Table of Contents

Introduction

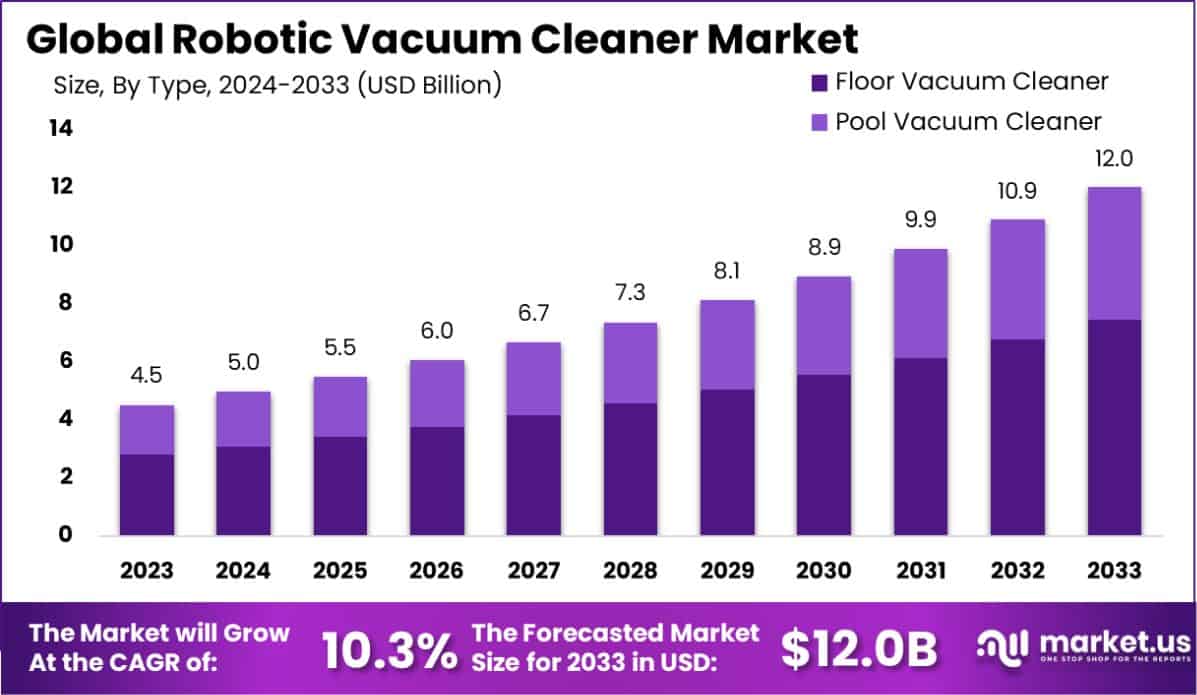

The Global Robotic Vacuum Cleaner market is projected to grow significantly, with its value estimated to rise from USD 4.5 billion in 2023 to approximately USD 12.0 billion by 2033. This represents a compound annual growth rate (CAGR) of 10.3% over the forecast period, 2024 to 2033.

A robotic vacuum cleaner, often referred to as a robovac, is an autonomous device equipped with intelligent programming and a limited vacuum cleaning system. The key characteristic of these devices is their ability to navigate home environments autonomously while removing dirt and debris from floors without human intervention. Typically, robotic vacuum cleaners are compact, disk-shaped appliances that utilize sensors and onboard cameras to map living spaces and identify obstacles, optimizing their cleaning paths for maximum efficiency.

The robotic vacuum cleaner market comprises the manufacturing, distribution, and sales of robotic vacuum cleaning devices. This market segment is part of the broader home automation and consumer electronics industries, reflecting the increasing consumer investment in smart home technology. The market is characterized by its rapid technological innovations, including the integration of AI, the development of multi-surface cleaning capabilities, and enhancements in battery life and suction power.

Growth in the robotic vacuum cleaner market is driven by several key factors. Firstly, the increasing consumer preference for smart home devices is a significant driver, as more individuals look to integrate technology that offers convenience and time-saving benefits. Additionally, advancements in artificial intelligence and machine learning have allowed these devices to offer enhanced navigation and efficiency, making them more appealing to tech-savvy consumers. Urbanization and smaller living spaces in cities also contribute to the demand for compact and efficient cleaning solutions, such as robotic vacuum cleaners.

Demand for robotic vacuum cleaners is primarily fueled by the rising need for convenient and hassle-free cleaning solutions, particularly in urban households. The growing number of dual-income families and the busy lifestyles associated with urban living have made time-saving devices more necessary and desirable. Moreover, the heightened awareness of indoor air quality and cleanliness has further propelled the demand for these devices, as they can maintain regular cleaning without requiring daily human effort.

The market presents numerous opportunities for expansion and innovation. There is a growing trend toward connected homes, where robotic vacuum cleaners can be integrated with other smart home systems for more synchronized and efficient household management. There is also potential for growth in developing markets, where penetration of home automation products is still in the early stages.

Companies can explore enhancements in battery technology, suction power, and even additional functionalities like mopping and UV sterilization to differentiate their products in a competitive market. The increasing consumer interest in products that support a hygienic home environment post-pandemic is also an opportunity for brands to expand their reach and influence within the market.

Key Takeaways

- The global robotic vacuum cleaner market is projected to reach approximately USD 12.0 billion by 2033, up from USD 4.5 billion in 2023, reflecting a robust CAGR of 10.3% over the forecast period from 2024 to 2033.

- The Floor Vacuum Cleaner segment led the market in 2023, commanding a significant 62.3% share. This underscores its widespread adoption for efficient floor cleaning solutions.

- The Residential segment emerged as the dominant category in 2023, accounting for 47.6% of the market. This highlights the growing preference for automated cleaning solutions in households.

- The Online segment captured the largest share of 57.2% in 2023, reflecting the increasing consumer shift toward e-commerce for purchasing robotic vacuum cleaners.

- The Asia Pacific region held a leading position in 2023, with a market share of 43.6% and revenue reaching USD 1.9 billion. This dominance is driven by the region’s expanding middle class, rising disposable incomes, and rapid urbanization.

Robotic Vacuum Cleaner Statistics

- By 2024, North America will have approximately 78 million smart homes, with widespread use of intelligent robot cleaners.

- In 2023, the vacuum cleaner market in homes reached $1.9 billion, making up 61.5% of total sales.

- China led the global smart robot vacuum market in 2023, shipping 4.6 million units.

- Ecovacs held 42% of China’s smart vacuum market in 2022, followed by Roborock (17%) and Mi (15%).

- Globally, 89% of users spend less than an hour vacuuming.

- Worldwide shipments of smart vacuum devices reached 18.5 million units in 2023, valued at $7.8 billion.

- The residential segment accounted for 75% of robot vacuum sales.

- As of 2023, 12% of U.S. households owned a robotic vacuum cleaner.

- 62% of robot vacuum owners use their devices at least four times weekly.

- Consumer spending on robotic vacuums rose by 15% in 2023 compared to 2022.

- User satisfaction with robotic vacuums stands at 83%.

- Battery life is a primary concern for 45% of users.

- Advanced robot vacuums can map spaces up to 600 square meters.

AI-powered obstacle detection lowers collision rates by 75%. - Newer models offer up to 180 minutes of runtime per charge.

- High-end models deliver suction power of up to 5000Pa.

- Smartphone app connectivity is included in 92% of new robot vacuum models.

- iRobot (Roomba) holds a 45% global market share, followed by Ecovacs at 15%.

- Over 100 brands compete in the global robotic vacuum market.

- The average price of robotic vacuums fell by 8% in 2023 due to competition.

- Five major manufacturers control about 75% of the market.

- Modern robots filter 99.9% of particles as small as 0.3 microns.

- Improved navigation systems reduced average cleaning time by 30%.

- Self-emptying models can store up to 60 days of debris.

- Smart mapping cuts cleaning time by 40% versus random navigation.

- Energy consumption in newer models is 20% lower than earlier versions.

- The average lifespan of a robotic vacuum ranges from 4 to 6 years.

- Battery replacement is typically required every 2 to 3 years.

Emerging Trends

- Integration with Smart Home Ecosystems: Robotic vacuum cleaners are increasingly integrated into smart home systems, allowing seamless connectivity with devices like Google Nest Hub and Amazon Alexa. This trend enhances their functionality, enabling users to control cleaning routines via voice commands or smartphone apps, reflecting the broader adoption of smart technologies in households.

- AI and Machine Learning Enhancements: Modern robotic vacuums utilize artificial intelligence and machine learning for advanced navigation, obstacle avoidance, and customized cleaning patterns. These features improve efficiency and user experience, as devices learn to adapt to the unique layouts of homes over time. Such technological sophistication positions these devices as essential in urban and tech-savvy homes.

- Growing Demand for HEPA-Equipped Models: As air quality becomes a priority, robotic vacuums with HEPA filters are gaining traction. These models not only clean floors but also improve indoor air quality by trapping allergens and fine particles, catering to health-conscious consumers and those with allergies.

- Expansion in Emerging Markets: The Asia-Pacific region, particularly China and India, is witnessing rapid adoption of robotic vacuum cleaners, driven by rising disposable incomes and urbanization. These markets are also benefiting from increased e-commerce penetration, which makes advanced cleaning solutions more accessible.

- Eco-Friendly and Cost-Efficient Innovations: Manufacturers are focusing on developing energy-efficient models with eco-friendly materials. Additionally, innovations such as automatic dirt disposal and long-lasting batteries are reducing maintenance efforts, appealing to environmentally conscious and cost-sensitive consumers

Top Use Cases

- Residential Cleaning and Smart Home Integration: Robotic vacuum cleaners have become indispensable in households, particularly within smart homes. These devices not only automate floor cleaning but also integrate with systems like Amazon Alexa and Google Assistant, allowing users to schedule and control cleaning via voice commands or apps. In 2023, approximately 63 million U.S. homes used smart home devices, with robotic vacuums being a key component in simplifying domestic chores.

- Enhanced Air Quality Through HEPA Filtration: Equipped with High-Efficiency Particulate Air (HEPA) filters, robotic vacuums address a critical health need by capturing allergens, dust, and fine particles. This feature is especially beneficial in urban areas with poor air quality and for individuals with allergies, supporting the dual purpose of cleaning and improving indoor air conditions.

- Commercial Cleaning in Public Spaces: In commercial settings such as hotels and airports, robotic vacuums are utilized to maintain high-traffic areas. Their ability to operate autonomously during non-business hours maximizes cleaning efficiency. As of 2024, businesses are increasingly adopting these robots to reduce labor costs while ensuring consistent cleaning standards.

- Cleaning Hard-to-Reach and Specialized Areas: Advanced models, such as those with slim designs or specialized navigation systems, excel in cleaning under furniture or along baseboards. Robotic vacuums with mopping functionalities further extend their use to hard floors, offering dual cleaning solutions. This versatility has driven their popularity in households and offices alike.

- Cost-Effective Maintenance of Large Spaces: For larger residential and commercial properties, robotic vacuums provide an economical cleaning solution. Their low maintenance and long-term operational savings outweigh the initial investment, which can range from $300 to $1,300 depending on features. This cost efficiency is a significant driver in the growing adoption of these devices

Major Challenges

- High Initial Costs: The premium pricing of robotic vacuum cleaners, with advanced models like the iRobot Roomba S9+ costing over $1,200, deters cost-conscious consumers. This challenge is particularly pronounced in emerging markets where purchasing power is lower. Despite the potential for long-term savings, the upfront investment remains a barrier to widespread adoption.

- Limited Performance in Complex Environments: Robotic vacuums often struggle in cluttered spaces, uneven surfaces, or homes with multiple levels. Their ability to navigate and clean effectively diminishes in these scenarios, leading to consumer dissatisfaction. Additionally, models with limited suction power may fail to clean thick carpets or remove pet hair efficiently.

- Privacy Concerns and Data Security: The use of cameras and mapping technologies raises privacy issues. Devices that store or transmit home layout data could become targets for cyberattacks. Consumers are increasingly wary of these risks, especially as the number of connected devices in smart homes grows, potentially slowing market penetration.

- Counterfeit Products and Low-Quality Alternatives: The market faces challenges from counterfeit or substandard products, which offer lower prices but compromise on quality. These products can harm brand reputation and erode consumer trust. Additionally, the availability of low-cost, non-branded alternatives complicates the competitive landscape for established players.

- Maintenance and Longevity Issues: While robotic vacuums are marketed as low-maintenance, users frequently encounter issues like battery degradation, limited dustbin capacity, and worn-out brushes. These issues, coupled with the cost of replacement parts, can affect the perceived value of the devices. This poses a challenge in retaining consumer loyalty and achieving long-term adoption.

Top Opportunities

- Integration with Smart Ecosystems: The increasing compatibility of robotic vacuum cleaners with smart home ecosystems such as Google Home and Amazon Alexa offers a significant growth avenue. These integrations allow users to control devices via voice commands, boosting convenience and driving adoption in tech-savvy households.

- Demand for Health-Focused Features: Features like HEPA filtration and UV sterilization, which enhance indoor air quality and reduce allergens, are gaining traction. These innovations cater to health-conscious consumers, particularly in regions with high pollution levels or growing awareness of respiratory health.

- Rising Adoption in Commercial Spaces: There is growing demand for robotic vacuum cleaners in commercial settings such as hospitals, hotels, and offices. Businesses benefit from automation, which reduces labor costs and ensures consistent cleaning standards, particularly in high-traffic or hygiene-critical environments.

- Product Diversification and Innovation: Manufacturers are expanding their product lines to include models with advanced navigation, self-emptying capabilities, and dual cleaning modes (vacuuming and mopping). These enhancements appeal to a wider range of consumers, offering solutions for diverse cleaning needs.

- Opportunities in Emerging Markets: Urbanization and rising disposable incomes in emerging economies, especially in Asia and Latin America, present a fertile ground for market expansion. Affordable, feature-rich models designed for these markets can drive adoption, especially as consumers in these regions increasingly seek time-saving home solutions.

Key Player Analysis

- iRobot Corporation: iRobot is a leader in the robotic vacuum space, renowned for its Roomba series. In 2022, the company launched the Roomba J7+, featuring advanced AI for obstacle detection and personalized cleaning routines. iRobot was acquired by Amazon for $1.7 billion, signaling its strategic importance in the smart home ecosystem.

- Ecovacs Robotics: Ecovacs is known for its DEEBOT line, which combines vacuuming and mopping functionalities. Its advanced models integrate AI and LiDAR technology for precise navigation. Ecovacs holds a strong presence in the Asia-Pacific market, contributing significantly to its regional dominance in the robotic vacuum segment.

- Samsung Electronics: Samsung’s robotic vacuums, such as the Jet Bot series, leverage smart connectivity with their SmartThings ecosystem. Equipped with advanced suction power and self-cleaning brush technology, Samsung appeals to high-end consumers and smart home enthusiasts.

- Neato Robotics: Part of the Vorwerk Group, Neato Robotics specializes in D-shaped vacuums designed for efficient corner cleaning. The company’s flagship models, such as the Neato D10, feature HEPA filters and laser mapping for superior performance. Neato maintains a strong footprint in North America and Europe.

- SharkNinja: SharkNinja’s products are recognized for their affordability and robust performance. The Shark IQ Robot series offers features like self-emptying dustbins and voice control compatibility. This brand appeals to budget-conscious consumers seeking smart cleaning solutions

Recent Developments

- In 2024, Amazon ended its planned acquisition of iRobot, citing “undue and disproportionate regulatory hurdles.” The move followed objections from the European Union, which raised antitrust concerns. Both companies expressed disappointment but agreed to terminate the deal. As part of the agreement, Amazon will pay iRobot a $94 million termination fee. Following the announcement, iRobot revealed plans to lay off 31% of its workforce and announced the departure of its CEO.

- In 2023, Berkshire Grey confirmed receiving a non-binding offer from SoftBank to acquire the company for $1.30 per share in cash. The proposal is subject to due diligence and final negotiations.

- In 2023, Rockwell Automation completed its acquisition of Clearpath Robotics, a leader in autonomous mobile robots (AMRs) for industrial applications.

- In 2023, Agile Robots took over the operations of FRANKA EMIKA GmbH, a robotics company based in Munich. The agreement was approved by FRANKA EMIKA’s creditors, though financial terms were not disclosed.

Conclusion

The global robotic vacuum cleaner market is poised for substantial growth, driven by advancements in technology, rising consumer interest in smart home integration, and the growing need for convenient cleaning solutions. The market’s trajectory highlights the increasing demand for efficient, time-saving devices, particularly in urban and dual-income households. Innovations such as AI-powered navigation, HEPA filtration, and multi-functional capabilities like mopping are reshaping consumer expectations and expanding the use cases of robotic vacuums.

Additionally, emerging markets present significant opportunities for expansion due to rising disposable incomes and urbanization trends. However, challenges such as high initial costs, data security concerns, and performance limitations in complex environments must be addressed to sustain growth. Companies that focus on enhancing product affordability, expanding smart ecosystem compatibility, and emphasizing health-oriented features will likely gain a competitive edge in this rapidly evolving landscape

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)