Introduction

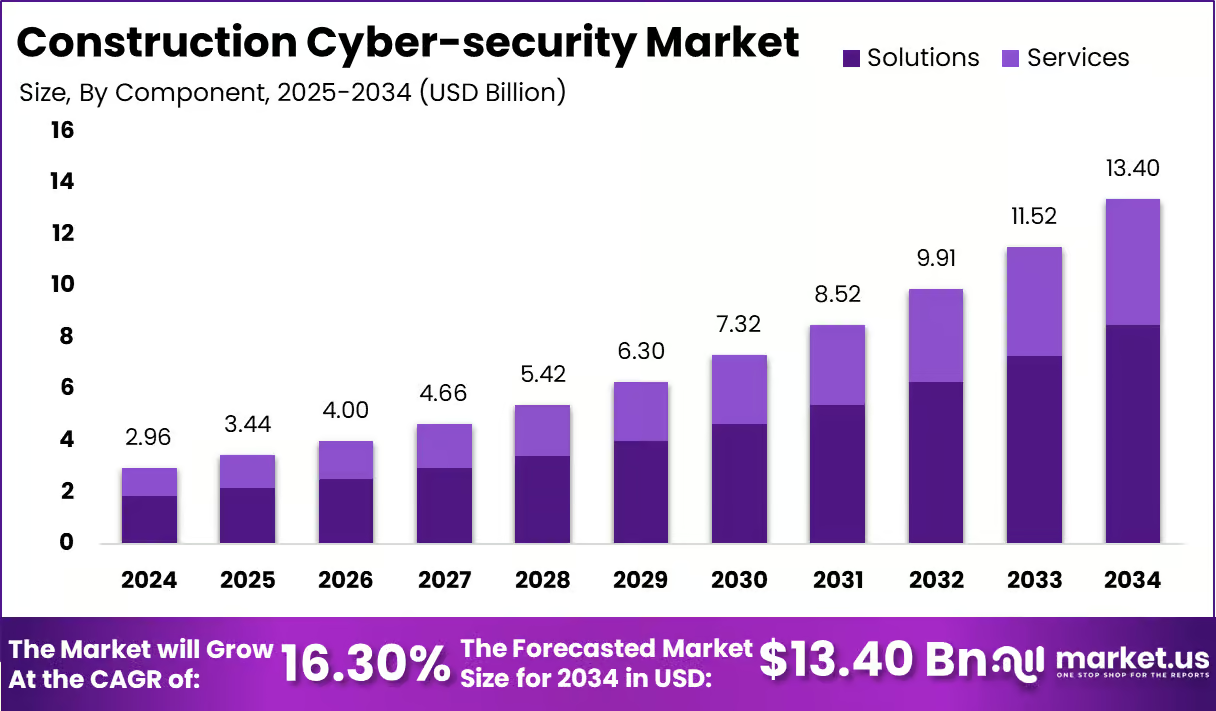

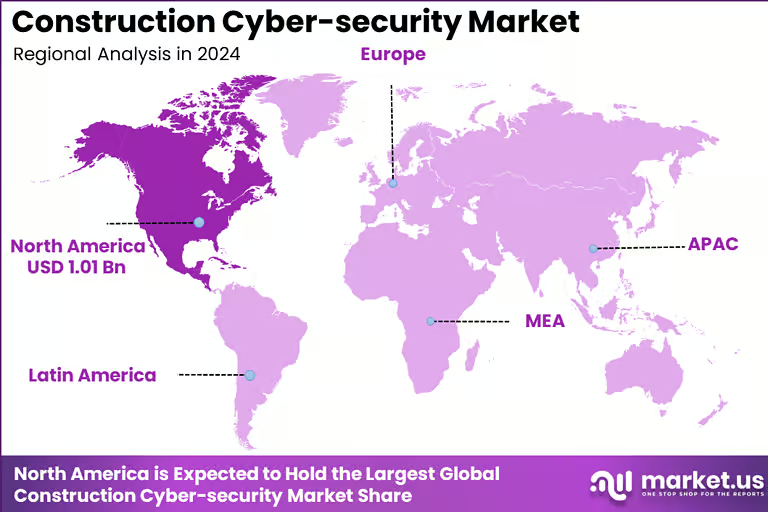

The construction cybersecurity market reached USD 2.96 billion in 2024 and is projected to grow at a CAGR of 16.30% to USD 13.40 billion by 2034. North America held 34.3% share valued at USD 1.01 billion, while the US accounted for USD 0.92 billion and is expected to reach USD 3.76 billion by 2034.

Solutions dominated with 63.4%, network security held 32.7%, and cloud-based deployment captured 58.9%. Large enterprises led with 71.5%, project management data protection accounted for 38.6%, and general contractors held 48.3%, highlighting rising cyber risks in digital construction ecosystems.

How Growth is Impacting the Economy

The rapid growth of construction cybersecurity is strengthening economic resilience by protecting critical infrastructure and large-scale development projects from cyber threats. As construction becomes increasingly digital, with the adoption of BIM, IoT-enabled machinery, and cloud collaboration platforms, cybersecurity investments are ensuring uninterrupted project execution and minimizing financial losses from cyber incidents.

This growth is also creating new economic opportunities in cybersecurity services, software development, and risk consulting. Governments and private players are investing in secure digital infrastructure, which supports safer urban development and smart city initiatives. Additionally, improved cybersecurity reduces delays caused by data breaches or system failures, ensuring timely project delivery and cost control. Overall, the market is contributing to economic stability, secure infrastructure expansion, and long-term digital transformation in the construction industry.

Impact on Global Businesses: Rising Costs and Supply Chain Shifts

Rising cybersecurity costs are becoming a key concern for construction firms as they allocate more budget toward threat detection, network protection, and compliance systems. Investments in secure cloud platforms, endpoint protection, and identity management are increasing operational expenses, particularly for large enterprises managing complex infrastructure projects.

Supply chain shifts are also occurring as construction companies prioritize secure vendors and digital platforms. Third-party risks are being closely evaluated, especially with multiple stakeholders involved in projects. Sector-specific impacts are visible in project management, where sensitive data such as BIM models and financial records require robust protection. Contractors and developers are integrating cybersecurity into procurement and project planning processes to reduce vulnerabilities and ensure secure collaboration across global supply chains.

Strategies for Businesses

Businesses are adopting comprehensive cybersecurity strategies to manage evolving risks in construction environments. One key approach is implementing integrated security frameworks that combine network protection, endpoint security, and identity management. This ensures a holistic defense against cyber threats across all project stages.

Another strategy involves adopting cloud-based security solutions that provide scalability and real-time monitoring. Companies are also investing in employee training and awareness programs to reduce human error, which remains a major vulnerability. Collaborating with cybersecurity providers and conducting regular risk assessments helps businesses strengthen their defenses. These strategies enable firms to maintain secure operations while supporting digital transformation initiatives.

Key Takeaways

- The market reached USD 2.96 billion in 2024

- Expected to reach USD 13.40 billion by 2034

- CAGR of 16.30% indicates rapid growth

- North America led with 34.3% share

- US projected to reach USD 3.76 billion by 2034

- Solutions dominated with 63.4% share

- Network security held 32.7% share

- Cloud-based deployment captured 58.9%

- Large enterprises accounted for 71.5%

- General contractors held 48.3% share

Analyst Viewpoint

The construction cybersecurity market is currently experiencing strong growth driven by increasing digitalization and rising cyber threats across infrastructure projects. The dominance of cloud-based solutions and network security reflects the need for scalable and robust protection systems. Large enterprises are leading adoption due to their complex operations and higher exposure to cyber risks.

Looking ahead, the market shows a positive outlook as construction firms continue integrating advanced technologies such as IoT and AI into their operations. This will further increase the demand for cybersecurity solutions. As regulatory frameworks strengthen and awareness improves, adoption is expected to expand across mid-sized firms, supporting sustained market growth and enhanced security across the industry.

Use Case and Growth Factors

| Use Case | Description | Growth Factor |

|---|---|---|

| BIM Data Protection | Securing building design and project files | Rising use of digital design tools |

| Network Security for Jobsites | Protecting connected devices and machinery | Growth of IoT in construction |

| Cloud Collaboration Security | Safeguarding remote project data access | Increase in cloud adoption |

| Identity and Access Management | Controlling user access to systems | Need for secure multi-party collaboration |

| Endpoint Protection | Securing devices used on-site | Expansion of mobile and remote work |

| Risk Monitoring and Analytics | Detecting threats in real time | Adoption of AI-driven security tools |

Regional Analysis

North America dominates the construction cybersecurity market with a 34.3% share, supported by high adoption of digital construction technologies and strong regulatory frameworks. The US leads regional growth with significant investments in infrastructure and cybersecurity solutions. Europe follows with steady adoption driven by compliance requirements and digital transformation initiatives.

Asia Pacific is emerging as a high-growth region due to rapid urbanization, increasing infrastructure projects, and growing awareness of cybersecurity risks. Other regions are gradually adopting cybersecurity solutions as construction activities expand and digitalization becomes more widespread across global markets.

Business Opportunities

The construction cybersecurity market presents strong opportunities driven by increasing digital transformation in the industry. As construction firms adopt cloud platforms, IoT devices, and data-driven project management tools, the demand for advanced security solutions continues to rise. Emerging markets offer untapped potential as infrastructure development accelerates.

Opportunities also exist in managed security services, which allow companies to outsource cybersecurity operations. Integration of AI and automation in threat detection is creating new avenues for innovation. Companies that focus on scalable, cloud-based solutions and industry-specific offerings are expected to capture significant market share. Partnerships with construction firms and technology providers further enhance growth prospects.

Key Segmentation

The construction cybersecurity market is segmented by component, security type, deployment mode, organization size, application, and end-user. Solutions lead with 63.4%, reflecting high demand for advanced security tools. Network security dominates with 32.7% due to increased connectivity across construction sites. Cloud-based deployment holds 58.9%, driven by remote collaboration needs.

Large enterprises account for 71.5%, highlighting their higher risk exposure. Project management data protection leads applications with 38.6%, while general contractors dominate end-users with 48.3%, emphasizing their central role in managing complex construction data ecosystems.

Key Player Analysis

The competitive landscape of the construction cybersecurity market is characterized by a strong focus on innovation, integration, and service delivery. Market participants are developing advanced security solutions tailored to construction-specific challenges such as multi-party collaboration and data protection. Emphasis is placed on enhancing threat detection capabilities and improving response times.

Top Key Players in the Market

- Palo Alto Networks, Inc.

- Cisco Systems, Inc.

- Fortinet, Inc.

- Check Point Software Technologies, Ltd.

- Broadcom, Inc. (Symantec)

- IBM Corporation

- Microsoft Corporation

- Trend Micro, Incorporated

- McAfee Corp.

- CrowdStrike Holdings, Inc.

- Sophos, Ltd.

- Tenable Holdings, Inc.

- Rapid7, Inc.

- Qualys, Inc.

- CyberArk Software, Ltd.

- Others

Companies are also expanding their offerings through cloud-based platforms and managed services. Strategic partnerships with construction firms and technology providers are helping players strengthen their market presence. Continuous investment in research and development is enabling companies to address evolving cyber threats and maintain a competitive advantage in a rapidly growing market.

Recent Developments

- Increased adoption of AI-based threat detection systems in construction projects

- Expansion of cloud-based cybersecurity platforms for remote collaboration

- Rising investment in managed security services for construction firms

- Integration of cybersecurity into smart city and infrastructure projects

- Growing focus on regulatory compliance and data protection standards

Conclusion

The construction cybersecurity market is growing rapidly due to increasing digitalization and cyber risks. Strong demand for cloud-based and network security solutions, along with expanding infrastructure projects, is expected to support long-term growth and strengthen security across the global construction industry.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)