Table of Contents

Introduction

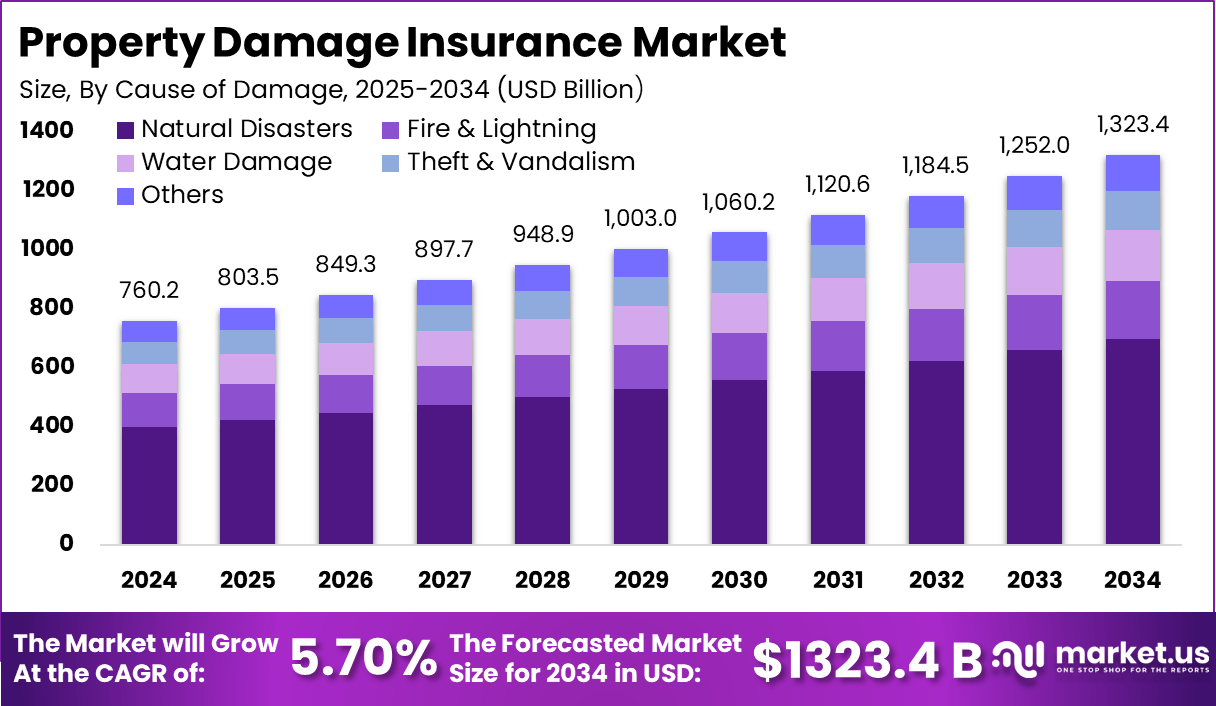

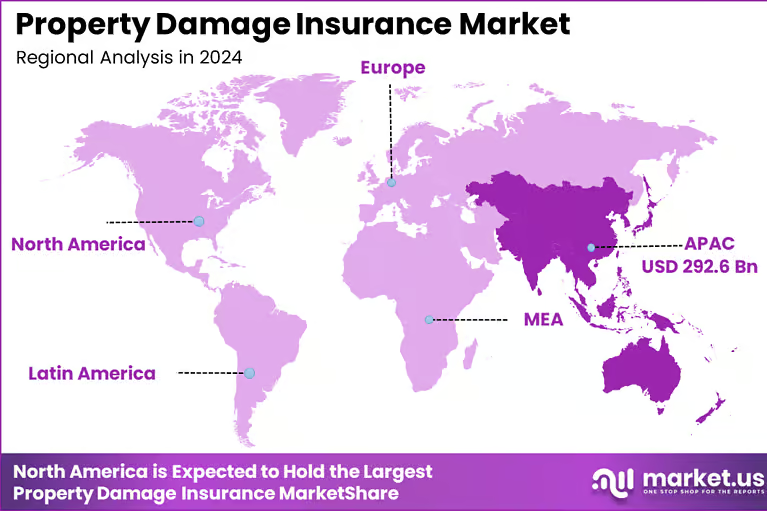

The global property damage insurance market reached USD 760.2 billion in 2024 and is projected to grow at a CAGR of 5.70%, reaching USD 1323.4 billion by 2034. Asia Pacific led with a 38.5% share, generating USD 292.6 billion, while China contributed USD 117.07 billion and is projected to reach USD 212.6 billion by 2034.

Residential property insurance dominated coverage with 41.8%, natural disasters accounted for 52.7% of claims, and homeowners held 31.9% share, reflecting rising climate risks, urban expansion, and increasing awareness of financial protection against property-related losses.

How Growth is Impacting the Economy

The growth of property damage insurance is playing a critical role in stabilizing national and regional economies. Insurance coverage helps distribute financial risk across institutions, reducing the burden on governments during disasters such as floods, storms, and wildfires. This ensures faster economic recovery and supports infrastructure rebuilding without significantly disrupting public finances.

Additionally, increased insurance penetration is strengthening real estate markets and financial systems. Banks and lending institutions rely on insured assets as collateral, enabling smoother credit flow in housing and commercial sectors. As climate risks intensify, insurers are also driving investment in risk modeling, climate analytics, and preventive infrastructure. This encourages the construction of resilient buildings and improved urban planning. Overall, the market is contributing to economic continuity, risk mitigation, and long-term financial stability across both developed and emerging economies.

Impact on Global Businesses

Rising costs in the property damage insurance market are influencing business operations globally. Premiums are increasing due to higher claim frequencies linked to climate events and asset concentration in urban areas. Businesses are also facing higher compliance costs as insurers demand improved risk assessments, safety measures, and documentation before underwriting policies.

Supply chain shifts are emerging as companies reassess facility locations and logistics networks. High-risk zones prone to disasters are becoming less attractive for manufacturing and warehousing. Sector-specific impacts are evident, with construction and real estate companies adopting stricter building standards, while retail and logistics sectors are investing in risk mitigation technologies. Industrial firms are also integrating insurance considerations into asset management strategies, ensuring continuity and reducing potential financial exposure during disruptions.

Strategies for Businesses

Businesses are adopting proactive strategies to manage rising insurance costs and risks. One key approach is investing in resilient infrastructure such as fire-resistant materials, flood defenses, and smart monitoring systems. These measures help reduce premiums and improve insurability.

Another strategy involves leveraging advanced analytics and predictive tools to assess risk exposure more accurately. Companies are also diversifying asset locations to minimize concentration risk and ensure operational continuity. Collaborating with insurers for customized policies and adopting digital risk management platforms are further helping businesses align insurance coverage with evolving operational needs and regulatory requirements.

Key Takeaways

- Market size reached USD 760.2 billion in 2024

- Projected to reach USD 1323.4 billion by 2034 at 5.70% CAGR

- Asia Pacific led with 38.5% market share

- China showed strong growth with 6.15% CAGR

- Residential property insurance dominated with 41.8% share

- Natural disasters accounted for 52.7% of damage claims

- Homeowners held 31.9% end-user share

- Climate risk is a major driver of market expansion

- Insurance is becoming essential for asset protection and financial stability

Analyst Viewpoint

The property damage insurance market is currently experiencing steady growth driven by climate-related risks, urban expansion, and increasing awareness of asset protection. Insurers are focusing on risk-based pricing and advanced analytics to manage exposure more effectively. The market is evolving toward digitalization, with improved underwriting models and faster claim processing systems.

Looking ahead, the outlook remains positive as governments and businesses prioritize risk resilience. Growth is expected to be supported by expanding insurance penetration in emerging markets and stronger regulatory frameworks. Increasing integration of climate data and predictive technologies is likely to enhance efficiency and improve risk assessment accuracy, strengthening long-term market sustainability.

Use Case and Growth Factors

| Use Case | Description | Growth Factor |

|---|---|---|

| Residential Protection | Coverage for homes against fire, floods, and disasters | Rising homeownership and climate risks |

| Commercial Property Coverage | Insurance for offices, retail, and warehouses | Expansion of urban infrastructure |

| Industrial Asset Protection | Coverage for factories and machinery | Growth in manufacturing and asset value |

| Disaster Risk Coverage | Protection against natural disasters | Increasing frequency of extreme weather events |

| Mortgage-linked Insurance | Mandatory insurance for financed properties | Growth in housing finance sector |

| Smart Risk Monitoring | Integration of sensors and analytics | Adoption of digital insurance solutions |

Regional Analysis

Asia Pacific dominated the property damage insurance market with a 38.5% share in 2024, driven by rapid urbanization, infrastructure development, and increasing awareness of risk protection. China remains a key contributor, supported by strong growth in residential and commercial construction. North America continues to be a mature market with high insurance penetration and advanced risk modeling practices.

Europe maintains steady growth due to regulatory frameworks and climate risk policies. Emerging regions such as Latin America and the Middle East are witnessing gradual adoption, supported by economic development and rising demand for asset protection solutions across residential and commercial sectors.

Business Opportunities

The property damage insurance market offers significant opportunities in emerging economies where insurance penetration remains relatively low. Rapid urbanization and infrastructure development are creating demand for new policies across residential and commercial segments. Digital transformation presents another major opportunity, as insurers can enhance customer experience through automated underwriting, real-time risk assessment, and faster claims processing.

Additionally, climate-focused insurance products are gaining traction, allowing companies to design customized coverage for specific risks such as floods and wildfires. Partnerships with construction firms, financial institutions, and technology providers are also opening new revenue streams. Businesses that focus on innovation, customer-centric solutions, and risk-based pricing are expected to capture long-term growth opportunities.

Key Segmentation

The property damage insurance market is segmented by coverage type, cause of damage, and end-user. Residential property insurance leads with 41.8%, driven by increasing homeownership and rising climate-related risks. Due to damage, natural disasters dominate with 52.7%, reflecting growing losses from environmental events.

In terms of end-users, homeowners hold a 31.9% share, supported by regulatory requirements and awareness of financial protection. These segments highlight the market’s focus on risk mitigation, particularly in residential spaces, where exposure to climate events and asset protection needs continue to grow across both developed and emerging regions.

Key Player Analysis

The competitive landscape of the property damage insurance market is characterized by strong emphasis on risk assessment capabilities, underwriting efficiency, and customer service. Market participants are focusing on digital transformation to improve claim processing speed and enhance customer experience. Advanced analytics and data-driven models are being used to assess risk more accurately and optimize pricing strategies.

Top Key Players in the Market

- State Farm

- Allstate

- Liberty Mutual

- USAA

- Farmers Insurance

- Nationwide

- Travelers

- American Family Insurance

- Chubb

- Erie Insurance

- The Hartford

- Auto-Owners Insurance

- Cincinnati Insurance

- CSAA Insurance Group

- MetLife

- Others

Companies are also expanding their product portfolios to include climate-specific coverage and customized insurance plans. Strategic collaborations with technology providers and financial institutions are helping insurers strengthen distribution networks and improve operational efficiency. The focus is shifting toward offering value-added services that enhance long-term customer relationships and retention.

Recent Developments

- Increased adoption of AI-based risk assessment tools for underwriting accuracy

- Growth in climate-focused insurance products targeting disaster risks

- Expansion of digital claims processing platforms for faster settlements

- Rising partnerships between insurers and fintech companies

- Greater regulatory focus on disaster resilience and mandatory coverage policies

Conclusion

The property damage insurance market is evolving with rising climate risks and growing asset values. Strong regional demand, digital transformation, and expanding insurance awareness are expected to support steady growth, making it a critical component of global financial stability and risk management.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)