Table of Contents

Overview

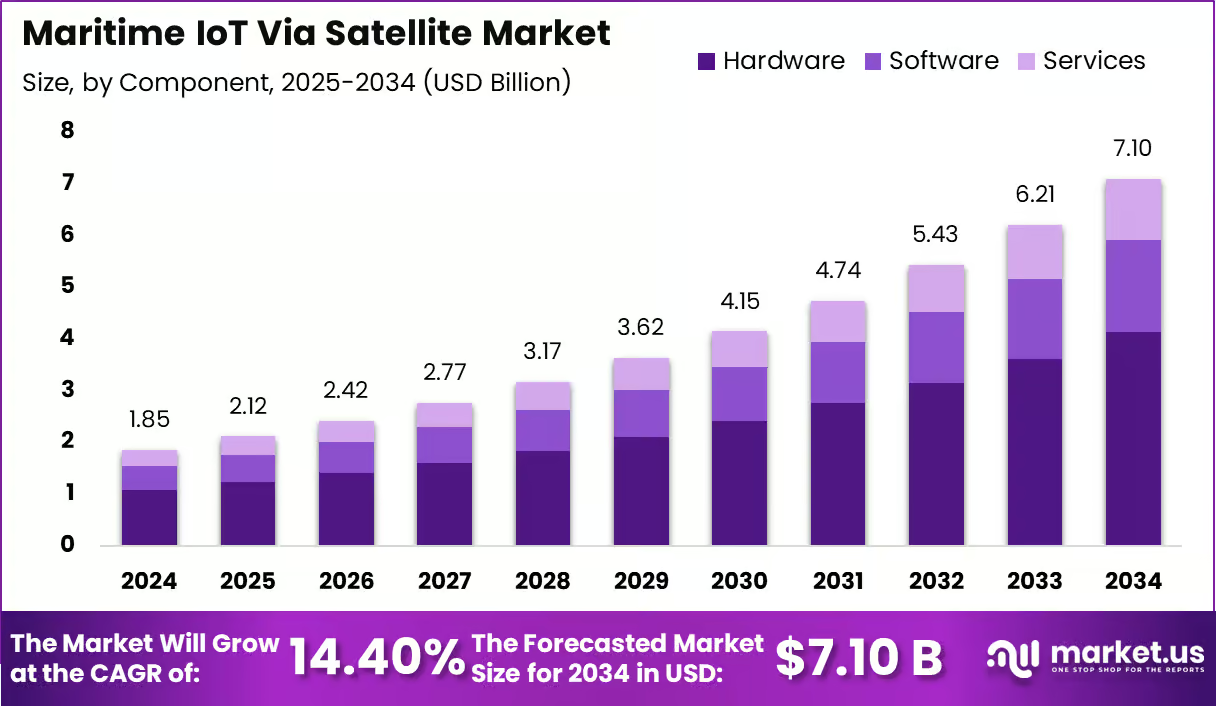

This report delivers strategic value for organizations operating in maritime technology, satellite communications, shipping logistics, and vessel operations. Based on the figures provided, the Maritime IoT via Satellite Market reached USD 1.85 billion in 2024 and is projected to grow to USD 7.10 billion by 2034 at a CAGR of 14.40%.

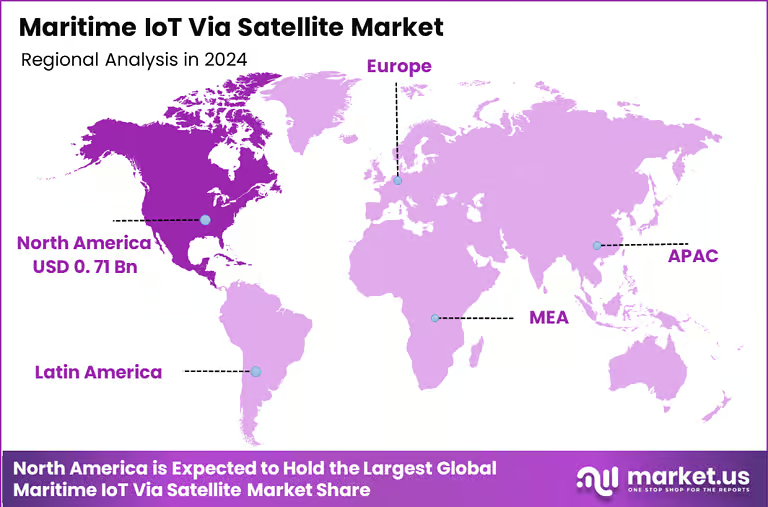

For clients evaluating digital maritime infrastructure, this market reflects a strong shift toward connected vessels and real-time operational intelligence at sea. North America leads the market with a 38.5% share, valued at USD 0.71 billion in 2024, supported by advanced satellite communication infrastructure and increasing adoption of connected vessel technologies.

The US accounts for USD 0.64 billion and is expected to reach USD 2.13 billion by 2034 at a CAGR of 12.78%. By component, hardware dominates with 58.2% due to rising installation of satellite terminals, onboard sensors, and communication modules.

Fleet management and operations lead applications with 36.8%, reflecting strong demand for vessel tracking and performance monitoring. Commercial shipping holds the largest vessel share at 47.5%, while VSAT services lead connectivity with 52.1%. Shipping companies and operators dominate end-user adoption with 62.7%, focusing on efficiency, safety, and regulatory compliance.

Statistics

Operational data across the maritime sector confirms the growing importance of satellite-enabled IoT connectivity. According to the International Maritime Organization, approximately 90% of global trade is transported by sea, highlighting the scale of maritime logistics that increasingly depends on digital connectivity for monitoring and operational efficiency.

The United Nations Conference on Trade and Development reported that global seaborne trade reached around 12 billion tons in recent years, emphasizing the critical role of connected shipping infrastructure. In satellite communications, the International Telecommunication Union states that thousands of commercial vessels rely on satellite networks for navigation, safety systems, and operational communications while traveling across remote ocean regions.

Major satellite providers such as Inmarsat report that modern maritime satellite systems enable real-time data transmission, crew communication, weather updates, and remote diagnostics for onboard equipment.

Additionally, connected vessel technologies help shipping companies reduce fuel consumption through route optimization and engine performance monitoring. These operational improvements are driving maritime companies to adopt IoT-enabled satellite solutions to enhance fleet visibility, improve safety standards, and optimize operational efficiency across global shipping routes.

Effective Takeaways

- The market shows strong long-term expansion, projected to grow from USD 1.85 billion in 2024 to USD 7.10 billion by 2034 based on the figures provided.

- North America leads global adoption due to advanced satellite infrastructure and early maritime digitalization initiatives.

- The US represents the largest national market supported by strong investment in maritime connectivity technologies.

- Hardware dominates the market as vessels increasingly install satellite communication terminals and IoT sensors.

- Fleet management and operational monitoring remain the most valuable application areas for maritime IoT adoption.

- Commercial shipping fleets represent the largest deployment segment due to large-scale cargo transportation networks.

- Shipping companies and fleet operators remain the primary buyers as they focus on improving safety, regulatory compliance, and operational efficiency through connected vessel technologies.

Emerging Trends Analysis

A key emerging trend in the Maritime IoT via Satellite Market is the rapid adoption of smart shipping and connected vessel ecosystems. Shipping companies are integrating satellite-based IoT platforms with onboard sensors, navigation systems, and predictive analytics to improve fleet visibility and operational efficiency. Real-time data transmission from vessels allows operators to monitor engine performance, fuel consumption, route optimization, and cargo conditions even in remote ocean regions.

VSAT connectivity, which accounts for 52.1% of service adoption, supports high-bandwidth communication needed for advanced maritime applications such as remote diagnostics, predictive maintenance, and autonomous vessel support systems. As digital transformation accelerates across the maritime industry, connected satellite IoT networks are becoming essential for improving safety, reducing operational costs, and enabling data-driven fleet management.

Driver Analysis

The primary driver of the market is the increasing need for real-time fleet monitoring, vessel tracking, and operational efficiency across global shipping networks. With commercial shipping representing 47.5% of vessel adoption and shipping companies accounting for 62.7% of end users, the demand for satellite IoT solutions is closely tied to the scale of global maritime logistics.

Satellite-based connectivity allows shipping operators to monitor vessel routes, fuel consumption, and mechanical conditions while ships operate far from terrestrial communication networks. This capability helps companies reduce fuel costs, optimize navigation routes, and improve compliance with international maritime safety regulations, making satellite IoT platforms an essential part of modern fleet management strategies.

Restraint Analysis

Despite strong adoption, high infrastructure and equipment costs remain a significant restraint for the Maritime IoT via Satellite Market. Installing satellite terminals, sensors, communication modules, and onboard data systems requires substantial investment, particularly for older fleets that require retrofitting.

Smaller shipping companies and regional operators may face financial barriers when upgrading vessels with advanced satellite IoT systems. In addition, satellite bandwidth costs and service subscriptions can increase operational expenses over time. These financial considerations may slow the pace of technology adoption, especially in price-sensitive segments of the maritime transport industry.

Opportunity Analysis

A major opportunity in this market lies in the expansion of digital maritime operations through integrated data platforms that combine satellite connectivity, IoT sensors, and predictive analytics. As vessels generate increasing volumes of operational data, shipping companies can use satellite IoT systems to analyze performance patterns, detect equipment failures early, and improve route planning.

Fleet management applications already account for 36.8% of the market, demonstrating strong demand for operational intelligence solutions. Future opportunities also include supporting autonomous shipping technologies, smart ports, and advanced maritime logistics systems that rely on continuous satellite connectivity and real-time data exchange.

Challenge Analysis

One of the key challenges in the Maritime IoT via Satellite Market is ensuring reliable and secure connectivity across vast ocean regions. Maritime operations require continuous communication links even in harsh weather conditions and remote areas where network reliability may fluctuate.

In addition, connected vessel systems increase exposure to cybersecurity risks, as operational data and navigation systems become digitally integrated. Protecting satellite communication networks from cyber threats, ensuring data integrity, and maintaining stable connectivity remain critical challenges for maritime operators adopting IoT-enabled satellite technologies.

Regional Analysis

North America dominates the Maritime IoT via Satellite Market with a 38.5% share, valued at USD 0.71 billion in 2024. The region benefits from advanced satellite communication infrastructure, strong maritime technology innovation, and increasing investments in connected vessel systems.

The United States represents the largest national market, contributing USD 0.64 billion in 2024 and projected to reach USD 2.13 billion by 2034 at a CAGR of 12.78%. Shipping companies in the region are increasingly adopting satellite IoT platforms to improve fleet monitoring, navigation efficiency, and regulatory compliance. Continuous investment in maritime digitalization and satellite communication services supports North America’s leadership in this market.

Competitive Analysis

The competitive landscape of the Maritime IoT via Satellite Market is shaped by satellite communication providers and maritime technology companies specializing in vessel connectivity solutions. Key players such as Inmarsat, Iridium Communications, Viasat, KVH Industries, and Thales Group are actively expanding satellite-based maritime IoT services.

These companies focus on delivering high-bandwidth satellite connectivity, advanced vessel monitoring systems, and integrated communication platforms for shipping operators. Strategic collaborations with maritime technology providers, satellite network expansion, and development of next-generation connectivity solutions remain central strategies for strengthening market presence and supporting the growing demand for connected maritime operations.

Top Key Players in the Market

- Inmarsat Global, Ltd.

- Iridium Communications, Inc.

- ORBCOMM, Inc.

- Globalstar, Inc.

- Thuraya Telecommunications Company

- KVH Industries, Inc.

- Intelsat S.A.

- Cobham SATCOM

- Airbus SE

- Astrocast SA

- Spire Global, Inc.

- Myriota, Ltd.

- Swarm Technologies, Inc.

- Marlink AS

- Sateliot

- Others

Conclusion

The Maritime IoT via Satellite Market is positioned for strong growth as the shipping industry accelerates digital transformation and connected vessel adoption. With the market projected to grow from USD 1.85 billion in 2024 to USD 7.10 billion by 2034, satellite-enabled IoT technologies are becoming critical tools for fleet management, operational monitoring, and maritime safety.

Hardware components, commercial shipping vessels, and VSAT connectivity currently dominate the market, reflecting the industry’s focus on reliable communication and operational efficiency. North America and the United States remain key markets due to advanced satellite infrastructure and strong maritime technology investments. For stakeholders, the market offers significant opportunities in connected vessel platforms, satellite communication systems, and maritime digitalization solutions.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)