Table of Contents

Introduction

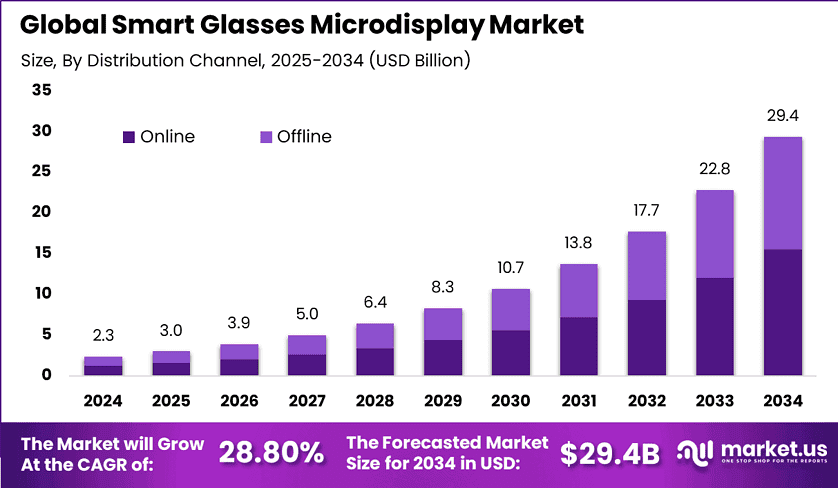

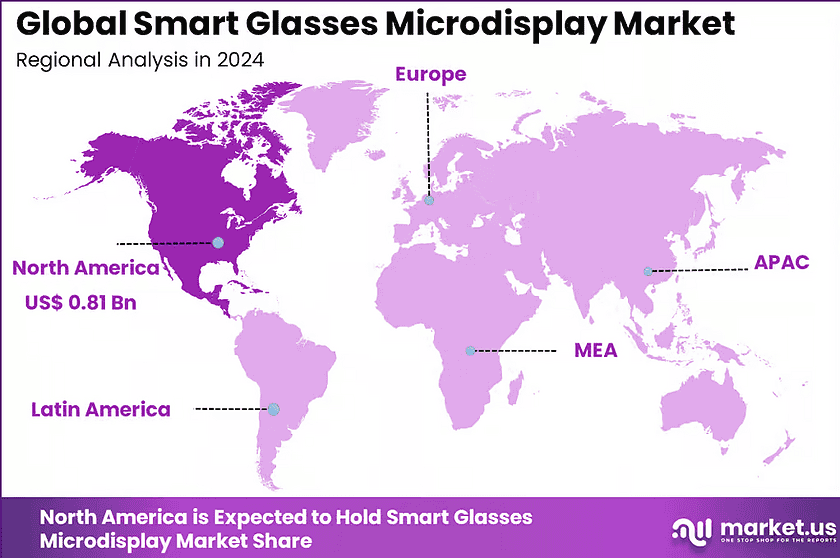

The Global Smart Glasses Microdisplay Market generated USD 2.3 billion in 2024 and is predicted to register growth from USD 3.0 billion in 2025 to about USD 29.4 billion by 2034, recording a CAGR of 28.80% throughout the forecast span. In 2024, North America held a dominan market position, capturing more than a 34.8% share, holding USD 0.81 Billion revenue.

Smart glasses microdisplays are compact display components used inside wearable glasses to project digital information directly in the user’s field of view. These microdisplays enable functions such as navigation guidance, notifications, augmented overlays, and real time data visualization without the need to look at a separate screen.

They are designed to be lightweight, energy efficient, and capable of delivering clear visuals in different lighting conditions. As wearable technology continues to evolve, microdisplays are becoming a key element in making smart glasses practical for everyday and professional use.

One of the main driving factors is the growing interest in hands free digital interaction across industries. Workers in fields such as manufacturing, logistics, healthcare, and maintenance require quick access to information while keeping their hands free, which is driving adoption of smart glasses.

In addition, the expansion of augmented reality applications is increasing demand for high quality microdisplays that can deliver sharp images and smooth visuals. The push toward smaller and more efficient electronic components is also supporting innovation in display technology. Improvements in brightness, resolution, and power efficiency are further making these displays suitable for long term use.

Demand for smart glasses microdisplays is rising as companies and consumers look for more immersive and convenient ways to access digital content. There is a strong preference for displays that offer high clarity, low power consumption, and compact design that fits comfortably into wearable devices.

Manufacturers are also seeking solutions that can perform well in both indoor and outdoor environments without compromising visibility. The demand is particularly strong in enterprise applications where productivity and real time information are critical, as well as in emerging consumer use cases. As wearable devices gain wider acceptance, the need for advanced and reliable microdisplay technology is expected to grow steadily.

Top Keytake aways

- Display Technology OLED accounts for 37.4% of the Smart Glasses Microdisplay market, as it offers high contrast, rich colors, and low power consumption suitable for wearable displays.

- End-User Enterprises make up 67.8% of demand, because businesses use smart glasses for tasks like remote assistance, field service, logistics, and industrial training.

- Distribution Channel Online channels represent 52.7% of the market, reflecting the growing use of e-commerce platforms and direct online sales for smart glasses solutions.

- Region North America holds 34.8% of the global market, supported by strong enterprise adoption of AR and wearable technologies.

- Country The U.S. market is valued at 0.69 billion and is expected to grow at a CAGR of 25.2%, driven by digital transformation initiatives and increasing use of smart glasses in enterprise workflows.

How AI is Reshaping the Future of this market?

AI is reshaping the Smart Glasses Microdisplay Market by making smart glasses more useful for daily tasks instead of only showing basic alerts. With AI, smart glasses can support real-time translation, object recognition, voice assistance, navigation guidance, meeting notes, and hands-free search. These use cases need clear, bright, and power-efficient microdisplays that can show text, symbols, and visual prompts without disturbing the user’s view. This is increasing the importance of Micro OLED, LCoS, and other compact display technologies that can fit into lightweight eyewear.

AI is also changing product design in this market. Smart glasses now need displays that work smoothly with cameras, sensors, processors, and voice systems. The display must respond quickly, remain visible in outdoor conditions, and consume less battery during continuous AI-assisted use. As more brands focus on practical AI features, microdisplay suppliers are expected to improve resolution, brightness, contrast, and heat management while keeping the display module thin and comfortable for long wear.

In the future, AI is expected to make microdisplay quality one of the main factors in smart glasses adoption. Users will prefer glasses that provide useful information in a natural way without feeling heavy, distracting, or difficult to read. This will create stronger demand from consumer electronics, enterprise training, healthcare support, field service, logistics, and industrial maintenance. Overall, AI is turning the Smart Glasses Microdisplay Market into a more experience-driven space where display performance, low power use, and real-time intelligence become central to product success.

Regional Analysis

In 2024, North America held a dominant Market position, capturing more than a 34.8% share, holding USD 0.81 Billion revenue and why only North America leading is mainly linked to its strong early adoption of AR, VR, and mixed reality devices across enterprise, healthcare, defense, education, and consumer technology applications.

The region has a well-developed smart wearable ecosystem, strong demand for compact display solutions, and higher spending capacity among technology users. Smart glasses microdisplays are gaining wider use in hands-free workflows, remote assistance, medical visualization, field service operations, and industrial training, which supports stronger adoption in North America compared to other regions.

The US plays a central role in North America’s leadership due to its advanced semiconductor base, strong presence of AR hardware developers, rising investment in optical display technologies, and faster commercialization of smart glasses for both enterprise and consumer use.

Companies in the region are focusing on lightweight designs, higher brightness, better power efficiency, and improved image clarity, which are key requirements for microdisplays used in smart glasses. Demand is also supported by growing interest in AI-enabled wearable devices, where microdisplays act as a core interface for real-time visual guidance, notifications, navigation, and contextual information.

Europe is expected to show steady growth due to rising adoption of smart glasses in manufacturing, automotive, logistics, and medical training applications. Latin America is gradually adopting smart wearable technologies, although cost sensitivity and limited local production slow down wider penetration.

The Middle East and Africa market is still emerging, supported by digital transformation programs, smart city projects, and enterprise modernization. However, North America remains ahead because of stronger technology infrastructure, higher R&D activity, faster enterprise adoption, and deeper integration of smart glasses into commercial and industrial workflows.

Driver

Growing demand for compact visual computing

The smart glasses microdisplay market is being driven by rising demand for lightweight visual devices that can deliver information directly in the user’s field of view. Industries are adopting smart glasses to support hands free work, remote guidance, training, navigation, and real time data access.

Microdisplays are important because they define image clarity, brightness, power use, and comfort. As users expect sharper visuals in smaller eyewear designs, demand is increasing for advanced microdisplay solutions that support better viewing quality without making the glasses bulky.

Restraint

High development and integration cost

A major restraint in the market is the high cost involved in designing compact, bright, and energy efficient microdisplays. Smart glasses need displays that are small, clear, durable, and suitable for long use, which makes product development technically difficult.

Cost pressure also affects adoption among price sensitive users and businesses. When smart glasses remain expensive, buyers delay large scale use, especially in sectors where return on investment needs to be clearly proven before deployment.

Opportunity

Wider use in enterprise and healthcare applications

A strong opportunity exists in enterprise, healthcare, logistics, and field service applications. These sectors need hands free access to instructions, records, visual assistance, and live communication, making smart glasses useful for improving worker efficiency and reducing errors.

Microdisplay suppliers can benefit by focusing on displays that offer better brightness, lower power consumption, and improved outdoor readability. As professional use cases become more practical, demand for reliable and comfortable display systems is expected to strengthen.

Challenge

Balancing performance with user comfort

One key challenge is balancing display performance with comfort, battery life, and device weight. A smart glasses display must be bright and sharp, but it should also consume low power and fit into a slim frame without causing heat or eye strain.

This creates a complex design challenge for manufacturers. If the display quality is strong but the device feels heavy or uncomfortable, users may not continue using it for long periods, which can slow market acceptance.

Key Market Segment

By Display Technology

- OLED

- LCD

- LCoS

- DLP

- MicroLED

- Others

By End-User

- Enterprises

- Consumer Electronics

- Healthcare

- Industrial

- Military & Defense

- Sports & Fitness

- Others

- Individuals

By Distribution Channel

- Online

- Offline

Competetive Analysis

The competitive landscape of the Smart Glasses Microdisplay Market is driven by strong participation from display manufacturers and semiconductor companies. Companies such as Sony Corporation, Samsung Electronics Co., Ltd., LG Display Co., Ltd., BOE Technology Group Co., Ltd., AU Optronics Corp., and Innolux Corporation focus on advanced display technologies including OLED, microLED, and LCD-based microdisplays.

These players invest in improving resolution, brightness, and power efficiency to support augmented reality and wearable applications. Their large-scale manufacturing capabilities and strong supply chains help them maintain a leading position in the market.

At the same time, companies such as Kopin Corporation, Himax Technologies, Inc., Microoled, eMagin Corporation, Seiko Epson Corporation, Jade Bird Display (JBD), Lumus Ltd., Vuzix Corporation, Syndiant, Inc., Raontech Inc., WiseChip Semiconductor Inc., Plessey Semiconductors Ltd., Magic Leap, Inc., and Goertek Inc. compete by offering specialized microdisplay solutions and optical technologies tailored for smart glasses and AR devices.

These players focus on compact design, low power consumption, and high image quality. Competition in this market is driven by innovation in display performance, miniaturization, and the ability to support lightweight and high-performance wearable devices.

Top Key Players

- Sony Corporation

- Kopin Corporation

- Himax Technologies, Inc.

- Microoled

- Seiko Epson Corporation

- Jade Bird Display (JBD)

- BOE Technology Group Co., Ltd.

- eMagin Corporation

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- Lumus Ltd.

- Vuzix Corporation

- Syndiant, Inc.

- AU Optronics Corp.

- Innolux Corporation

- Raontech Inc.

- WiseChip Semiconductor Inc.

- Plessey Semiconductors Ltd.

- Magic Leap, Inc.

- Goertek Inc.

- Others

Recent Development

- April 2026, Kopin Corporation – Kopin announces a strategic collaboration with Fabric.AI to develop a MicroLED‑based optical‑interconnect technology for AI data centers, funded by a USD 15 million order; the company notes that the same MicroLED and NeuralDisplay know‑how was originally developed for AR/VR and smart‑glasses microdisplays.

- November 2025, Sony Corporation – Sony Semiconductor Solutions publishes information on high‑resolution and high‑luminance technologies for OLED microdisplays and liquid‑crystal microdisplays, aimed at next‑generation near‑eye devices such as AR/VR smart glasses.

Conclusion

The Smart Glasses Microdisplay Market is expected to grow steadily as demand rises for compact, clear, and energy efficient display solutions in wearable devices. Microdisplays are becoming an important part of smart glasses because they support better image quality, lightweight design, and improved user comfort. The market is gaining support from wider use in healthcare, enterprise training, industrial assistance, gaming, defense, and consumer applications.

At the same time, challenges such as high production cost, limited battery performance, and display integration issues may affect adoption in price sensitive markets. Overall, the market outlook remains positive as manufacturers focus on brighter displays, smaller form factors, and better compatibility with AI, AR, and connected device ecosystems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)