Introduction

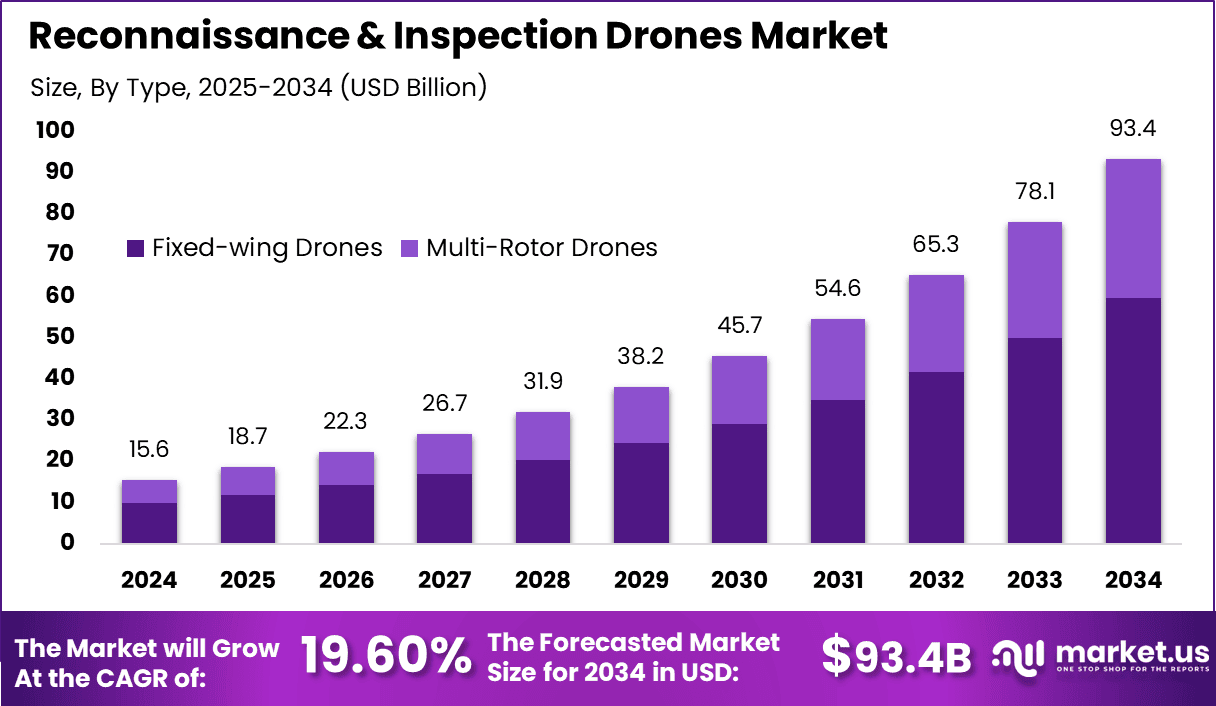

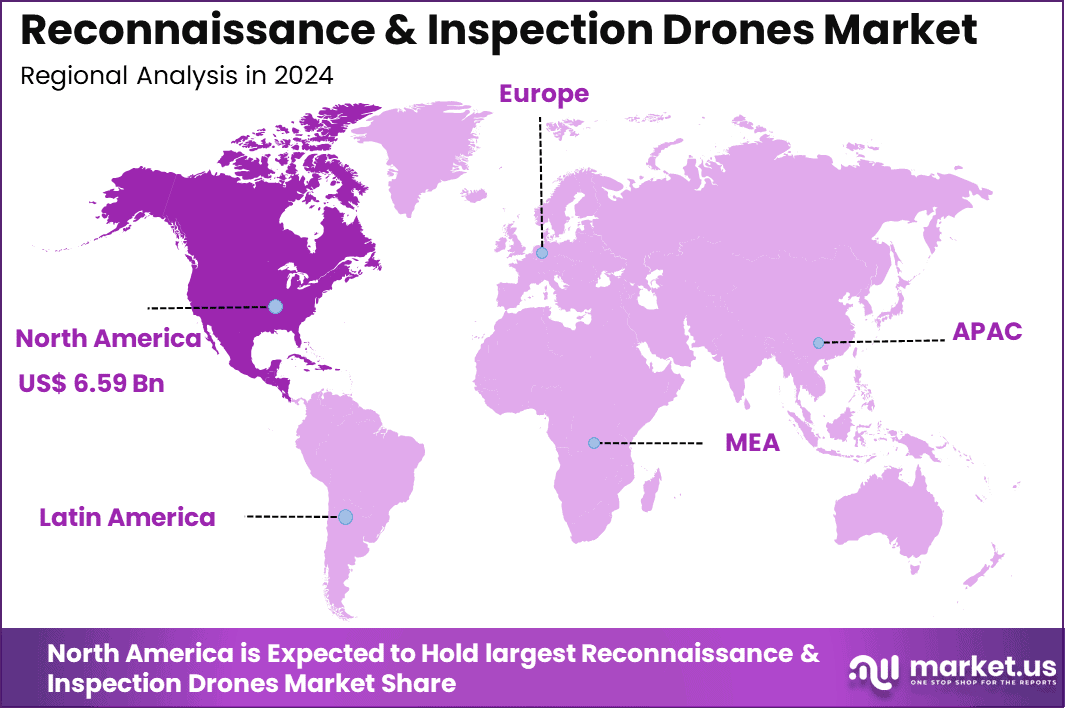

The Global Reconnaissance & Inspection Drones Market generated USD 15.6 billion in 2024 and is predicted to register growth from USD 18.7 billion in 2025 to about USD 93.4 billion by 2034, recording a CAGR of 19.60% throughout the forecast span. In 2024, North America held a dominan market position, capturing more than a 42.3% share, holding USD 6.59 Billion revenue.

Reconnaissance and inspection drones are becoming essential tools for monitoring, surveillance, and asset inspection across a wide range of industries. These drones are equipped with cameras, sensors, and imaging technologies that allow users to capture real time data from areas that are difficult or risky to access.

They are widely used in defense operations, infrastructure inspection, energy facilities, agriculture, and environmental monitoring. As organizations focus on improving safety and operational efficiency, drones are replacing manual inspection methods and enabling faster and more accurate data collection.

One of the key driving factors is the increasing need for safer inspection practices in hazardous and remote environments. Industries such as oil and gas, power generation, and construction require regular inspections of assets located in challenging conditions, and drones help reduce the need for human exposure to risks.

In addition, advancements in imaging and sensor technologies are improving the quality and detail of data collected by drones, making them more reliable for decision making. The growing use of drones in defense and security applications is also supporting market growth, as they provide real time surveillance and situational awareness. Regulatory support for commercial drone operations in several regions is further encouraging adoption.

Demand for reconnaissance and inspection drones is rising as organizations seek efficient and cost effective alternatives to traditional methods. There is a strong preference for drones that can operate for longer durations, cover large areas, and deliver high quality data in real time. Companies are also looking for solutions that can integrate with data analysis systems to convert captured information into actionable insights.

The demand is particularly strong in sectors that require frequent monitoring and maintenance, where drones help reduce downtime and improve accuracy. As industries continue to adopt digital and automated solutions, the need for advanced drone based inspection and reconnaissance capabilities is expected to grow steadily.

Keytake away

- Fixed-wing drones command 61.5% market share, delivering extended endurance, high-altitude operations, and real-time EO/IR feeds for persistent area coverage.

- Visual Line of Sight (VLOS) range captures 63.9%, enabling tactical coordination, immediate threat assessment, and operator oversight in forward operating environments.

- Military reconnaissance applications claim 41.8%, powering border patrol, target acquisition, and battle damage assessment with low-signature loitering capabilities.

- Defense & security end-users hold 52.6%, leveraging drones for counter-UAS training, infrastructure protection, and special operations force multiplication.

- North America drives 42.3% global value, with U.S. market at USD 5.94 billion and 17.4% CAGR, fueled by DoD Replicator initiatives and MQ-9 successor programs.

How AI is Reshaping the Future of this market?

AI is changing the Reconnaissance & Inspection Drones Market by making drones more intelligent, faster, and more independent during operations. Instead of only capturing images and videos, AI-enabled drones can now detect cracks, corrosion, heat leaks, intrusions, equipment faults, and unusual activity in real time.

This improves the value of drone inspections because operators receive usable insights much faster, with less dependence on manual review. AI is also helping drones improve route planning, obstacle avoidance, target tracking, and decision-making, which is increasing their role in security monitoring, infrastructure inspection, industrial asset checks, and border surveillance.

The future of this market is being shaped by higher autonomy and smarter analytics. AI is expected to support automated mission execution, predictive maintenance, and faster interpretation of large volumes of aerial data. This is especially important in sectors where timely inspection and continuous monitoring are critical.

As software becomes more capable, drones are expected to move from being support tools to becoming essential operational assets. This shift is strengthening market demand because end users are looking for solutions that improve accuracy, reduce response time, lower labor pressure, and deliver more reliable field intelligence.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 42.3% share and holding USD 6.59 Billion in revenue. This leadership was mainly supported by early and large scale adoption of reconnaissance and inspection drones across defense, homeland security, energy, utilities, and critical infrastructure monitoring.

The region has a strong advantage in drone software, sensor integration, AI-enabled imaging, and real-time data processing, which makes drone operations more reliable for complex inspection tasks. Demand has also remained strong because enterprises in the US and Canada continue to replace manual inspection methods with drone-based operations to improve worker safety, reduce inspection time, and increase coverage across large or hazardous sites.

North America also leads because of its mature commercial ecosystem and high spending capacity for advanced aerial systems. Government programs, defense modernization efforts, and industrial digitization have created a favorable environment for both tactical reconnaissance and asset inspection use cases. In sectors such as power transmission, pipelines, railways, construction, and public safety, drones are increasingly used for routine monitoring, predictive maintenance, and emergency assessment. This broad and practical adoption base keeps North America ahead of other regions, as the market benefits not only from technology development but also from faster deployment at scale.

Europe represents a strong and steadily developing market, supported by growing use of drones in border monitoring, environmental surveying, infrastructure inspection, and public safety operations. Countries across the region are focusing on modern inspection methods for bridges, rail systems, wind farms, and utilities, which is creating stable demand for drone solutions. Latin America is emerging at a moderate pace, with adoption mainly driven by mining, oil and gas, agriculture, and law enforcement applications, although budget limitations and uneven regulatory progress continue to affect wider deployment.

The Middle East and Africa are also showing rising interest, particularly for perimeter surveillance, pipeline inspection, desert infrastructure monitoring, and large-scale industrial site assessment. Growth in this region is supported by energy sector demand and security needs, though adoption remains more selective due to differences in funding, technical expertise, and drone operating frameworks across countries.

Driver

One of the main drivers in the Reconnaissance & Inspection Drones Market is the growing need for safe and efficient inspection across critical assets and remote sites. Many industries now prefer drones for checking pipelines, power lines, towers, bridges, industrial plants, and restricted zones because these systems reduce the need for manual field visits. This improves worker safety and allows inspection teams to gather visual information from areas that are difficult or risky to access. As a result, drones are becoming a practical tool for routine monitoring.

Another reason this driver is becoming stronger is the need for faster decision making in field operations. Drones can capture images, videos, and site data in a short time, which helps teams review asset conditions without long delays. This is especially useful in sectors where quick inspection can reduce downtime and support maintenance planning. The ability to cover large areas with less effort is also making drones more attractive for regular use.

Restraint

A major restraint in this market is the strict regulatory environment around drone operations. In many locations, drone flights are subject to airspace limits, safety rules, operator requirements, and permissions that vary by region and use case. This creates extra planning work for service providers and end users before any mission can begin. It also makes cross region deployment more complex for companies that want to scale drone inspection programs.

Another restraint is the concern around privacy and operational risk. Inspection drones often work near public spaces, private property, industrial facilities, or sensitive sites, which can raise concerns about data capture and air safety. These issues may slow approvals and create hesitation among users who are new to drone based inspections. In some cases, organizations continue to rely on conventional inspection methods because they are already familiar with those workflows.

Opportunity

A strong opportunity in this market lies in the rising use of drones as part of regular asset management programs rather than only for one time inspection tasks. Utilities, transport operators, construction teams, and industrial site managers are increasingly looking for ways to monitor assets more frequently and with better visibility. Drones fit well into this need because they can support planned inspections, condition checks, and site reviews with lower disruption. This creates room for wider adoption across both public and private sector operations.

There is also a major opportunity in combining drones with advanced software and sensor systems. When drone inspections are linked with thermal imaging, mapping tools, real time analytics, and automated fault detection, the value of each mission becomes much higher. This helps users move beyond simple image collection and toward faster issue identification and smarter maintenance planning. Over time, this can make drone based inspection a more trusted part of operational strategy.

Challenge

One key challenge in this market is maintaining reliable performance in real world inspection environments. Drones often operate near complex structures, harsh terrain, signal barriers, or changing weather conditions that can affect flight stability and data quality. Even when a drone reaches the target area, poor lighting, wind, dust, or limited visibility can reduce the usefulness of the captured information. This makes consistent inspection results harder to achieve across different job sites.

Another challenge is turning large volumes of inspection data into clear and useful outcomes. Drone missions can generate a high amount of visual and sensor data, but this information still needs to be reviewed, interpreted, and integrated into maintenance workflows. If the analysis process is slow or unclear, the practical value of the inspection becomes limited. Many users also face difficulty in finding skilled operators and teams who can manage both flight execution and inspection reporting effectively.

Key Market Segment

By Type

- Fixed-Wing Drones

- Multi-Rotor Drones

By Range

- Visual Line of Sight (VLOS)

- Beyond Visual Line of Sight (BVLOS)

By Application

- Military Reconnaissance

- Infrastructure Inspection

- Environmental Monitoring

- Public Safety

- Others

By End-User

- Defense & Security

- Agriculture

- Construction

- Energy & Utilities

- Government

- Others

Competetive Analysis

The competitive landscape of the Reconnaissance and Inspection Drones Market includes a mix of defense contractors and commercial drone manufacturers. Companies such as Lockheed Martin, AeroVironment, Insitu (Boeing), Elbit Systems, and Israel Aerospace Industries focus on military-grade drones designed for surveillance, intelligence gathering, and defense operations.

These players emphasize advanced imaging systems, long endurance, and secure communication capabilities. Their strong experience in defense and aerospace allows them to deliver high-performance solutions for critical missions. At the same time, companies like Teledyne FLIR provide specialized sensor technologies that enhance drone capabilities for both defense and industrial use.

On the commercial side, companies such as DJI, Parrot, Skydio, Autel Robotics, Yuneec, senseFly, PrecisionHawk, Delair, and Microdrones focus on inspection and mapping applications across industries like energy, agriculture, and infrastructure. These players offer user-friendly drones with features such as autonomous flight, real-time data capture, and AI-based analytics. Competition in this market is driven by innovation in flight automation, imaging technology, and data processing, as companies aim to deliver efficient and reliable solutions for both defense and commercial applications.

Recent Development

- March, 2026 – Insitu ScanEagle upgrades MX-20HD thermal camera for maritime patrol. 24-hour endurance and 100km range with automated ship detection. US Navy contracts expand Blue sUAS compliance.

- February, 2026 – FLIR SIRAS thermal drone adds 640×512 radiometric sensor. Public safety inspections and 55-minute flight time. NDAA-compliant for government use.

Conclusion

The Reconnaissance & Inspection Drones Market is expected to remain an important part of the broader drone industry as demand continues to rise across defense, public safety, infrastructure, energy, agriculture, and industrial inspection. Growth in this market is mainly supported by the need for faster monitoring, better image quality, lower human risk, and improved access to hard to reach or hazardous locations. Advances in sensors, cameras, AI-based analytics, and autonomous flight are also making these drones more useful for both routine inspection and critical surveillance tasks.

At the same time, the market is likely to benefit from wider commercial adoption as organizations look for cost-efficient and accurate ways to collect real-time data. Even though regulatory issues, privacy concerns, and high operating complexity may remain key challenges, the overall outlook for the market stays positive due to its strong practical value across many end-use sectors.