Table of Contents

- Market Overview and Industry Growth

- Economic Impact of the 3A Gaming Industry

- Impact on Global Businesses and Industry Operations

- Strategic Approaches for Gaming Companies

- Key Takeaways

- Analyst Perspective and Future Market Outlook

- Use Cases and Growth Drivers

- Regional Market Landscape

- Emerging Business Opportunities

- Key Segmentation Overview

- Competitive Market Landscape

- Recent Industry Developments

- Conclusion

Market Overview and Industry Growth

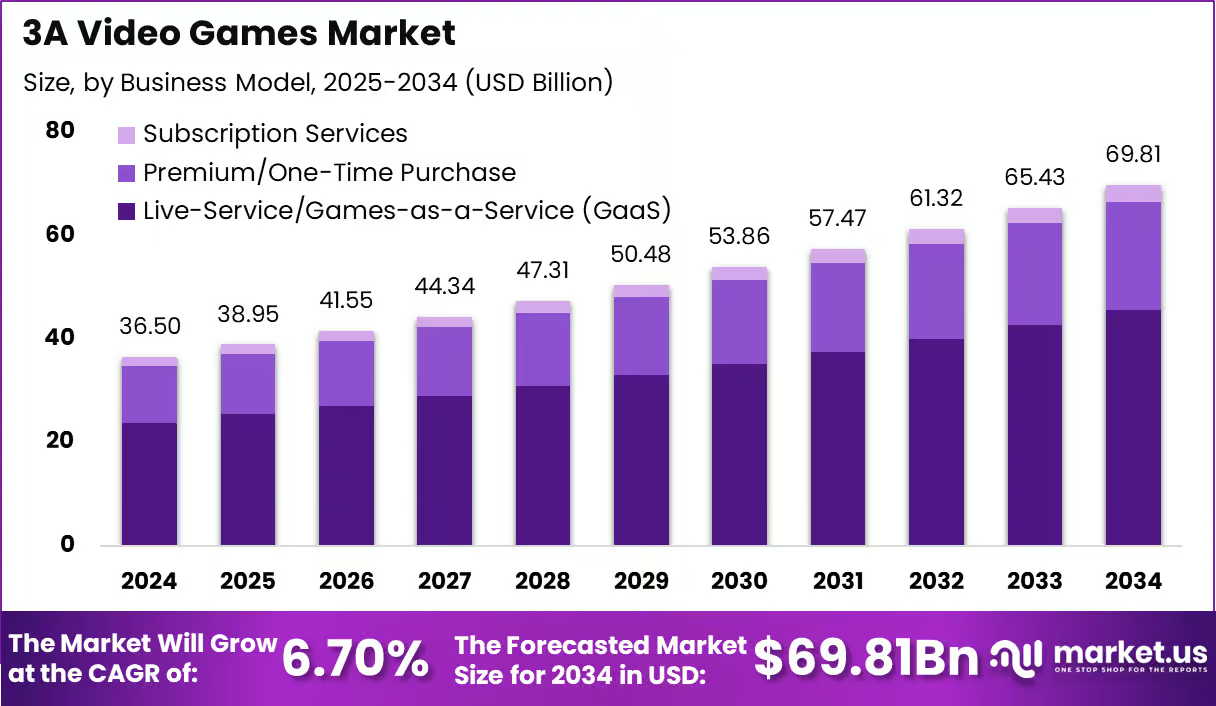

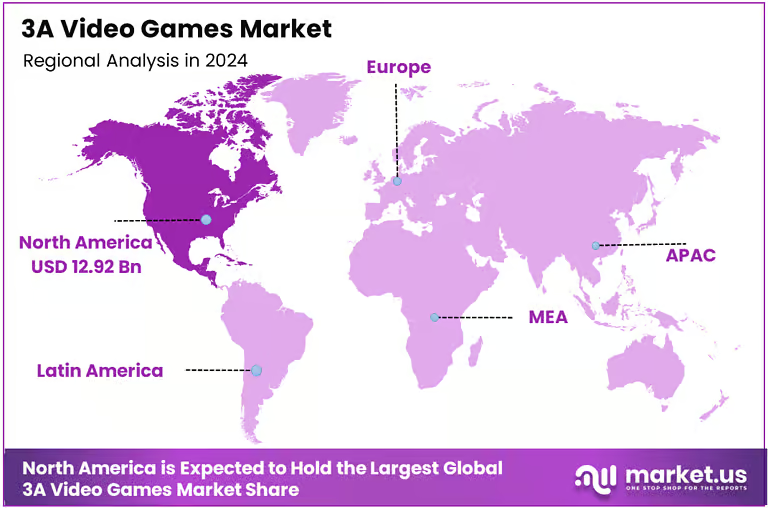

The global 3A video games market continues to expand as the gaming industry evolves with advanced graphics, immersive storytelling, and next-generation console technology. The market is valued at USD 36.5 billion in 2024 and is projected to reach USD 69.81 billion by 2034, growing at a CAGR of 6.7%. North America accounts for 35.4% of the global market, reflecting strong consumer demand and developed gaming infrastructure.

The United States leads the region with USD 11.78 billion in 2024 and is projected to reach USD 18.29 billion by 2034 at a CAGR of 4.5%. Live service or Games as a Service models dominate with a 65.3% share. Action games lead genres with 45.1%, consoles represent 54.8% of platforms, digital downloads account for 85.2% of distribution, and casual gamers represent 80.4% of users.

Economic Impact of the 3A Gaming Industry

The expansion of the 3A video games market contributes significantly to the global digital entertainment economy. Large scale game development projects require extensive investments in design, software engineering, graphics technology, and creative talent. These activities support employment across game studios, animation companies, software development firms, and digital content platforms. The industry also stimulates demand for gaming hardware such as consoles, graphics processing units, and high performance computing systems.

In addition, global gaming events, esports tournaments, and streaming platforms generate new economic activity through sponsorships, advertising, and media broadcasting. As gaming continues to evolve into a major entertainment sector, it plays a growing role in digital media revenue and technology-driven creative industries worldwide.

Impact on Global Businesses and Industry Operations

The growth of the 3A gaming market is reshaping business strategies across entertainment, technology, and digital media sectors. Game publishers are shifting toward live service models that deliver ongoing content updates, expansions, and in game purchases. This approach creates continuous revenue streams and strengthens long term player engagement. However, the increasing complexity of large scale game development has raised production costs due to higher expectations for graphics quality, storytelling, and open world environments.

Different sectors are experiencing varied impacts from this transformation. Technology companies benefit from increased demand for advanced gaming hardware and graphics technology. Streaming platforms and digital content creators gain audiences through game-related broadcasts and live gameplay content. Telecommunications companies also benefit from higher data usage associated with digital game downloads and online multiplayer gaming.

Strategic Approaches for Gaming Companies

Game developers and publishers are implementing multiple strategies to capitalize on the growth of the 3A gaming market. Companies are investing heavily in advanced game engines, artificial intelligence driven gameplay systems, and realistic graphics technologies. Many developers are focusing on cross platform compatibility to ensure that games can be played across consoles, PCs, and cloud gaming services.

Another key strategy involves expanding live service ecosystems that include seasonal updates, multiplayer modes, and downloadable content. Gaming companies are also building stronger online communities through social features, esports tournaments, and player engagement platforms. Strategic collaborations with media companies and entertainment franchises are also helping developers expand audience reach.

Key Takeaways

- The 3A video games market is valued at USD 36.5 billion in 2024.

- The market is projected to reach USD 69.81 billion by 2034 at a CAGR of 6.7%.

- North America holds 35.4% share of the global market.

- The United States generated USD 11.78 billion in 2024.

- Live service or Games as a Service models dominate with 65.3%.

- Action games represent the largest genre with 45.1% share.

- Consoles account for 54.8% of gaming platforms.

- Digital downloads represent 85.2% of total distribution.

- Casual gamers account for 80.4% of the global player base.

Analyst Perspective and Future Market Outlook

Industry analysts observe steady growth in the 3A video games market as gaming continues to evolve into a mainstream entertainment medium. The current market environment is characterized by high player engagement, strong console adoption, and increasing popularity of live service gaming models. Game publishers are investing heavily in immersive gameplay experiences, advanced graphics technologies, and long-term player engagement strategies.

Looking ahead, the future outlook remains positive as cloud gaming, artificial intelligence, and interactive storytelling technologies continue to evolve. These innovations are expected to enhance gameplay experiences and broaden access to high-quality games. As global internet connectivity improves and gaming communities expand, the 3A video games market is expected to maintain steady growth across the next decade.

Use Cases and Growth Drivers

| Use Case | Growth Factor | Market Impact |

|---|---|---|

| Immersive storytelling games | Demand for cinematic gaming experiences | Increases player engagement |

| Multiplayer online gaming | Growth of global gaming communities | Expands active user base |

| Esports competitions | Rising popularity of competitive gaming | Generates media and sponsorship revenue |

| Digital distribution platforms | Expansion of online game stores | Simplifies global game access |

| Cross platform gaming | Demand for seamless player experiences | Enhances accessibility across devices |

Regional Market Landscape

North America remains the leading region in the global 3A video games market, accounting for 35.4% of global revenue in 2024. The region benefits from a strong gaming culture, advanced digital infrastructure, and high adoption of gaming consoles and high-performance computers. Gaming communities across the region actively participate in online multiplayer games, esports tournaments, and digital gaming platforms.

The United States represents the largest market within North America with USD 11.78 billion in revenue in 2024. The US market is projected to reach USD 18.29 billion by 2034 at a CAGR of 4.5%. Strong consumer spending on entertainment, widespread adoption of next-generation consoles, and a large base of game developers and publishers continue to support market growth.

Emerging Business Opportunities

The expansion of the 3A video games market is creating multiple opportunities across entertainment, technology, and digital media industries. Game developers can benefit from the increasing demand for immersive open-world experiences and multiplayer online games. Streaming platforms and content creators also benefit from the rising viewership of gaming-related broadcasts and esports competitions.

Technology companies have opportunities to develop advanced gaming hardware, cloud gaming infrastructure, and graphics processing technologies. Digital distribution platforms can expand global reach by offering downloadable content, seasonal game updates, and subscription-based gaming services. As gaming becomes a dominant form of digital entertainment, new opportunities continue to emerge across content creation, gaming technology, and digital media platforms.

Key Segmentation Overview

The 3A video games market is segmented by business model, genre, platform, distribution channel, and end user. By business model, live service or Games as a Service leads with a 65.3% share due to continuous content updates and in-game purchases. Genre, action games dominate with 45.1% share because of the strong demand for cinematic gameplay experiences.

By platform, consoles account for 54.8% of the market, driven by next-generation systems such as PlayStation and Xbox. Distribution channel, digital downloads represent 85.2% of sales, reflecting the shift from physical game copies to online distribution. By end user, casual gamers represent 80.4% of the global market due to increasing accessibility and growing gaming communities.

Competitive Market Landscape

The 3A video games market is highly competitive and driven by continuous innovation in game development, graphics technology, and interactive storytelling. Companies compete by launching large-scale game titles with high production quality, engaging narratives, and expansive multiplayer features. The industry places strong emphasis on delivering immersive player experiences supported by advanced graphics engines and realistic gameplay mechanics.

Top Key Players in the Market

- Electronic Arts

- Take-Two Interactive

- Capcom

- Ubisoft

- Epic Games

- Bluehole

- Nexon

- Riot Games

- Tencent

- Niantic

- Neowiz Games

- Activision Blizzard

- Nintendo

- PlayStation Studios

- Sony Interactive Entertainment

- 2K Games

- Warner Bros. Games

- Xbox Game Studios

- Sega

- Bandai Namco

- Krafton

- Rockstar

- Blizzard Entertainment

- Others

Competition is also influenced by the expansion of live service ecosystems and digital distribution platforms. Developers focus on creating long-term player engagement through regular updates, downloadable content, and community-driven gaming environments. Strategic partnerships with entertainment franchises and digital streaming platforms are also shaping the competitive landscape.

Recent Industry Developments

- Game developers are expanding live service models with seasonal updates and new downloadable content.

- Next-generation consoles continue to support higher resolution graphics and faster processing speeds.

- Digital distribution platforms are strengthening global access to downloadable game titles.

Conclusion

The 3A video games market continues to grow as technological innovation, digital distribution, and immersive gameplay experiences attract a global player base. Increasing console adoption, strong gaming communities, and evolving live service models are expected to support steady industry expansion over the coming decade.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)