Table of Contents

Introduction

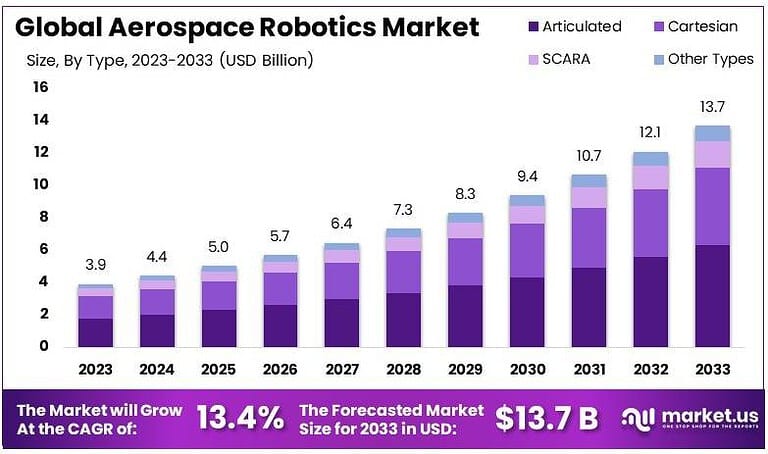

The Global Aerospace Robotics Market is projected to reach USD 13.7 billion by 2033, rising from USD 3.9 billion in 2023, expanding at a CAGR of 13.4%. Growth is driven by increasing automation in aerospace manufacturing, rising demand for precision in assembly, and the adoption of robotics for inspection and maintenance. The integration of AI, IoT, and advanced robotic arms is revolutionizing production efficiency, reducing errors, and enhancing safety standards across the aerospace sector.

How Growth is Impacting the Economy

The expansion of aerospace robotics is significantly contributing to economic growth by modernizing aerospace manufacturing and strengthening global competitiveness. Robotics-driven efficiency reduces production costs, increases throughput, and accelerates aircraft delivery timelines, which directly impacts revenue in commercial and defense aviation sectors.

The industry is also fueling investment in robotics, AI, and sensor technologies, creating high-value jobs in engineering, programming, and system integration. Governments benefit from enhanced exports and stronger aerospace supply chains, while regional economies with advanced aerospace industries, such as the U.S., Europe, and Asia Pacific, see stronger GDP contributions. By fostering innovation, the aerospace robotics market is reshaping the future of industrial automation and defense capabilities.

➤ Unlock growth! Get your sample now! – https://market.us/report/aerospace-robotics-market/free-sample/

Impact on Global Businesses

The adoption of aerospace robotics is driving operational changes in manufacturing and maintenance. Businesses face rising initial investment costs for advanced robotic systems, sensors, and AI integration, but benefit from long-term reductions in labor and maintenance costs. Supply chains are shifting toward specialized component suppliers for robotic arms, sensors, and AI-driven systems.

Sector-specific impacts include commercial aviation improving precision assembly and reducing defects, defense aerospace enhancing inspection and quality control, and maintenance providers adopting robotics for aircraft servicing and repair. While costs and technical complexity remain challenges, the efficiency and scalability benefits outweigh the hurdles.

Strategies for Businesses

- Invest in robotics-driven precision assembly to reduce errors and downtime.

- Collaborate with AI and IoT providers for advanced automation capabilities.

- Expand the use of robotics into maintenance, repair, and inspection activities.

- Focus on workforce reskilling to support human-robot collaboration.

- Strengthen cybersecurity frameworks to protect robotic systems from cyber threats.

Key Takeaways

- Market expected to reach USD 13.7 billion by 2033, growing at 13.4% CAGR.

- Automation reduces costs, enhances precision, and accelerates aircraft production.

- North America and Europe remain key hubs for adoption and innovation.

- High initial investment and technical complexity are major challenges.

- AI, IoT, and predictive maintenance integration create strong growth potential.

Analyst Viewpoint

The aerospace robotics market is rapidly expanding as manufacturers and defense players prioritize efficiency and precision. Currently, adoption is strongest in assembly, welding, and drilling, while future growth lies in predictive maintenance and autonomous inspection. With rising investments in AI-driven robotics and global aerospace demand, the market outlook is highly positive, positioning robotics as a critical enabler of next-generation aerospace capabilities.

➤ Stay ahead—secure your copy now – https://market.us/purchase-report/?report_id=129680

Use Case and Growth Factors

| Use Case | Growth Factors Driving Adoption |

|---|---|

| Aircraft Assembly Automation | Demand for precision and reduced manufacturing errors |

| Robotic Drilling & Welding | Need for consistent, high-quality structural assembly |

| Inspection & Maintenance Robots | Rising demand for predictive and automated servicing |

| Composite Material Handling | Growth in lightweight aircraft component adoption |

| Defense Aerospace Applications | Focus on advanced automation for mission readiness |

Regional Analysis

North America leads the market, supported by strong aerospace manufacturing in the U.S. and rising defense spending. Europe follows closely with automation adoption in countries such as Germany, France, and the U.K., driven by established aerospace players. Asia Pacific is emerging as the fastest-growing region, with China, Japan, and India investing in aerospace production and automation technologies. The Middle East is increasingly adopting robotics in defense and maintenance operations, while Latin America sees steady integration in aircraft servicing.

Business Opportunities

Opportunities exist in robotic solutions for composite material handling, predictive maintenance, and autonomous aircraft inspection. Startups and SMEs can capitalize by developing cost-effective robotic systems tailored for mid-sized aerospace firms. Expanding defense budgets worldwide open avenues for robotics in unmanned systems and military aircraft maintenance. Additionally, partnerships between aerospace OEMs and robotics firms present significant growth potential for innovation-driven projects.

Key Segmentation

The market is segmented by application into assembly, drilling, welding, inspection, and maintenance. By type, it includes articulated, SCARA, and collaborative robots. Technology adoption spans AI integration, IoT-enabled robotics, and predictive analytics. End-users include commercial aviation, defense aerospace, and maintenance service providers. These segments reflect diverse adoption trends across the aerospace value chain.

Key Player Analysis

Market leaders focus on R&D in AI-enabled robotics, advanced sensors, and collaborative systems to enhance production efficiency. Partnerships with aerospace OEMs and defense contractors strengthen market presence, while acquisitions expand technological portfolios. Investment in human-robot collaboration and predictive maintenance solutions ensures long-term growth. Balancing innovation with affordability remains central to competitive positioning.

- ABB Ltd.

- KUKA AG

- FANUC Corporation Company Profile

- Yaskawa Electric Corporation

- Siemens AG

- Lockheed Martin Corporation

- The Boeing Company Company Profile

- Northrop Grumman Corporation Company Profile

- Airbus Group

- Teradyne, Inc.

- MHI (Mitsubishi Heavy Industries)

- Universal Robots A/S

- Electroimpact, Inc.

- Kawasaki Robotics

- Other Key Players

Recent Developments

- In 2023, aerospace firms expanded robotics use in drilling and assembly lines.

- AI-driven inspection robots gained traction in predictive maintenance.

- Collaborative robots were introduced to enhance workforce productivity.

- Defense agencies increased investment in robotics for mission-critical tasks.

- Automation suppliers launched lightweight robotic arms for composite handling.

Conclusion

The aerospace robotics market is set for robust growth, fueled by rising demand for automation, AI integration, and precision engineering. With strong adoption across commercial and defense aviation, robotics will play a pivotal role in shaping the next decade of aerospace innovation.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)