Table of Contents

Introduction

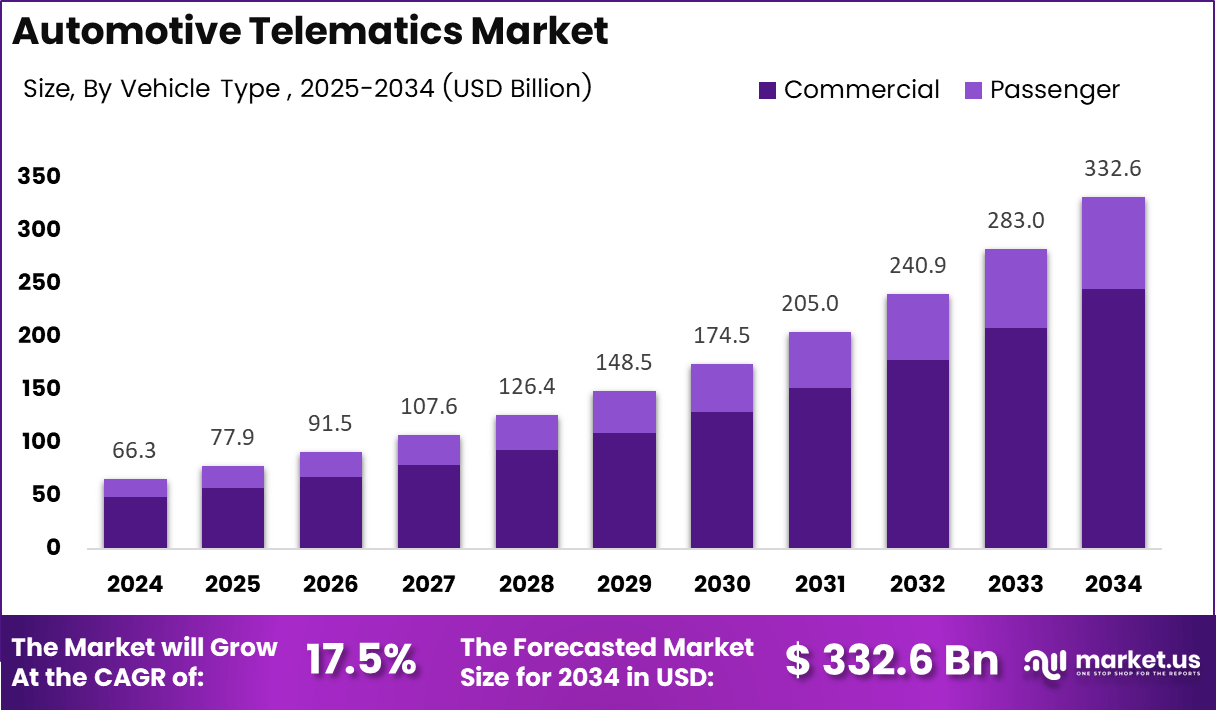

Market.us has released a comprehensive analysis of the Global Automotive Telematics Market, projecting robust expansion from USD 66.3 Billion in 2024 to USD 332.6 Billion by 2034. The market is forecast to grow at a CAGR of 17.5% over the 2025–2034 period, reflecting accelerating demand for connected-vehicle ecosystems enabling real-time monitoring, navigation, and predictive maintenance.

Consequently, automakers are integrating advanced telematics units directly into vehicle architectures to enhance operational visibility and customer engagement. Growing emphasis on intelligent routing, remote diagnostics, and vehicle safety is driving broader deployment of in-vehicle connectivity modules and cloud-enabled telematics services across both passenger and commercial segments.

Furthermore, government investment in Intelligent Transportation Systems and vehicle-to-everything communication frameworks is playing a critical role in market acceleration. Regulatory mandates requiring telematics-enabled emergency response systems, emission reporting, and automated safety features are compelling OEMs to adopt standardized connected architectures at scale.

Additionally, emerging opportunities across fleet automation, usage-based insurance, predictive maintenance, and EV ecosystem management are expanding the market’s addressable base. According to global telecom assessments, 9 out of 10 new vehicles are shipped with built-in internet connectivity, creating a strong foundation for high-bandwidth telematics data exchange powered by expanding 5G networks.

Finally, technology maturation across edge computing, AI-enabled diagnostics, cloud analytics, and cybersecurity frameworks is improving real-time decision-making and reducing vehicle operating downtime. As smart-city investments grow, telematics integration with traffic systems, environmental monitoring, and automated enforcement networks is broadening the market’s strategic importance globally.

Key Takeaways

- The Global Automotive Telematics Market is projected to grow from USD 66.3 Billion in 2024 to USD 332.6 Billion by 2034 at a CAGR of 17.5%.

- Asia Pacific dominates the market with a 47.4% share, generating USD 31.4 Billion in telematics revenue.

- Embedded technology leads the technology type segment with a 49.6% share.

- Component holds the highest solution share at 62.4%, driven by hardware and sensor integration.

- Passenger vehicles represent the largest vehicle segment with a 73.8% market share.

- Information and Navigation is the leading application area with a 34.9% share.

Market Segmentation Overview

By technology type, Embedded systems dominate with a 49.6% share, driven by OEM adoption of integrated connectivity, diagnostics, and performance monitoring built directly into vehicle architecture. Tethered systems serve cost-sensitive and retrofit markets, while Integrated systems advance steadily as manufacturers invest in unified digital ecosystems combining embedded processing with cloud-based applications.

By solution, Component leads with 62.4%, reflecting rising demand for GPS modules, sensors, and diagnostic control units. By vehicle type, Passenger vehicles hold a dominant 73.8% share, supported by EV adoption and digital cockpit preferences. By application, Information and Navigation commands 34.9%, driven by real-time traffic data, predictive routing, and integrated mapping platform adoption across connected vehicles globally.

Drivers

Expansion of software-defined vehicle architectures is a primary market driver. Automakers leveraging these designs can manage features remotely, push real-time navigation data, and deliver over-the-air updates without physical servicing. AI-based telematics layered onto these platforms further strengthens adoption by enabling driving behavior analysis, personalized safety recommendations, and improved insurance and fleet planning outcomes.

Cloud-based telematics platforms are driving equally significant demand. These systems store large volumes of vehicle data securely while enabling real-time monitoring, route optimization, and performance tracking across both passenger and commercial fleets. Combined with OEM mandates for predictive maintenance and remote diagnostics, cloud telematics is becoming a foundational component of next-generation connected mobility strategies worldwide.

Use Cases

Fleet management represents one of the most active and commercially mature telematics use cases. Logistics operators leverage vehicle tracking, fuel monitoring, automated compliance reporting, and driver performance analytics to reduce operational costs and optimize asset utilization. Mid-scale and large commercial fleets increasingly rely on telematics platforms to enhance on-road performance and strengthen competitiveness across transportation and delivery sectors.

Usage-based insurance is a rapidly growing application. Real-time driving-behavior analytics, mileage data, and risk scoring enable insurers to develop personalized premium products that reward safe driving. Both individual consumers and commercial fleet owners are embracing telematics-driven insurance for cost transparency and improved claims accuracy, deepening engagement across connected mobility ecosystems.

Major Challenges

High upfront installation costs present a meaningful adoption barrier, particularly among smaller fleets and budget-conscious buyers in developing markets. Hardware components, data subscription plans, and system integration fees create financial hurdles that push cost-sensitive customers toward basic solutions, slowing the transition to advanced connected telematics features and limiting market penetration in price-sensitive segments.

Data privacy and interoperability concerns compound the challenge. Location tracking, behavioral data, and continuous vehicle monitoring require strict regulatory compliance, and growing consumer distrust slows adoption in regions with stringent data protection frameworks. Simultaneously, legacy vehicles lacking compatible hardware make platform unification difficult for mixed-age fleets, creating inconsistent data quality and operational inefficiencies that reduce telematics return on investment.

Business Opportunities

Insurer-backed usage-based telematics models represent a compelling commercial opportunity. As insurers expand personalized premium programs rewarding safe driving, telematics providers gain recurring revenue streams while deepening integration into both consumer and commercial vehicle ecosystems. Growing acceptance among younger drivers and fleet operators globally is strengthening demand for telematics-enabled insurance products across major markets.

Expanding EV adoption creates a parallel and rapidly growing opportunity horizon. Electric vehicles rely heavily on connected systems for battery performance monitoring, charging route optimization, and energy-efficiency analytics. Telematics providers that develop EV-specific solutions and integrate seamlessly with charging infrastructure networks are positioned to capture premium revenue as electrification accelerates across passenger and commercial vehicle segments worldwide.

Regional Analysis

Asia Pacific leads the global market with a commanding 47.4% share valued at USD 31.4 Billion, driven by rapid connected-vehicle adoption, aggressive electrification programs, and strong 5G rollout across China, Japan, and South Korea. Government investments in smart mobility and intelligent transport systems further accelerate telematics penetration across both passenger and commercial fleets throughout the region.

North America demonstrates steady growth supported by advanced regulatory frameworks around vehicle safety, data compliance, and telematics-enabled insurance models, alongside expanding fleet digitization across logistics. Europe expands through strict EU safety mandates, eCall compliance requirements, and growing EV ecosystem connectivity needs. Latin America and Middle East & Africa are advancing gradually as OEM integration deepens, smart-city programs expand, and 4G/5G network coverage improves across emerging urban hubs.

Recent Developments

- In October 2025, Teletrac Navman, a Vontier company, was named “Vehicle Telematics Solution of the Year” at the 6th annual AutoTech Breakthrough Awards, recognizing its leadership in automotive and transportation technology innovation.

- In December 2025, Blue Cloud Softech Solutions announced a strategic MoU with ConnectM Technology Solutions to jointly develop a semiconductor-based EdgeAI System on Chip for advanced automotive cybersecurity applications, driving shares up 3%.

Conclusion

The Global Automotive Telematics Market is entering a high-growth phase anchored by vehicle electrification, software-defined architectures, AI-powered analytics, and expanding 5G connectivity infrastructure. With the market forecast to grow from USD 66.3 Billion in 2024 to USD 332.6 Billion by 2034 at a CAGR of 17.5%, stakeholders across automotive, insurance, logistics, and technology sectors face significant opportunities to capture value in the rapidly evolving connected-vehicle landscape.

As subscription-based service models, cybersecurity frameworks, and EV-specific telematics solutions mature, providers that invest in scalable, interoperable, and AI-enhanced platforms will define the competitive landscape of global automotive telematics through the decade ahead.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)