Table of Contents

Market Overview

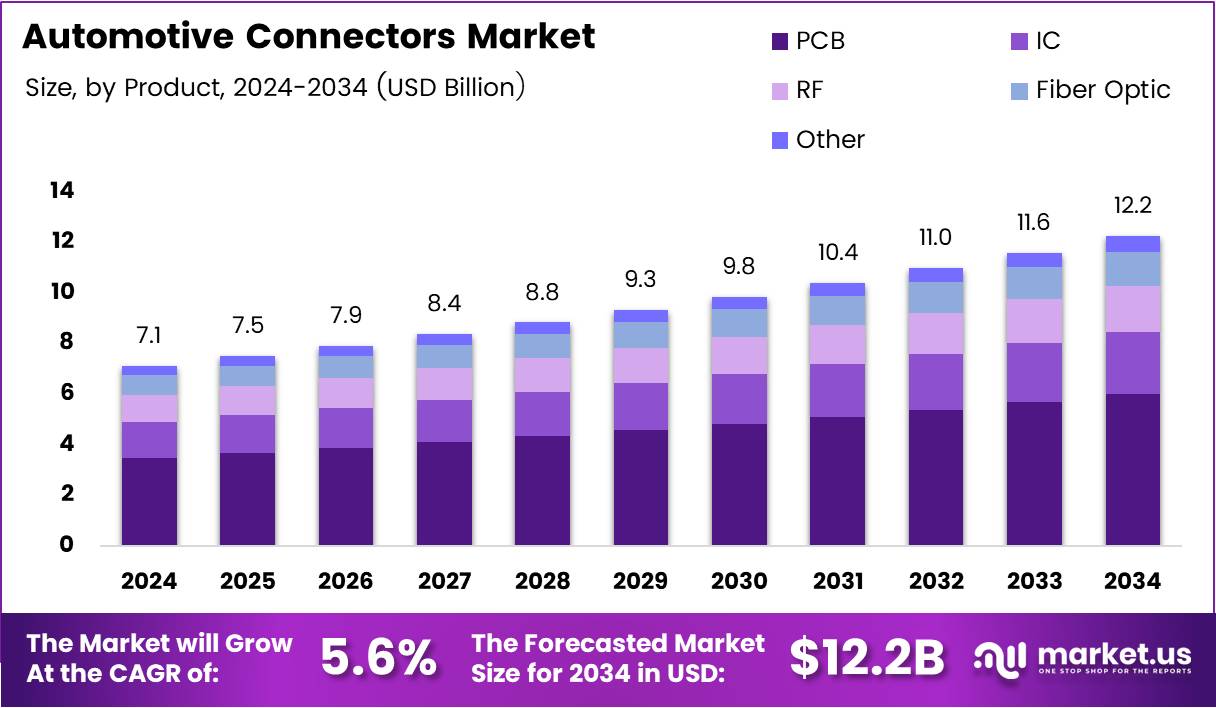

The Global Automotive Connectors Market was valued at USD 7.1 Billion in 2024 and is projected to reach USD 12.2 Billion by 2034. The market is expected to expand at a CAGR of 5.6% during 2025–2034. Rising vehicle electrification and connected mobility technologies continue accelerating demand for advanced automotive connectivity solutions globally.

Automotive connectors are precision-engineered components that enable electrical signal transfer and power distribution across vehicle systems. These devices connect sensors, electronic control units, infotainment modules, and powertrains throughout modern vehicles. Passenger cars, electric vehicles, and commercial transportation platforms increasingly depend on reliable connector systems for advanced electronic operations.

Get further insight into the global trends shaping the future of the Automotive Connectors industry: Request Free Sample

Passenger vehicle manufacturers, electric mobility companies, and commercial fleet operators continue driving demand for sophisticated automotive connectors. Automakers integrate these systems into infotainment platforms, safety technologies, climate controls, and autonomous driving systems. Consequently, advanced connectivity solutions support vehicle communication, operational efficiency, and passenger safety across modern automotive architectures.

Manufacturers increasingly develop lightweight, miniaturized, and high-speed connector technologies to support connected-car ecosystems and autonomous driving functions. These innovations improve signal integrity and reduce vehicle weight without compromising durability. Moreover, electric vehicle platforms require specialized high-voltage connectors capable of safely managing substantial power loads and rapid charging operations.

Governments worldwide continue promoting electric mobility adoption and smart transportation infrastructure development through supportive policies and regulatory frameworks. Regulatory agencies also enforce strict standards for vehicle safety, emissions, and interoperability. Consequently, automotive connector manufacturers invest heavily in sustainable materials and advanced engineering solutions to comply with evolving international requirements.

Global automotive consumer studies indicate growing interest in connected vehicle technologies among consumers worldwide. Approximately 25% of U.S. consumers are willing to invest in connected-car technologies. This growing acceptance supports demand for advanced automotive connectivity systems, encouraging manufacturers to develop high-bandwidth connectors supporting intelligent mobility and real-time vehicle communication.

Key Takeaways

- The global Automotive Connectors Market is expected to reach USD 12.2 Billion by 2034 from USD 7.1 Billion in 2024.

- The market is projected to expand at a CAGR of 5.6% during the forecast period from 2025 to 2034.

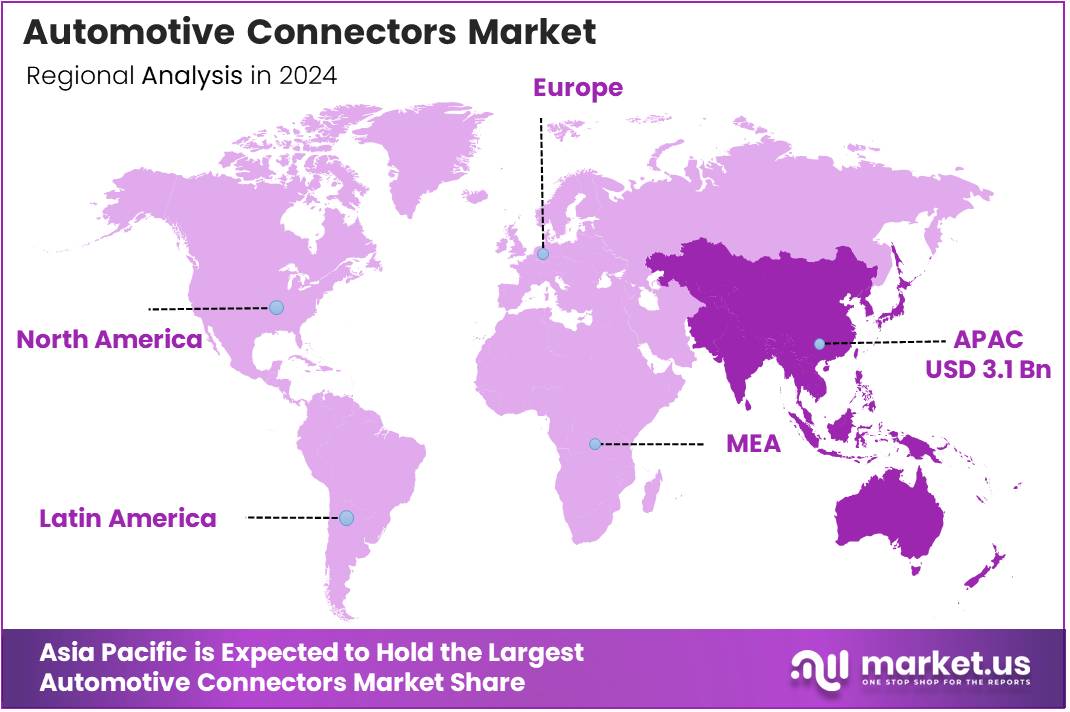

- Asia-Pacific dominated the regional landscape with a 44.9% market share valued at USD 3.1 Billion.

- PCB connectors led the product segment with a dominant 54.2% market share in 2024.

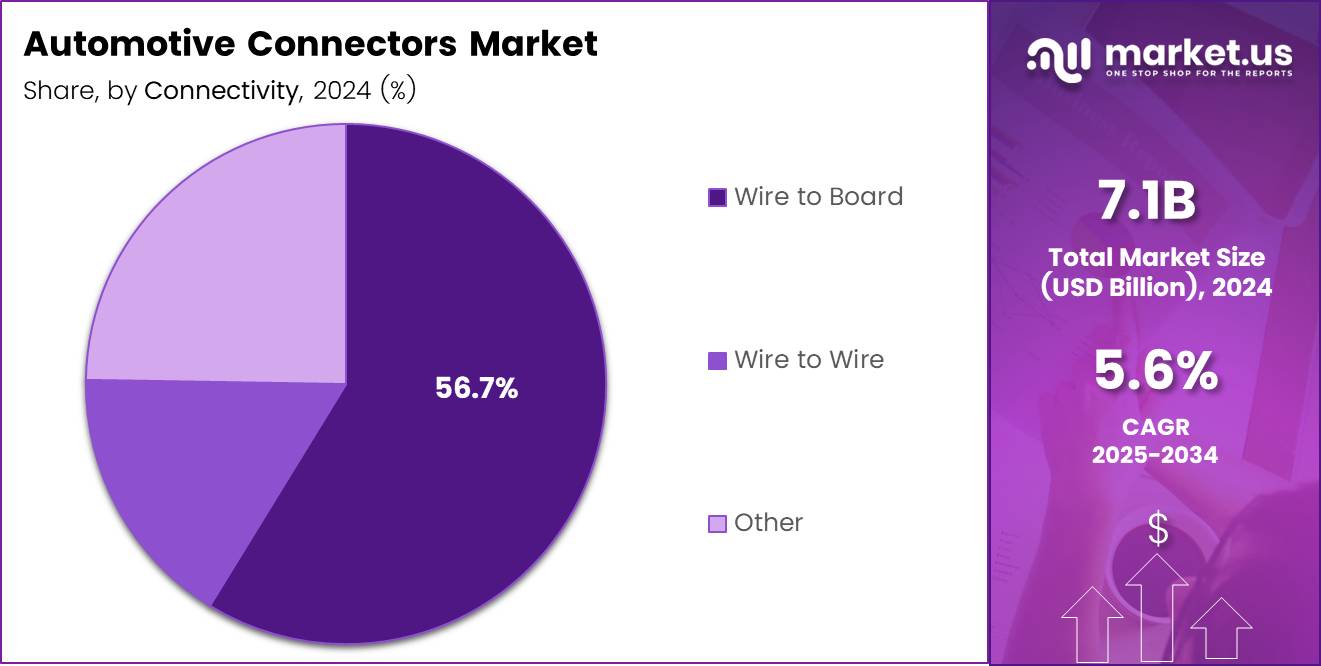

- Wire to Board connectivity accounted for a leading 56.7% share due to broad automotive integration.

- Passenger Cars represented 78.8% of vehicle segment demand in 2024.

- Safety & Security applications captured the highest application segment share at 36.3%.

- Electric vehicle adoption and autonomous driving technologies continue driving demand for high-speed connector systems.

Market Segmentation Overview

PCB connectors dominated the product segment with a 54.2% market share in 2024 because automakers widely integrate them across vehicle electronic systems. These connectors support engine management, infotainment, and transmission control applications efficiently. Consequently, manufacturers prefer PCB connectors for their cost-effectiveness, compatibility with automated production, and reliable operational performance.

IC and RF connectors continue gaining momentum as advanced vehicle electronics and wireless communication systems expand globally. IC connectors support sophisticated control units and autonomous technologies requiring precise signal transmission. Moreover, RF connectors enable GPS navigation, telematics, and vehicle-to-everything communication systems essential for connected-car ecosystems and intelligent transportation infrastructure.

Wire to Board connectors led the connectivity segment with a dominant 56.7% share due to broad applications across automotive wiring systems. These solutions provide reliable interfaces between electronic modules and wiring harnesses throughout vehicles. Therefore, automakers increasingly adopt these connectors to support efficient power distribution and signal transmission requirements.

Passenger Cars accounted for a leading 78.8% market share because modern vehicles integrate extensive electronic systems and advanced safety technologies. Consumers increasingly demand connected infotainment, climate control, and driver-assistance features requiring multiple connector interfaces. Additionally, commercial vehicles continue supporting market growth through demand for durable and vibration-resistant connectivity solutions.

Safety & Security applications captured a dominant 36.3% share in 2024 due to rising integration of airbag systems, electronic stability control, and advanced driver-assistance technologies. These systems require highly reliable connectors to ensure uninterrupted communication during critical operations. Consequently, manufacturers prioritize rigorous testing and quality assurance for safety-focused connectivity solutions.

Drivers

Growing integration of advanced driver-assistance systems strongly drives demand for ultra-reliable automotive connectors worldwide. Modern vehicles increasingly depend on radar sensors, cameras, and electronic control units for autonomous functionalities. Consequently, automakers prioritize connector technologies with superior vibration resistance and signal integrity to ensure safe and accurate vehicle operations.

Rapid vehicle electrification continues transforming automotive electrical architectures and connector requirements globally. Electric vehicles require specialized high-voltage connectors capable of safely handling substantial power loads during charging and driving operations. Moreover, hybrid powertrain systems depend on advanced connectivity solutions supporting battery management, energy distribution, and real-time system monitoring.

Use Cases

Automotive manufacturers use high-speed connectors within advanced infotainment and connected-car systems to support real-time communication and entertainment services. These systems enable seamless navigation, wireless connectivity, and telematics functionalities for drivers and passengers. Consequently, connector technologies enhance user experiences and improve overall vehicle intelligence across modern transportation platforms.

Electric vehicle manufacturers depend on specialized high-voltage connectors to support battery charging, energy transfer, and powertrain management operations. These connectors safely handle substantial electrical loads during fast-charging processes and daily driving conditions. Additionally, autonomous driving systems require high-bandwidth connectivity interfaces for rapid sensor data transmission and processing reliability.

Major Challenges

Developing durable automotive connectors capable of withstanding extreme temperatures, vibrations, and environmental conditions requires significant engineering investment. Manufacturers must conduct extensive testing to ensure long-term operational reliability across demanding vehicle lifecycles. Consequently, connector development costs continue rising alongside increasing technological complexity and evolving automotive performance requirements.

Complex international compliance standards create operational challenges for automotive connector manufacturers serving global markets. Different countries maintain varying regulations regarding electrical safety, environmental sustainability, and electromagnetic compatibility. Moreover, proprietary OEM specifications increase customization demands, limiting economies of scale and complicating supply chain management across international automotive industries.

Business Opportunities

Autonomous driving platforms present substantial growth opportunities for manufacturers developing high-bandwidth automotive connector solutions. Self-driving systems require ultra-fast data transmission capabilities to process information from multiple sensors simultaneously. Consequently, companies investing in advanced connectivity technologies can strengthen competitive positioning within emerging intelligent mobility markets.

Expanding electric vehicle charging infrastructure creates strong demand for specialized high-power connectors supporting rapid energy transfer operations. Manufacturers increasingly develop modular and smart connector systems capable of improving operational efficiency and predictive maintenance capabilities. Additionally, sustainable and recyclable materials present new opportunities aligned with green manufacturing and environmental compliance initiatives.

Regional Analysis

Asia-Pacific dominated the Automotive Connectors Market with a 44.9% share valued at USD 3.1 Billion in 2024. Strong automotive production capabilities across China, Japan, South Korea, and India supported regional leadership. Consequently, government support for electric mobility and smart transportation infrastructure accelerated advanced automotive connector demand throughout the region.

North America emerged as a significant market due to rising adoption of advanced driver-assistance systems, electric vehicles, and connected-car technologies. Automakers across the United States and Canada continue investing heavily in intelligent automotive architectures and charging infrastructure. Moreover, strict safety regulations support long-term demand for high-performance automotive connectivity solutions.

Recent Developments

- February 2024 — FIT Voltaira Group acquired Auto-Kabel Group to strengthen automotive connectivity capabilities and expand European market presence.

- November 2025 — Molex expanded its eHV High-Voltage Connector Portfolio to support electric and hybrid vehicle charging applications.

- October 2025 — KYOCERA formed a business alliance with Japan Aviation Electronics Industry to accelerate advanced connector technology innovation.

- Automotive connector manufacturers increasingly invested in sustainable materials and high-density connectivity technologies supporting autonomous mobility systems.

Conclusion

The Automotive Connectors Market demonstrates strong long-term growth potential supported by electrification trends, connected mobility adoption, and increasing vehicle electronics integration. Automotive manufacturers continue investing in advanced connectivity technologies to support intelligent transportation systems and autonomous driving capabilities. Consequently, demand for high-performance automotive connectors will continue expanding globally.

PCB connectors, Wire to Board connectivity systems, and Passenger Cars continue dominating industry demand due to widespread automotive electronic integration. Asia-Pacific maintains regional leadership through strong automotive manufacturing and government support for electric mobility infrastructure. Meanwhile, North America continues strengthening demand for advanced safety and connected vehicle technologies.

Manufacturers must prioritize lightweight designs, sustainable materials, and high-bandwidth connectivity solutions to remain competitive within evolving automotive markets. Strategic investment in autonomous driving technologies and electric vehicle infrastructure will further support long-term market growth. The global Automotive Connectors Market is projected to reach USD 12.2 Billion by 2034.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)