Table of Contents

Market Overview

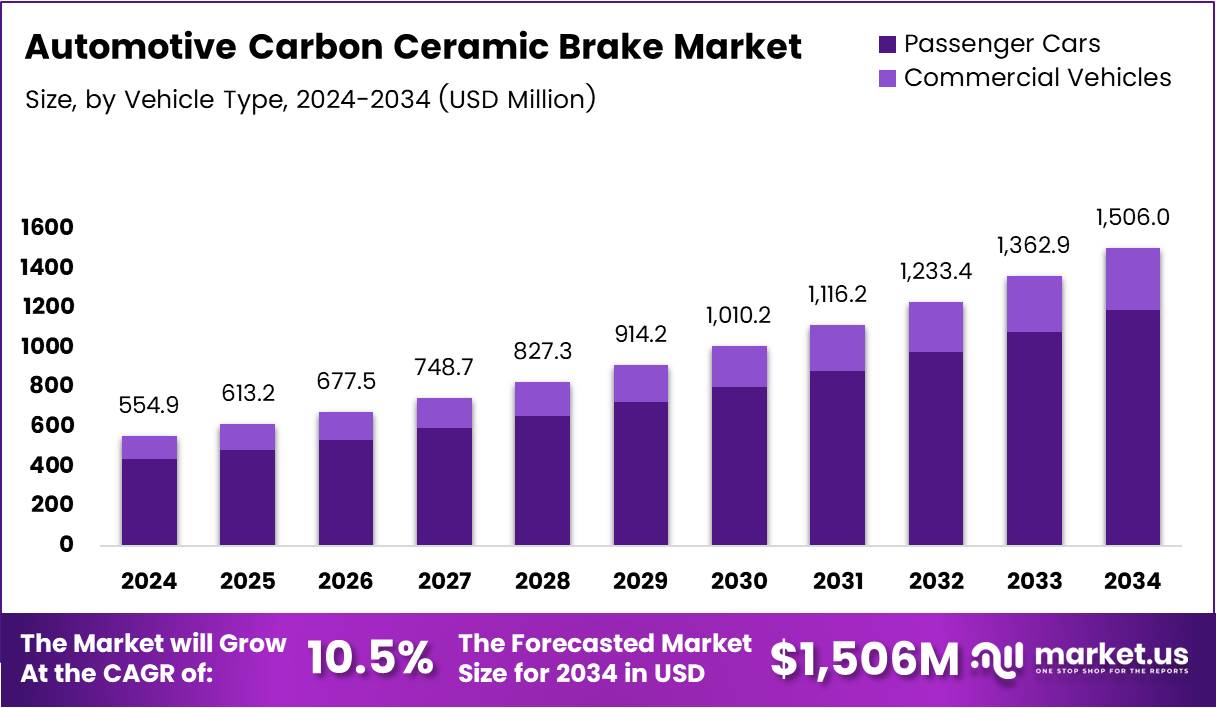

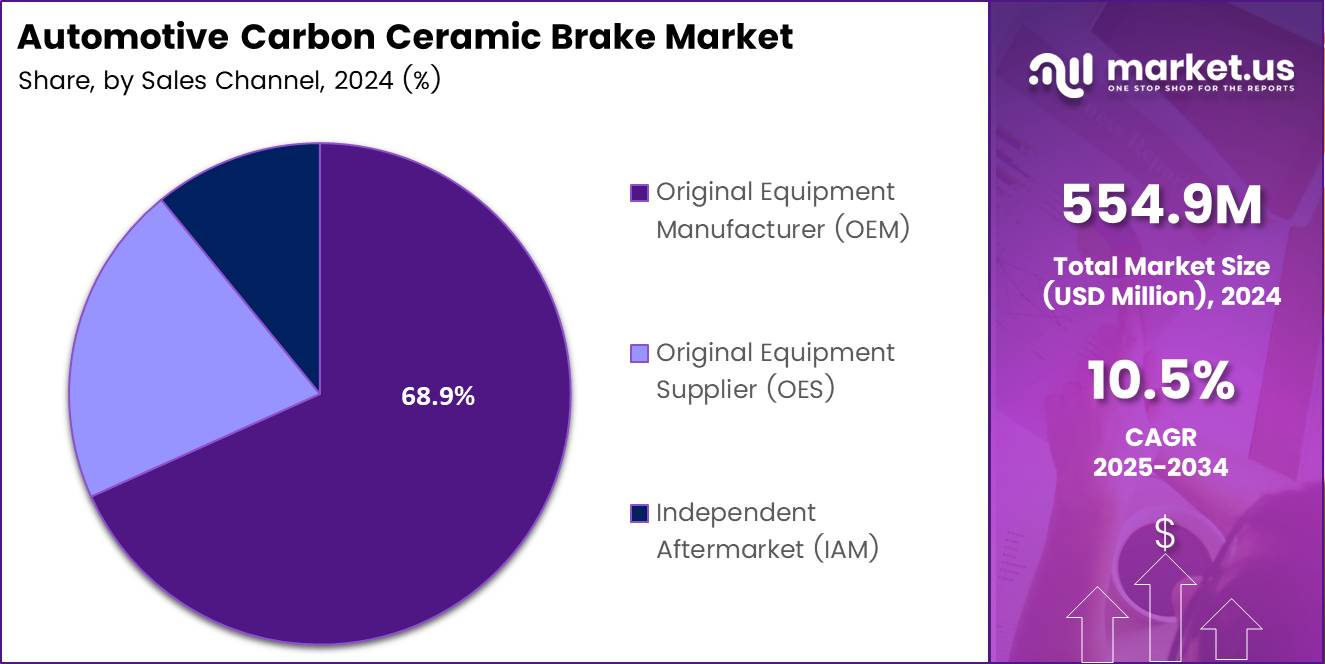

The global Automotive Carbon Ceramic Brake Market was valued at USD 554.9 Million in 2024 and is projected to reach USD 1506.0 Million by 2034. The market is expected to grow at a CAGR of 10.5% during the forecast period from 2025 to 2034. Rising demand for lightweight braking systems continues to support long-term industry expansion.

Automotive carbon ceramic brakes use advanced composite materials to improve stopping performance and thermal stability. Luxury vehicle manufacturers, sports car producers, and premium electric vehicle brands widely adopt these systems. These brakes reduce rotational weight and improve handling efficiency. Consequently, automakers increasingly position them as premium safety and performance upgrades.

Get further insight into the global trends shaping the future of the Automotive Carbon Ceramic Brake industry. Request Sample

Luxury automotive brands, motorsport companies, and electric vehicle manufacturers are major contributors to market demand. Performance vehicle makers use these brakes to improve driving precision during high-speed operations. Additionally, electric vehicle companies integrate lightweight brake systems to increase driving range and improve energy efficiency across premium mobility platforms.

Manufacturers continue integrating smart sensors and brake diagnostics into modern braking systems. Advanced monitoring technologies help track brake wear, temperature, and operational performance in real time. Consequently, predictive maintenance capabilities reduce unexpected repairs and improve vehicle safety. Companies also develop stronger composite materials to extend brake lifespan and reduce dust generation.

Government emission standards and vehicle efficiency regulations continue supporting advanced material adoption across the automotive industry. European automotive policies encourage lightweight vehicle development to reduce carbon emissions and improve fuel economy. Additionally, safety regulations promote advanced braking technologies that maintain performance under extreme conditions, encouraging automakers to expand carbon ceramic brake integration.

Industry reports state that PCCB carbon-ceramic discs are nearly 50% lighter than traditional cast-iron brake discs. This weight reduction improves vehicle handling and responsiveness while supporting energy efficiency. Furthermore, battery-electric vehicles reached a 13.6% market share in the European Union during 2024 and 16.1% by September 2025, increasing demand for lightweight automotive components.

Key Takeaways

- The global Automotive Carbon Ceramic Brake Market is projected to reach USD 1506.0 Million by 2034 from USD 554.9 Million in 2024.

- The market is expected to expand at a CAGR of 10.5% during the forecast period from 2025 to 2034.

- Passenger Cars dominated the vehicle type segment with a market share of 79.2% due to strong luxury vehicle demand.

- Original Equipment Manufacturer (OEM) channels led the sales category with a share of 68.9% through direct factory integration.

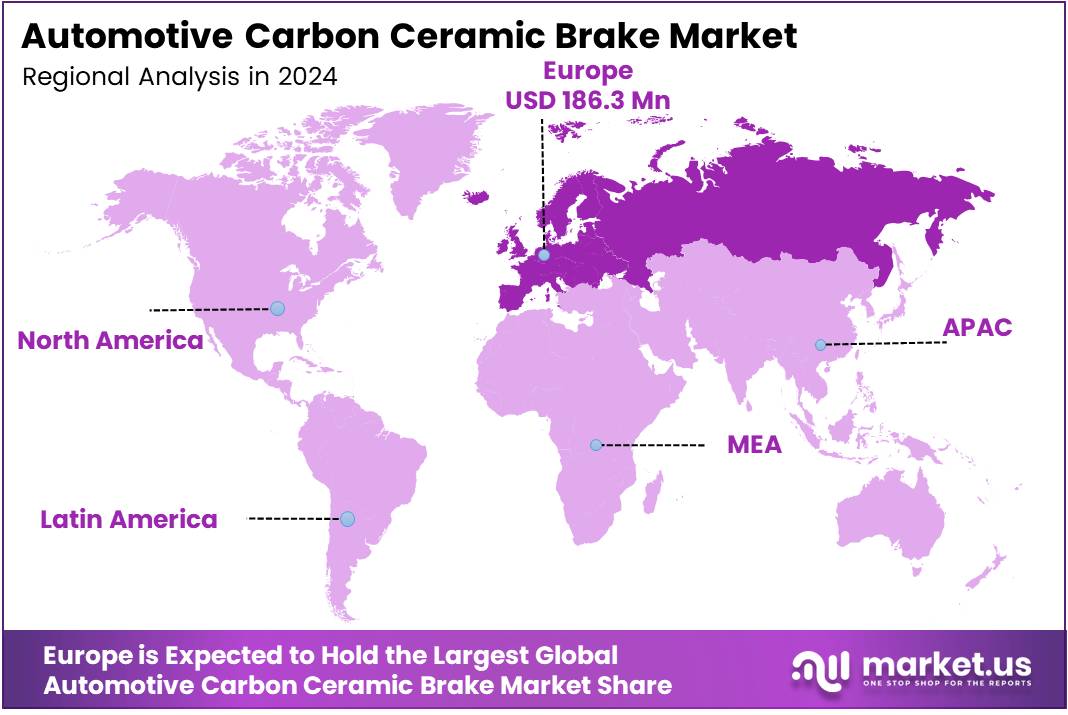

- Europe accounted for a leading regional share of 34.9%, valued at USD 193.6 Million in 2024.

- Rising electric vehicle adoption continues increasing demand for lightweight and thermally stable braking technologies worldwide.

Market Segmentation Overview

Passenger Cars dominated the Automotive Carbon Ceramic Brake Market with a share of 79.2% in 2024. Strong demand from luxury sedans, sports cars, and premium electric vehicles supported this leadership position. Manufacturers prioritize carbon ceramic systems because they improve braking precision, reduce weight, and enhance driving dynamics in performance-focused vehicle categories.

Commercial Vehicles continue witnessing gradual adoption due to increasing focus on durability and operational efficiency. Light commercial fleets and heavy-duty vehicles benefit from reduced brake wear and stable thermal performance during long-distance operations. Additionally, off-road vehicles increasingly use advanced braking systems to improve reliability under harsh environmental conditions.

Original Equipment Manufacturer channels held a dominant share of 68.9% in 2024 due to strong factory-level integration in premium vehicles. Automakers prefer OEM-installed braking systems because they ensure compatibility, safety validation, and higher resale value. Consequently, luxury vehicle buyers increasingly demand factory-certified performance braking technologies.

Original Equipment Supplier and Independent Aftermarket channels continue supporting replacement and customization demand across global markets. OES providers deliver certified replacement parts for high-value vehicles requiring precise performance standards. Meanwhile, aftermarket adoption grows steadily as vehicle enthusiasts seek premium braking upgrades for sports and performance-oriented driving applications.

Drivers

Growing demand for luxury and high-performance vehicles strongly drives the Automotive Carbon Ceramic Brake Market. Premium automakers require advanced braking systems that maintain stability during high-speed driving conditions. Consequently, manufacturers continue integrating carbon ceramic technologies into sports cars, supercars, and premium electric vehicles to improve safety and driving precision.

Rising focus on lightweight automotive components further accelerates market growth worldwide. Carbon ceramic brake systems reduce vehicle weight compared to traditional metal brakes, improving fuel efficiency and battery range. Additionally, automakers use lightweight braking materials to improve acceleration, handling performance, and energy recovery efficiency in modern electric vehicles.

Use Cases

Luxury automotive manufacturers use carbon ceramic brakes in sports sedans and supercars to improve high-speed braking performance. These systems maintain thermal stability during repeated braking cycles and reduce brake fade under demanding driving conditions. Consequently, premium vehicle brands strengthen driving safety while delivering superior handling and responsive driving experiences.

Electric vehicle manufacturers increasingly integrate carbon ceramic brakes into premium EV platforms to improve energy efficiency and durability. Lightweight brake systems reduce unsprung mass and support extended driving range during regular operation. Additionally, thermally stable braking technologies improve regenerative braking efficiency, supporting smoother energy recovery and long-term operational reliability.

Major Challenges

High manufacturing and installation costs continue limiting adoption across mass-market vehicle platforms. Economy vehicle manufacturers often avoid carbon ceramic systems because production expenses remain significantly higher than traditional brake technologies. Consequently, premium and luxury vehicle segments continue representing the primary customer base for advanced carbon ceramic braking solutions.

Specialized maintenance requirements create additional operational challenges for automotive service providers and vehicle owners. Carbon ceramic brake systems require trained technicians and dedicated repair equipment, increasing servicing expenses. Additionally, supply chain complexity for advanced carbon fibers and ceramic materials can disrupt production schedules and affect pricing stability.

Business Opportunities

Growing development of electric and hybrid sports vehicles creates strong opportunities for carbon ceramic brake manufacturers. Performance electric vehicles generate higher torque and frequent braking cycles, increasing demand for thermally stable brake systems. Consequently, suppliers that develop EV-specific braking technologies can strengthen partnerships with premium electric mobility brands.

Aftermarket customization trends also create new commercial opportunities across global automotive markets. Performance vehicle enthusiasts increasingly upgrade braking systems to improve aesthetics and driving precision. Additionally, luxury transport fleets and premium rental services adopt durable braking systems to reduce maintenance frequency and improve long-term operational reliability.

Regional Analysis

Europe dominated the Automotive Carbon Ceramic Brake Market with a share of 34.9%, valued at USD 193.6 Million in 2024. Germany, Italy, the United Kingdom, and France remain major contributors due to strong luxury vehicle production and advanced automotive engineering capabilities. Additionally, strict emission regulations encourage lightweight vehicle component adoption across the region.

Asia Pacific is emerging as a rapidly growing market due to rising disposable incomes and increasing demand for premium vehicles. China, Japan, South Korea, and India continue expanding automotive manufacturing capabilities across luxury and electric vehicle categories. Moreover, growing motorsport culture and aftermarket customization trends further support regional product penetration.

Recent Developments

- September 2025 — BREMBO S.p.A. expanded production capacity by nearly 50% at facilities in Italy and Germany to meet rising demand.

- October 2024 — BREMBO S.p.A. agreed to acquire Öhlins Racing of Sweden for US$405 million to strengthen integrated braking solutions.

- September 2024 — Brembo showcased aftermarket carbon-ceramic brake discs during Automechanika 2024 to expand adoption beyond OEM supercars.

- July 2025 — Surface Transforms secured undisclosed funding to improve carbon-ceramic brake material development and production scalability.

Conclusion

The Automotive Carbon Ceramic Brake Market continues showing strong long-term growth supported by rising luxury vehicle demand and increasing electric vehicle adoption. Automakers prioritize lightweight and thermally stable braking systems to improve performance, efficiency, and safety. Consequently, advanced carbon ceramic technologies are gaining broader acceptance across premium automotive segments.

Passenger Cars remain the dominant segment with a share of 79.2% due to strong integration in sports and luxury vehicles. OEM channels continue leading market sales through factory-installed braking technologies. Additionally, Europe maintains regional leadership with a market share of 34.9% supported by established automotive manufacturing infrastructure.

Manufacturers must focus on scalable production, advanced composite materials, and strategic OEM partnerships to capture future market opportunities. Companies that align product development with electric vehicle requirements and lightweight mobility trends will strengthen competitive positioning. The market is projected to reach USD 1506.0 Million by 2034.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)