Table of Contents

Overview

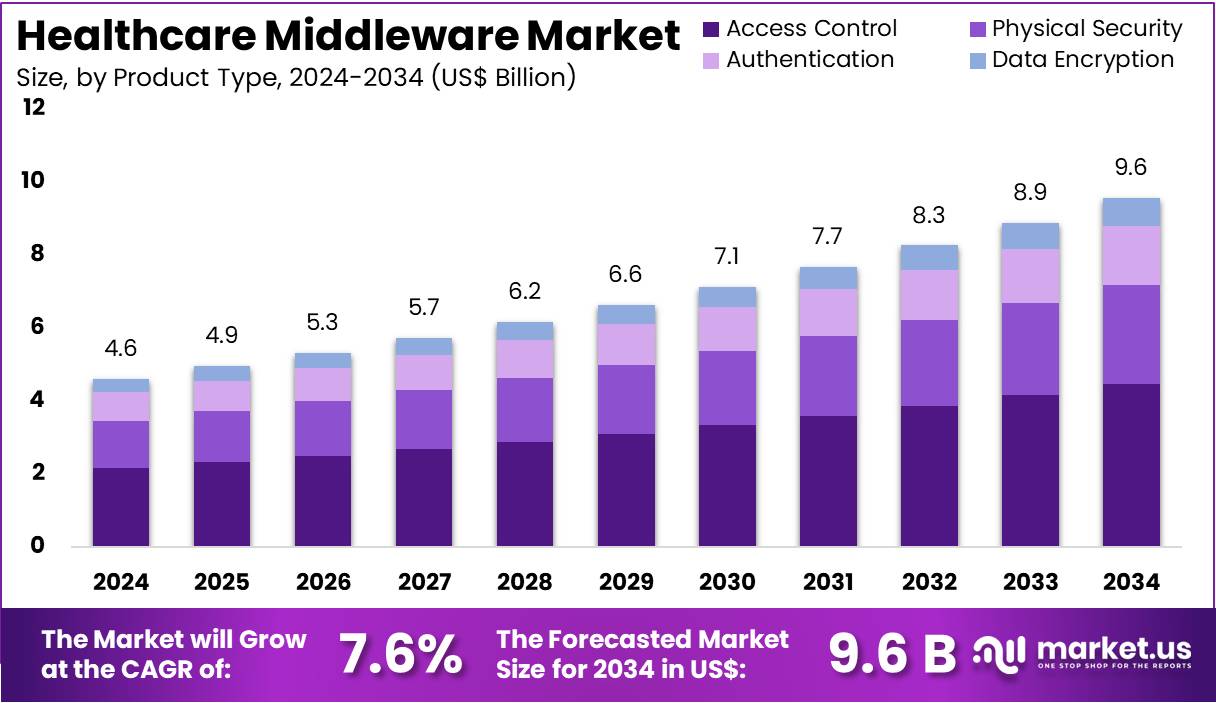

New York, NY – April 23, 2026 – The Healthcare Middleware Market Size is expected to be worth around US$ 9.6 Billion by 2034 from US$ 4.6 Billion in 2024, growing at a CAGR of 7.6% during the forecast period 2025 to 2034.

Healthcare middleware refers to software that enables seamless communication and data exchange between diverse healthcare systems, applications, and devices. It acts as an integration layer, connecting electronic health records (EHRs), laboratory systems, imaging platforms, and wearable devices to ensure interoperability across healthcare ecosystems.

The adoption of healthcare middleware has been driven by the increasing need for real-time data accessibility, improved patient outcomes, and operational efficiency. It facilitates standardized data exchange using protocols such as HL7 and FHIR, reducing fragmentation and enabling coordinated care delivery. Additionally, middleware supports secure data transmission, ensuring compliance with regulatory frameworks and data privacy standards.

Market growth is supported by the rising digitization of healthcare infrastructure and the expansion of telehealth services. Healthcare providers are increasingly relying on middleware solutions to integrate legacy systems with modern cloud-based platforms. This integration enhances clinical decision-making by providing unified patient data and analytics capabilities.

Furthermore, the demand for middleware is strengthened by the growing adoption of Internet of Medical Things (IoMT) devices, which require efficient data integration and management. North America and Europe currently represent significant market shares, while emerging economies are witnessing accelerated adoption due to healthcare modernization initiatives.

Overall, healthcare middleware is positioned as a critical enabler of connected healthcare, supporting data-driven and patient-centric care models.

Key Takeaways

- In 2024, the healthcare middleware market generated revenue of US$ 4.6 billion and is projected to reach US$ 9.6 billion by 2034, expanding at a CAGR of 7.6%.

- Based on product type, the market is segmented into physical security, access control, authentication, and data encryption, with access control dominating the segment with a 46.7% share in 2024.

- By technology, the market is categorized into cloud-based, on-premise, and hybrid solutions, where cloud-based deployments accounted for the largest share of 53.2%.

- In terms of application, the market includes clinical integration, patient management, enterprise resource planning, and data analytics, with patient management leading at 44.3% revenue share.

- Based on format, the segmentation comprises health level 7 (HL7), fast healthcare interoperability resources (FHIR), and digital imaging and communications in medicine (DICOM), with HL7 holding the leading share of 49.1%.

- By end-user, the market is divided into hospitals & clinics, pharmaceutical companies, insurance companies, and healthcare providers, with hospitals & clinics accounting for a dominant 57.8% share.

- Regionally, North America emerged as the leading market, capturing a 53.2% share in 2024.

Regional Analysis

North America accounted for the largest share of the healthcare middleware market, supported by the growing demand for efficient data exchange and interoperability across healthcare IT systems. Regulatory initiatives led by the US Department of Health & Human Services and the Office of the National Coordinator for Health Information Technology have strengthened the adoption of standardized data-sharing frameworks. Additionally, the widespread implementation of Electronic Health Records (EHRs) across hospitals has increased the need for middleware solutions to enable seamless system integration and coordinated patient care.

Asia Pacific is projected to register the fastest CAGR during the forecast period. Growth is being driven by rising investments in digital health infrastructure and increasing government focus on integrated healthcare systems. The expansion of hospitals, along with growing EHR adoption and development of health information exchange platforms, is expected to accelerate demand for middleware solutions that support efficient communication and data interoperability across healthcare networks.

Emerging Trends

- Shift toward cloud-based deployment: Cloud adoption is increasing, with nearly 50% of healthcare workloads expected on cloud platforms by 2027, improving scalability, reducing IT cost, and enabling faster deployment of middleware solutions.

- Growing focus on interoperability standards: Standards like HL7 and FHIR are widely adopted, with over 60% of systems aligning to FHIR, improving data exchange across hospitals and digital platforms.

- Integration of AI and automation: AI-enabled middleware adoption is rising by nearly 25–30% annually, supporting automated workflows, predictive analytics, and improved clinical decision-making across healthcare IT systems.

- Expansion of connected medical devices (IoMT): The number of connected devices is expected to exceed 50 billion globally by 2030, increasing reliance on middleware for secure, real-time data transfer and device interoperability.

Key Use Cases

- EHR system integration: Middleware connects fragmented EHR platforms, enabling unified patient records. With over 80% hospital adoption, seamless integration is essential for efficient clinical workflows and data accuracy.

- Real-time patient data exchange: Middleware supports instant communication between labs, imaging systems, and clinicians, reducing diagnosis time and improving treatment outcomes in high-dependency care environments.

- Telehealth and remote monitoring systems: More than 35–40% of healthcare providers use telehealth services, where middleware ensures secure transmission of patient data between devices, applications, and healthcare professionals.

- Healthcare administration and billing integration: Middleware streamlines billing, claims processing, and scheduling systems, improving operational efficiency, with administrative automation reducing processing time by nearly 20–30% in hospitals.

Frequently Asked Questions on Healthcare Middleware

- What are the key drivers of the healthcare middleware market?

Market growth is primarily driven by rising adoption of electronic health records, increasing demand for real-time data exchange, expansion of telehealth services, and the need for interoperability among diverse healthcare IT infrastructures across hospitals and healthcare providers. - Which technologies are commonly used in healthcare middleware?

Healthcare middleware commonly utilizes cloud-based, on-premise, and hybrid technologies, along with interoperability standards such as HL7 and FHIR, to enable secure, scalable, and efficient integration of healthcare data across multiple platforms and applications. - What are the major applications of healthcare middleware?

Key applications include clinical integration, patient management, enterprise resource planning, and data analytics, with patient management systems holding significant importance due to their role in improving care coordination and enhancing patient outcomes across healthcare settings. - Who are the primary end-users of healthcare middleware solutions?

Primary end-users include hospitals and clinics, pharmaceutical companies, insurance providers, and other healthcare organizations, with hospitals leading adoption due to their complex IT environments and the need for seamless integration across multiple clinical systems. - Which regions dominate the healthcare middleware market?

North America currently dominates the market due to advanced healthcare infrastructure, high adoption of digital health technologies, and supportive regulatory frameworks, while Asia Pacific is expected to witness rapid growth driven by increasing healthcare investments and digital transformation initiatives. - What are the future trends in the healthcare middleware market?

Future trends include increasing adoption of cloud-based integration platforms, growing use of artificial intelligence in data management, expansion of Internet of Medical Things devices, and rising focus on interoperability standards to enable connected and patient-centric healthcare ecosystems.

Conclusion

Healthcare middleware is positioned as a foundational component in modern healthcare IT ecosystems, enabling seamless interoperability, real-time data exchange, and improved care coordination. Market expansion is being supported by increasing EHR adoption, rapid digital transformation, and the proliferation of connected medical devices.

Cloud-based deployments and AI-driven integration capabilities are enhancing scalability, efficiency, and decision-making processes. While North America maintains market leadership, Asia Pacific is emerging as a high-growth region due to infrastructure investments. Overall, sustained demand for integrated, secure, and patient-centric systems is expected to drive steady market growth and innovation over the forecast period.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)