Table of Contents

Market Overview

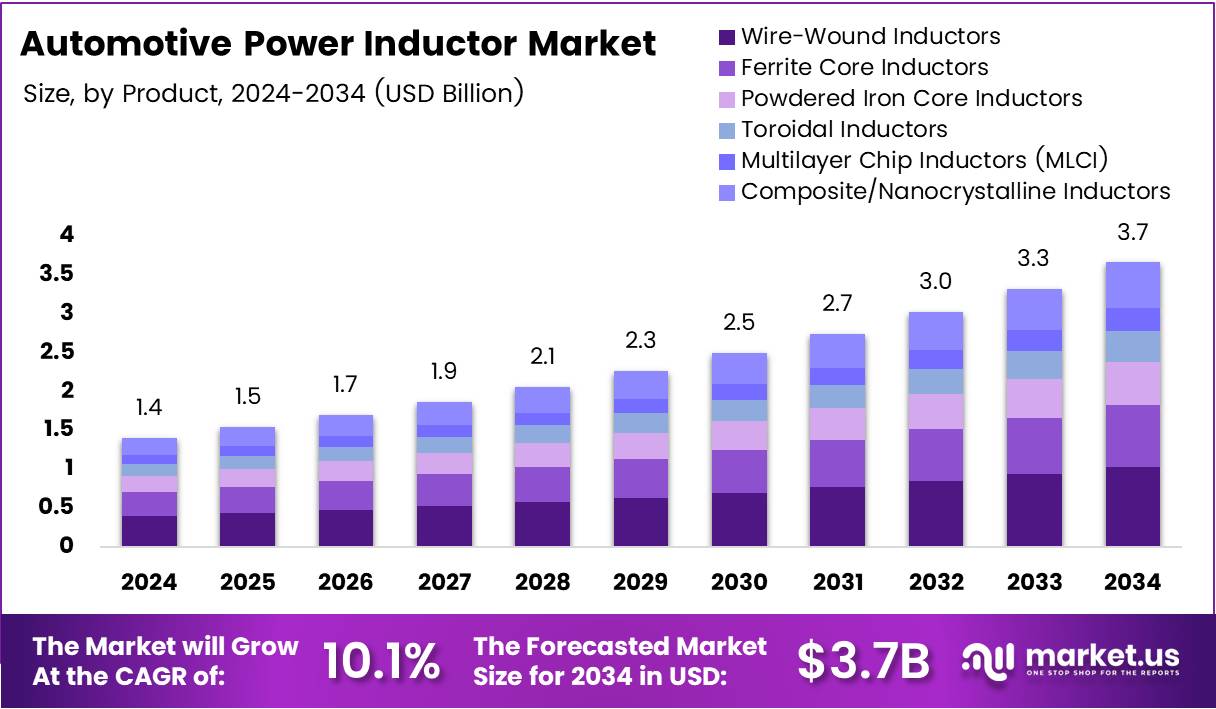

The global Automotive Power Inductor market was valued at USD 1.4 Billion in 2024. Analysts project the market will reach approximately USD 3.7 Billion by 2034, expanding at a CAGR of 10.1% during 2025–2034. Rising vehicle electrification and increasing electronic complexity continue driving strong demand for automotive-grade inductive components globally.

Automotive power inductors are electronic components that manage energy storage, filtering, and voltage regulation inside vehicle systems. Automakers use these inductors in electric drivetrains, onboard chargers, ADAS modules, infotainment systems, and battery-management units. Consequently, advanced inductors help improve energy efficiency, thermal stability, and operational reliability in modern vehicles.

Get further insight into the global trends shaping the future of the Automotive Power Inductor industry. Request Sample

Automotive OEMs increasingly deploy power inductors across electric vehicles, hybrid systems, and connected mobility platforms. Manufacturers integrate these components into DC-DC converters, fast-charging systems, and advanced powertrain electronics. Additionally, rising adoption of autonomous driving technologies and digital infotainment solutions continues strengthening demand for efficient power-management components.

Technology innovation continues improving automotive power inductors through miniaturization, high-frequency switching, and advanced semiconductor integration. Manufacturers increasingly develop compact inductors with better thermal resistance and higher current-handling capability. Moreover, wide-bandgap semiconductor technologies such as SiC and GaN continue accelerating demand for high-performance inductive components across EV architectures.

Government initiatives supporting electric mobility and emission reduction continue boosting market growth worldwide. Regulatory authorities increasingly encourage clean-energy transportation through EV incentives, charging-network investments, and stricter emission standards. Therefore, automotive manufacturers rely on advanced inductors to support efficient power conversion, reduce electrical losses, and maintain stable system performance.

Industry research further confirms strong market potential for automotive power inductors. Research from 2023 shows a vehicle requires more than 100 power inductors, over twice the number used in smartphones. Additionally, electric car sales approached 14 million units in 2024, with 95% concentrated in China, Europe, and the United States, significantly increasing component demand.

Key Takeaways

- The Automotive Power Inductor market will grow from USD 1.4 Billion in 2024 to USD 3.7 Billion by 2034 at a CAGR of 10.1%.

- Wire-Wound Inductors dominate the product segment with a market share of 33.8% due to superior durability and current-handling performance.

- Ferrite materials lead the material segment with a share of 48.1% because of excellent magnetic efficiency and low energy losses.

- Surface-Mount (SMD) inductors account for 61.2% share as manufacturers prioritize compact and automated assembly designs.

- Low Inductance (1–10 µH) inductors captured 41.6% share due to strong adoption in switching circuits and power converters.

- High-Frequency Switching inductors lead the frequency segment with a share of 41.7% driven by fast-charging and EV power systems.

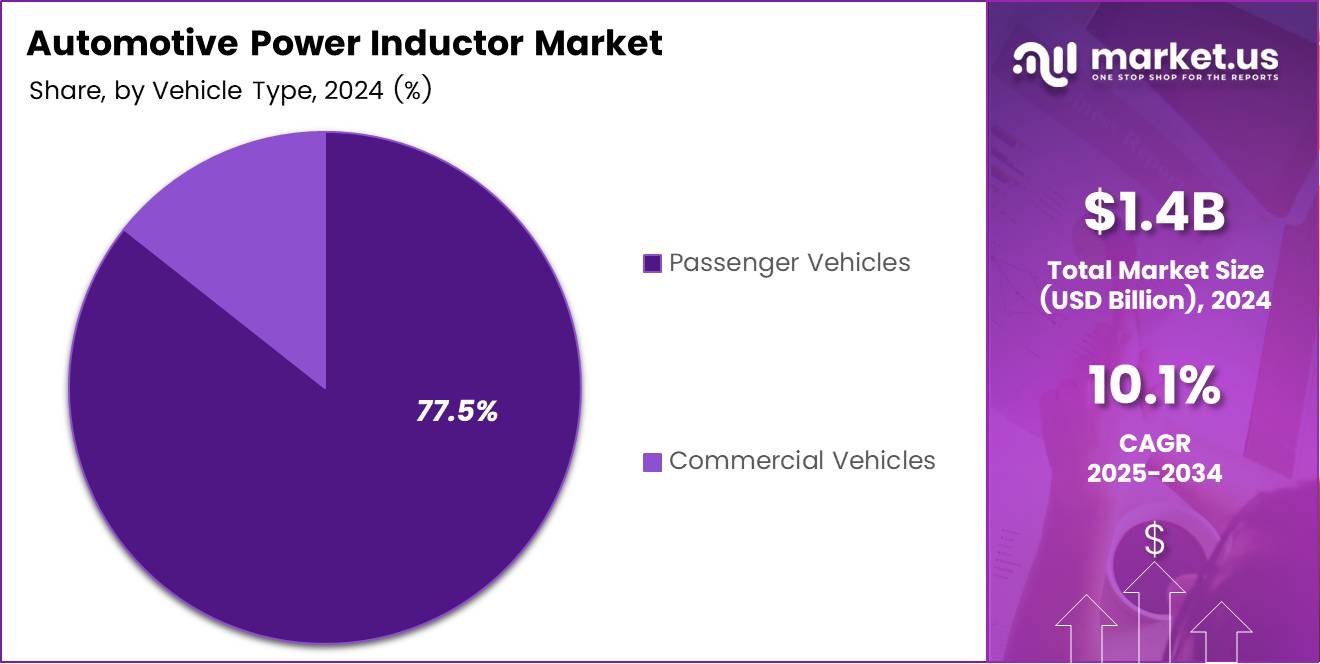

- Passenger Vehicles dominate the vehicle segment with 77.5% share, while OEMs represent 85.3% of end-user demand.

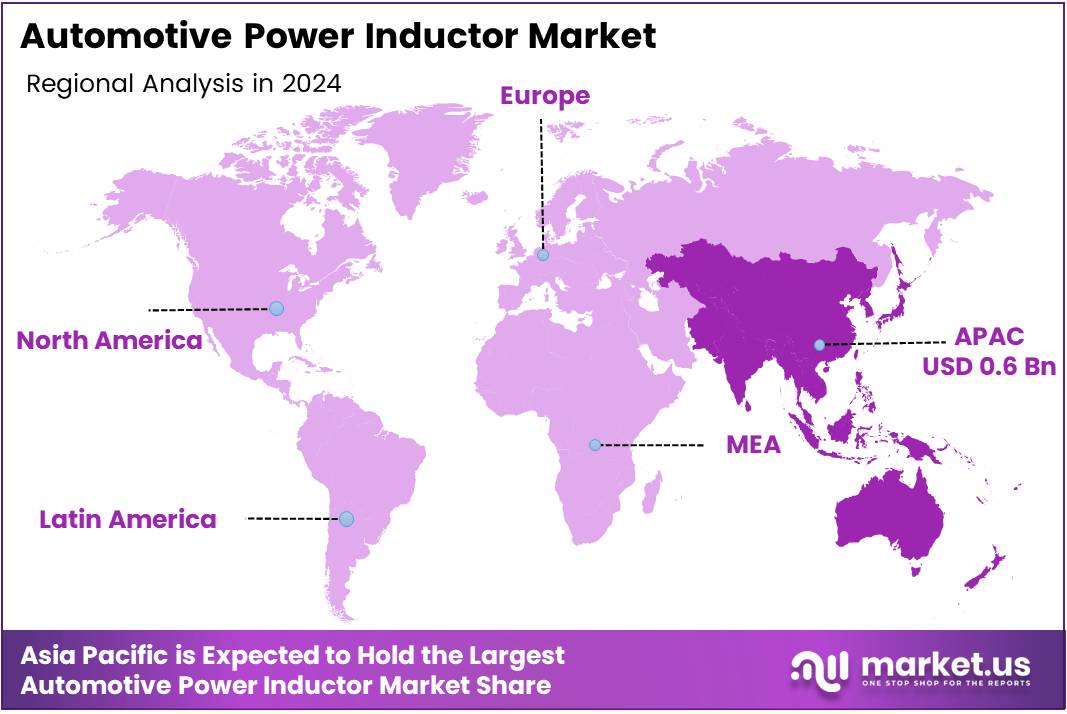

- Asia Pacific leads globally with a market share of 47.2%, reaching a regional value of USD 0.6 Billion.

Market Segmentation Overview

Wire-Wound Inductors held the leading product share of 33.8% in 2024. Automotive manufacturers increasingly prefer these inductors because they provide excellent current-handling capability, thermal stability, and long-term durability. Consequently, wire-wound designs support demanding EV powertrains, infotainment systems, and advanced onboard charging applications across modern vehicle platforms.

Ferrite Core, Powdered Iron Core, and Composite/Nanocrystalline inductors also generated strong market demand. Ferrite solutions help suppress electrical noise in compact automotive circuits efficiently. Additionally, nanocrystalline materials improve magnetic performance and energy efficiency, supporting next-generation EV systems requiring miniaturized, high-frequency, and thermally robust inductive components.

Ferrite materials dominated the material segment with a market share of 48.1% due to superior permeability and low core losses. Manufacturers increasingly deploy ferrite inductors in EV control systems and onboard electronics. Therefore, ferrite-based components continue enabling efficient energy conversion and stable power management across advanced automotive architectures.

Surface-Mount (SMD) inductors captured the largest mounting share at 61.2% because automakers increasingly prioritize compact electronics and automated assembly compatibility. SMD designs improve manufacturing efficiency and reduce space requirements within vehicle control units. Moreover, shielded and planar PCB-embedded variants continue supporting high-density automotive electronic modules.

Low Inductance (1–10 µH) inductors represented the leading inductance category with a share of 41.6%. These components deliver fast response and efficient energy transfer across power converters and motor-control systems. Consequently, automotive companies increasingly integrate low-inductance solutions into EV battery-management and powertrain control applications.

High-Frequency Switching inductors led the frequency segment with 41.7% share, while Low-Voltage inductors captured 44.3% share in power ratings. Passenger Vehicles dominated vehicle applications with 77.5% share, and OEMs accounted for 85.3% of end-user demand due to extensive factory-installed electronic integration.

Drivers

Growing adoption of electric vehicles continues driving demand for high-efficiency power electronics and automotive inductors worldwide. Automakers increasingly require stable energy conversion systems to improve battery efficiency and driving range. Consequently, advanced power inductors help optimize EV drivetrains while supporting compact and reliable power-management architectures.

Advanced driver-assistance systems and high-power onboard charging modules also strengthen market demand significantly. Safety systems such as adaptive cruise control and lane-keeping assistance require stable electrical performance and low electromagnetic interference. Moreover, compact inductors help automakers reduce vehicle weight while maintaining high power density and thermal reliability.

Use Cases

Automotive manufacturers increasingly deploy power inductors in DC-DC converters and battery-management systems for electric vehicles. These components regulate voltage flow, minimize electrical noise, and improve charging efficiency during vehicle operation. Consequently, power inductors enhance energy utilization while supporting stable battery and drivetrain performance across EV platforms.

Automakers also use automotive-grade inductors extensively within ADAS modules and infotainment systems. These components help maintain clean electrical signals and reduce electromagnetic interference during real-time data processing. Additionally, stable power regulation improves reliability for connected vehicle features, navigation systems, and autonomous driving technologies.

Major Challenges

Fluctuating prices for ferrite, powdered metals, and specialized magnetic materials continue creating supply-chain challenges for inductor manufacturers. Rising raw-material costs increase production expenses and reduce profit margins across the automotive electronics industry. Consequently, manufacturers face difficulties maintaining stable pricing and long-term procurement strategies for automotive-grade inductive components.

Strict automotive qualification and certification standards also slow market expansion and technology adoption. Manufacturers must conduct extensive testing under harsh environmental and thermal conditions before components receive approval. Moreover, lengthy validation cycles and compliance requirements increase operational costs and delay commercialization of advanced inductor technologies.

Business Opportunities

Wide-bandgap semiconductor technologies such as silicon carbide and gallium nitride create strong opportunities for high-frequency automotive inductors. These advanced semiconductors require compact inductors capable of operating efficiently at elevated frequencies and temperatures. Consequently, manufacturers developing compatible solutions can capture growing EV and fast-charging market demand.

Smart inductors with integrated sensing and monitoring capabilities also represent promising business opportunities for automotive electronics suppliers. These advanced components enable predictive maintenance and real-time diagnostics within connected vehicle systems. Additionally, custom inductors for ultra-fast DC-DC converters continue creating new revenue opportunities across next-generation EV platforms.

Regional Analysis

Asia Pacific dominated the Automotive Power Inductor market with a regional share of 47.2% and a market value of USD 0.6 Billion. Strong automotive manufacturing capacity, rapid EV adoption, and expanding semiconductor ecosystems continue supporting regional leadership. Consequently, China, Japan, and South Korea remain major production hubs for automotive inductive components.

North America and Europe continue demonstrating stable market growth due to rising investments in electric mobility and advanced automotive electronics. Both regions emphasize clean transportation, autonomous driving technologies, and energy-efficient vehicle systems. Moreover, stringent emission regulations and strong R&D activities continue increasing demand for high-performance automotive inductors.

Recent Developments

- August 2024 — Delta Electronics acquired power inductor and powder materials assets from Alps Alpine and Alps Electric Korea to strengthen magnetic-component capabilities.

- February 2024 — Niron Magnetics secured US$25 Million in strategic funding led by Samsung Ventures, supporting rare-earth-free magnet production for EV applications.

- January 2024 — Murata Manufacturing launched the automotive-grade DFE2MCPH_JL series power inductors featuring improved DC resistance and higher current-handling capability.

Conclusion

The Automotive Power Inductor market continues expanding steadily as vehicle electrification and advanced automotive electronics accelerate globally. Rising demand for efficient power conversion, thermal management, and compact electronic architectures strengthens adoption across EVs, hybrid systems, and connected mobility platforms. Consequently, manufacturers continue investing heavily in high-performance inductive technologies.

Wire-Wound Inductors remain the leading product category with a share of 33.8%, while Ferrite materials dominate due to strong magnetic efficiency and energy conversion performance. Additionally, Asia Pacific maintains regional leadership through large-scale automotive production, robust semiconductor ecosystems, and aggressive electric vehicle expansion strategies.

Automotive electronics suppliers must prioritize miniaturization, thermal stability, and high-frequency performance to remain competitive in evolving mobility markets. Companies investing in advanced semiconductor compatibility and intelligent inductive solutions will capture significant long-term opportunities. Therefore, analysts expect the market to reach USD 3.7 Billion by 2034.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)