Table of Contents

Overview

This report provides strategic value for organizations evaluating the next generation of artificial intelligence capabilities that extend beyond narrow AI systems. Based on the figures provided, the global Artificial General Intelligence market was valued at USD 990.7 million in 2024 and is projected to reach USD 32,332.6 million by 2034, expanding at a CAGR of 41.70%.

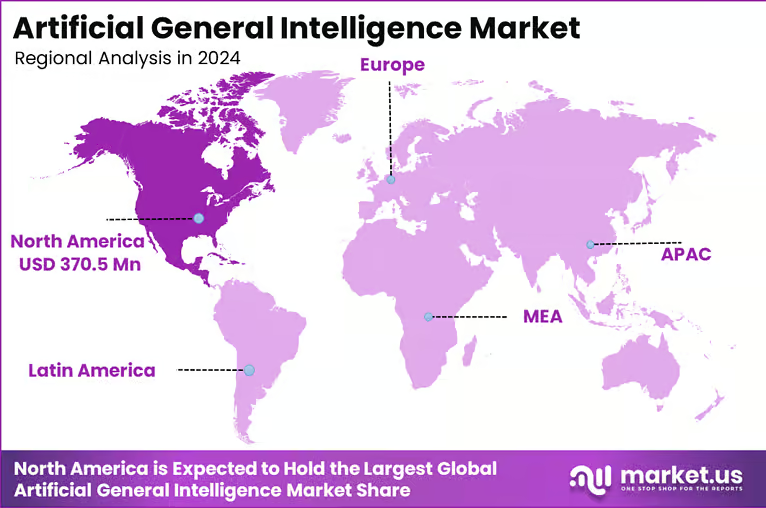

For clients operating in advanced AI research, robotics, healthcare technology, and enterprise AI platforms, this reflects a rapidly emerging market that is transitioning from theoretical development toward early commercialization. North America holds 37.4% of the market, valued at USD 370.5 million in 2024, supported by strong research ecosystems, advanced computing infrastructure, and major technology investments.

The US alone contributed USD 314.94 million and is expected to grow at a CAGR of 38.6%. Cloud deployment leads with 60.6% share, reflecting the need for scalable computing power for complex AI models. Functional AGI holds 40.5% of the market, driven by efforts to create systems capable of performing diverse tasks autonomously.

Autonomous robotics and humanoid AI account for 34.6% of applications, while healthcare and life sciences dominate end-user adoption with 32.2%, highlighting strong demand for AI-driven diagnostics and research support.

Statistics

Real-world technology indicators demonstrate the accelerating momentum behind advanced AI systems. According to the International Data Corporation, global spending on artificial intelligence systems surpassed USD 154 billion in 2023, reflecting strong investments in AI infrastructure, research, and enterprise deployment.

The US National Science Foundation has significantly increased funding for AI research programs across universities and research institutions, supporting the development of advanced machine learning and cognitive computing systems. In robotics, the International Federation of Robotics reported that over 553,000 industrial robots were installed globally in a single year, demonstrating expanding automation capabilities that could benefit from AGI-based intelligence systems.

The World Health Organization has also highlighted the growing role of AI in healthcare diagnostics, medical imaging, and drug discovery research. Additionally, the US Department of Energy has invested in large-scale supercomputing systems designed to support advanced AI research and simulation models.

These developments show that government agencies, research institutions, and technology companies are rapidly expanding investments in computing infrastructure and AI capabilities, which directly supports the evolution of more advanced AI systems with broader reasoning and decision-making capabilities.

Effective Takeaways

- The market shows extremely rapid expansion, projected to grow from USD 990.7 million in 2024 to USD 32,332.6 million by 2034 based on the figures provided.

- North America remains the leading innovation hub due to strong research investment, advanced computing infrastructure, and major technology companies.

- The United States is the largest national market supported by strong government funding and technology development programs.

- Cloud-based deployment dominates the market because AGI systems require highly scalable computing infrastructure.

- Functional AGI represents the most active development segment as researchers pursue systems capable of performing multiple cognitive tasks.

- Robotics and humanoid AI applications are emerging as key commercial use cases for AGI technologies.

- Healthcare and life sciences remain the leading end users due to strong demand for AI-driven diagnostics, drug discovery, and medical research.

Emerging Trends Analysis

A major emerging trend in the Artificial General Intelligence market is the convergence of advanced AI models with robotics, autonomous systems, and human-machine interaction technologies. Research institutions and technology companies are increasingly developing AI systems capable of reasoning across multiple domains rather than performing narrow tasks.

This shift is reflected in the growing share of functional AGI systems and the rising role of autonomous robotics and humanoid AI applications. These technologies aim to combine perception, reasoning, planning, and decision-making abilities within a single AI architecture, enabling machines to perform complex real-world tasks.

Driver Analysis

The primary driver of the AGI market is the rapid increase in investments in advanced artificial intelligence research and high-performance computing infrastructure. Governments, technology companies, and research organizations are investing heavily in AI development to support innovation in automation, healthcare diagnostics, robotics, and scientific research.

Cloud-based computing platforms have enabled researchers to train large AI models more efficiently, which is why cloud deployment accounts for 60.6% of the market. These investments are accelerating the development of more advanced AI capabilities with broader problem-solving abilities.

Restraint Analysis

One of the key restraints in the AGI market is the extremely high computational requirements and development costs associated with advanced AI systems. Training large-scale AI models requires significant processing power, specialized hardware, and extensive datasets.

These requirements can create financial and technical barriers for smaller organizations and research groups attempting to develop AGI technologies. Additionally, concerns around ethical AI development, safety frameworks, and regulatory oversight may slow deployment as governments work to establish guidelines for responsible AI innovation.

Opportunity Analysis

Significant opportunities exist in applying AGI technologies across complex industries that require advanced reasoning and decision-making capabilities. Healthcare, which currently represents 32.2% of end-user demand, presents strong potential for AGI systems capable of supporting diagnostics, personalized medicine, and medical research.

Robotics, autonomous vehicles, and industrial automation also represent promising areas where AGI technologies could enable machines to adapt to dynamic environments and perform tasks that currently require human cognitive abilities.

Challenge Analysis

The biggest challenge in the AGI market is developing AI systems that can generalize knowledge across different tasks while maintaining reliability and safety. Current AI technologies often excel in specific tasks but struggle with broad reasoning or contextual understanding.

Achieving true general intelligence requires significant breakthroughs in algorithm design, learning architectures, and cognitive modeling. Ensuring safe and ethical deployment of highly capable AI systems remains a critical challenge for researchers, policymakers, and technology companies.

Regional Analysis

North America dominates the Artificial General Intelligence market with a 37.4% share and a market size of USD 370.5 million in 2024. The region benefits from strong research institutions, advanced computing infrastructure, and substantial investments from leading technology companies.

The United States represents the largest national market, contributing USD 314.94 million and projected to grow at a CAGR of 38.6% during the forecast period. Government-funded research programs, large-scale AI development initiatives, and partnerships between universities and technology companies continue to accelerate AGI innovation in the region, positioning North America as the global center for advanced AI research and commercialization.

Competitive Analysis

The competitive landscape of the Artificial General Intelligence market is shaped by major technology companies, AI research laboratories, and emerging startups focused on developing advanced cognitive AI systems. Leading organizations such as OpenAI, DeepMind (Google), IBM, Microsoft, and NVIDIA are investing heavily in next-generation AI architectures and high-performance computing systems to support AGI research.

Top Key Players in the Market

- Alphabet Inc.

- Microsoft Corporation

- NVIDIA Corporation

- Meta

- OpenAI

- Anthropic PBC

- Numenta

- Hanson Robotics Ltd.

- SingularityNET

- SAP SE

- xAI

- Glean

- DataRobot, Inc.

- InWorld AI

- Aleph Alpha

- Markovate

- Zhipu AI

- Other Major Players

These companies focus on developing large-scale AI models, reinforcement learning systems, and advanced neural network architectures capable of performing diverse cognitive tasks. Strategic collaborations with research institutions and cloud infrastructure providers remain central to accelerating AGI innovation and expanding real-world applications.

Conclusion

The Artificial General Intelligence market represents one of the most transformative opportunities within the global technology sector. With the market projected to grow from USD 990.7 million in 2024 to USD 32,332.6 million by 2034, AGI technologies are expected to reshape industries ranging from healthcare and robotics to scientific research and automation.

Cloud-based deployment, functional AGI systems, and robotics applications currently dominate market development, while healthcare remains the leading end-user segment. North America and the United States continue to lead innovation due to strong research investment and advanced computing infrastructure. For stakeholders, the market offers significant long-term opportunities in advanced AI research, intelligent automation, and next-generation cognitive computing platforms.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)