Introduction

The global drone simulator market is projected to reach USD 7.7 billion by 2034, growing from USD 1.4 billion in 2024 at a CAGR of 18.6%. In 2024, North America dominated with a 36.5% market share, generating USD 0.51 billion in revenue. The U.S. segment, valued at USD 0.43 billion, is expected to grow at a CAGR of 16.7%, fueled by increasing demand for advanced training, defense applications, and mission planning. The rising adoption of drones across commercial and military sectors drives the growing need for sophisticated simulation technologies globally.

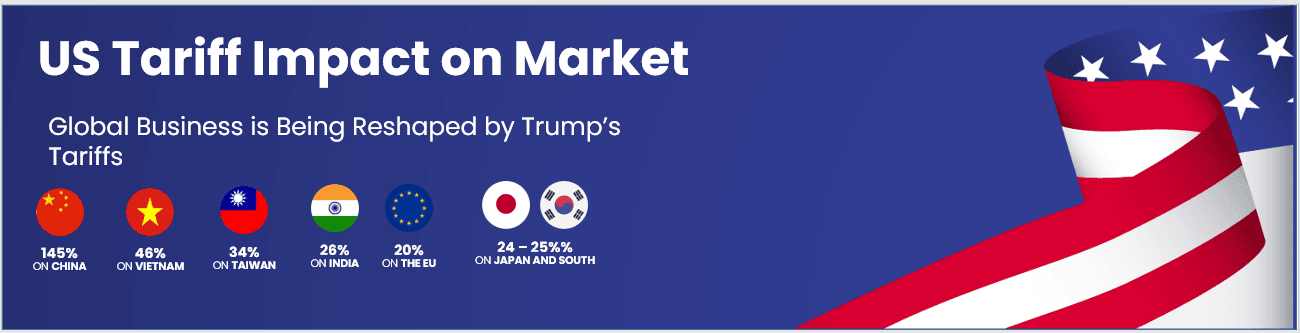

How Tariffs Are Impacting the Economy

Tariffs on drone components and simulation hardware elevate manufacturing costs, leading to higher prices for end-users and increased operational expenses for businesses. This cost inflation limits investments and slows down infrastructure development, dampening overall economic growth.

➤ Discover how our research uncovers business opportunities @ https://market.us/report/global-drone-simulator-market/free-sample/

(Use corporate mail ID for quicker response)

Supply chains face disruptions as companies seek alternative suppliers outside tariff-imposed regions, often incurring higher costs and extended lead times. Retaliatory tariffs amplify global trade tensions, increasing uncertainty and complicating cross-border collaborations. These factors collectively restrain innovation and expansion in drone technologies and related training markets, impacting sectors dependent on advanced drone simulation capabilities.

Impact on Global Businesses

Global businesses operating in drone simulation face rising component costs due to tariffs, affecting profitability and project timelines. Supply chain diversification or relocation adds operational complexity and capital expenditure. Defense contractors and commercial drone firms encounter delays in deploying training platforms, impacting workforce readiness.

Sector-specific challenges include increased compliance costs and technology sourcing difficulties. Emerging markets, heavily reliant on imported technology, face amplified barriers to adoption. Consequently, companies are driven to enhance supply chain resilience, optimize resource allocation, and accelerate digital transformation to maintain competitiveness amid tariff-induced volatility.

Strategies for Businesses

Businesses respond to tariff challenges by diversifying suppliers and increasing localized production where feasible. Investing in modular and scalable simulation technologies reduces dependency on costly hardware. Predictive analytics assist in managing inventory and anticipating tariff policy changes. Strategic partnerships with regional manufacturers and technology firms improve supply chain stability. Embracing cloud-based simulation platforms enhances flexibility and reduces infrastructure costs. Additionally, active engagement in trade policy advocacy helps shape favorable regulatory environments. Overall, agility, innovation, and collaboration remain critical for sustaining growth in a tariff-sensitive market.

Key Takeaways

- Drone simulator market projected to grow at 18.6% CAGR through 2034

- Tariffs increase costs and disrupt supply chains in drone technology

- Defense and commercial sectors face deployment delays and higher expenses

- Supply diversification and cloud adoption are key business strategies

- Predictive analytics support proactive tariff risk management

➤ Get full access now @ https://market.us/purchase-report/?report_id=148809

Analyst Viewpoint

The drone simulator market is poised for robust growth driven by increasing demand for pilot training and mission planning tools. Despite tariff-related cost pressures and supply chain disruptions, technological advancements and strategic business adaptations sustain momentum. Cloud and AI integration will further enhance simulation capabilities. Regional investments in defense and commercial drone applications promise continued expansion. The market outlook is optimistic, with innovation and policy support playing vital roles in overcoming trade-related challenges.

Regional Analysis

North America dominates the drone simulator market with a 36.5% revenue share in 2024, driven by strong defense spending and commercial drone adoption. The U.S. leads regional growth with substantial investments in training and simulation infrastructure. Europe shows steady growth, supported by aerospace innovation and regulatory frameworks. Asia-Pacific exhibits rapid expansion potential due to increasing drone applications in industries like agriculture and logistics. Regional growth disparities reflect differences in technology readiness, regulatory environments, and investment priorities.

➤ Discover More Trending Research

- Deadhand System Market

- AI in Cellular Networks Market

- Tax Tech Market

- AI-Powered Asset Tracking System Market

Business Opportunities

Emerging applications in defense training, disaster management, and commercial drone operations create diverse opportunities for simulator providers. Cloud-based and AI-enhanced simulation platforms cater to scalable and cost-effective training needs. Growth in emerging economies, driven by infrastructure development and drone adoption, expands market potential. Collaborations with government agencies and private sector players enable customized solutions. Additionally, integrating simulators with real-time data and VR/AR technologies opens avenues for innovation and enhanced user experience.

Key Segmentation

Component

- Hardware

- Software

- Services

Application

- Defense Training

- Commercial Drone Pilot Training

- Mission Planning

- Research and Development

Deployment Mode

- On-premises

- Cloud-based

End User

- Military & Defense

- Commercial Enterprises

- Academic & Research Institutions

Key Player Analysis

Leading companies emphasize innovation in realistic simulation environments and AI integration to improve training effectiveness. Investments focus on scalable cloud solutions and modular hardware designs. Strategic alliances with defense agencies and commercial drone manufacturers accelerate market penetration. Market leaders prioritize user experience, regulatory compliance, and customization to meet diverse client needs. Expansion in emerging markets and continuous R&D sustain competitive advantages.

Top Key Players in the Market

- CAE Inc.

- Israel Aerospace Industries Ltd.

- Leonardo S.p.A.

- Zen Technologies Limited

- Havelsan A.S.

- General Atomics Aeronautical Systems, Inc.

- Simlat UAS & ISR Training Solutions

- Others

Recent Developments

In 2025, major providers launched cloud-based drone simulators with enhanced AI-driven training modules. Partnerships with defense organizations expanded simulation deployments. Increased focus on VR/AR integration improved immersive training experiences.

Conclusion

The drone simulator market is on a strong growth trajectory fueled by rising demand in defense and commercial sectors. Tariff challenges drive supply chain innovation and cloud adoption, ensuring continued expansion. Technological advancements and regional investments will support sustained market momentum.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)