Table of Contents

Introduction

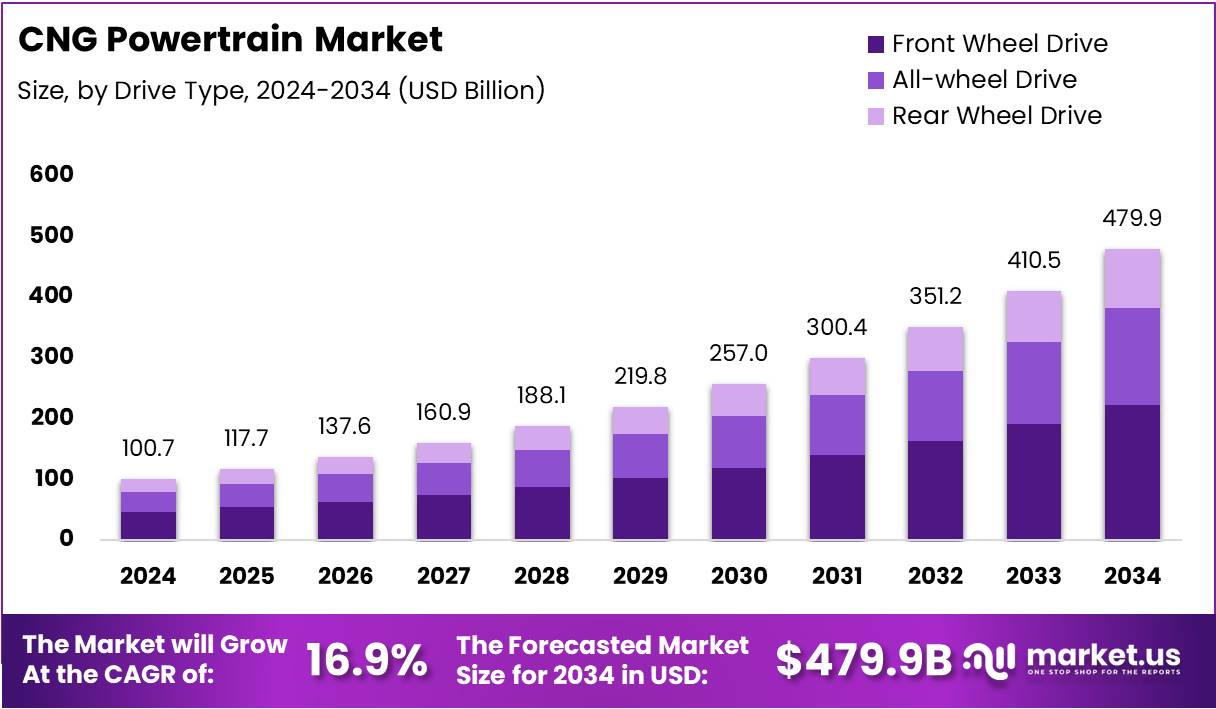

Market.us has released a comprehensive analysis of the Global CNG Powertrain Market, projecting robust expansion from USD 100.7 Billion in 2024 to USD 479.9 Billion by 2034. The market is forecast to grow at a CAGR of 16.9% over the 2025–2034 period, reflecting accelerating global demand for cleaner, cost-efficient mobility solutions.

Consequently, governments across major economies are tightening emission standards and directing investment toward low-carbon transportation. These regulatory measures are compelling automakers, fleet operators, and public transit agencies to accelerate their shift toward CNG-based powertrains, creating a consistent demand pipeline across both emerging and mature markets.

Furthermore, rising fuel-price volatility is reinforcing CNG’s appeal as a predictable, economical alternative to gasoline and diesel. CNG achieves 12–20% lower fuel consumption than gasoline and delivers an average mileage of 25–30 km per kg, providing measurable operational savings for both individual users and large commercial fleets.

Additionally, the ongoing expansion of refueling infrastructure and the entry of OEM-backed factory-fitted CNG models are removing traditional adoption barriers. Together, these developments are generating a self-reinforcing growth cycle that is broadening the market’s reach across passenger vehicles, logistics fleets, and urban transit networks worldwide.

Finally, innovation in CNG system design — spanning advanced onboard diagnostics, lightweight composite cylinders, and dual-fuel engine compatibility — is elevating performance standards. These technological advances are strengthening end-user confidence, positioning CNG powertrains as a durable bridge technology in the global clean-energy transition.

Key Takeaways

- The Global CNG Powertrain Market is projected to grow from USD 100.7 Billion in 2024 to USD 479.9 Billion by 2034 at a CAGR of 16.9%.

- Front Wheel Drive dominates the drive type segment with a 46.6% share.

- Bi-fuel leads the fuel type segment with a 76.9% share.

- Passenger Vehicle dominates the vehicle type segment with an 82.4% share.

- Asia Pacific is the leading region with a 58.7% market share, valued at USD 59.1 Billion.

Market Segmentation Overview

By drive type, Front Wheel Drive holds the largest share at 46.6%, driven by its efficiency advantages and suitability for compact and mid-size platforms. Meanwhile, All-wheel Drive maintains steady traction in utility segments, while Rear Wheel Drive continues serving light trucks and logistics fleets requiring strong load-carrying capability.

By fuel type, Bi-fuel configurations lead with a commanding 76.9% share, as the ability to switch between CNG and gasoline reduces range anxiety and operational risk. By vehicle type, Passenger Vehicles account for 82.4% of the market, supported by urban incentives and rising consumer preference for economical, lower-emission daily transportation.

Drivers

Government mandates are a primary growth engine. As emission norms tighten across North America, Europe, and Asia Pacific, automakers and fleet operators are under mounting pressure to adopt compliant alternatives. CNG powertrains offer an immediate, proven pathway to regulatory alignment, making them a practical choice for public transport agencies managing large-scale fleet modernization programs.

Rising operational cost pressure is equally influential. CNG’s lower per-kilometer running cost makes it highly attractive for logistics operators, ride-sharing companies, and urban commuter services where fuel expenses represent a significant proportion of total operating costs. As energy price uncertainty persists, the predictability of CNG expenditure strengthens its competitive positioning against conventional fuels.

Use Cases

Urban public transportation represents one of the most active use cases. City bus fleets across Asia Pacific and Europe are increasingly converting to CNG to reduce inner-city pollution and comply with zero-emission zone requirements. CNG buses deliver reliable range, lower noise levels, and reduced particulate emissions, making them well-suited to dense urban operating conditions.

Commercial last-mile delivery is another high-growth application. Logistics operators running delivery vans and light commercial vehicles are adopting CNG powertrains to lower fleet operating costs while meeting sustainability targets. Bi-fuel configurations are especially valued in this segment, as they allow drivers to complete routes without being constrained by CNG station availability.

Major Challenges

Infrastructure gaps remain the most critical restraint. Many regions lack adequate high-pressure CNG refueling networks, making daily operation difficult for users outside major urban centers. Building these stations demands significant capital investment and strict safety compliance, causing uneven rollout that limits CNG vehicle adoption particularly in rural and semi-urban areas.

Performance limitations in heavy-duty applications also constrain growth. While CNG engines excel in light and medium vehicle categories, they struggle to deliver the torque levels required by heavy trucks, construction machinery, and high-payload transport. In these segments, diesel and hybrid alternatives retain a competitive advantage, reducing the addressable market available to CNG system suppliers.

Business Opportunities

OEM expansion into factory-fitted CNG lineups presents a compelling commercial opportunity. As manufacturers integrate CNG systems at the production stage rather than relying on aftermarket conversions, buyers gain warranty coverage, improved reliability, and greater resale confidence. This shift is expected to broaden consumer acceptance significantly, particularly in markets where brand trust plays a key role in alternative-fuel adoption decisions.

The emergence of Bio-CNG and dual-fuel CNG–hydrogen compatible platforms opens a further opportunity horizon. Suppliers and manufacturers that develop engines capable of blending or switching between CNG and hydrogen will be strategically positioned as the hydrogen economy matures. This forward compatibility reduces technology obsolescence risk and strengthens the long-term investment case for CNG powertrain development.

Regional Analysis

Asia Pacific leads the global market with a 58.7% share valued at USD 59.1 Billion, driven by large vehicle production volumes, rapid urbanization, and strong government support for affordable clean mobility. Countries including India and China are central to regional growth, with expanding refueling networks and rising OEM participation reinforcing demand momentum across both passenger and commercial segments.

North America and Europe represent high-value secondary markets. North America benefits from abundant domestic natural gas supply and growing alternative-fuel fleet conversion programs, while Europe’s stringent emission regulations and rising interest in renewable CNG are accelerating adoption across passenger and light commercial vehicle categories. Both regions continue investing in infrastructure and regulatory frameworks that support long-term CNG market expansion.

Recent Developments

- In November 2025, the U.S. Federal Transit Administration allocated USD 2 Billion in funding focused on CNG and hybrid bus replacement programs, expected to accelerate alternative-fuel public transportation adoption nationally.

- In November 2025, Westport unveiled a new CNG solution for its HPDI natural gas engine technology, targeting expanded market share across North America.

- In December 2024, Aramco completed the acquisition of a 10% stake in Horse Powertrain Limited, a joint venture between Renault Group and Geely, aimed at fostering innovation in sustainable mobility technologies.

- In September 2024, Cummins launched the X15N natural gas engine designed for heavy-duty, long-haul applications in North America, offering improved fuel efficiency and lower emissions for commercial fleets.

Conclusion

The Global CNG Powertrain Market is entering a sustained growth phase anchored by regulatory momentum, rising fuel-cost sensitivity, and accelerating OEM participation. With the market forecast to expand from USD 100.7 Billion in 2024 to USD 479.9 Billion by 2034 at a CAGR of 16.9%, stakeholders across the automotive, energy, and infrastructure sectors face a significant opportunity to capture value in the clean-mobility transition.

As infrastructure expands, technology matures, and policy frameworks align, CNG powertrains are positioned to serve as a practical, scalable bridge between conventional combustion systems and the emerging hydrogen and fully electrified future. Organizations that move decisively now — through investment in OEM partnerships, refueling network development, and next-generation engine platforms — stand to define the competitive landscape of this fast-evolving market.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)