Table of Contents

Introduction

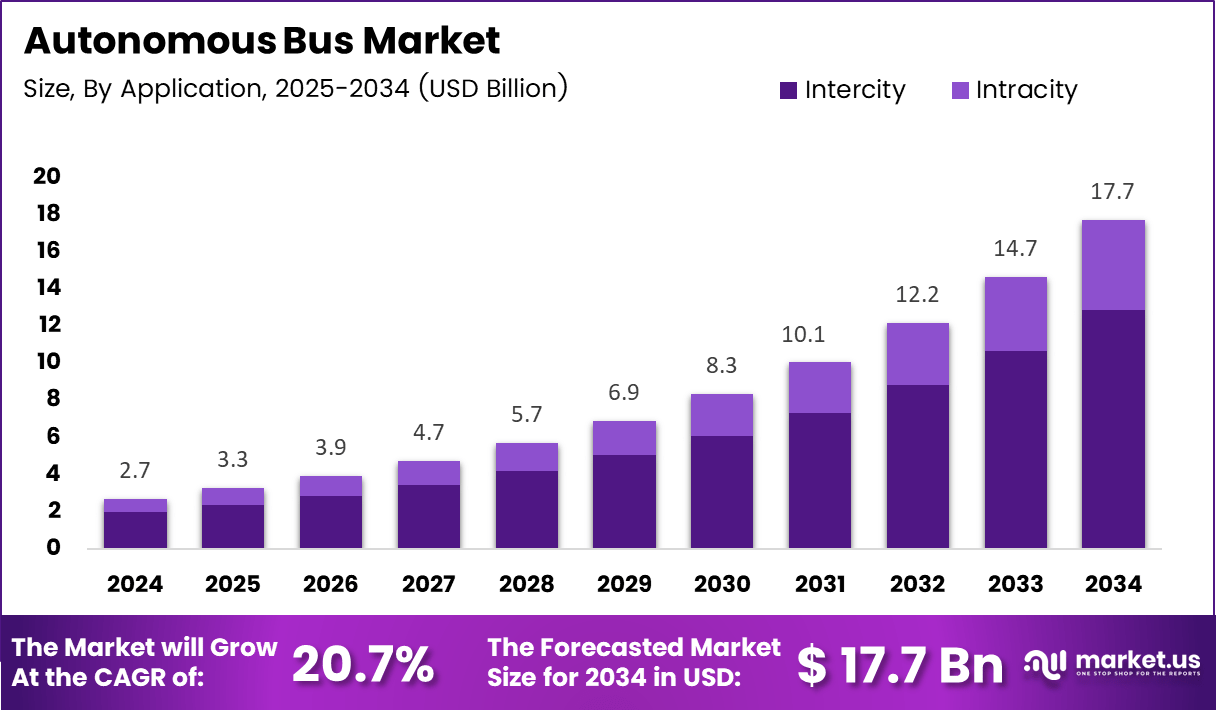

Market.us has released a comprehensive analysis of the Global Autonomous Bus Market, projecting robust expansion from USD 2.7 Billion in 2024 to USD 17.7 Billion by 2034. The market is forecast to grow at a CAGR of 20.7% over the 2025–2034 period, reflecting accelerating global demand for self-driving public transport solutions that enhance efficiency, sustainability, and route optimization.

Consequently, governments across major economies are investing in cleaner fleets and modernized transit systems, with cities exploring autonomous transit corridors to reduce congestion and improve urban accessibility. Regulatory agencies are gradually refining safety frameworks to support controlled deployments, enabling early-stage commercial services across campuses, smart districts, and dedicated urban routes.

Furthermore, transit operators are increasingly attracted by the long-term cost advantages of autonomous bus platforms. Research indicates that autonomous bus services can reduce travel costs by 6%–11%, improving economic viability for public transit agencies while delivering 24/7 on-demand service availability without the operational constraints of driver fatigue or shift-based scheduling.

Additionally, electric autonomous buses are accelerating investment as countries prioritize low-emission mobility. Governments support zero-emission fleet initiatives through financial incentives, and manufacturers are developing energy-optimized designs with remote monitoring tools that maximize vehicle uptime across structured urban deployment environments.

Finally, passenger acceptance is strengthening market confidence. According to a survey of 576 ride-experienced users, in-vehicle safety, service quality, and riding habits positively influenced continued willingness to use autonomous bus services, indicating growing public trust in vehicle automation and encouraging deeper investment in human-centric safety and ride-experience features.

Key Takeaways

- The Global Autonomous Bus Market is projected to grow from USD 2.7 Billion in 2024 to USD 17.7 Billion by 2034 at a CAGR of 20.7%.

- Level 2 autonomy leads the segment with a 38.3% share in 2024.

- Electric fuel type dominates with a 52.9% share in 2024.

- Intracity applications hold the largest share at 72.8% in 2024.

- North America leads regionally with a 38.8% share valued at USD 1.0 Billion.

Market Segmentation Overview

By autonomy, Level 2 dominates with a 38.3% share as cities adopt partial automation for controlled routes, reducing driver workload while maintaining regulatory compliance. Level 3 and Level 4 systems are gaining traction through government-backed pilot programs on dedicated lanes and campus environments, while Level 1 continues supporting transitional adoption in regions gradually shifting toward automated public transit.

By fuel type, Electric leads with a commanding 52.9% share, driven by sustainability mandates and rapid charging infrastructure improvements. Hybrid systems serve operators transitioning between fuel types, while Diesel maintains relevance in regions where charging infrastructure remains limited. By application, Intracity dominates with 72.8%, reflecting strong demand for last-mile connectivity, short-route automation, and smart-city-integrated shuttle deployments across dense urban environments.

Drivers

Growing deployment of autonomous transit pilots across smart city corridors is a primary market driver. Cities are testing small driverless fleets to evaluate real-world performance, reduce congestion, and build regulatory confidence. Rising investment in AI-based perception systems simultaneously improves object detection, lane recognition, and pedestrian monitoring, reducing human error and supporting long-term adoption in structured traffic environments.

Expansion of electric autonomous bus fleets provides an equally powerful growth catalyst. Transport authorities selecting electric, self-driving buses achieve lower operating costs, meet national emission-reduction targets, and benefit from government incentive programs supporting zero-emission fleet transitions. Growing demand for continuous, schedule-independent public transportation further strengthens the case for autonomous platforms capable of operating without the constraints of driver availability.

Use Cases

Intracity last-mile and shuttle connectivity represents the most commercially active use case. Cities are deploying autonomous shuttles to bridge gaps between transit hubs, residential zones, and employment centers, improving multimodal journey continuity. High passenger demand, predictable short-route patterns, and smart-city infrastructure investment create ideal conditions for autonomous bus deployment within dense urban networks.

Campus and corporate facility transportation is a fast-growing controlled-environment application. Universities, technology parks, and airports are introducing fully autonomous shuttles for short-distance mobility, leveraging these structured settings to simplify regulatory compliance and gather real-world performance data. These early deployments act as commercial testbeds, accelerating system maturity and building the operational evidence base needed for broader public transit adoption.

Major Challenges

Limited urban infrastructure readiness remains the most critical restraint. Many cities lack connected traffic management systems, high-definition mapping coverage, or dedicated autonomous lanes necessary for reliable mixed-traffic navigation. These infrastructure gaps reduce operational predictability and hinder seamless route execution, slowing the transition from controlled pilot programs to full-scale commercial deployments across broader urban networks.

High upfront procurement costs and fragmented regulatory frameworks compound the challenge. Autonomous bus platforms require expensive sensor arrays, redundant control systems, and extensive safety validation, increasing financial pressure on transit agencies evaluating long-term investment viability. Inconsistent approval processes and safety norms across jurisdictions simultaneously delay cross-border rollouts and create compliance uncertainty that discourages early-stage operators from committing to large-scale fleet purchases.

Business Opportunities

Vehicle-to-everything communication integration presents a compelling commercial opportunity. As autonomous buses connect with traffic signals, road infrastructure, and other vehicles, route efficiency improves, collision risks decrease, and coordinated traffic movement becomes achievable across busy urban corridors. Vendors developing V2X-compatible autonomous platforms are positioned to capture premium contracts from smart-city programs prioritizing interconnected, intelligent transportation ecosystems.

Campus and private-facility deployments offer a parallel near-term revenue opportunity. These controlled environments simplify regulatory requirements and enable vendors to demonstrate commercial readiness with lower deployment risk. Institutions gain improved internal mobility while operators accumulate critical real-world performance data that accelerates product refinement and builds the credibility needed to win competitive public transit tenders in broader urban markets.

Regional Analysis

North America leads the global market with a 38.8% share valued at USD 1.0 Billion, driven by strong federal mobility funding, large-scale autonomous pilot programs, and rapid smart infrastructure deployment across the United States. Universities, airports, and technology-driven cities are actively deploying autonomous shuttles, supported by advanced R&D ecosystems and progressively supportive state-level regulatory frameworks.

Europe demonstrates strong momentum as countries expand low-emission zones and invest in autonomous public transport corridors, with Nordic and Western European cities leading large-scale trials. Asia Pacific is growing rapidly, fueled by megacity expansion, large public transport networks, and government-backed autonomous mobility pilots across universities, airports, and business districts in East and Southeast Asia. Middle East & Africa and Latin America are advancing gradually as smart-city programs, controlled-route deployments, and urban congestion pressures strengthen long-term regional market potential.

Recent Developments

- In May 2024, Volvo Autonomous Solutions unveiled Volvo’s first production-ready autonomous truck, the Volvo VNL Autonomous, at ACT Expo in Las Vegas, combining Volvo’s commercial vehicle expertise with Aurora Innovation’s autonomous driving technology to increase freight capacity across the United States.

- In January 2025, May Mobility entered a partnership with Italian minibus manufacturer Tecnobus, announced at CES 2025, introducing a new autonomous minibus platform based on the Gulliver model and expanding May Mobility’s autonomous vehicle use cases across multiple markets.

Conclusion

The Global Autonomous Bus Market is entering a sustained high-growth phase anchored by urban electrification mandates, advancing AI perception technologies, and expanding government support for smart public transportation networks. With the market forecast to grow from USD 2.7 Billion in 2024 to USD 17.7 Billion by 2034 at a CAGR of 20.7%, stakeholders across automotive, transit, and smart-city sectors face significant opportunities to shape the future of automated public mobility.

As V2X communication matures, sensor-fusion architectures advance, and passenger confidence deepens, autonomous buses are positioned to transition from controlled pilot programs to mainstream urban transit networks. Organizations that invest decisively in scalable platforms, regulatory alignment, and infrastructure partnerships today will define the competitive landscape of global autonomous public transportation through the decade ahead.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)