Table of Contents

Introduction

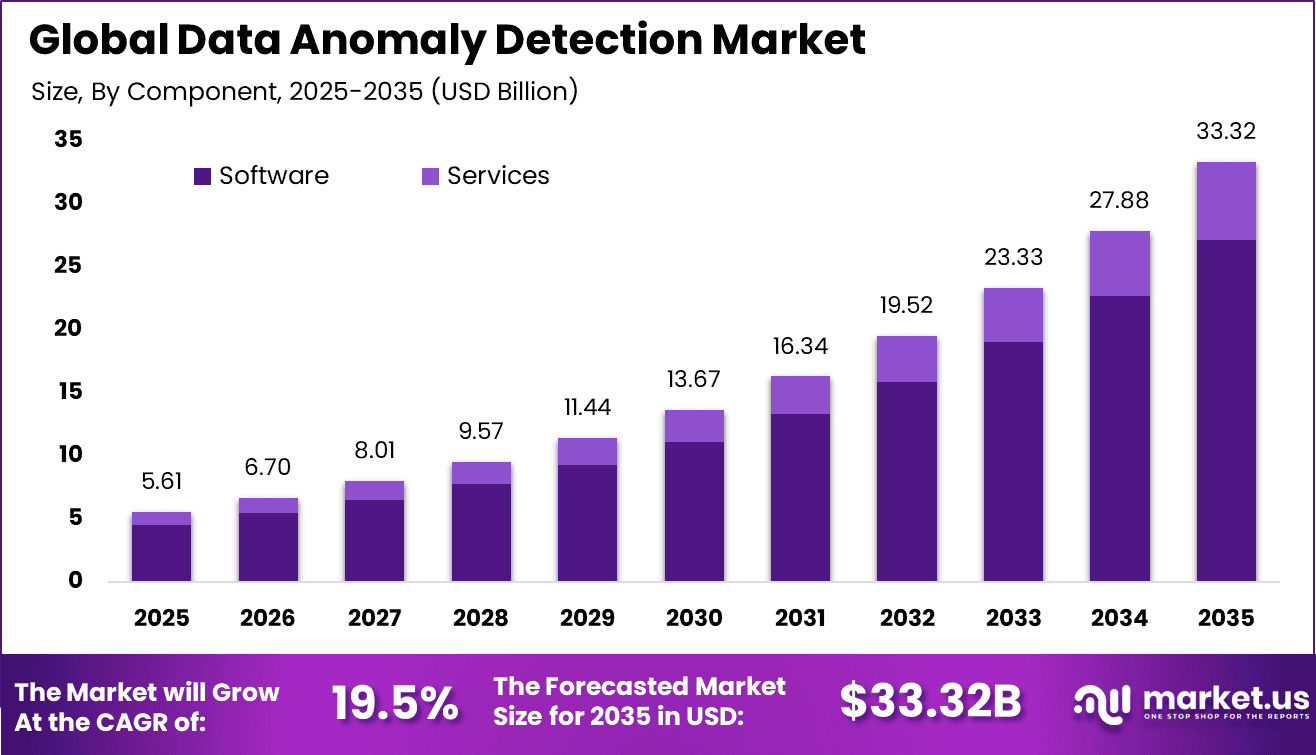

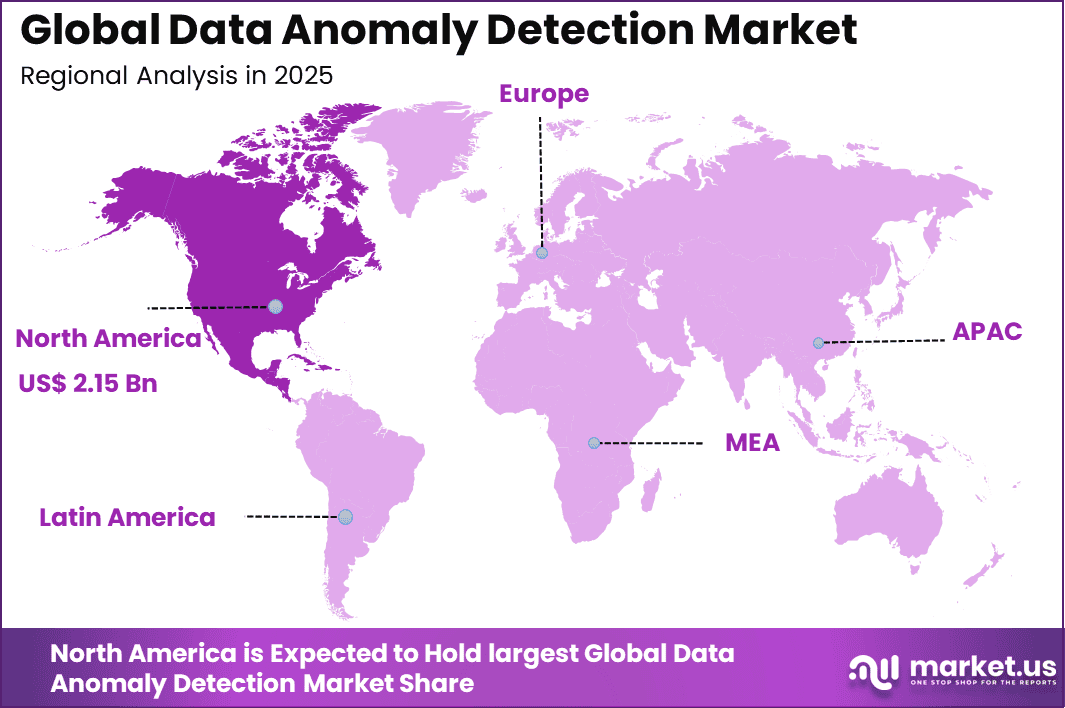

The Global Data Anomaly Detection Market size is expected to be worth around USD 33.32 billion by 2035, from USD 5.61 billion in 2025, growing at a CAGR of 19.5% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 38.5% share, holding USD 2.15 billion in revenue.

The anomaly detection market refers to a set of advanced analytical systems designed to identify unusual patterns, deviations, or irregular behavior across datasets, systems, and operational environments. These solutions are widely used in cybersecurity, financial monitoring, industrial systems, and data management processes. The growing volume of digital data and the increasing complexity of IT infrastructure have made manual monitoring inefficient, which has strengthened the role of automated anomaly detection.

Top driving factors for this market are closely linked to the rapid expansion of cyber threats and the need for continuous monitoring. Organizations are dealing with more sophisticated attack techniques and internal vulnerabilities, which require intelligent systems capable of identifying unknown threats. The increasing adoption of cloud platforms, digital transactions, and connected devices has significantly expanded the volume and speed of data generation.

One of the key driving factors is the rising need for data security and fraud prevention across industries. Financial institutions, e commerce platforms, and digital services are under constant risk from unauthorized activities, making early detection of anomalies essential. At the same time, organizations are focusing on improving operational efficiency, and anomaly detection helps identify system failures or process inefficiencies before they escalate.

The growing adoption of advanced analytics and machine learning is also supporting this market, as these technologies can detect complex patterns that are not visible through traditional methods. In addition, regulatory requirements around data integrity and reporting are encouraging companies to implement stronger monitoring systems. Demand for data anomaly detection solutions is increasing as organizations seek more accurate and timely insights from their data. Businesses are looking for systems that can integrate with existing data platforms and provide real time alerts without requiring extensive manual intervention.

Key Takeaway

- On-premise deployment captures 55%, ensuring data sovereignty, low-latency processing, and seamless integration with legacy systems in regulated environments.

- Big data analytics technology dominates at 41%, enabling scalable pattern recognition, behavioral baselining, and correlation across petabyte-scale transaction volumes.

- BFSI end-use holds 26.2%, powering transaction monitoring, anti-money laundering detection, and credit risk assessment through continuous anomaly surveillance.

- North America drives 31.1% global value, with U.S. market at USD 2.3 billion and 16.2% CAGR, fueled by regulatory compliance mandates and financial sector digitalization.

How AI is Reshaping the Future of this market?

Artificial Intelligence is reshaping the anomaly detection market by moving it from rule-based monitoring to intelligent, self-learning systems. Earlier approaches depended on fixed thresholds and manual analysis, which often failed to capture complex or evolving patterns. AI-driven models learn from historical and real-time data, allowing them to understand what normal looks like and quickly detect deviations. This shift has improved accuracy and reduced false alerts, making anomaly detection more reliable and practical for modern digital environments.

A major transformation is the ability to perform real-time and predictive detection. AI continuously analyzes streaming data across systems such as networks, financial platforms, and connected devices. Instead of reacting after an issue occurs, these systems can identify early warning signals and help prevent incidents like fraud, downtime, or cyber threats. This proactive capability is becoming critical for organizations that depend on uninterrupted operations and fast decision-making.

AI is also enabling automation and scalability in anomaly detection. Modern systems can process large volumes of structured and unstructured data without human intervention. This is especially important as data generation continues to grow across industries. AI helps automate tasks such as alert generation, pattern recognition, and root cause analysis, which reduces operational burden and improves response speed. As a result, organizations can manage complex environments more efficiently with fewer resources.

Another key impact is the use of advanced learning techniques that can detect subtle and complex anomalies. These systems improve over time as they are exposed to more data, allowing them to identify hidden risks that traditional systems often miss. This is particularly valuable in detecting sophisticated cyber threats, insider activities, and operational inefficiencies that do not follow obvious patterns.

AI is also expanding the role of anomaly detection beyond security into broader business applications. It is being used in areas such as predictive maintenance, healthcare monitoring, financial risk management, and smart manufacturing. This shift is turning anomaly detection into a strategic tool for improving performance, reducing costs, and supporting data-driven decisions across industries.

Regional Analysis

In 2025, North America held a dominant Market position, capturing more than a 31.1% share, holding USD 2.15 Billion revenue. This leadership is driven by the early adoption of advanced analytics and artificial intelligence across industries such as banking, healthcare, and cybersecurity. Organizations in the US and Canada are actively investing in real-time monitoring systems to detect fraud, network intrusions, and operational anomalies. The strong presence of cloud infrastructure and mature IT ecosystems further supports rapid deployment of anomaly detection solutions.

Another key factor behind North America’s leadership is the strict regulatory environment around data protection and risk management. Enterprises are required to maintain high standards of data integrity and compliance, which increases the demand for intelligent detection tools. Additionally, the region benefits from a highly skilled workforce and strong collaboration between technology providers and enterprises, enabling continuous innovation and faster implementation of advanced detection models.

Europe is expected to maintain steady growth in the data anomaly detection market due to increasing focus on data privacy and compliance requirements. Regulations such as GDPR are pushing organizations to adopt more transparent and secure data monitoring practices. Industries such as finance, manufacturing, and telecommunications are actively deploying anomaly detection systems to improve operational efficiency and prevent data breaches.

The Asia Pacific region is projected to witness significant growth driven by rapid digital transformation and increasing internet penetration. Countries such as China, India, and Japan are investing in smart technologies, digital payments, and e-commerce platforms, which generate large volumes of data. This creates a strong need for anomaly detection systems to ensure data accuracy and security across expanding digital ecosystems.

Latin America is anticipated to experience gradual growth as organizations increasingly adopt digital solutions and cloud-based platforms. Businesses in sectors such as banking and retail are beginning to recognize the importance of detecting fraudulent activities and operational inefficiencies. Government initiatives aimed at digitalization are also contributing to the growing demand for anomaly detection technologies in the region.

The Middle East and Africa region is expected to show emerging growth potential due to increasing investments in digital infrastructure and smart city projects. Countries in the Middle East are focusing on strengthening cybersecurity frameworks, while African nations are gradually adopting data-driven technologies. As awareness around data security and analytics continues to rise, the demand for anomaly detection solutions is projected to expand steadily across the region.

Driver

The growing need to detect unusual behavior in real time is a major driver for the anomaly detection market. As digital systems expand across enterprises, organizations are dealing with more complex data flows and operational risks. This is increasing the importance of identifying abnormal patterns early to prevent disruptions, fraud, or security breaches.

At the same time, businesses are focusing more on automation and data-driven decision making. Anomaly detection helps in monitoring systems continuously without manual intervention, which improves efficiency and reduces the chances of missing critical events. This is supporting its wider adoption across multiple industries.

Restraint

One of the key restraints is the difficulty in achieving accurate results without generating too many false alerts. Many systems struggle to differentiate between normal variations and actual anomalies, which can lead to unnecessary investigations and reduced confidence in the system.

Another limiting factor is the challenge of integrating anomaly detection solutions with existing infrastructure. Organizations with older systems often face compatibility issues, which increases implementation time and requires additional technical effort. This slows down adoption in many cases.

Opportunity

The increasing use of artificial intelligence and machine learning is creating strong opportunities in the anomaly detection market. These technologies allow systems to learn from data patterns and improve detection accuracy over time, making them more effective in identifying unknown or evolving anomalies.

In addition, the expansion of digital ecosystems such as connected devices and cloud platforms is generating large volumes of real-time data. This creates new use cases for anomaly detection in areas like predictive maintenance, fraud prevention, and system optimization, supporting future growth.

Challenge

A major challenge in this market is the shortage of skilled professionals who can design and manage advanced anomaly detection systems. Many organizations lack the expertise needed to build and maintain these models, which limits their ability to fully benefit from the technology.

Another challenge is handling diverse and dynamic data environments. Anomalies differ across industries and applications, making it difficult to create models that perform consistently. Continuous tuning and updates are required, which adds to operational complexity.

Key Market Segment

By Component

- Solution

- Network Behavior Anomaly Detection

- User Behavior Anomaly Detection

- Services

- Professional Services

- Managed Services

By Deployment

- Cloud

- On-Premise

By Technology

- Machine Learning & Artificial Intelligence

- Big Data Analytics

- Business Intelligence & Data Mining

By End-use Outlook

- BFSI

- Retail

- IT & Telecom

- Healthcare

- Manufacturing

- Government & Defense

- Others

Competetive Analysis

The Anomaly Detection Market is led by major cloud and enterprise technology providers offering scalable AI-driven monitoring solutions. Amazon Web Services, Inc., Microsoft Corporation, and International Business Machines Corporation provide advanced analytics platforms for real-time anomaly detection. Cisco Systems, Inc. and Dell Technologies, Inc. strengthen infrastructure and security capabilities. These companies focus on automation and AI integration. Their solutions enhance operational visibility. This supports faster detection of irregular patterns across systems.

Analytics and monitoring-focused firms play a critical role in delivering specialized anomaly detection capabilities. Splunk, Inc., Dynatrace, LLC, and SAS Institute, Inc. offer advanced data analytics and observability tools. Broadcom, Inc. and Trend Micro, Inc. enhance security-focused anomaly detection. LogRhythm, Inc. supports threat detection and response. These solutions improve accuracy and reduce response time.

Emerging and niche players contribute to innovation in AI-based anomaly detection and managed services. Anodot Ltd., GURUCUL, and Happiest Minds focus on machine learning-driven insights. Hewlett Packard Enterprise Company provides enterprise-grade data platforms. These companies support predictive analytics and automation. Their role is expanding with increasing data complexity. This competitive landscape drives continuous innovation in anomaly detection technologies.

Recent Development

- IBM Instana Observability used agentless anomaly detection for hybrid clouds. AIOps correlates 10,000 dependencies automatically. Enterprises prevented 80% of outages proactively.

Conclusion

The anomaly detection market is expected to remain an important part of modern digital operations as businesses focus more on preventing risks, reducing downtime, and improving decision making. Demand is rising across industries because organizations need faster ways to identify unusual patterns in data, systems, transactions, and user behavior.

The market is also benefiting from the wider use of cloud platforms, connected devices, and artificial intelligence tools that support more accurate and real-time monitoring. At the same time, challenges such as data complexity, false alerts, and integration issues are encouraging providers to improve solution performance and usability. Overall, the market outlook remains positive, supported by the growing need for security, operational efficiency, and better control over business processes.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)