Table of Contents

Overview

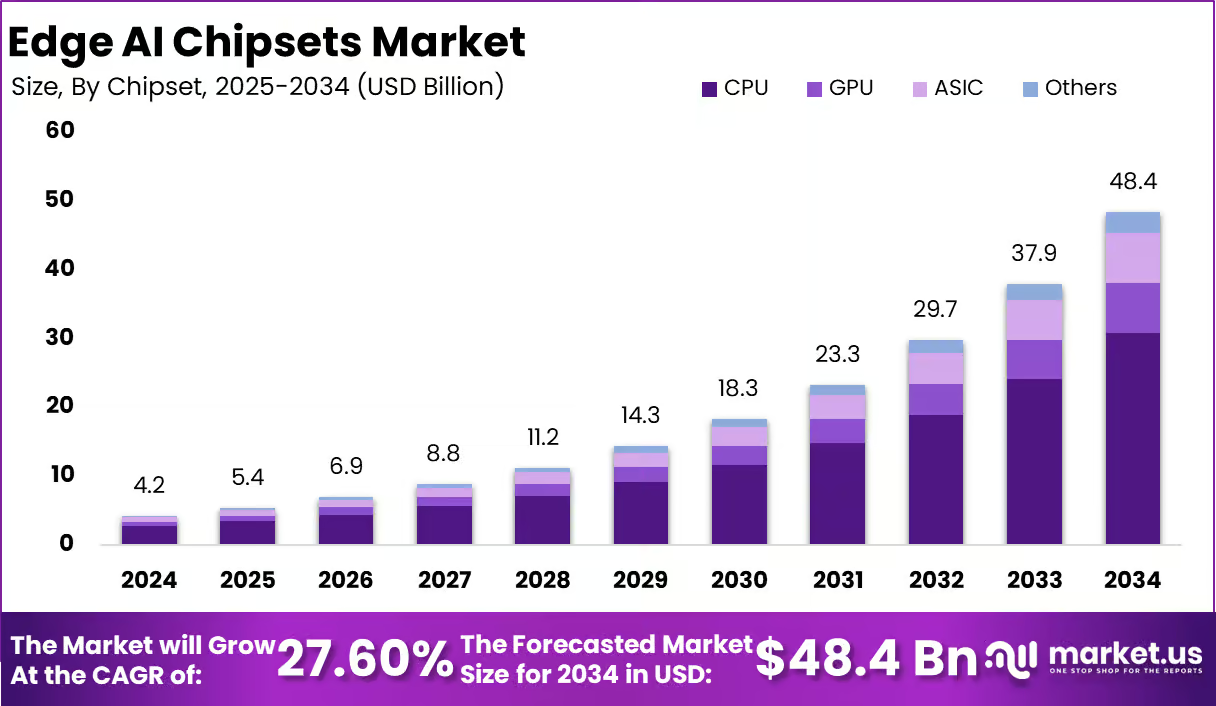

This market offers strong strategic value because it sits at the intersection of artificial intelligence, semiconductor innovation, and real-time device intelligence. Based on the figures provided, the global Edge AI Chipsets market was valued at USD 4.23 billion in 2024 and is projected to reach USD 48.4 billion by 2034, advancing at a CAGR of 27.6%.

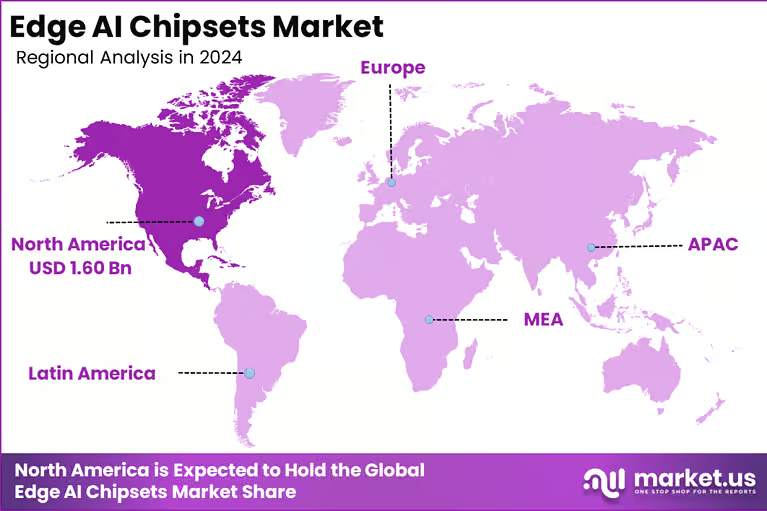

For clients assessing growth opportunities in semiconductors, embedded systems, consumer electronics, and intelligent devices, this reflects a high-potential market moving from performance enhancement to core system enablement. North America held 38% of the market in 2024, equivalent to USD 1.60 billion, supported by strong uptake of AI-enabled IoT, robotics, and autonomous systems.

The US alone contributed USD 1.45 billion and is expected to reach USD 13.29 billion by 2034, reinforcing its role as the leading commercialization center. By chipset, CPUs accounted for 63.7%, reflecting their broad deployment in inference execution, local processing, and system coordination at the edge.

Function, training held 68.3%, showing rising demand for adaptive, on-device learning. By device, consumer devices dominated with 84.2%, driven by the rapid integration of edge AI into smartphones, wearables, smart home products, and personal digital assistants.

Statistics

The business case for edge AI chipsets is supported by real device and infrastructure trends across computing and consumer electronics. IDC reported that global PC shipments reached 262.7 million units in 2024, up 1% year over year, showing that the installed hardware base for AI-capable edge processing continues to expand.

Reuters, citing Companies, reported that AI-enabled PCs accounted for 14% of global PC shipments in the second quarter of 2024, highlighting the growing role of processors designed to run AI tasks locally rather than in the cloud.

Companies reported that AI-enabled PCs accounted for 14% of global PC shipments in the second quaCanalys, reported that AI-enabled PCs accounted for 14% of global PC shipments in NVIDIA states that its Jetson Nano platform delivers 472 GFLOPs for AI workloads at just 5 to 10 watts, which reflects the performance-per-watt advantage that is accelerating edge AI deployment in compact systems.

NVIDIA also says its Jetson AGX Thor developer kit delivers up to 2,070 FP4 TFLOPS and offers up to 7.5 times higher AI compute and 3.5 times better energy efficiency than Jetson AGX Orin, showing how fast edge AI hardware capability is advancing. On the consumer side, IDC projected that personal computing devices, including PCs and tablets, would reach 403.5 million units in 2024, while public reporting on AI smartphones and AI PCs indicates rising demand for devices with dedicated on-device AI processing.

Effective Takeaways

- The market is moving from niche embedded intelligence to mainstream device integration, supported by strong projected growth from USD 4.23 billion in 2024 to USD 48.4 billion by 2034, based on the figures provided.

- North America and especially the US should remain the priority region for commercial focus because of strong AI-IoT adoption, mature semiconductor ecosystems, and high-value autonomous system deployment.

- CPUs remain commercially important because they continue to anchor edge data processing, model execution, and system management across multiple device categories.

- The high 68.3% share for training indicates that adaptive, on-device learning is becoming a serious differentiator, especially for privacy-sensitive and low-latency use cases.

- Consumer devices represent the largest monetization pool, with 84.2% share, making smartphones, wearables, smart home systems, and personal assistants the most immediate volume drivers.

- This report is worth purchasing because it helps connect semiconductor demand with real deployment trends across consumer electronics, edge computing infrastructure, and AI-enabled endpoint devices.

Emerging Trends Analysis

A major emerging trend in the Edge AI Chipsets market is the shift from cloud-dependent AI processing to on-device intelligence across consumer and embedded systems. This trend is closely aligned with your data, where consumer devices account for 84.2% of the market and training holds 68.3%, indicating rising demand for real-time, adaptive AI directly on the device.

Chipmakers are now integrating CPU, GPU, and NPU capabilities into compact architectures to support personal AI assistants, smart cameras, wearables, AI PCs, and intelligent home products. Qualcomm highlights that modern Snapdragon mobile platforms are designed to run large-scale generative AI workloads entirely on-device, while AMD is also expanding edge AI capabilities across embedded and client platforms.

Driver Analysis

The key market driver is the rapid expansion of AI-enabled consumer electronics and intelligent endpoint devices that require fast, low-latency, and power-efficient processing. With consumer devices holding 84.2% share and CPUs leading at 63.7%, the market is clearly benefiting from large-volume deployment across smartphones, laptops, wearables, smart home systems, and personal assistants.

AI PCs are also reinforcing this trend. Intel positions its Core Ultra processors for edge AI workloads, including generative AI and autonomous action, while AMD promotes Ryzen AI as a dedicated on-device AI processing platform. These developments support strong demand for edge chipsets that can execute AI models locally while improving responsiveness, privacy, and energy efficiency.

Restraint Analysis

A major restraint is the technical and commercial trade-off between high AI performance and strict power, thermal, and cost limits at the device level. Edge AI chipsets must deliver strong model execution in compact devices without draining battery life or increasing hardware costs beyond acceptable levels. This challenge is especially relevant in consumer electronics, where performance gains must remain affordable at scale.

Even as edge hardware improves, advanced workloads still require careful optimization across memory bandwidth, power consumption, and system design. NVIDIA’s Jetson platforms illustrate how performance gains are closely tied to power envelopes, which shows why scaling advanced edge AI across mass-market products can remain constrained by design complexity and cost sensitivity.

Opportunity Analysis

The strongest opportunity lies in expanding edge AI chipsets into next-generation consumer and embedded platforms that require private, low-latency, always-on intelligence. Since North America accounts for 38% of the market and the US alone is projected to reach USD 13.29 billion by 2034 based on the figures provided, there is clear commercial upside in AI-capable smartphones, AI PCs, smart home devices, industrial endpoints, and autonomous systems.

Vendors that combine efficient compute, flexible software support, and integrated AI acceleration can capture strong demand as device makers move from basic automation toward adaptive and context-aware products. On-device generative AI and embedded AI learning represent especially valuable growth paths because they reduce cloud dependence and improve user responsiveness.

Challenge Analysis

The biggest challenge is building a balanced ecosystem of hardware, software, and developer tools that allows AI models to run efficiently across diverse edge devices. Market success does not depend only on silicon performance. Vendors also need strong SDKs, model optimization tools, and compatibility across applications, operating systems, and device categories.

This is becoming more important as edge AI use cases expand from simple inference to multimodal and generative workloads. AMD’s recent Ryzen AI software updates and Qualcomm’s support for edge AI developer frameworks show that software enablement is now a major competitive factor, not just chip design. Companies that fail to simplify deployment and developer adoption may struggle even if their hardware is technically capable.

Regional Analysis

North America leads the Edge AI Chipsets market with a 38% share, valued at USD 1.60 billion in 2024 based on the figures provided. The region benefits from strong adoption of AI-enabled IoT, autonomous systems, advanced consumer electronics, and a mature semiconductor innovation base.

The US remains the core growth engine, with a market value of USD 1.45 billion in 2024 and projected expansion to USD 13.29 billion by 2034. This leadership is supported by the presence of major chip developers, AI software ecosystems, and rapid integration of on-device AI into PCs, smartphones, robotics, and embedded systems, making North America the primary commercialization hub.

Competitive Analysis

The competitive landscape is led by diversified semiconductor and platform companies that combine hardware performance with software ecosystems. Intel is strengthening its position through Core Ultra processors for edge AI, generative AI, and industrial use cases. AMD is expanding its reach with Ryzen AI and embedded AI portfolios that combine CPU, GPU, and NPU capabilities for responsive on-device intelligence.

Qualcomm is advancing mobile and edge AI through Snapdragon platforms designed for large-scale on-device AI. NVIDIA remains highly influential in embedded and autonomous edge systems through Jetson and related platforms, especially where high-performance AI and robotics applications are required. Competition is increasingly centered on performance efficiency, software support, and deployment flexibility.

Top Key Players in the Market

- Advanced Micro Devices, Inc.

- Alphabet Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Apple Inc.

- Mythic

- Arm Limited

- Samsung

- NVIDIA Corporation

- Huawei Technologies Co., Ltd.

- Others

Conclusion

The Edge AI Chipsets market represents a strong long-term growth opportunity as AI processing shifts closer to the device. Based on the figures provided, the market is expected to rise from USD 4.23 billion in 2024 to USD 48.4 billion by 2034, supported by expanding use across consumer devices, AI PCs, IoT systems, and autonomous platforms.

North America and the US remain the leading commercialization centers, while CPUs, training functions, and consumer devices define the current revenue structure. For clients, this market offers clear value because it connects semiconductor innovation with fast-growing demand for low-latency, power-efficient, and intelligent on-device computing across both high-volume and advanced-edge applications.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)