Table of Contents

Workplace Transformation Market Size

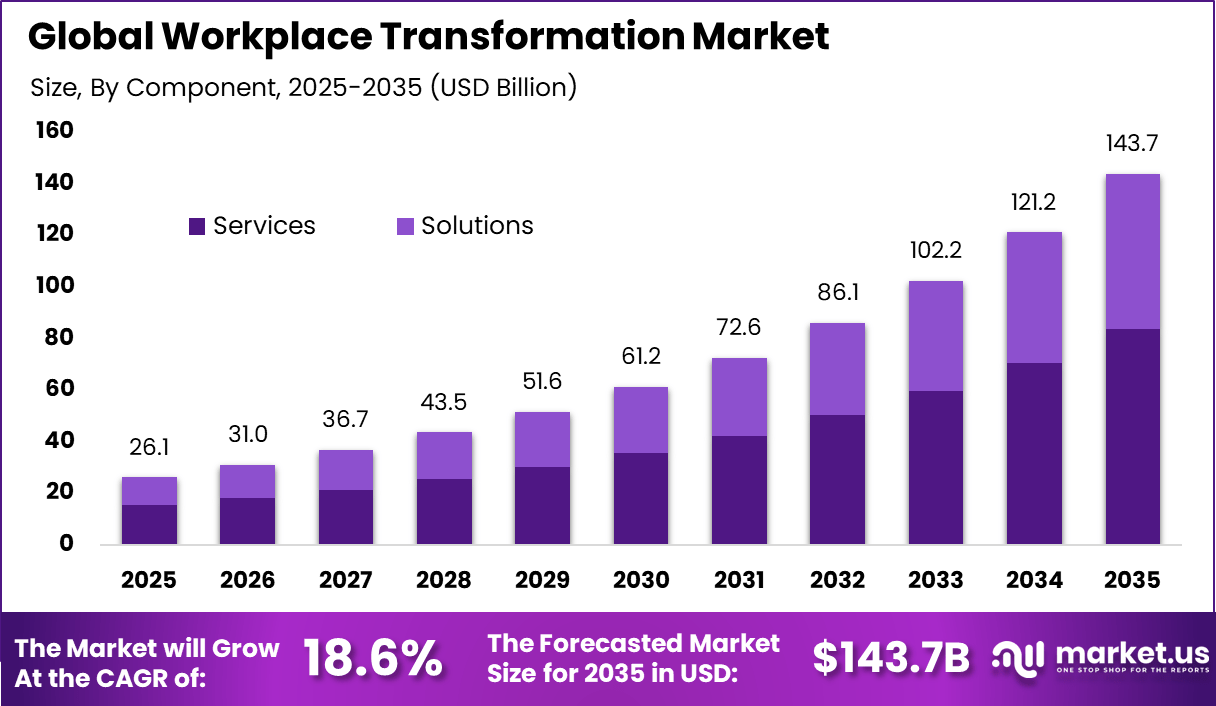

The global Workplace Transformation market was valued at USD 26.1 billion in 2025 and is expected to expand rapidly over the forecast period. The market is projected to reach approximately USD 143.7 billion by 2035, growing at a strong CAGR of 18.6% from 2026 to 2035. This growth is driven by rising adoption of digital workplace tools, hybrid work models, and cloud based collaboration platforms. Organizations are increasingly investing in technology led transformation to improve productivity and employee experience.

The workplace transformation market refers to technology solutions, services, and strategies that enable organizations to redesign how work is performed, supported, and experienced in modern business environments. This market includes digital collaboration platforms, workspace analytics, flexible scheduling tools, employee experience platforms, automation solutions, and change management services. Workplace transformation enables organizations to support hybrid work models, improve productivity, enhance employee engagement, and align physical and digital workspaces with strategic goals. Adoption spans enterprises, government agencies, and small and medium-sized businesses focused on modernizing operations and culture.

Market growth has been shaped by evolving work patterns, particularly accelerated by the rise of hybrid and remote work. Traditional office-centric models have been challenged by demands for flexibility, digital connectivity, and performance continuity. Workplace transformation solutions allow organizations to maintain operational resilience, enable real-time collaboration, and design work experiences that attract and retain talent. As business priorities shift toward agility and digital fluency, workplace transformation has become a strategic imperative.

Market Key Takeaways

- Services dominated with a 58.3% share, as organizations relied on consulting, integration, and managed services to modernize workflows, infrastructure, and employee experience at scale.

- Large enterprises led adoption with 68.9%, driven by enterprise wide transformation programs, hybrid work models, and sustained focus on workforce productivity.

- IT and telecommunications emerged as the top end user industry at 41.7%, reflecting early adoption of cloud workplaces, collaboration platforms, and automation tools.

- North America held 38.1% of the global market, supported by strong enterprise IT spending and mature digital workplace ecosystems.

- The U.S. market reached USD 8.96 billion, expanding at a 16.83% growth rate, driven by hybrid work adoption, AI enabled collaboration, and continuous workplace digitization.

Key Statistics and Adoption Signals

- More than 80% of organizations now operate with a formal workplace transformation strategy.

- 84% of companies offer flexible or hybrid work models, reinforcing long term structural change in how work is organized.

- Around 91% of enterprises rely on cloud based collaboration platforms for daily operations, underscoring the central role of digital infrastructure.

- By 2030, about 22% of roles are expected to be created or displaced, increasing demand for reskilling and workforce planning.

- 81% of employees require AI related upskilling to remain relevant, while 78% of jobs are already being enhanced by technology.

- AI and big data, cybersecurity, and digital literacy ranked as the most in demand skills across transformed workplaces.

Execution Gaps and Performance Impact

- 55% of organizations cited technology selection and data security as major challenges during transformation initiatives.

- Nearly 70% of workplace transformation programs failed to fully meet objectives, highlighting execution and change management gaps.

- Only 19% of HR leaders felt prepared to address future talent shortages linked to digital and AI driven change.

- Around 13% of employees reported using generative AI for more than 30% of daily tasks, compared with 4% perceived by senior leaders, revealing a visibility gap.

- Organizations that successfully embedded AI tools reported productivity improvements of up to 37%, supported by faster task execution and reduced manual effort.

- Despite progress, more than 33% of enterprises still perform up to half of workplace processes manually, indicating significant remaining automation potential.

Drivers Impact Analysis

| Category | Key Driver Description | Estimated Impact on CAGR (%) | Geographic Relevance | Impact Timeline |

|---|---|---|---|---|

| Hybrid Work Adoption | Long term shift toward flexible and remote work models across enterprises. | ~4.8% | North America, Europe | Short to Mid Term |

| Digital Collaboration Demand | Rising dependence on cloud based collaboration and communication platforms. | ~3.9% | Global | Short Term |

| Workforce Productivity Focus | Growing emphasis on efficiency, automation, and performance monitoring tools. | ~3.2% | North America, Asia Pacific | Mid Term |

| Employee Experience Improvement | Organizations prioritize engagement, retention, and digital workplace satisfaction. | ~2.7% | North America, Europe | Mid to Long Term |

| Enterprise IT Modernization | Migration from legacy systems toward modern digital workplace environments. | ~2.1% | Global | Long Term |

Risk Impact Analysis

| Risk Category | Risk Description | Estimated Negative Impact on CAGR (%) | Geographic Exposure | Risk Timeline |

|---|---|---|---|---|

| Cybersecurity Exposure | Expansion of digital workplace platforms increases attack surfaces and security vulnerabilities. | ~2.4% | Global | Short Term |

| Change Management Failure | Employee resistance and low adoption slow the transition to new digital work models. | ~1.9% | Global | Short to Mid Term |

| Data Privacy Compliance | Failure to meet data protection regulations creates legal and operational risks. | ~1.5% | North America, Europe | Mid Term |

| IT Skill Shortage | Limited availability of skilled professionals delays digital transformation initiatives. | ~1.2% | Asia Pacific, Emerging Markets | Long Term |

Restraint Impact Table

| Restraint Factor | Restraint Description | Impact on Market Expansion (%) | Most Affected Regions | Duration |

|---|---|---|---|---|

| High Implementation Cost | Large upfront investments are required for digital tools, platforms, and supporting infrastructure. | ~3.1% | Emerging Markets | Mid Term |

| Integration Complexity | Challenges in integrating new digital workplace solutions with legacy IT systems. | ~2.6% | Global | Mid Term |

| Cultural Readiness Gap | Limited digital adoption mindset and resistance to change slow transformation. | ~2.1% | Emerging Markets | Long Term |

| ROI Measurement Challenges | Difficulty in clearly measuring productivity improvements and return on investment. | ~1.7% | Global | Long Term |

Regional Analysis

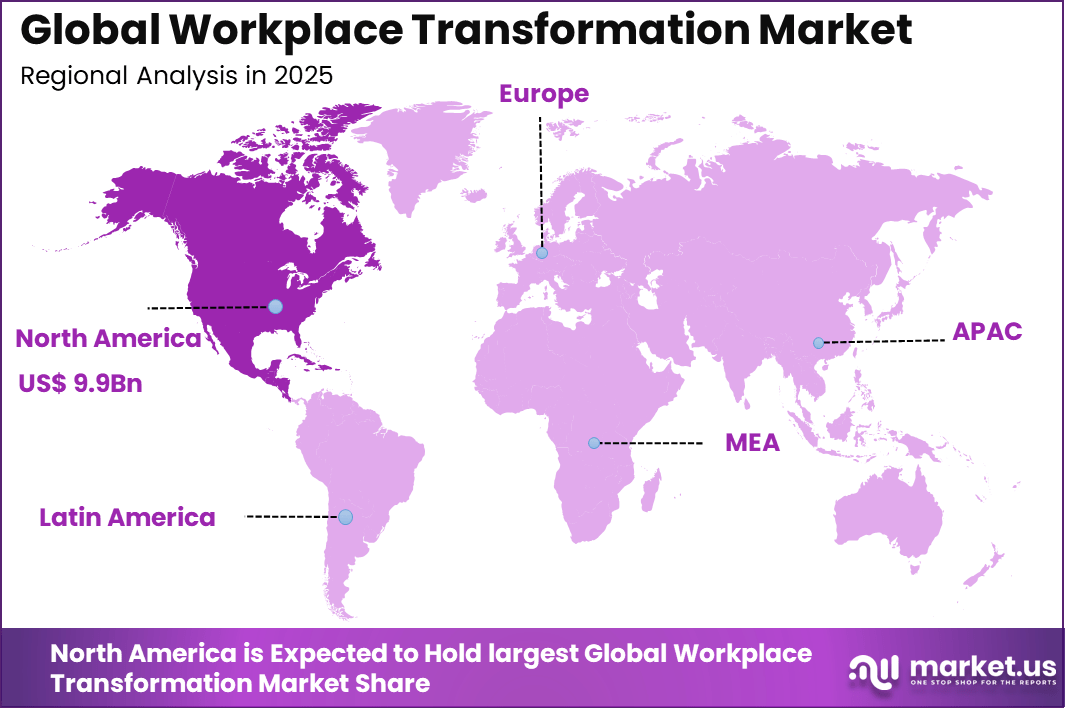

North America held a dominant position in the global market, accounting for more than 38.1% of total revenue. The region generated around USD 9.9 billion, supported by early adoption of digital transformation initiatives and high enterprise IT spending. Strong presence of technology providers and advanced workplace infrastructure further strengthened regional leadership. As a result, North America continued to shape global workplace transformation trends.

Demand Analysis

Demand for workplace transformation solutions is influenced by enterprise digitalization strategies. As organizations modernize applications, automate processes, and adopt data-driven decision making, they require supportive workplace technologies. Integrated platforms that unite communication, project management, and performance insights are increasingly sought. Demand is particularly strong where digital maturity is high and strategic outcomes are tied to collaborative efficiency.

Demand is also shaped by demographic and workforce trends. Younger and more mobile workers often prioritize flexibility and purpose-driven work environments. Organizations seeking to attract and retain this talent focus on transformation initiatives that deliver autonomy, connection, and meaningful interaction. This labour market dynamic reinforces market growth.

Increasing Adoption Technologies

Cloud computing technologies are accelerating adoption of workplace transformation solutions by enabling scalable, secure, and anywhere-accessible services. Cloud platforms support remote access to applications, data, and collaboration tools without reliance on centralized infrastructure. Scalability and rapid deployment reduce barriers to adoption, particularly for distributed teams. Cloud-native design enhances resilience and interoperability across digital tools.

Artificial intelligence and automation technologies are also influencing adoption by supporting smarter workflows, personalized experiences, and operational insights. AI-driven features such as intelligent scheduling, resource recommendations, sentiment analysis, and adaptive collaboration support more efficient and human-centric work. Automation of repetitive tasks allows knowledge workers to focus on strategic priorities. These intelligent capabilities enhance the value delivered by transformation solutions.

One key reason organizations adopt workplace transformation solutions is improved productivity and operational agility. Integrated platforms and automation tools reduce friction in communication, decision making, and task coordination. Employees can collaborate efficiently across locations and time zones, reducing delays and rework. This operational efficiency supports faster response to market changes and internal goals.

Another reason for adoption is enhanced workforce engagement and satisfaction. Tools that provide clarity of expectations, feedback loops, and support for autonomy contribute to positive employee experiences. Better engagement is associated with lower turnover, higher innovation, and stronger organizational performance. Workplace transformation solutions help organizations foster inclusive and adaptive work cultures.

Investment Opportunities

Investment opportunities in the workplace transformation market exist in analytics and insight platforms that support data-driven decision making. Solutions that provide real-time visibility into work patterns, productivity, collaboration networks, and employee wellbeing help leaders optimize resources and strategies. Investors may focus on technologies that unify operational and human experience data into actionable intelligence. Enhancing predictive capabilities can support continuous improvement.

Another opportunity lies in services that support change management, employee development, and cultural alignment. Technological transformation requires adoption support, training, and behavioural change initiatives. Providers that integrate technology implementation with coaching, engagement programs, and long-term optimization services can build recurring revenue streams. This holistic approach enhances adoption success and deepens client relationships.

Business Benefits

Adoption of workplace transformation solutions improves operational efficiency and execution speed. Automated workflows, integrated communication channels, and shared digital workspaces reduce duplication of effort and enable smoother handoffs. This efficiency supports higher throughput and better coordination across functions. Organizations benefit from reduced operational friction and improved delivery outcomes.

Workplace transformation also strengthens strategic alignment and organizational resilience. Teams equipped with adaptive tools and insights are better prepared to manage disruptions, scale operations, and innovate. Enhanced collaboration and data connectivity support informed decision making and cross-functional integration. These benefits contribute to long-term competitiveness and sustainable growth.

Regulatory Environment

The regulatory environment for the workplace transformation market includes labour and employment laws that govern worker rights, workplace conditions, and remote work practices. Organizations must ensure that transformation initiatives align with regulations on working hours, compensation, health and safety, and accommodations. Compliance reduces legal exposure and reinforces ethical practices.

Data protection and cybersecurity regulations also shape how workplace technologies are implemented and managed. Digital platforms often process personal information, collaboration data, and performance metrics, which are subject to privacy laws and security standards. Providers and users must implement secure data governance, access controls, and transparent policies. Adherence to regulatory frameworks builds trust and supports lawful operation across geographic regions.

Key Market Segments

By Component

- Solutions

- Cloud-based

- On-premises

- Services

- Consulting Services

- Technology Integration Services

- Managed Services

By Organization Size

- Large Enterprises

- Small & Medium Businesses

By End-User Industry

- IT & Telecommunications

- BFSI

- Healthcare

- Retail & Manufacturing

- Others

Top Key Players in the Market

- Accenture

- Deloitte

- IBM

- Microsoft

- Cisco

- HPE

- Citrix

- VMware

- Adobe

- Salesforce

- ServiceNow

- Atlassian

- Slack

- Zoom

- Others

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 26.1 Bn |

| Forecast Revenue (2035) | USD 143.7 Bn |

| CAGR(2026-2035) | 18.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)