Market Overview

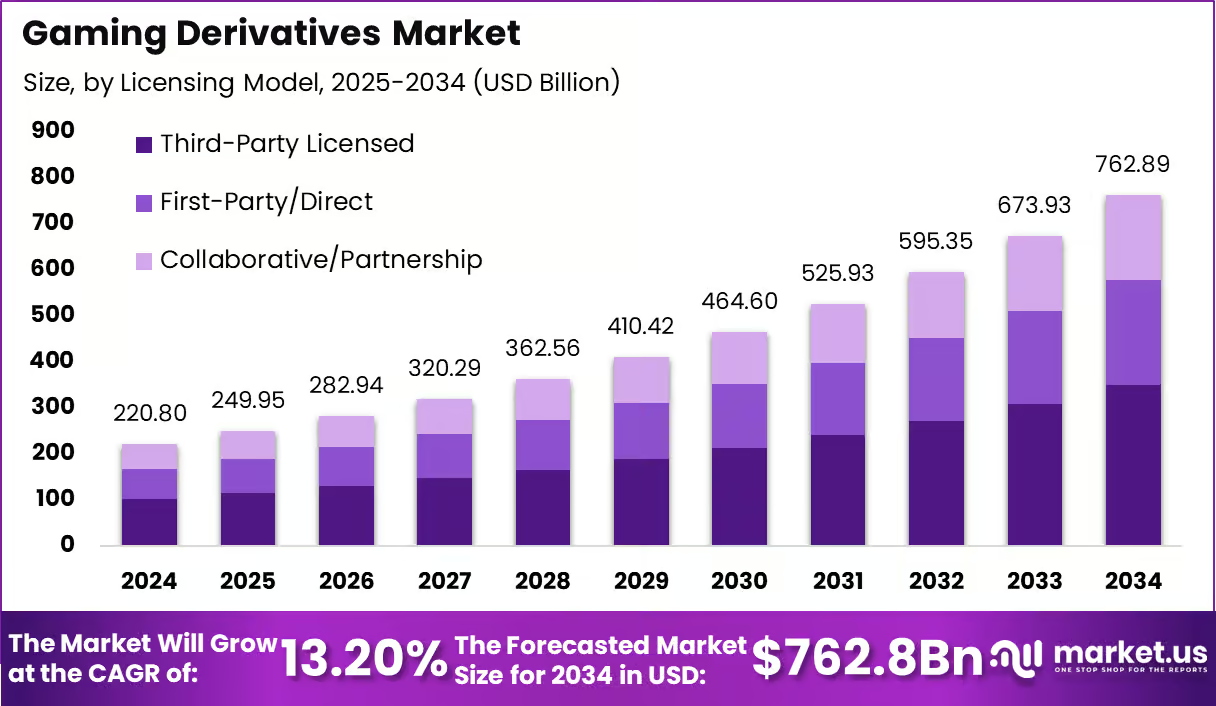

The Gaming Derivatives Market is expanding strongly as gaming intellectual property continues to create value beyond core gameplay through digital goods, licensed merchandise, collectibles, and fan-driven virtual assets. The market stands at USD 220.8 billion in 2024 and is projected to reach USD 762.8 billion by 2034, reflecting a CAGR of 13.2%.

Growth is being supported by deeper fan engagement, stronger franchise ecosystems, and rising spending on in-game and licensed experiences. Digital Goods & Assets lead the product mix, while Third-Party Licensed models remain important for scale. Casual Gamers & Fans drive demand, showing the market’s broad and highly commercial consumer base.

Key Takeaways

- Market size in 2024: USD 220.8 billion

- Projected market size by 2034: USD 762.8 billion

- CAGR: 13.2%

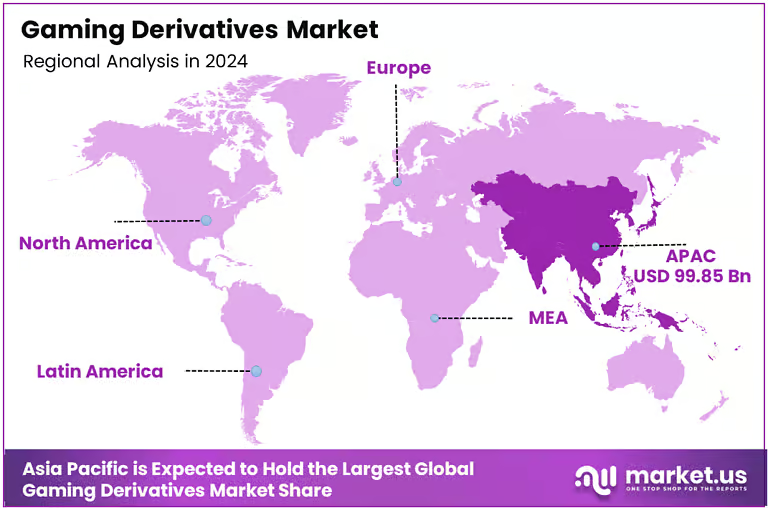

- Asia-Pacific share: 45.1%

- Asia-Pacific value in 2024: USD 99.85 billion

- China market value in 2024: USD 38.04 billion

- China projected value by 2034: USD 192.4 billion

- China CAGR: 17.6%

- Leading product type: Digital Goods & Assets at 54.2%

- Leading licensing model: Third-Party Licensed at 45.8%

- Leading end-user: Casual Gamers & Fans at 60.4%

Role of AI

AI is becoming a valuable layer in the Gaming Derivatives Market by improving personalization, pricing, content recommendations, fraud detection, and user engagement. It helps platforms understand player behavior, identify spending patterns, and offer more relevant digital goods, skins, collectibles, and promotional bundles.

In licensing and merchandising, AI supports demand forecasting and inventory planning by reading fan preferences across regions and genres. It also improves moderation in user-driven digital economies and helps detect counterfeit or suspicious asset activity. As gaming ecosystems become more data-led, AI is strengthening monetization efficiency and helping publishers, platforms, and rights holders create more targeted derivative offerings for wider audiences.

Analyst’s Viewpoint

The Gaming Derivatives Market is no longer a side extension of the gaming industry. It has become a major commercial layer built around fan identity, digital ownership, and brand loyalty. The dominance of Digital Goods & Assets shows that users increasingly value virtual extensions of gaming experiences as much as physical ones.

The strong share of Casual Gamers & Fans also shows that demand is not limited to hardcore players. Asia-Pacific’s leadership reflects a powerful mix of mobile gaming culture, franchise popularity, and digitally active consumers. In our view, the market is expected to remain highly attractive as game worlds continue to evolve into broader consumer ecosystems.

Regional Highlights

Asia-Pacific holds the leading position in the Gaming Derivatives Market with a 45.1% share and a 2024 value of USD 99.85 billion. The region benefits from a large gaming population, high mobile usage, strong community participation, and deep consumer interest in character-driven franchises and digital purchases.

China remains one of the most influential country-level markets, valued at USD 38.04 billion in 2024 and projected to reach USD 192.4 billion by 2034 at a CAGR of 17.6%. This growth reflects strong consumer demand, active game ecosystems, and expanding monetization across digital goods, licensed products, and fan-centered experiences tied to popular titles and brands.

Key Market Segmentation

- By Product Type: Digital Goods & Assets lead with 54.2% as players increasingly spend on virtual items, skins, collectibles, and game-linked content.

- By Licensing Model: Third-Party Licensed models account for 45.8% because they allow wider commercialization through brand partnerships and external distribution channels.

- By End-User: Casual Gamers & Fans dominate with 60.4%, showing that gaming derivative spending is now driven by mainstream entertainment behavior.

Emerging Trends

- Rising demand for virtual collectibles tied to gaming franchises

- Growth of cross-platform fan economies linked to game identities

- Higher use of limited-edition digital assets to drive engagement

- Expanding collaboration between game brands and lifestyle products

- Stronger localization of derivative offerings for regional audiences

Top Use Cases

- In-game skins, upgrades, and digital accessories

- Franchise-based collectibles and fan merchandise

- Licensed apparel and character-themed consumer goods

- Event-linked promotional items and digital drops

- Community reward systems tied to player engagement

Major Challenges

- Counterfeit and unauthorized derivative products

- Demand volatility tied to short franchise life cycles

- Licensing complexity across multiple territories

- Balancing monetization with player trust

- Regulatory uncertainty around digital ownership models

Attractive Opportunities

- Expansion of premium digital collectible ecosystems

- Growth in franchise licensing beyond core gaming channels

- Rising demand from casual and mainstream fan communities

- Strong monetization potential in Asia-Pacific markets

- Development of personalized derivative bundles using player data

Business Benefits

Gaming derivatives create meaningful business value by extending monetization beyond direct game sales and subscriptions. They help publishers and brand owners increase customer lifetime value, deepen engagement, and build stronger emotional attachment to franchises. Digital goods often offer faster scalability and better margin structures than traditional physical formats, while licensed products improve brand visibility across retail and online channels.

These derivatives also support community building by giving fans more ways to express identity and loyalty. For businesses, this market creates recurring revenue opportunities, lowers reliance on one-time title launches, and strengthens the long-term commercial potential of successful gaming intellectual property.

Recent Developments

Recent market activity has focused on expanding digital asset portfolios, building stronger franchise licensing partnerships, and increasing region-specific fan merchandise offerings. Companies are also improving direct-to-consumer channels and using player behavior insights to shape more targeted derivative products that align with community demand and monetization goals.

Key Players Analysis

The market is shaped by companies that manage strong gaming intellectual property, effective licensing networks, digital distribution strength, and active fan communities. Competitive advantage depends on franchise depth, monetization strategy, merchandising reach, and the ability to convert player engagement into long-term derivative revenue across both virtual and physical formats.

Top Key Players in the Market

- Tencent Holdings

- CME Group Inc.

- Eurex Frankfurt AG

- Intercontinental Exchange, Inc.

- Shanghai Futures Exchange

- Dalian Commodity Exchange

- Cboe Global Markets, Inc.

- China Financial Futures Exchange

- Hong Kong Exchanges and Clearing Limited

- Singapore Exchange Limited

- Zhengzhou Commodity Exchange

- Others

Customer Insights

Customer behavior in this market shows that buyers are driven by identity, fandom, exclusivity, and connection to game worlds. Casual Gamers & Fans form the largest segment because derivative purchases often come from emotional affinity rather than gameplay need alone. Many buyers prefer digital goods because they offer instant access, lower friction, and direct in-game relevance.

Others are drawn to licensed merchandise that reflects community belonging and collectible appeal. Purchasing preferences vary by age, platform usage, franchise loyalty, and spending intent. This makes segmentation highly behavior-based, with different customer groups responding to convenience, rarity, aesthetics, social visibility, and brand attachment in distinct ways.

Future Outlook

The future of the Gaming Derivatives Market remains highly promising as gaming continues to expand into a broader cultural and commercial ecosystem. Demand is expected to rise as players and fans seek more ways to interact with gaming brands through digital goods, collectibles, merchandise, and licensed experiences.

Asia-Pacific is likely to remain the largest regional hub, while China is expected to deliver especially strong growth. Digital derivatives are anticipated to stay at the center of market expansion because they scale quickly and align with changing consumption habits. Over time, stronger personalization, licensing sophistication, and franchise-led engagement are expected to push the market into a more mature and valuable phase.

Conclusion

The Gaming Derivatives Market is positioned as a major growth engine within the wider gaming economy. With the market projected to rise from USD 220.8 billion in 2024 to USD 762.8 billion by 2034, the outlook remains strong. Asia-Pacific leads global demand, while China stands out as a fast-growing national market.

The dominance of Digital Goods & Assets, Third-Party Licensed models, and Casual Gamers & Fans highlights how the market is being shaped by scalable digital consumption and broad audience participation. Overall, gaming derivatives are becoming central to franchise monetization, customer engagement, and long-term value creation across the global interactive entertainment landscape.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)