Table of Contents

Media and Entertainment Market Size

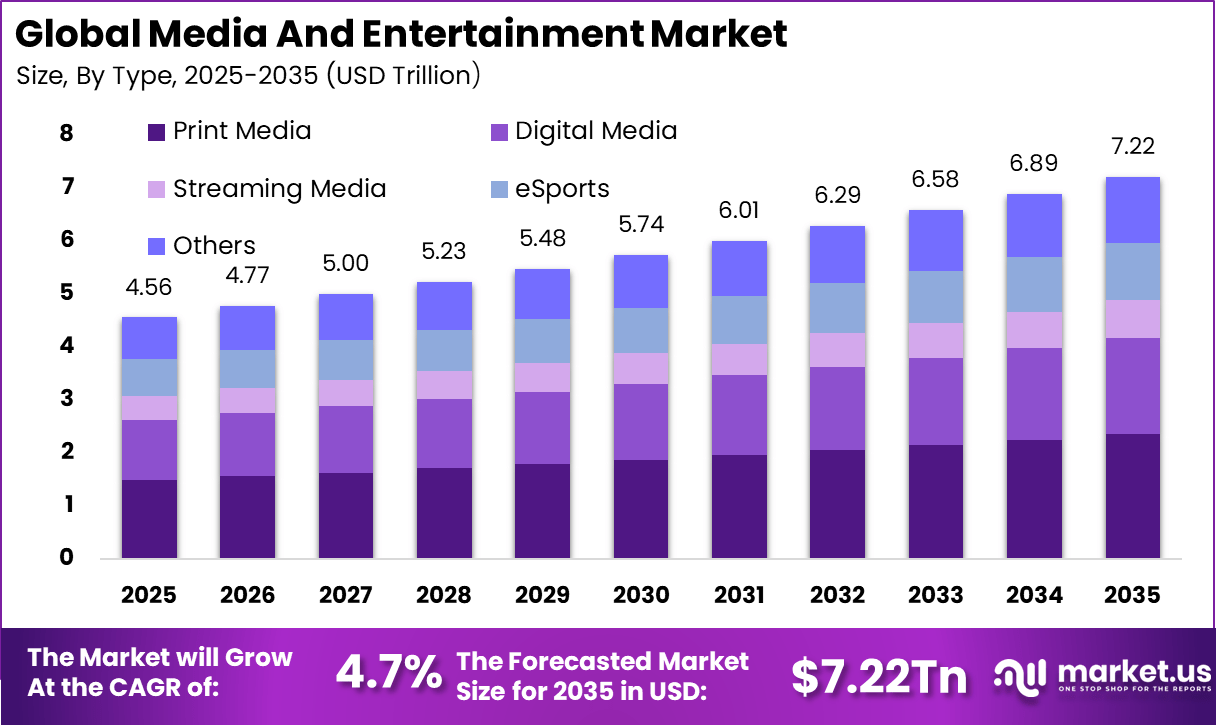

The Global Media and Entertainment Market represents a massive, resilient investment landscape, expanding from USD 4.56 trillion in 2025 to nearly USD 7.22 trillion by 2035 at a steady CAGR of 4.7%. North America leads the market with more than 37.1% share and USD 1.69 trillion in revenue, reflecting continued dominance in premium content creation, streaming platforms, and digital media monetization models.

The media and entertainment market covers the creation, distribution, and consumption of content across television, film, music, gaming, live events, and digital platforms. This market has shifted from linear and physical formats toward on demand, mobile first, and interactive experiences. Content is increasingly delivered through connected devices, cloud platforms, and data driven recommendation systems.

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.5 trillion |

| Forecast Revenue (2035) | USD 7.2 trillion |

| CAGR(2026-2035) | 4.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

Key driver factors shaping this market include widespread broadband access, growing use of smartphones and connected TVs, and rising consumer preference for personalized and flexible content consumption. Media and entertainment is now positioned as a digital experience economy where engagement, convenience, and content relevance define success.

Key Takeaway

- In 2025, print media remained the leading segment in the global media and entertainment market, accounting for 32.7% of the total share.

- In 2025, subscription based models became the dominant revenue stream, capturing 43.6% of global market revenue.

- In 2025, smartphones and tablets were the primary devices for media consumption, representing 40.8% of total usage.

- In 2025, the US media and entertainment market reached USD 1.43 trillion, supported by a steady CAGR of 3.7%.

- In 2025, North America held a dominant regional position, accounting for more than 37.1% of the global market share.

Driver Analysis

A primary driver of the media and entertainment market is the rapid adoption of digital distribution channels. Streaming platforms, social media, and direct to consumer models allow content to reach global audiences instantly. This reduces reliance on traditional distribution constraints and enables continuous content availability. As consumers favor on demand access, digital delivery continues to gain importance.

Another important driver is growth in content consumption across demographics. Media usage has expanded beyond scheduled viewing to include short form video, interactive content, and immersive formats. Increased screen time across devices supports higher content demand. This sustained consumption drives investment across production and distribution ecosystems.

Restraint Analysis

A key restraint in the media and entertainment market is rising content production and licensing costs. High quality content requires significant investment in talent, technology, and marketing. Profitability pressure increases when audience attention becomes fragmented across platforms. Managing costs while maintaining content quality remains a constraint.

Another restraint is regulatory and compliance complexity. Content providers must navigate copyright rules, regional content regulations, and data protection requirements. Compliance increases operational overhead and can limit cross border distribution. Regulatory variability remains a challenge for global media operations.

Opportunity Analysis

A significant opportunity in the media and entertainment market lies in personalization and data driven content strategies. Advanced analytics allow platforms to tailor content recommendations and advertising to individual preferences. Personalization improves engagement and retention. This capability creates competitive differentiation and higher lifetime value.

Another opportunity is the expansion of immersive and interactive formats. Virtual experiences, live streaming, and audience participation features are reshaping content engagement. These formats attract younger audiences and open new monetization models. Innovation in experience design supports long term growth.

Challenge Analysis

A major challenge for the media and entertainment market is audience fragmentation and attention competition. Consumers have access to abundant content choices across platforms. Capturing and retaining attention requires continuous innovation and strong brand identity. Content discoverability remains a persistent challenge. Another challenge is managing digital rights and monetization consistency. Content is consumed across multiple devices and regions. Ensuring fair monetization while preventing unauthorized distribution is complex. Rights management remains a critical operational issue.

Emerging Trends Analysis

An emerging trend in the media and entertainment market is the rise of creator driven ecosystems. Independent creators are gaining influence through digital platforms. This trend decentralizes content creation and reshapes traditional studio models. Creator economies are becoming an integral part of the market.

Another trend is convergence between media, gaming, and social interaction. Entertainment experiences increasingly blend gameplay, social engagement, and live content. This convergence creates new hybrid formats. Cross format innovation is shaping future consumption patterns.

Growth Factors Analysis

One of the key growth factors for the media and entertainment market is increasing global internet penetration. As connectivity improves, access to digital content expands across regions. This broadens the addressable audience for content providers. Connectivity driven expansion supports sustained growth.

Another growth factor is ongoing technological advancement in content production and delivery. Cloud workflows, advanced editing tools, and efficient distribution systems lower barriers to entry. These improvements increase content volume and diversity. Technology driven efficiency continues to fuel market expansion.

Key Market Segments

By Type

- Print Media

- Newspaper

- Magazines

- Billboards

- Banners, Leaflets, and Flyers

- Other Print Media

- Digital Media

- Television

- Music and Radio

- Electronic Signage

- Mobile Advertising

- Podcasts

- Other Digital Media

- Streaming Media

- OTT Streaming

- Live Streaming

- Video Games and eSports

- Virtual / Augmented Reality Content

By Revenue Model

- Advertising

- Subscription

- Pay-Per-View / Transactional

- Licensing and Merchandising

By Device Platform

- Smartphones and Tablets

- Smart TVs and Set-top Boxes

- PCs and Laptops

- Gaming Consoles

- VR/AR Headsets

Top Key Players in the Market

- News Corporation

- Comcast Corporation

- Walt Disney Company

- Warner Bros. Discovery, Inc.

- Paramount Global

- Netflix, Inc.

- com, Inc. (Prime Video)

- Alphabet Inc. (YouTube)

- Apple Inc.

- Sony Group Corporation

- Tencent Holdings Ltd.

- Bertelsmann SE and Co. KGaA

- ByteDance

- Axel Springer SE

- Reliance Industries

- Roku, Inc.

- WPP plc

- Omnicom Group Inc.

- Publicis Groupe

- Spotify Technology S.A.

- Electronic Arts Inc.

- Nintendo Co. Ltd.

- Activision Blizzard, Inc.

- Others

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)