Introduction

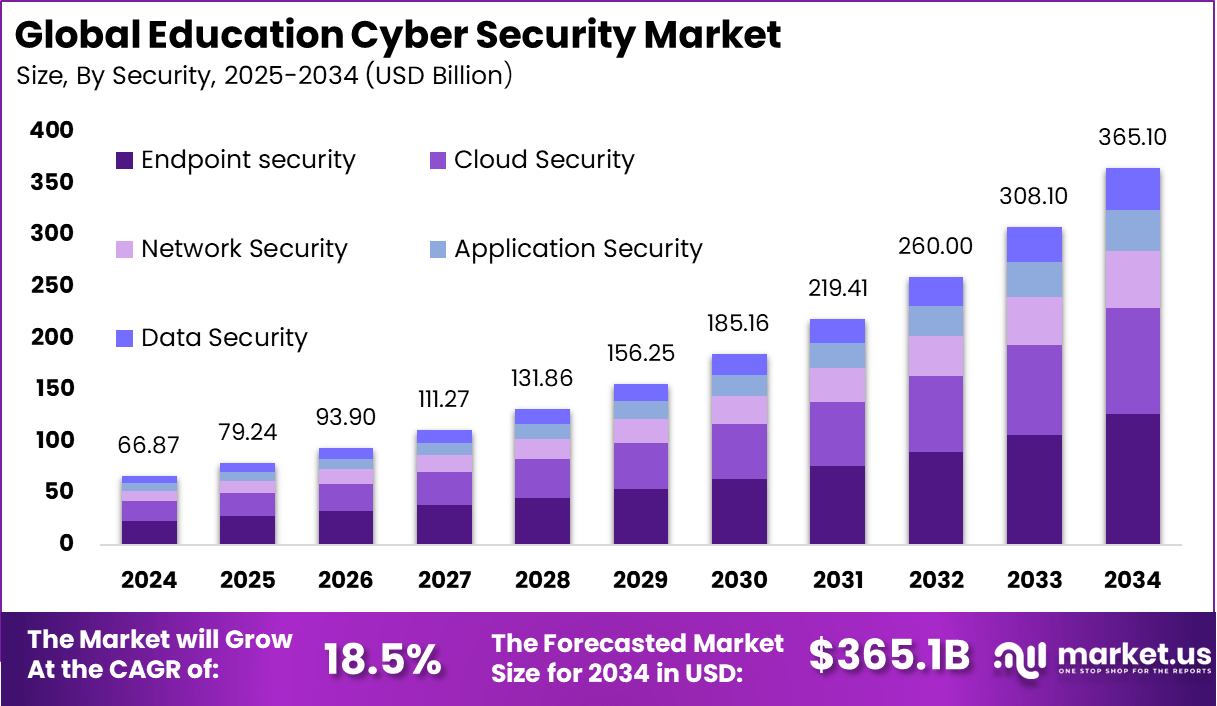

The Global Education Cyber Security Market is projected to expand from USD 66.87 billion in 2024 to USD 365.10 billion by 2034, registering a strong CAGR of 18.5% (2025–2034). In 2024, North America dominated with 37.2% market share, generating USD 24.87 billion in revenue. The growth is fueled by rising cyber threats targeting schools, universities, and e-learning platforms.

With the increasing adoption of digital education, cloud-based systems, and connected devices, the need for secure data handling, compliance, and protection of intellectual property is at an all-time high. Cybersecurity is becoming an indispensable component of the education sector globally.

How Growth is Impacting the Economy

The rapid growth of cybersecurity education is positively influencing global economies by strengthening digital infrastructure, enhancing institutional resilience, and creating new employment opportunities in IT and cyber defense. Investments in cyber security solutions are reducing risks of data breaches, minimizing economic losses, and ensuring the smooth operation of academic institutions. Governments are allocating larger budgets to secure national education systems, while private players are fueling innovation with advanced AI and machine learning-based solutions.

This growth is boosting demand for skilled professionals, contributing to the expansion of cyber training programs and certifications. Additionally, the rise in secure e-learning platforms is driving growth in the broader digital economy, empowering startups and SMEs to provide specialized services. Collectively, the expansion of this sector underpins stronger data governance, economic stability, and sustainable development in the global education ecosystem.

➤ Unlock growth! Get your sample now! – https://market.us/report/education-cyber-security-market/free-sample/

Impact on Global Businesses

Rising Costs & Supply Chain Shifts

Educational institutions and solution providers face rising costs due to higher investments in advanced software, security frameworks, and compliance tools. Supply chains are shifting toward cloud-based and regionalized solutions to reduce dependency on global vendors and ensure faster threat response.

Sector-Specific Impacts

- K-12 Schools: Increasing demand for secure online learning platforms.

- Universities: Protection of research data and intellectual property.

- EdTech Firms: Stronger compliance with global privacy laws.

- Training Institutes: Adoption of cyber defense to protect student data.

Strategies for Businesses

Businesses should focus on AI-driven security, cloud-native protection, and multi-factor authentication systems. Strengthening partnerships with educational institutions, offering customized solutions, and ensuring compliance with laws like GDPR, FERPA, and HIPAA will be key strategies. Additionally, investing in cybersecurity awareness training, developing scalable cloud platforms, and prioritizing zero-trust frameworks will enhance competitiveness and market presence.

Key Takeaways

- Market to reach USD 365.10 billion by 2034.

- Strong CAGR of 18.5% (2025–2034).

- North America held 37.2% share in 2024.

- Rising cyberattacks driving adoption of AI-driven security.

- K-12, universities, and EdTech are major growth segments.

➤ Stay ahead—secure your copy now – https://market.us/purchase-report/?report_id=157734

Analyst Viewpoint

Present: Education institutions face increasing cyberattacks, prompting investments in data security and compliance systems. Cloud-based platforms and AI-driven tools are gaining traction.

Future Positive View: Integration of predictive analytics, blockchain, and zero-trust frameworks will redefine education cybersecurity. As digital learning expands globally, cybersecurity adoption will become universal, ensuring safer learning ecosystems and opening vast opportunities for innovation and partnerships.

Use Case and Growth Factors

| Use Case | Growth Factors |

|---|---|

| Secure Virtual Classrooms | Rising e-learning adoption, need for data privacy |

| Research Data Protection | Intellectual property security in universities |

| Cloud Security for EdTech | Expansion of digital platforms, SaaS adoption |

| Identity & Access Control | Multi-factor authentication demand |

| Threat Intelligence | AI-driven predictive analytics for cyber defense |

Regional Analysis

North America leads the market due to strict regulations, large-scale EdTech adoption, and frequent cyberattacks on education systems. Europe follows with growing GDPR compliance and investments in school security frameworks. Asia-Pacific is set for the fastest growth, driven by digital transformation in India, China, and Southeast Asia, alongside government-backed e-learning initiatives. Latin America and the Middle East & Africa are gradually adopting education cybersecurity, focusing on protecting growing e-learning ecosystems. Each region reflects unique drivers but shares the collective push toward safer, data-secure learning environments.

➤ Don’t Stop Here—check Our Library

- Digital Signage in Education & Universities Market

- Aerospace MRO Market

- Digital Signage for Events Market

- Display Market

Business Opportunities

The sector offers opportunities in AI-driven security platforms, blockchain-based identity management, and cloud-native cyber defense systems. Growing demand for secure online testing platforms and digital classrooms provides a fertile ground for startups. Partnerships with universities and government-led digital education programs will expand market entry opportunities. Companies that deliver cost-effective, scalable solutions targeting K-12 schools and emerging economies will capture significant market share. Integration of compliance-as-a-service solutions also presents untapped business potential.

Key Segmentation

The education cybersecurity market can be segmented by component, deployment, application, and region:

- By Component: Software, hardware, services.

- By Deployment: Cloud-based, on-premises.

- By Application: K-12 schools, higher education, EdTech platforms, and training institutes.

- By Region: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa.

Key Player Analysis

The market is highly competitive, with players focusing on advanced security solutions tailored for the education sector. Companies are investing in AI, blockchain, and cloud-native platforms to provide predictive threat detection and identity management. Strategic collaborations with universities, partnerships with governments, and acquisitions to expand service portfolios are common strategies. Firms are also targeting developing economies with affordable and scalable solutions, while maintaining strict compliance with global regulations. Sustainability in IT operations and user-friendly security platforms are emerging as key differentiators.

- Fortinet, Inc.

- IBM Corporation

- Microsoft Corporation

- BAE Systems Plc

- Broadcom, Inc.

- Centrify Corporation

- Check Point Software Technology Ltd.

- Palo Alto Networks, Inc.

- Proofpoint, Inc.

- Sophos Ltd.

- Others

Recent Developments

- Launch of AI-driven platforms to detect phishing and ransomware attacks in schools.

- Expansion of cloud-native cybersecurity solutions for EdTech firms.

- Strategic partnerships between governments and providers to secure e-learning platforms.

- Deployment of blockchain-based identity management for universities.

- Increased investment in training programs for cybersecurity awareness in K-12 institutions.

Conclusion

The education cybersecurity market is expanding rapidly, driven by rising cyberattacks, strict compliance needs, and digital learning adoption. With North America leading and Asia-Pacific emerging as a key growth hub, the sector offers immense opportunities for innovation and partnerships, ensuring safer and more resilient global education ecosystems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)