Table of Contents

Introduction

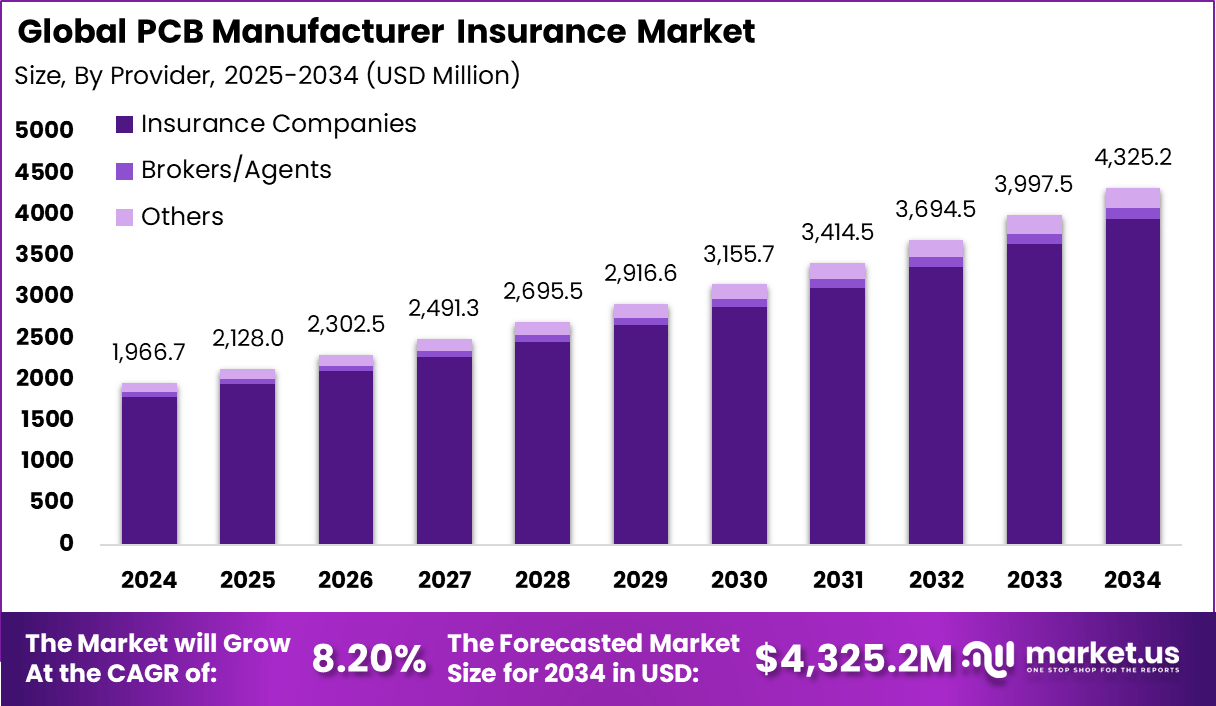

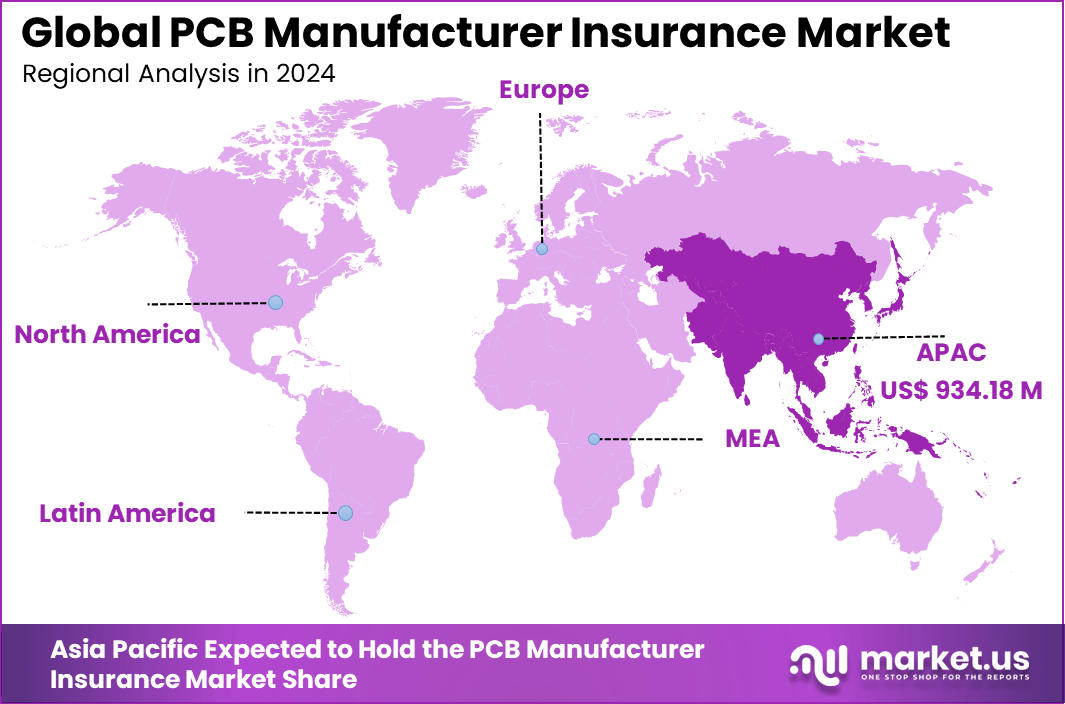

The Global PCB Manufacturer Insurance Market generated USD 1,966.7 million in 2024 and is predicted to register growth from USD 2,128.0 million in 2025 to about USD 4325.2 million by 2034, recording a CAGR of 8.20% throughout the forecast span. In 2024, Asia Pacific held a dominant market position, capturing more than 47.5% share, holding USD 934.18 Million revenue.

PCB manufacturer insurance is a specialized insurance segment created for businesses involved in producing printed circuit boards used in electronics, automotive systems, industrial equipment, and communication devices. PCB manufacturing involves precision machinery, chemical processing, inventory handling, and strict quality standards, which creates a unique risk environment.

Insurance solutions in this market help protect manufacturers against property damage, equipment failure, product liability, workplace incidents, and business interruption. As electronics supply chains grow more complex, insurance is becoming an important tool for financial protection and operational continuity.

One of the main driving factors is the increasing demand for electronic components across multiple industries, which is expanding production activity and factory investments. As manufacturing volumes rise, exposure to machinery breakdown, fire risks, contamination issues, and supply chain delays also increases.

In addition, PCB producers often serve sectors with strict quality requirements, making product liability coverage more important. The use of advanced production equipment and automated lines is further driving demand for policies that cover expensive assets and downtime losses. Growing awareness of cyber risks in connected manufacturing environments is also supporting the need for broader insurance protection.

Demand for PCB manufacturer insurance is rising as companies seek customized coverage that reflects their production processes and contractual obligations. There is a strong preference for policies that combine property, liability, transit, environmental, and interruption protection under one structured solution.

Manufacturers are also looking for insurers that understand export exposure, supplier dependencies, and customer quality claims. The demand is particularly strong among medium and large production facilities supplying automotive, consumer electronics, telecom, and industrial markets where continuity is critical. As manufacturing technology advances and customer requirements become stricter, the need for specialized and reliable insurance solutions is expected to grow steadily.

Top Market Segment

- Property insurance commands 32.5%, safeguarding cleanrooms, etching equipment, multilayer presses, and high-value WIP against fire, contamination, and natural disasters.

- Insurance companies hold 91.3% provider share, delivering specialized policies covering yield losses, supply chain disruptions, and prototype development risks.

- Large enterprises dominate at 73.2% end-user share, securing comprehensive coverage for global facilities, HDI production lines, and export compliance liabilities.

- Brokers/agents lead distribution at 85.9%, negotiating tailored terms for cyber-physical risks, machinery breakdown, and product recall exposures.

- Asia-Pacific drives 47.5% global value, with China at USD 283.9 million and 4.9% CAGR, fueled by smartphone/automotive PCB scale-up and fab investment surge.

How AI is Reshaping the Future of this market?

AI is reshaping the future of the PCB manufacturer insurance market by helping insurers evaluate risk with more precision. PCB manufacturing involves complex production lines, chemical handling, sensitive machinery, quality control issues, and strict delivery timelines. AI helps insurers study these factors in a more practical way by using plant data such as machine performance, defect trends, maintenance records, and production interruptions. This is improving underwriting because policies can be aligned more closely with the actual operating condition of a PCB facility instead of relying only on traditional manufacturing risk assumptions.

AI is also changing claims handling and loss prevention in this market. When a PCB manufacturer faces equipment damage, fire incidents, contamination, product defects, or business interruption, AI can help review records faster and identify the likely cause with better accuracy. It also supports early warning systems by spotting patterns that may lead to breakdowns or quality failures before they become major losses.

Over time, this is expected to make insurance more proactive, with stronger focus on prevention, plant monitoring, and customized coverage for machinery, liability, property damage, and supply chain disruption. As PCB production becomes more advanced and automated, AI is likely to make insurance products more responsive to the real risks faced by manufacturers.

Driver

A key driver for the PCB manufacturer insurance market is the growing operational risk inside PCB production facilities. PCB manufacturing involves chemical processing, heat treatment, precision machinery, clean production environments, and strict quality control. This creates a broad insurance need because even a small incident can affect production continuity, worker safety, product quality, and customer deliveries.

Manufacturers are also facing stronger pressure to protect their plants, equipment, and supply commitments against unexpected disruptions. Insurance is becoming an important part of business continuity planning as PCB producers work with tighter delivery schedules and higher product reliability standards. This is increasing demand for coverage that supports stable manufacturing operations.

Restraint

A major restraint in this market is the complexity of underwriting PCB manufacturing risk. These facilities handle specialized raw materials, chemical waste, sensitive equipment, and fire related hazards, which makes risk assessment more difficult than in general industrial settings. Insurers may take a cautious approach when the full exposure is not easy to measure.

Another restraint is that many manufacturers may view insurance as a cost center rather than a strategic protection tool. Smaller producers in particular may focus more on production spending and process upgrades, which can delay broader insurance adoption. This can limit market expansion, especially in cost sensitive manufacturing environments.

Opportunity

A strong opportunity in this market lies in tailored insurance products designed specifically for PCB manufacturing operations. Standard industrial policies may not fully address the mix of property damage, environmental exposure, machinery breakdown, product liability, and business interruption faced by these manufacturers. This creates room for more specialized coverage solutions.

There is also an opportunity for insurers to support manufacturers with risk improvement services. Guidance related to fire prevention, chemical storage, equipment maintenance, workplace safety, and contamination control can reduce claim frequency and improve plant resilience. This allows insurers to build stronger long term relationships with PCB producers.

Challenge

A major challenge in this market is the changing risk profile of PCB production as manufacturing becomes more advanced. The use of finer circuit designs, higher precision equipment, and more complex materials increases the technical nature of both production and risk evaluation. Insurers must keep pace with these changes to provide relevant and practical coverage.

Another challenge is balancing broad protection with affordable policy structures. PCB manufacturers want coverage that supports plant operations, product responsibility, and sudden disruptions, but insurers must also manage high severity risks linked to fire, pollution, and equipment failure. Maintaining this balance remains difficult, especially in a market where risk exposure can vary greatly from one facility to another.

Regional Analysis

In 2024, Asia Pacific held a dominant market position, capturing more than a 47.5% share, holding USD 934.18 Million revenue. The region led the PCB Manufacturer Insurance Market due to its strong concentration of electronics manufacturing facilities, large printed circuit board production clusters, and deep integration with the global electronics supply chain.

Countries across Asia Pacific serve as major production hubs for consumer electronics, automotive electronics, industrial equipment, and telecom components, which creates a broad need for insurance solutions covering property damage, machinery breakdown, business interruption, cargo exposure, and product liability. The high density of manufacturing operations in the region naturally supports stronger demand for specialized insurance protection.

Another major reason behind Asia Pacific’s leadership is the scale and diversity of PCB manufacturing activity across both large industrial groups and mid sized contract manufacturers. The region faces a wide mix of operational risks linked to chemical handling, fire hazards, equipment intensive production lines, export dependence, and strict delivery commitments.

As a result, manufacturers increasingly view insurance as an essential part of operational continuity rather than only a financial safeguard. In addition, rising investments in advanced electronics manufacturing, semiconductor-linked supply chains, and precision production infrastructure have further strengthened the insurance requirement across the region.

North America represents an important market, supported by demand from high value electronics production, defense related manufacturing, aerospace applications, and growing interest in supply chain resilience. Europe is also a steady market, driven by industrial automation, automotive electronics, and compliance focused manufacturing practices that support structured insurance adoption.

Latin America is developing gradually, with growth linked to the expansion of regional electronics assembly and industrial manufacturing, although coverage penetration remains lower than in more mature regions.

The Middle East and Africa region remains comparatively smaller, but demand is expected to rise with industrial diversification, electronics related investments, and the gradual development of local manufacturing ecosystems.

Key Market Segment

By Insurance Type

- General Liability Insurance

- Product Liability Insurance

- Property Insurance

- Workers Compensation Insurance

- Professional Liability Insurance

- Others

By Provider

- Insurance Companies

- Brokers/Agents

- Others

By End-User

- Small and Medium Enterprises

- Large Enterprises

By Distribution Channel

- Direct

- Brokers/Agents

- Online

Competetive Analysis

The competitive landscape of the PCB Manufacturer Insurance Market is led by major global insurers and specialty commercial insurance providers. Companies such as AIG, Chubb, Zurich Insurance Group, Allianz, AXA XL, Travelers Insurance, Liberty Mutual, and The Hartford focus on coverage solutions for manufacturing risks such as property damage, equipment breakdown, product liability, cyber incidents, and business interruption.

These players use their broad underwriting experience and industrial risk expertise to serve PCB manufacturers operating in complex production environments. Their strong financial capacity and global networks help them maintain a leading position in the market.

At the same time, companies such as Tokio Marine HCC, Sompo International, Munich Re, Berkshire Hathaway, CNA Financial, Markel Corporation, Hanover Insurance Group, Assurant, QBE Insurance Group, and Swiss Re compete through specialty insurance, reinsurance, and customized risk management programs.

These players focus on tailored policies for supply chain disruptions, environmental liabilities, export operations, and technology-related manufacturing risks. Competition in this market is driven by pricing flexibility, industry-specific coverage, claims support quality, and the ability to manage evolving risks in electronics manufacturing.

Top Key Players

- AIG

- Chubb

- Zurich Insurance Group

- Allianz

- AXA XL

- Travelers Insurance

- Liberty Mutual

- The HartfordTokio Marine HCC

- Sompo International

- Munich Re

- Berkshire Hathaway

- CNA Financial

- Markel Corporation

- Hanover Insurance Group

- Assurant

- QBE Insurance Group

- Swiss Re

- Others

Recent Development

- February, 2026 – Chubb Electronics Risk Solutions adds IoT predictive analytics monitoring equipment health. Parametric payouts trigger on power failures while cyber covers production data breaches. Digital transformation pioneer.

- January, 2026 – Zurich PCB PlantGuard insures high-density interconnect lines against fire/explosions. Business interruption calculates lost EV board production while workers comp covers cleanroom injuries. Swiss reliability specialist.

Conclusion

The PCB Manufacturer Insurance Market is expected to grow at a steady pace as manufacturers face rising operational risks linked to equipment damage, fire hazards, product defects, cyber threats, and supply chain disruptions. Insurance is becoming more important for PCB producers because manufacturing environments are complex and highly sensitive to production delays, quality issues, and liability claims.

Demand is also supported by the expansion of electronics production across automotive, industrial, telecom, and consumer applications. Although policy pricing, risk assessment, and coverage customization remain key challenges, the market outlook stays positive as manufacturers increasingly view insurance as an essential tool for financial protection, business stability, and long term operational planning.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)