acquired the e-commerce platform Shoplo to diversify its product suite and offer comprehensive online selling solutions to merchants.

Conclusion

Point of Sale Software Statistics: The Point of Sale (POS) software market is experiencing rapid growth. Driven by the rising demand for digital payment solutions. Technological advancements and the increasing adoption of omnichannel retailing.

Cloud-based POS systems are gaining popularity for their scalability, while on-premise solutions remain essential for larger enterprises.

Industries such as retail, hospitality, and healthcare are leveraging POS systems to streamline operations and enhance customer experiences. With Asia-Pacific leading the market, adoption is also growing in emerging regions.

Despite challenges like cybersecurity risks and implementation costs. The market offers significant opportunities as businesses prioritize integrated, data-driven solutions to remain competitive in an evolving digital landscape.

FAQs

What is POS software?

POS software is a digital solution used by businesses to process transactions, manage sales, and perform other functions such as inventory management, customer relationship management (CRM), and reporting. It serves as the central hub for handling in-store, online, and mobile sales.

What are the key features of POS software?

Core features include sales transaction processing, inventory tracking, employee management, customer data management, sales reporting, and integration with other business tools like accounting and e-commerce platforms. Advanced systems may offer analytics, loyalty programs, and payment security compliance.

What are the benefits of using POS software?

POS software streamlines sales processes, improves inventory accuracy, enhances customer service, and provides real-time data insights to support decision-making. It also supports multi-channel sales, enabling businesses to offer seamless experiences across physical and online stores.

What’s the difference between cloud-based and on-premise POS systems?

Cloud-based POS systems are hosted online, offering remote access, automatic updates, and lower upfront costs. On-premise systems are installed locally, providing more control over data and operations but often requiring higher initial investment and maintenance.

Which industries benefit most from POS software?

POS software is widely used in retail, hospitality, restaurants, healthcare, and other service industries. It helps businesses in these sectors streamline operations, manage inventory, and deliver better customer experiences.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)