Table of Contents

Introduction

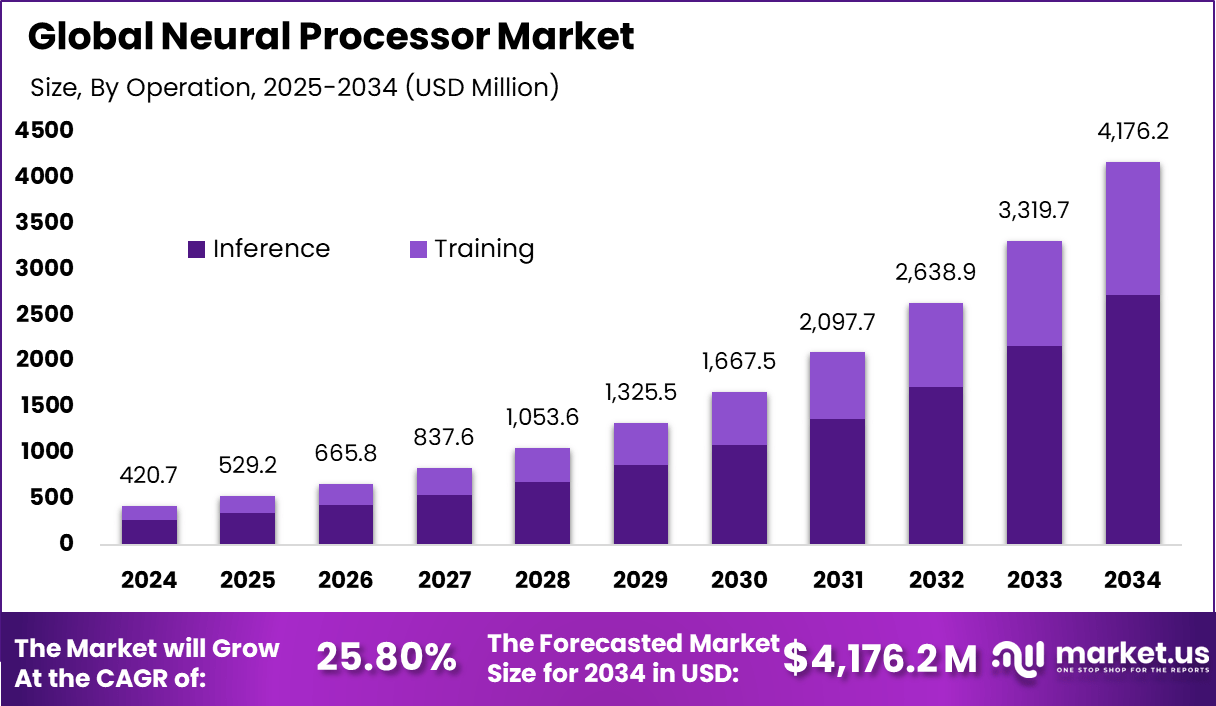

The Global Neural Processor Market generated USD 420.7 million in 2024 and is projected to reach USD 4,176.2 million by 2034, expanding at a CAGR of 25.80%. Asia Pacific led the market with a 36.6% share valued at USD 153.9 million. Growth is driven by rising adoption of AI accelerators, edge computing expansion, increasing deployment of intelligent devices, and advances in autonomous systems, robotics, smart sensors, and high-performance computing architectures that require low-latency neural processing capabilities.

How Growth is Impacting the Economy

The rapid expansion of the neural processor market is reshaping global economic dynamics by accelerating AI-driven automation, improving industrial productivity, and enhancing digital infrastructure capacity. Faster and more efficient processors reduce computational costs, enabling industries to scale AI workloads in healthcare, financial services, automotive, and manufacturing.

Nations investing in fabless chip design, semiconductor fabrication, and AI hardware R&D attract foreign investment and strengthen technological sovereignty. The growth further drives demand for cloud services, 5G networks, and edge computing frameworks, stimulating job creation in engineering, microchip design, and advanced manufacturing. By powering emerging sectors such as autonomous mobility, smart factories, and intelligent consumer electronics, neural processors contribute directly to GDP expansion and future-proofing of national digital economies.

➤ Smarter strategy starts here! Get the sample – https://market.us/report/neural-processors-market/free-sample/

Impact on Global Businesses

Businesses face rising capital expenditure for advanced computing hardware, higher integration costs, and increased cybersecurity needs. Supply chain shifts occur due to global semiconductor dependencies, raw material shortages, and geographic concentration of chip fabrication. Sector-specific impacts include faster AI inference in healthcare imaging, improved fraud detection in finance, real-time automation in manufacturing, enhanced driver-assistance systems in automotive, and more efficient power management in consumer electronics.

Strategies for Businesses

Companies should prioritize the adoption of scalable AI hardware, integrate neural accelerators into edge devices, and form partnerships with semiconductor vendors and cloud providers. Investing in in-house AI engineering teams, optimizing workloads through model compression, and building resilient supply chains strengthens operational efficiency. Diversifying sourcing, implementing hardware-aware AI models, and leveraging energy-efficient processors also help control costs while improving performance.

Key Takeaways

- Strong CAGR of 25.80% reflects accelerating AI hardware adoption

- Asia Pacific dominates with a 36.6% market share

- Neural processors enable faster inference and lower latency

- Edge computing and autonomous systems drive demand

- Semiconductor supply chain shifts affect global production

➤ Unlock growth secrets! Buy the full report – https://market.us/purchase-report/?report_id=159057

Analyst Viewpoint

The market is experiencing powerful momentum driven by rapid AI scaling, growth in edge intelligence, and rising demand for energy-efficient computation. In the present landscape, neural processors serve as critical enablers of real-time analytics and autonomous decision-making. Looking ahead, advancements in 3D chip stacking, neuromorphic computing, and quantum-inspired architectures will expand capabilities further. Strong government investments in semiconductor manufacturing and strategic partnerships across AI ecosystems reinforce a highly optimistic long-term outlook for the sector.

Use Case and Growth Factors

Use Cases Table

| Use Case | Description |

|---|---|

| Autonomous Vehicles | Enables real-time perception, path planning, and object detection. |

| Smart Edge Devices | Powers low-latency AI inference in IoT and consumer electronics. |

| Healthcare Imaging | Supports high-speed diagnostics and medical image recognition. |

| Industrial Automation | Enhances robotics, predictive maintenance, and quality inspection. |

Growth Factors Table

| Growth Factor | Description |

|---|---|

| Expansion of Edge AI | Drives demand for low-power, high-efficiency processors. |

| Semiconductor Innovation | Improves processing speed and architecture efficiency. |

| Rising AI Workloads | Increases the need for dedicated neural inference hardware. |

| Government Semiconductor Programs | Boosts R&D and domestic chip production capacity. |

Regional Analysis

Asia Pacific leads due to extensive semiconductor manufacturing capacity, strong government incentives, and expanding AI deployment across automotive, electronics, and industrial sectors. North America holds significant share driven by advanced R&D ecosystems, AI startups, and major cloud service providers integrating neural accelerators. Europe focuses on energy-efficient chip design, autonomous mobility, and AI regulations supporting hardware innovation. The Middle East, Latin America, and Africa show rising adoption in smart city programs, telecommunications upgrades, and industrial digitalization.

➤ Want more market wisdom? Browse reports –

Business Opportunities

Strong opportunities are emerging in edge AI processors, neuromorphic chips, robotics accelerators, and energy-efficient inference hardware. Rapid expansion of autonomous vehicles, AR/VR systems, smart wearables, and IoT infrastructure creates demand for optimized neural processors. Enterprises deploying private 5G networks and intelligent automation solutions also offer significant growth potential. Startups developing domain-specific processors for healthcare, finance, and security analytics can scale quickly through strategic collaborations.

Key Segmentation

The market is segmented by type, application, architecture, and end-user. Types include training processors, inference processors, and hybrid neural units. Applications span autonomous systems, computer vision, NLP, robotics, edge AI, and smart devices. Architectures include neuromorphic systems, ASIC-based neural engines, and FPGA accelerators. End-users include automotive, healthcare, industrial automation, consumer electronics, BFSI, and telecom, each requiring high-speed, low-latency intelligent processing.

Key Player Analysis

Leading market participants prioritize architectural innovation, energy-efficient chip design, and integration with cloud and edge ecosystems. Their strategies include expanding fabrication partnerships, enhancing AI model optimization, and scaling hardware-software co-design platforms. Companies focus on strengthening semiconductor supply resilience, improving inference speeds, supporting domain-specific accelerators, and entering high-growth verticals such as autonomous mobility and industrial robotics. Strong investment in R&D ensures continuous performance advancements and competitive differentiation.

- Advanced Micro Devices, Inc.

- Arm Limited

- Aspinity, Inc.

- Bitbrain Technologies

- BrainChip, Inc.

- BrainCo, Inc.

- General Vision, Inc.

- Google LLC

- Halo Neuroscience

- Intel Corporation

- NVIDIA Corporation

- Qualcomm Inc.

- Samsung Electronics Co. Ltd.

- Other Major Players

Recent Developments

- Launch of next-generation neural accelerators for edge devices

- Expansion of fabrication partnerships for advanced AI chips

- Introduction of neuromorphic-inspired architectures for ultra-low power AI

- Collaborations between semiconductor firms and autonomous vehicle developers

- Government funding initiatives to strengthen domestic chip ecosystems

Conclusion

The neural processor market is expanding rapidly as industries accelerate adoption of edge AI, automation, and intelligent devices. With strong demand, continuous innovation, and rising global investment, the sector is positioned for sustained long-term growth and technological advancement.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)