Table of Contents

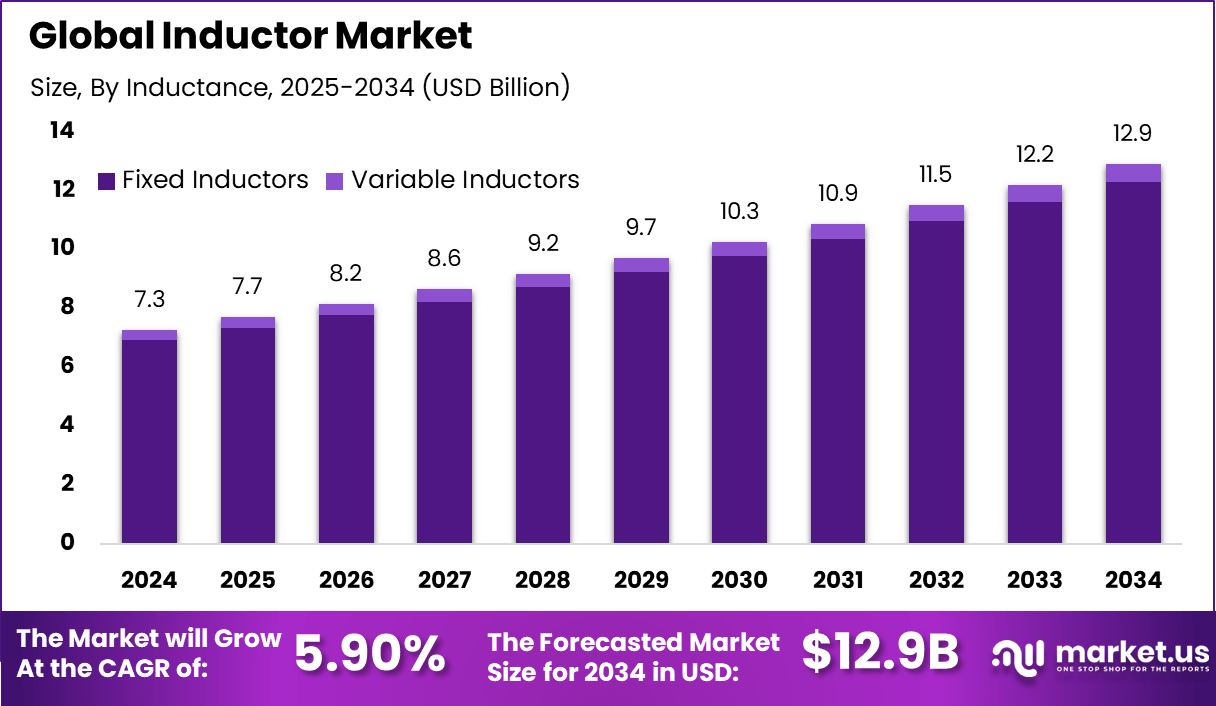

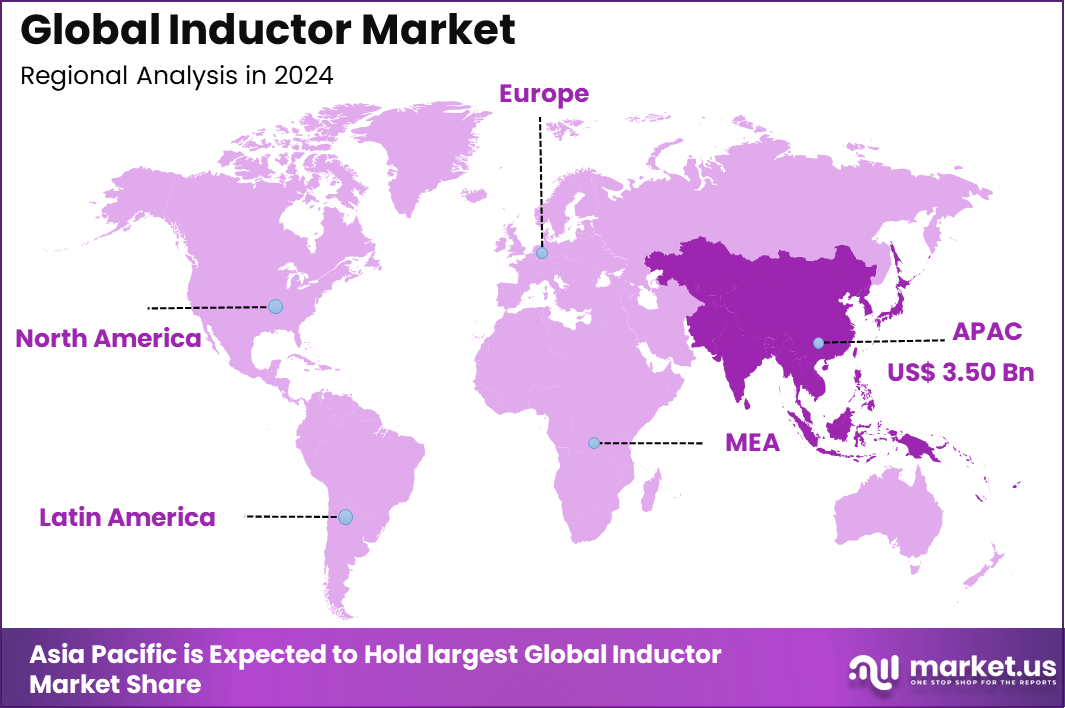

The Global Inductor Market generated USD 7.3 billion in 2024 and is predicted to register growth from USD 7.7 billion in 2025 to about USD 12.9 billion by 2034, recording a CAGR of 5.90% throughout the forecast span. In 2024, Asia Pacific held a dominan market position, capturing more than a 48.2% share, holding USD 3.50 Billion revenue.

Inductors are passive electronic components used to store energy in a magnetic field when electric current flows through them. They are widely used in circuits for power management, filtering, and signal processing across devices such as smartphones, automotive systems, industrial equipment, and power supplies.

As electronic systems become more advanced and compact, inductors are playing a critical role in ensuring stable performance and efficient energy control. Their importance is increasing with the growing complexity of electronic designs and the need for reliable circuit operation.

One of the main driving factors is the rising demand for efficient power management in electronic devices. As devices become smaller and more powerful, there is a need for components that can handle higher frequencies and maintain energy efficiency.

In addition, the growth of electric vehicles and renewable energy systems is increasing the use of inductors in power conversion and energy storage applications. The expansion of communication networks and connected devices is also supporting demand, as inductors help maintain signal quality and reduce interference. Continuous advancements in materials and design are further improving performance and enabling use in compact devices.

Demand for inductors is increasing as industries seek reliable components for modern electronic systems. There is a strong preference for inductors that offer high efficiency, thermal stability, and compact size. Manufacturers are also looking for components that can support high frequency operations and integrate easily into complex circuit designs.

The demand is particularly strong in sectors such as consumer electronics, automotive, and industrial automation, where consistent performance is essential. As electronic applications continue to expand and evolve, the need for durable and efficient inductors is expected to grow steadily.

Top Key Market Segment

- Fixed inductors command 95.2% by inductance, providing stable performance in power supplies, filters, and RF circuits without tuning requirements.

- Multilayered type holds 41.6%, enabling compact high-frequency operation through stacked ceramic layers for miniaturized SMD applications.

- Ferromagnetic/ferrite core captures 66.8%, delivering high permeability, low losses at high frequencies, and effective EMI suppression in compact form factors.

- Shielded variants lead at 71.4%, minimizing crosstalk and magnetic interference in dense PCB layouts for reliable signal integrity.

- Surface mount technique dominates 85.2%, supporting automated assembly, space efficiency, and reflow soldering in high-volume production.

- Consumer electronics end-user claims 30.3%, powering smartphones, laptops, and wearables with efficient DC-DC conversion and noise filtering.

- Asia-Pacific drives 48.2% global value, with China at USD 1.06 billion and 3.7% CAGR, fueled by smartphone assembly hubs and EV component localization.

How AI is Reshaping the Future of this market?

Artificial intelligence is changing how inductors are designed and optimized. Engineers are using AI-based simulation tools to test different materials, core shapes, and winding patterns much faster than traditional methods. This helps in improving efficiency, reducing energy loss, and making inductors smaller without affecting performance.

AI is also helping in predictive modeling, where performance under different load and temperature conditions can be tested virtually before manufacturing. This reduces design errors and shortens development cycles, which is important as electronic devices continue to become more compact and complex.

AI is also improving manufacturing and quality control in the inductor market. Smart production systems use machine learning to monitor production lines, detect defects in real time, and maintain consistency in product quality. This is especially useful in high-demand sectors such as automotive electronics and telecom equipment, where reliability is critical.

In addition, AI-driven demand forecasting helps manufacturers plan production more accurately and manage inventory efficiently. As industries move toward automation and smart electronics, the integration of AI in both design and manufacturing is expected to play a key role in shaping the future of the inductor market.

Regional Analysis

In 2024, Asia Pacific held a dominant market position, capturing more than a 48.2% share, holding USD 3.50 Billion revenue. This leadership is primarily driven by the region’s strong electronics manufacturing ecosystem, where countries such as China, Japan, South Korea, and Taiwan act as global production hubs for consumer electronics, automotive components, and industrial equipment.

The presence of large-scale semiconductor and electronics supply chains has supported consistent demand for inductors across applications like smartphones, power supplies, and automotive electronics. In addition, government support for domestic manufacturing and rising investments in electric vehicles and renewable energy systems are expected to strengthen the regional demand outlook.

Another key factor supporting Asia Pacific’s dominance is the rapid expansion of consumer electronics consumption and industrial automation across emerging economies. Increasing urbanization, rising disposable income, and strong export-oriented production have led to higher adoption of advanced electronic devices, directly influencing inductor demand.

The region also benefits from cost advantages in manufacturing and the presence of skilled labor, which enables large-scale production at competitive pricing. As industries continue to adopt miniaturized and high-efficiency electronic components, Asia Pacific is anticipated to maintain its leading position over the forecast period.

North America is projected to witness steady growth, supported by strong adoption of advanced technologies such as electric vehicles, 5G infrastructure, and industrial automation systems. The region’s focus on high-performance electronics and increasing investments in semiconductor manufacturing are expected to drive demand for specialized inductors. Europe is anticipated to show consistent expansion, driven by the growing automotive electronics sector and the region’s push toward electrification and renewable energy integration.

Latin America is expected to experience gradual growth, supported by improving industrial infrastructure and rising demand for consumer electronics. Meanwhile, the Middle East and Africa region is projected to see moderate growth, driven by increasing investments in telecommunications and infrastructure development. Although these regions are at a relatively early stage compared to Asia Pacific, ongoing digital transformation and industrial development are expected to create new opportunities for inductor adoption over time.

Driver

The rising demand for consumer electronics is a key driver for the inductor market. Devices such as smartphones, laptops, wearable gadgets, and home appliances require stable power management, where inductors play an important role. As these devices continue to become more compact and feature-rich, the need for efficient energy storage and filtering components has increased. This trend is supporting steady demand for inductors across various electronic applications.

In addition, the growing use of electronics in automotive systems is strengthening this demand. Modern vehicles rely on electronic control units, infotainment systems, and safety features that require reliable power regulation. Inductors help maintain voltage stability and reduce signal noise, making them essential in these systems. As vehicle electrification continues, the dependence on such components is expected to remain strong.

Restraint

One major restraint in the inductor market is the fluctuation in raw material availability. Materials such as copper and ferrite are widely used in inductor manufacturing, and their supply can be affected by global trade conditions and mining limitations. These fluctuations create uncertainty in production planning and can impact overall supply consistency.

Another challenge related to this is cost pressure on manufacturers. When raw material prices rise, it becomes difficult for producers to maintain margins without increasing product prices. At the same time, end users often expect stable pricing, especially in highly competitive electronics markets. This creates a difficult balance between cost management and pricing strategies for manufacturers.

Opportunity

The expansion of electric vehicles presents a strong opportunity for the inductor market. Electric powertrains, battery management systems, and charging infrastructure require efficient energy control, where inductors play a critical role. As governments and industries promote cleaner transportation, the adoption of electric vehicles is increasing, which supports demand for advanced electronic components.

Along with this, the development of renewable energy systems is opening new growth areas. Solar and wind energy systems rely on power conversion and energy storage technologies that use inductors. These systems require stable and efficient performance, which increases the need for high-quality inductors. As energy systems shift toward sustainability, this segment is expected to contribute significantly to market expansion.

Challenge

Miniaturization of electronic components remains a key challenge for the inductor market. As devices become smaller, there is a need to reduce the size of inductors without affecting their performance. Achieving this balance is technically complex, as smaller components often face issues related to heat management and efficiency.

Another related challenge is maintaining performance under high-frequency conditions. With the rise of advanced communication systems and fast processing devices, inductors are required to operate at higher frequencies. Ensuring consistent performance, low energy loss, and durability under these conditions requires continuous innovation in design and materials, which can increase development complexity.

Key Market Segment

By Inductance

- Fixed Inductors

- Variable Inductors

By Type

- Film Type

- Multilayered

- Wire Wound

- Molded

By Core Type

- Air Core

- Ferromagnetic/Ferrite Core

- Iron Core

By Shield Type

- Shielded

- Unshielded

By Mounting Technique

- Surface Mount

- Through Hole

By End-user

- Automotive

- Industrial

- RF & Telecommunication

- Military & Defense

- Consumer Electronics

- Transmission & Distribution

- Healthcare

- Others

Competetive Analysis

The competitive landscape of the Inductor Market is led by a group of established electronic component manufacturers with strong global presence. Companies such as TDK Corporation, Murata Manufacturing Co. Ltd, Vishay Intertechnology Inc., Panasonic Holdings Corporation, Taiyo Yuden Co. Ltd, and Samsung Electro-Mechanics Co. Ltd focus on producing a wide range of inductors for applications in consumer electronics, automotive systems, and industrial equipment.

These players emphasize high reliability, miniaturization, and performance efficiency to meet the growing demand for compact and advanced electronic devices. Their strong manufacturing capabilities and continuous product development help them maintain a leading position in the market.

At the same time, companies such as Pulse Electronics (Yageo Corporation), Delta Electronics Inc., Coilcraft Inc., Bourns Inc., Würth Elektronik GmbH & Co. KG, Sumida Corporation, TE Connectivity Ltd, Chilisin Electronics Corporation, AVX Corporation (Kyocera AVX), Bel Fuse Inc., Sunlord Electronics Co. Ltd, Eaton Corporation (Coiltronics), KEMET Corporation (Yageo), and API Delevan Inc. compete by offering specialized and application-specific inductor solutions.

These players focus on cost-effective production, customized designs, and support for high-frequency and power applications. Competition in this market is driven by innovation in component design, demand for energy-efficient electronics, and the ability to supply high-quality components across various end-use industries.

Recent Development

- February, 2026 – Murata expands Thailand plant for high-saturation SMD power inductors serving telecom 5G. LQH series multilayer RF inductors handle 10GHz while DFE metal wirewound boost DC-DC efficiency 98%. Production ramps EV demand.

- January, 2026 – Vishay IHLP high-current inductors rated 125°C for military power supplies. IHVR thin-profile cuts PCB height 50% while Dale wirewound shield EMI in inverters. US distributor giant.

Conclusion

The inductor market is expected to remain stable and grow steadily as demand continues from electronics, automotive, and industrial applications. The increasing use of advanced electronic devices, electric vehicles, and communication systems is supporting consistent demand for inductors across different use cases. Manufacturers are focusing on improving performance, miniaturization, and energy efficiency to meet changing design requirements.

At the same time, the market is facing some pressure from supply chain challenges and the need for cost control, especially with rising raw material concerns. Even with these factors, the long-term outlook remains positive as industries continue to adopt more electronic components in everyday products. Overall, the market is anticipated to move forward with gradual growth, supported by innovation and expanding application areas.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)