Table of Contents

Introduction

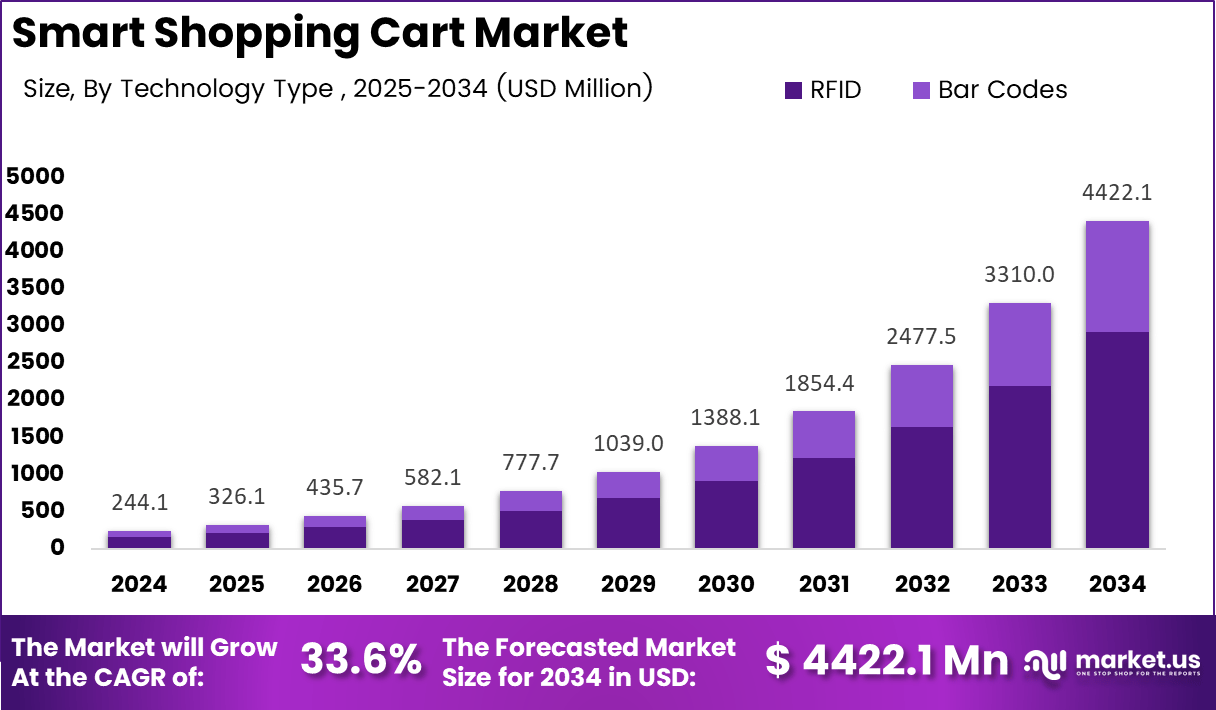

Market.us has released a comprehensive analysis of the Global Smart Shopping Cart Market, projecting exceptional expansion from USD 244.1 Million in 2024 to USD 4,422.1 Million by 2034. The market is forecast to grow at a CAGR of 33.6% over the 2025–2034 period, reflecting accelerating retail digitalization and rising demand for autonomous, frictionless in-store shopping experiences.

Consequently, retailers across supermarkets, hypermarkets, and grocery formats are adopting sensor-based carts equipped with RFID modules, touchscreen interfaces, barcode scanners, and AI-enabled checkout systems. These platforms reduce checkout friction, improve customer flow, and provide real-time inventory monitoring that strengthens operational efficiency across high-footfall retail environments.

Furthermore, government initiatives promoting digital retail transformation, cashless ecosystems, and AI adoption across supply chains are reinforcing market momentum. Public programs supporting smart retail infrastructure and data-driven commerce are encouraging broader deployment of intelligent cart technologies designed for regulatory compliance and consumer data privacy.

Additionally, measurable performance outcomes are accelerating adoption. Smart carts equipped with dual cameras recognize thousands of SKUs with over 95% accuracy, and in-cart personalized promotions have boosted conversion rates by up to 36.8% in regions where these systems operate, demonstrating a compelling return on investment for retailers committing to connected cart platforms.

Finally, the market is evolving beyond hardware into hybrid ecosystems combining AI analytics, cloud processing, guided navigation, and self-checkout capabilities. As retail digitalization accelerates and consumer expectations for seamless in-store experiences rise, smart shopping carts are emerging as essential enablers of interactive, data-driven commerce globally.

Key Takeaways

- The Global Smart Shopping Cart Market is projected to grow from USD 244.1 Million in 2024 to USD 4,422.1 Million by 2034 at a CAGR of 33.6%.

- Hardware dominates the By Offering segment with a 62.8% share.

- Bar Codes lead the By Technology Type segment with a 66.2% share.

- Supermarket/Hypermarket contributes the highest By End-User share at 48.4%.

- North America dominates the regional landscape with a 45.8% share, valued at USD 111.7 Million.

Market Segmentation Overview

By offering, Hardware leads with a 62.8% share, driven by strong adoption of touchscreen displays, barcode scanners, weight sensors, and IoT payment components supporting real-time inventory tracking. Services advance steadily as retailers outsource consulting, installation, and maintenance needs, while Software expands as AI-based recommendation engines, billing algorithms, and analytics platforms become integral to smart cart ecosystems.

By technology type, Bar Codes dominate with 66.2% due to low deployment cost, high compatibility, and proven accuracy across retail formats. RFID is gaining traction in high-volume stores prioritizing hands-free tracking and faster multi-item identification. By end-user, Supermarket/Hypermarket leads with 48.4%, reflecting higher daily footfall, larger basket sizes, and stronger digital transformation investment budgets across large-format retail operators.

Drivers

Rising demand for lightweight, durable cart components and telematics-enabled monitoring is a key growth driver. Retailers increasingly rely on embedded sensors to track cart usage patterns, identify wear, and plan timely servicing, reducing downtime and improving fleet performance. As stores digitize operations, real-time condition monitoring becomes essential for maintaining high-performing smart cart fleets across large-format retail networks.

Government-driven modernization programs and digital retail infrastructure investments are providing additional momentum. Public initiatives encouraging automation, sustainability, and smarter logistics create favorable environments for AI, RFID, and ergonomic system integration. Retailers leverage these policy tailwinds to justify capital investment in smart cart platforms that simultaneously improve operational efficiency and customer experience outcomes.

Use Cases

Supermarket and hypermarket checkout automation represents the most commercially active use case. Smart carts reduce congestion at traditional checkout lanes by enabling item-level scanning and payment directly within the cart throughout the shopping journey. Retailers in high-footfall formats benefit from improved customer throughput, reduced labor dependency, and enriched shopper engagement data that supports targeted promotional strategies.

Personalized in-store promotion delivery is a high-value emerging application. Smart carts equipped with AI recognition engines and touchscreen displays deliver dynamic, context-relevant offers to shoppers as they navigate store aisles. According to research, in-cart personalized promotions have boosted conversion rates by up to 36.8%, making this use case a compelling revenue driver for retailers seeking to monetize in-store digital real estate.

Major Challenges

Persistent material shortages and standard harmonization gaps present meaningful adoption barriers. Forged steel and specialty component shortages disrupt manufacturing schedules and extend procurement lead times for retailers upgrading their cart fleets. Simultaneously, varying safety, design, and digital compliance regulations across regions force manufacturers to adjust technical specifications market by market, slowing cross-border scaling and increasing engineering costs.

Limited digital readiness among smaller retailers restricts sensor-driven maintenance and cloud dashboard adoption. Many independent grocery and specialty formats lack the IT infrastructure needed to support real-time monitoring or predictive servicing, creating unequal adoption patterns across fragmented retail networks. This digital gap keeps modernization slower in cost-sensitive regions where the business case for smart carts remains harder to justify without strong institutional support.

Business Opportunities

Automated supply chain orchestration platforms present a compelling commercial opportunity. Retailers integrating procurement dashboards that streamline ordering for cart components, sensors, and digital modules reduce operational friction and accelerate upgrade cycles across large store networks. Vendors offering end-to-end supply chain visibility alongside smart cart hardware are positioned to capture longer-term, higher-value relationships with major retail chains.

Sustainability-driven refurbishment and remanufacturing services represent a parallel revenue opportunity. Retailers increasingly prefer upgrading existing carts with new sensors, screens, and lightweight alloy components rather than purchasing entirely new units. This trend extends cart lifecycle value, reduces environmental impact, and opens recurring service-based revenue streams for maintenance providers as the market transitions from hardware-only toward hybrid platform models.

Regional Analysis

North America leads the global market with a 45.8% share valued at USD 111.7 Million, supported by advanced retail digitalization, widespread AI-enabled in-store automation, and strong IoT network infrastructure across the United States and Canada. National supermarket chains continue expanding smart cart deployments, and rising consumer preference for contactless, automated shopping experiences sustains strong regional demand momentum.

Asia Pacific is emerging as a rapidly evolving market, fueled by high supermarket footfall, deep mobile payment penetration, and rising AI-powered retail automation across China, Japan, and South Korea. Europe demonstrates steady expansion driven by cashierless format adoption, labor optimization needs, and strong regulatory support for digital commerce innovation across Germany, France, and the UK. Latin America and Middle East & Africa are advancing gradually as retail modernization programs and IoT integration gain traction across key urban markets.

Recent Developments

- In November 2025, Caper Carts launched at Coles Supermarkets in Australia and at a Morrisons store in the UK, while ShopRite and Schnucks expanded smart cart deployments across additional U.S. store locations, accelerating checkout automation momentum.

- In April 2025, organizers announced EuroShop 2026, highlighting technology innovations reshaping retail from back-office operations to customer checkout. The EuroCIS Retail Technology dimension is scheduled for February 22–26, 2026, showcasing industry expertise and solutions across the global retail technology ecosystem.

Conclusion

The Global Smart Shopping Cart Market is entering a period of exceptional growth driven by retail digitalization, AI-powered in-store automation, and rising consumer demand for frictionless shopping experiences. With the market forecast to expand from USD 244.1 Million in 2024 to USD 4,422.1 Million by 2034 at a CAGR of 33.6%, stakeholders across retail technology, hardware manufacturing, and AI commerce sectors face significant opportunities to capture value in this rapidly evolving landscape.

As smart cart ecosystems mature from standalone hardware into fully integrated platforms combining AI analytics, personalized promotions, and autonomous checkout, retailers and technology providers that invest decisively in scalable, compliant, and experience-driven solutions will define the competitive future of intelligent in-store commerce globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)