Table of Contents

Introduction

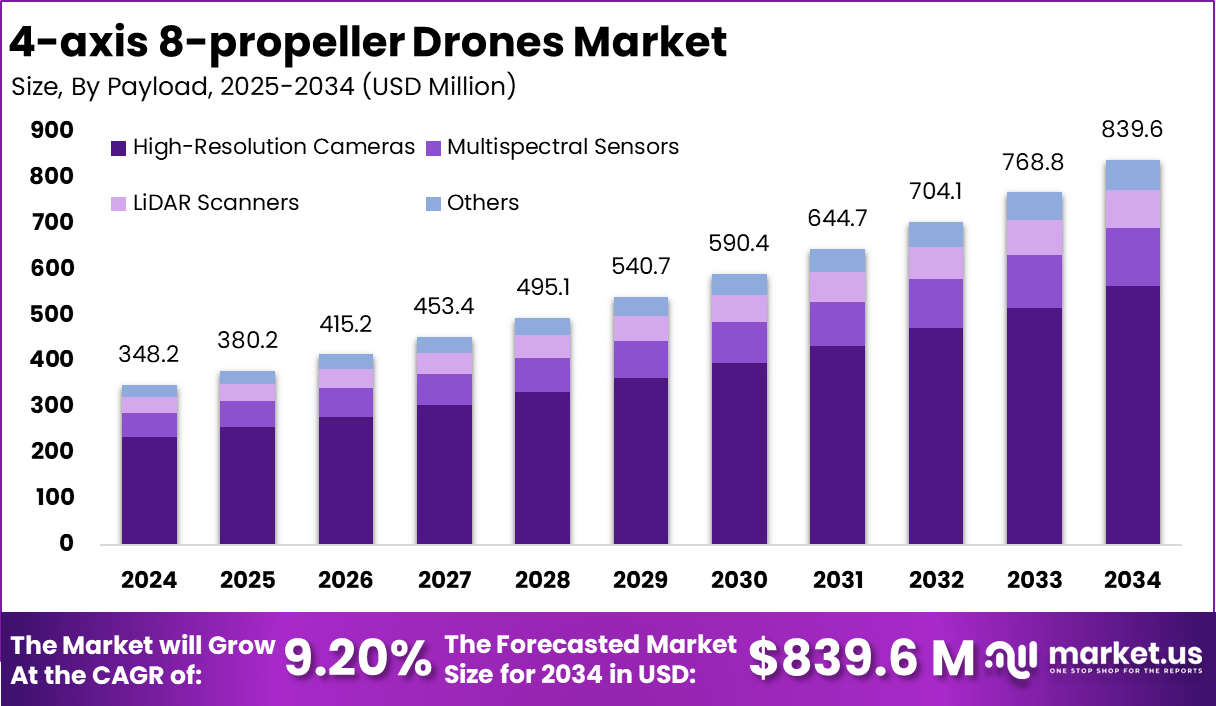

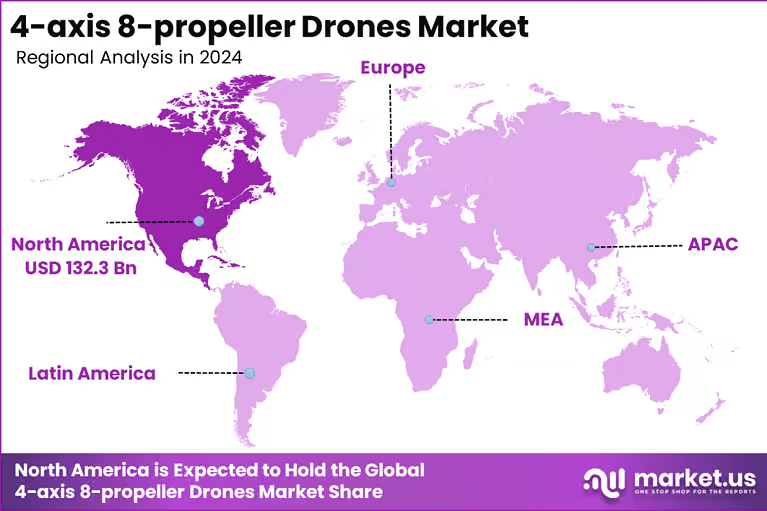

The global 4-axis 8-propeller drones market reached USD 348.2 million in 2024 and is projected to climb to USD 839.6 million by 2034 at a CAGR of 9.20%. North America held the leading 38% share in 2024, valued at USD 132.3 million, while the US accounted for USD 119.3 million and is projected to reach USD 241.3 million by 2034.

Demand remains concentrated in high-value industrial work, where high-resolution cameras led payload demand with 67.3%, surveying and mapping accounted for 48.7% of applications, construction contributed 39.4% of end-user demand, and semi-autonomous control systems captured 52.8%, showing a market shaped by precision imaging, workflow efficiency, and safer field operations.

How Growth is Impacting the Economy

Growth in the 4-axis 8-propeller drones market is supporting a wider digital field-services economy. These drones improve land surveys, progress tracking, inspection cycles, and asset documentation, which helps engineering, construction, utilities, mining, and public infrastructure projects reduce manual time and improve decision speed. In the US, total construction spending for December 2025 was reported at a seasonally adjusted annual rate of USD 2,168.8 billion, showing the size of the addressable environment where drone-based mapping, inspection, and site intelligence can create measurable productivity gains.

Economic impact also appears through software demand, pilot training, maintenance services, sensor integration, and compliance spending. As drone regulations mature, businesses invest not only in aircraft but also in traffic management, remote identification, data processing, and mission planning systems. The FAA states that UTM is a collaborative ecosystem for safely managing low-altitude drone operations, which means future growth extends across hardware, software, operations, and digital airspace services rather than aircraft sales alone.

Impact on Global Businesses

Rising costs and supply chain shifts are changing how global businesses procure and deploy 4-axis 8-propeller drones. Multi-sensor payloads, compliant communication modules, batteries, and ruggedized airframes add cost pressure, while tighter rules around tracking, airspace safety, and flight approvals increase pre-deployment expenses. The FAA’s Remote ID framework makes identification and location broadcasting a basic operating requirement for many registered drones, pushing manufacturers and buyers to favor compliant platforms and upgrade cycles.

Sector-specific impacts are becoming clearer. Construction and surveying firms benefit from faster topographic mapping, site verification, volumetric calculations, and inspection accuracy. Utilities and infrastructure operators gain safer access to hard-to-reach assets. Government and emergency teams benefit from situational awareness and route planning. In Europe, EASA’s 2025 update introduced the latest SORA 2.5 guidance into the regulatory framework, which supports more structured risk assessment for advanced operations and can improve confidence in industrial drone deployment.

Strategies for Businesses

Businesses entering the 4-axis 8-propeller drones market should prioritize mission-specific value instead of competing only on hardware price. The strongest strategy is to align drone design with high-frequency commercial workflows such as surveying, mapping, construction monitoring, infrastructure inspection, and public safety imaging. Firms should also package aircraft with analytics, training, maintenance, and compliance support to build recurring revenue.

A second strategy is regulatory readiness. Companies that integrate Remote ID, safe-navigation features, data security, and documentation workflows into their products are better positioned for enterprise and government contracts. A third strategy is vertical specialization, where vendors tailor payloads, software outputs, and service models for construction, utilities, mining, and infrastructure rather than offering generic platforms. This improves customer retention and operating margins over time.

Key Takeaways

- The 4-axis 8-propeller drones market stood at USD 348.2 million in 2024 and is projected to reach USD 839.6 million by 2034.

- North America led with 38% share, confirming strong commercial adoption and ecosystem maturity.

- The US market reached USD 119.3 million in 2024 and is projected to expand steadily through 2034.

- High-resolution cameras remained the leading payload with 67.3%, showing the importance of imaging-led missions.

- Surveying and mapping dominated applications with 48.7%, making geospatial work the core revenue engine.

- Construction led end-user demand with 39.4%, reflecting strong use in site planning and progress monitoring.

- Semi-autonomous control systems held 52.8%, indicating customer preference for safer and more efficient operations.

- Compliance, airspace management, and data workflows are becoming as important as hardware performance.

Analyst Viewpoint

At present, the 4-axis 8-propeller drones market is in a strong commercial adoption phase, supported by growing use in surveying, mapping, construction monitoring, and infrastructure inspection. The segment is benefiting from clear demand for stable lift, better redundancy, and high-quality imaging in industrial missions. Regulation is also moving in a direction that supports scale, with FAA work on BVLOS and EASA’s updated guidance improving the framework for advanced operations. Looking ahead, the market carries a positive outlook because enterprise users increasingly want drones that fit into repeatable workflows, compliance systems, and data platforms, which supports both hardware sales and long-term service revenue.

Use Case and Growth Factors

| Use case | Why it matters | Growth factor |

|---|---|---|

| Surveying and mapping | Produces fast aerial data for land, terrain, and project measurement | Dominant application share of 48.7% supports repeat industrial demand |

| Construction progress monitoring | Tracks site changes, planning accuracy, and material movement | Construction led end-user demand with 39.4% |

| Infrastructure inspection | Helps inspect roofs, bridges, towers, and remote assets more safely | Need for safer, faster field inspection is expanding enterprise adoption |

| High-detail imaging and documentation | Captures accurate visual records for analysis and reporting | High-resolution cameras led payload demand with 67.3% |

| Semi-autonomous field operations | Reduces pilot burden and supports consistent mission execution | Semi-autonomous systems led with 52.8% |

| Compliance-ready enterprise deployment | Improves suitability for regulated commercial missions | Remote ID, UTM, and BVLOS progress are improving operating confidence |

Regional Analysis

North America is the leading regional market for 4-axis 8-propeller drones, holding 38% of global revenue in 2024. The region benefits from a mature commercial drone ecosystem, strong construction and infrastructure activity, and early regulatory movement around advanced operations. The US remains the key revenue base, reaching USD 119.3 million in 2024, with steady long-term expansion expected.

Europe remains important because EASA continues refining its drone regulatory framework, while the Asia Pacific is likely to gain momentum through infrastructure development, industrial inspections, and smart-city applications. Overall, regional demand is expected to stay strongest where regulation, enterprise budgets, and digital project management adoption move together.

Business Opportunities

The best business opportunities in the 4-axis 8-propeller drones market sit in specialized industrial deployments rather than broad consumer use. Surveying and mapping present a major opening because these missions require reliable lift, accurate imaging, and repeatable data capture. Construction monitoring is another strong area, especially where drones connect with digital project controls, site documentation, and inspection workflows.

Service-based models also offer room for growth, including drone-as-a-service, maintenance packages, analytics subscriptions, pilot support, and compliance consulting. Further, as regulation advances and enterprise customers seek fewer manual processes, vendors that combine aircraft, imaging payloads, software outputs, and post-flight intelligence are likely to capture the highest-value contracts.

Key Segmentation

The 4-axis 8-propeller drones market is currently defined by a clear industrial segmentation pattern. By payload, high-resolution cameras dominate with 67.3%, showing that image quality and field documentation remain central to buyer decisions. By application, surveying and mapping lead with 48.7%, making geospatial and measurement tasks the largest commercial use case.

End-user, construction holds 39.4%, supported by site planning, progress monitoring, and inspection demand. By control system, semi-autonomous drones account for 52.8%, reflecting a shift toward safer and easier operations. Together, these segments show a market built around precision data capture, operational reliability, and enterprise workflow integration.

Key Player Analysis

The competitive landscape in the 4-axis 8-propeller drones market is shaped by manufacturers and solution providers that compete on flight stability, payload quality, automation, compliance, and workflow integration rather than simple aircraft supply. Leading participants usually focus on improving endurance, camera output, navigation intelligence, and enterprise software compatibility.

Top Key Players in the Market

- DJI

- Autel Robotics

- Yuneec

- PowerVision

- Walkera

- Holy Stone

- Hubsan

- Contixo

- Snaptain

- Potensic

- Syma

- Eachine

- Betafpv

- GoolRC

- JJRC

- Others

Vendors that serve construction, surveying, utilities, and public-sector users are better positioned because these buyers value reliability, service support, and measurable field productivity. Competitive advantage also comes from building compliant systems that align with Remote ID, traffic management, and advanced operating requirements, which helps suppliers move from equipment sales toward broader solution-based contracts.

Recent Developments

- In August 2025, the FAA issued a proposed rule to standardize beyond-visual-line-of-sight drone operations, a major step toward safer and more scalable commercial deployment.

- In January 2026, the FAA reopened the comment period on that BVLOS proposal, showing continued policy activity around commercial drone operations.

- In March 2025, the FAA refreshed its Remote ID guidance, reinforcing identification and location broadcasting as a core compliance layer for many drone operations.

- In May 2025, the FAA updated its UTM guidance, underscoring the importance of interoperable low-altitude traffic management for future drone scale-up.

- In September 2025, EASA issued Decision 2025/018/R to introduce the latest SORA 2.5 package into guidance for drone operations, improving the regulatory pathway for advanced risk-based missions in Europe.

Conclusion

The 4-axis 8-propeller drones market is moving from equipment-led demand to workflow-led adoption. Strong momentum in surveying, mapping, and construction, combined with improving regulation and enterprise use cases, supports a favorable long-term outlook for manufacturers, service providers, and software-led drone ecosystem participants.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)