Table of Contents

Overview

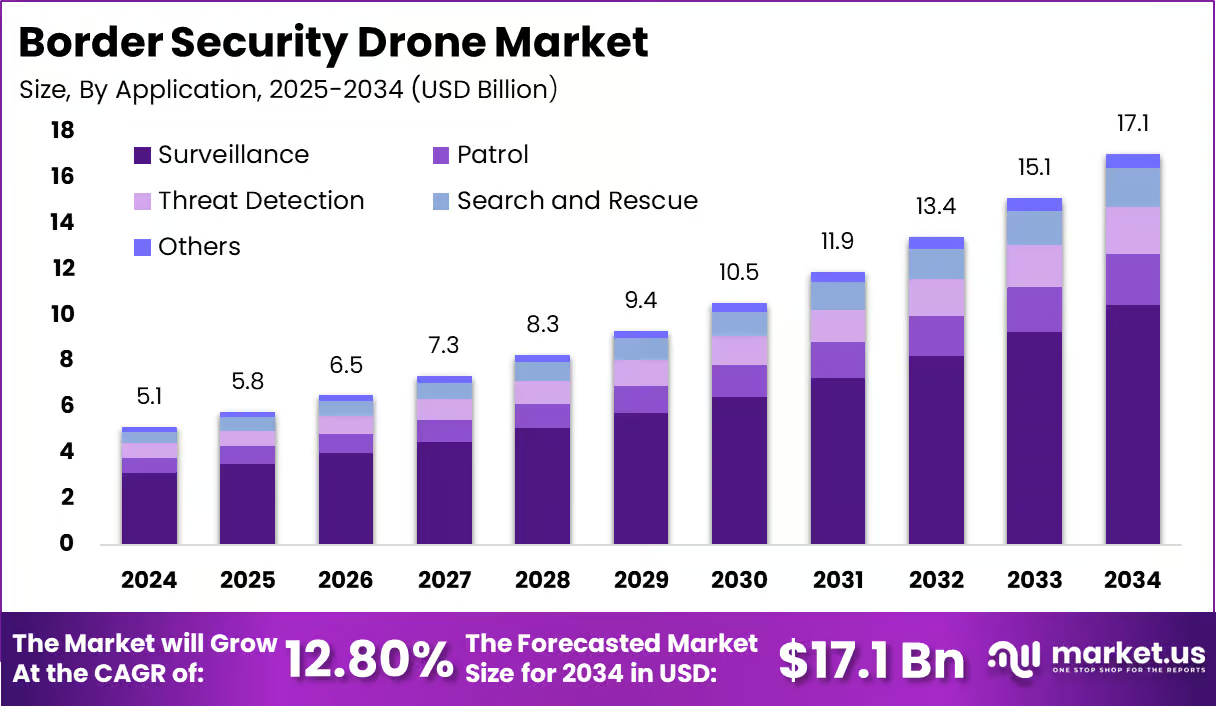

This report provides strategic value for organizations evaluating investments in defense technology, unmanned aerial systems, and border monitoring infrastructure. Based on the figures provided, the Border Security Drone Market is valued at USD 5.12 billion in 2024 and is projected to reach USD 17.1 billion by 2034, expanding at a CAGR of 12.80%.

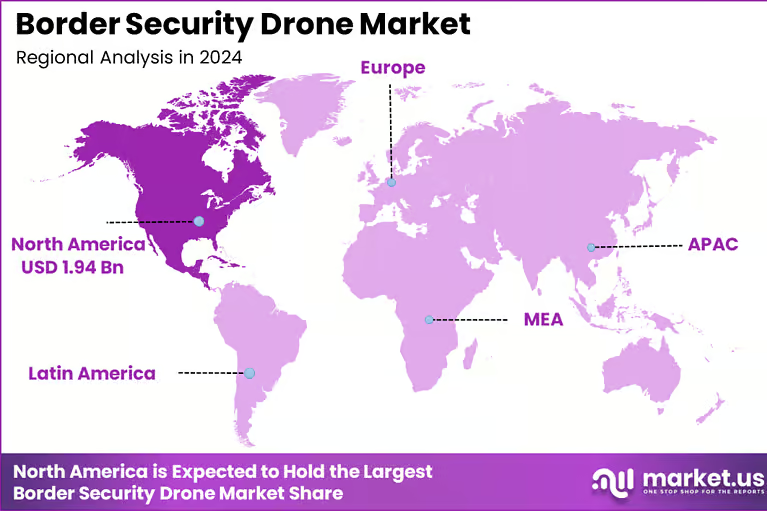

For clients operating in defense, aerospace, security technology, or government contracting, this reflects a steadily expanding opportunity driven by growing geopolitical tensions and increasing border surveillance requirements. North America leads the market with a 38% share, equivalent to USD 1.94 billion in 2024, supported by strong defense budgets and large-scale border modernization initiatives.

Within the region, the US accounts for USD 1.75 billion in 2024 and is expected to reach USD 4.79 billion by 2034, highlighting significant adoption by federal border protection agencies. By type, fixed-wing drones dominate with 59.7% share due to their long endurance and wide-area coverage.

Surveillance remains the leading application with 61.3% share, reflecting the need for persistent monitoring across remote border zones. Thermal imaging holds 38.6% share, enabling night-time and low-visibility operations, while military end-users lead deployment with 57.4%, demonstrating the critical role of drones in defense-led border protection strategies.

Statistics

Operational data from government agencies and defense organizations highlights the growing importance of unmanned aerial systems in border security missions. According to the US Customs and Border Protection agency, its unmanned aircraft systems program has logged more than 150,000 flight hours since deployment began, supporting surveillance along US land and maritime borders. The agency operates MQ-9 Predator B drones capable of flying above 40,000 feet with endurance exceeding 27 hours, allowing persistent border monitoring over large territories.

The US Department of Homeland Security has also reported that drones significantly enhance border surveillance coverage, particularly in remote areas where traditional patrols are difficult. NATO has expanded its Alliance Ground Surveillance program using high-altitude drones designed to provide real-time intelligence across wide operational zones.

Additionally, the US Department of Defense states that unmanned systems now account for thousands of reconnaissance missions annually, demonstrating their growing operational role in defense and border protection activities. These developments confirm that governments are increasingly relying on drone-based intelligence systems to strengthen national security, improve situational awareness, and respond quickly to cross-border threats.

Effective Takeaways

- The market shows stable long-term expansion, projected to grow from USD 5.12 billion in 2024 to USD 17.1 billion by 2034 based on the figures provided.

- North America remains the most commercially important region due to high defense spending and active border modernization initiatives.

- The US market continues to lead adoption with strong investments from federal border protection and homeland security agencies.

- Fixed-wing drones dominate deployments because of their longer endurance and ability to monitor large border territories.

- Surveillance remains the most critical operational application, highlighting the demand for continuous border intelligence and monitoring.

- Military agencies remain the primary buyers, indicating that defense procurement programs will continue to shape the market’s growth trajectory.

- This report offers valuable insights into technology trends, regional opportunities, and procurement drivers that can guide strategic investments and competitive positioning in the border security drone ecosystem

Emerging Trends Analysis

A key emerging trend in the Border Security Drone Market is the growing integration of AI-enabled analytics, autonomous navigation, and multi-sensor payload systems to improve border monitoring efficiency. Modern border drones increasingly combine electro-optical cameras, thermal imaging, radar, and AI-based object detection to track movements across large and remote areas.

Fixed-wing drones, which hold 59.7% share by type, are especially suited for long-range border patrol due to their endurance and ability to cover wide territories. Governments are also investing in drone fleets capable of operating in coordinated swarms and integrated command systems that provide real-time intelligence to border control authorities. These developments allow border agencies to detect suspicious activities faster while reducing operational costs associated with traditional manned patrols.

Key Market Segments

Type

- Fixed-Wing Drones

- Multi-Rotor Drones

Application

- Surveillance

- Patrol

- Threat Detection

- Search and Rescue

- Others

Technology

- Thermal Imaging

- Radar

- LiDAR

- AI & Analytics

- Others

End-User

- Military

- Homeland Security

- Coast Guard

- Law Enforcement

Driver Analysis

The primary driver of the market is the rise in geopolitical tensions, cross-border security threats, and illegal activities such as smuggling, trafficking, and unauthorized migration. Governments are increasing investments in aerial surveillance technologies that provide persistent monitoring across difficult terrains, including deserts, mountains, and maritime borders.

This demand explains why surveillance applications account for 61.3% of the market and why military end-users dominate with a 57.4% share. Drones enable authorities to monitor large border areas continuously while minimizing the risks faced by personnel. With border modernization initiatives expanding across several countries, drones are becoming essential tools for intelligence gathering, reconnaissance missions, and early threat detection, strengthening their role in national security strategies.

Restraint Analysis

Despite strong adoption, regulatory restrictions and operational limitations remain key restraints in the border security drone market. Airspace regulations, privacy concerns, and strict government procurement processes can delay drone deployment programs. Border drones often operate near civilian airspace or populated areas, requiring compliance with complex aviation rules and safety frameworks.

In addition, integrating drones with existing border monitoring infrastructure such as radar systems, communication networks, and command centers can involve high technical complexity and implementation costs. These factors may slow the pace of deployment, particularly in regions where regulatory frameworks for unmanned aerial systems are still evolving.

Opportunity Analysis

A significant opportunity lies in expanding the role of border drones in integrated surveillance networks that combine satellite monitoring, ground sensors, and autonomous aerial platforms. As governments modernize border infrastructure, there is growing interest in deploying drones that can operate continuously and relay intelligence to centralized control systems.

Thermal imaging technology, which currently holds 38.6% share, is expected to gain further traction as agencies seek improved night-time and low-visibility surveillance capabilities. In addition, the development of long-endurance drones capable of operating for extended periods offers new opportunities for border agencies to monitor remote areas more efficiently, improving response times and situational awareness.

Challenge Analysis

One of the major challenges facing the market is the risk of counter-drone threats and electronic warfare that can disrupt drone operations in sensitive border regions. Drones operating near contested areas may face signal interference, GPS spoofing, or cyber intrusions that compromise mission reliability. Ensuring secure communication links, resilient navigation systems, and anti-jamming technologies is therefore critical for border security operations.

At the same time, agencies must balance technological sophistication with operational costs and maintenance requirements. Managing large drone fleets, ensuring operator training, and maintaining high mission reliability across harsh environmental conditions remain ongoing operational challenges.

Regional Analysis

North America dominates the Border Security Drone Market with a 38% share and a market value of USD 1.94 billion in 2024. The region benefits from strong defense budgets, advanced drone technology development, and large-scale border monitoring programs.

The United States is the leading contributor, accounting for USD 1.75 billion in 2024 and projected to reach USD 4.79 billion by 2034 at a CAGR of 10.6%. Federal border protection agencies increasingly deploy drones for surveillance, reconnaissance, and rapid response missions along extensive land and maritime borders. Continuous investments in border modernization initiatives and unmanned aerial systems integration further strengthen North America’s leadership in this market.

Competitive Analysis

The competitive landscape of the Border Security Drone Market is shaped by defense contractors and aerospace companies specializing in unmanned aerial systems. Companies such as Northrop Grumman, General Atomics Aeronautical Systems, Lockheed Martin, AeroVironment, and Elbit Systems play a major role in developing advanced surveillance drones for defense and border security applications.

These companies focus on improving endurance, sensor integration, and real-time intelligence capabilities to meet evolving security requirements. Strategic partnerships with government agencies, defense departments, and border control authorities remain central to market expansion. Vendors are also investing in AI-enabled analytics and advanced imaging technologies to strengthen their drone platforms’ operational capabilities.

Top Key Players in the Market

- Israel Aerospace Industries

- Elbit Systems

- Lockheed Martin

- Northrop Grumman

- Boeing

- Teledyne FLIR

- Skydio

- Autel Robotics

- SenseFly

- PrecisionHawk

- Thales

- BAE Systems

- Others

Conclusion

The Border Security Drone Market presents strong growth potential as governments worldwide prioritize advanced surveillance technologies to protect national borders. With the market projected to grow from USD 5.12 billion in 2024 to USD 17.1 billion by 2034, drones are becoming essential tools for intelligence gathering, reconnaissance, and continuous border monitoring.

Fixed-wing drones, surveillance applications, and thermal imaging technologies currently dominate market adoption, reflecting the need for long-range and all-weather monitoring capabilities. North America and the United States remain the key markets due to large defense budgets and ongoing border modernization initiatives. For stakeholders, this market offers significant opportunities in advanced drone systems, sensor technologies, and integrated border surveillance solutions.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)