Table of Contents

Introduction

According to Semiconductor IP Statistics, Semiconductor Intellectual Property (IP) consists of pre-made and verified elements employed in the production of semiconductor chips. These elements, such as processors and memory units, are safeguarded by intellectual property protections and reduce the workload and expenses for chip designers.

Semiconductor IP is used in various fields, including consumer electronics, automotive technology, and industrial automation, among others. It can be tailored to specific needs, and its dependability is confirmed through rigorous testing. Users have flexibility in licensing Semiconductor IP, with options like royalties, permanent licenses, and subscriptions.

Editor’s Choice

- In 2023, the Semiconductor IP market revenue stood at USD 6.4 billion.

- Royalty-based IP sources claim the majority market share, commanding a substantial 70%.

- Arm Holdings Ltd. stands as the dominant leader with a substantial 41% market share, reflecting its prominent position in the industry.

- North America leads the way with a substantial 31.0% market share, reflecting its prominence in the industry.

- Soft Semiconductor Intellectual Property (SIP) is typically provided in high-level languages like RTL, C++, Verilog, or VHDL, or sometimes as a netlist.

- Connectivity SIP, also called standards SIP, adheres to specific specifications like USB, PCI, IEEE1394 (known as “Firewire”), IrDA, Bluetooth, or 802.11.

- According to the 2020 IPnest Semiconductor Design IP Report, Arteris IP held the 12th position among the world’s largest semiconductor IP companies.

Semiconductor Industry Overview

- The semiconductor industry has undergone remarkable growth and transformation between 1996 and 2019, marked by significant percentage changes across various metrics.

- Total semiconductor trade surged from $294 billion to a staggering $1.655 trillion, representing a remarkable 463% increase.

- Cell phone subscriptions per 100 people witnessed an exponential rise, soaring from 2 to 104.9, a staggering 3,371% increase.

- Internet users per 100 people displayed an even more impressive growth, surging from 1.19 to 49.7, a remarkable 4,076% jump.

- The global semiconductor market’s total revenue increased substantially from $132 billion to $412 billion, marking a 212% rise.

- Semiconductor production experienced substantial expansion, with the total number of units produced soaring from 215 billion to 932 billion, a significant 333% increase.

Semiconductor Intellectual Property (IP) Market Overview

Global Semiconductor Intellectual Property (IP) Market Size

- The global Semiconductor Intellectual Property (IP) market is exhibiting a consistent and promising growth trajectory, with revenues projected to increase steadily over the next decade at a CAGR of 6.7%.

- In 2022, the market revenue stood at USD 6.0 billion, marking the starting point of this upward trend.

- As we progress into the late 2020s, the market is projected to achieve even greater heights, with revenue figures reaching USD 8.7 billion in 2028, USD 9.3 billion in 2029, and USD 9.8 billion in 2030.

- Looking further into the future, the Semiconductor IP market is anticipated to breach the USD 10 billion mark by 2031, reaching USD 10.5 billion, and continue its robust growth, with projections indicating revenues of USD 11.3 billion in 2032.

Global Semiconductor Intellectual Property (IP) Market Share – By IP Source

- The global market for Semiconductor Intellectual Property (IP) is segmented by IP source, with two primary categories.

- Royalty-based IP sources claim the majority market share, commanding a substantial 70%.

- In this model, users pay royalties based on their production volume using the IP, making it a prevalent choice in the industry.

- On the other hand, licensing models hold a 30% share of the market.

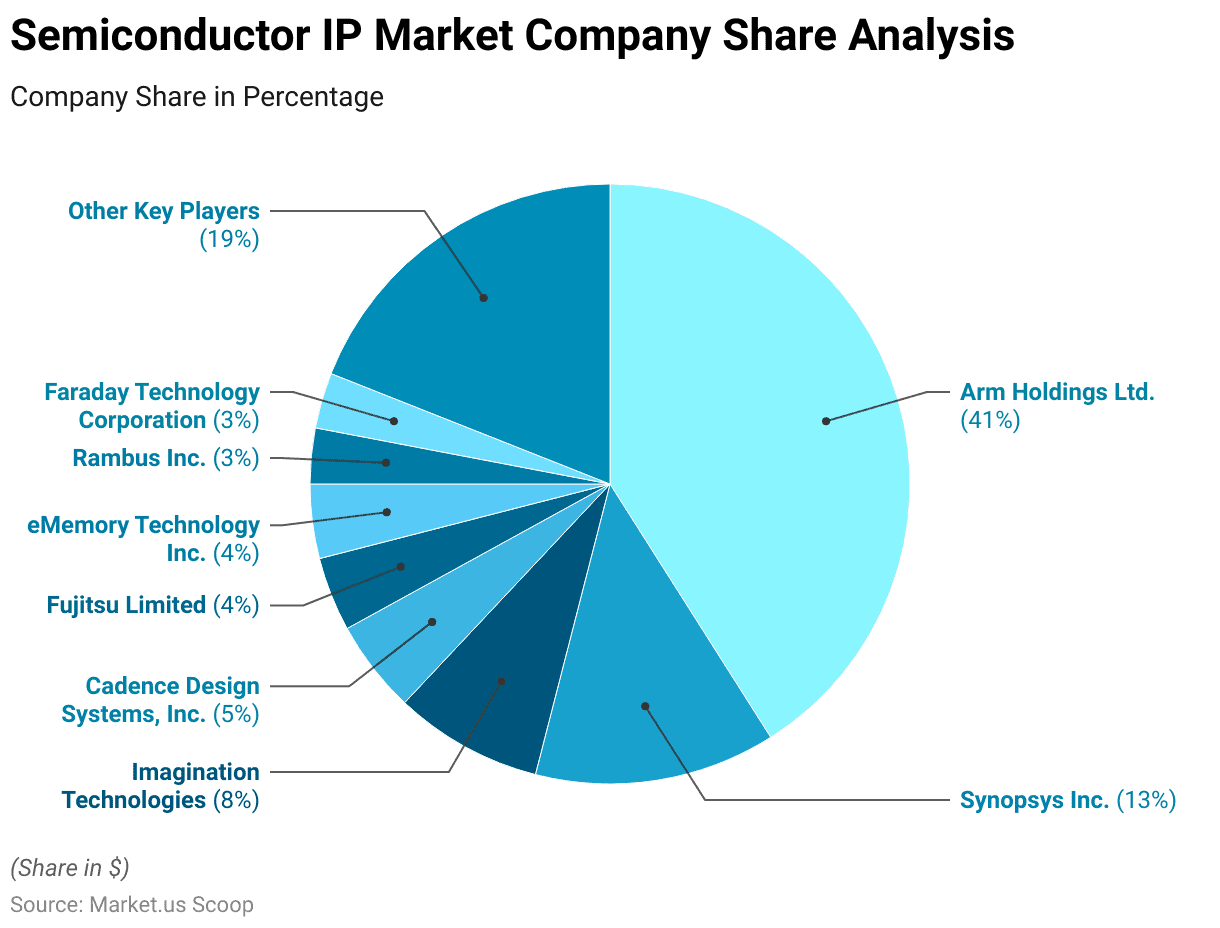

Key Players in the Global Semiconductor Intellectual Property (IP) Market

- In the global Semiconductor Intellectual Property (IP) market, several key players hold significant market shares.

- Arm Holdings Ltd. stands as the dominant leader with a substantial 41% market share, reflecting its prominent position in the industry.

- Following Arm Holdings, Synopsys Inc. holds a notable 13% market share, underscoring its influence in the Semiconductor IP sector.

- Imagination Technologies, Cadence Design Systems, Inc., and Fujitsu Limited each contribute significantly with 8%, 5%, and 4% market shares, respectively.

- eMemory Technology Inc., Rambus Inc., and Faraday Technology Corporation also make valuable contributions, each holding 4%, 3%, and 3% of the market share, respectively.

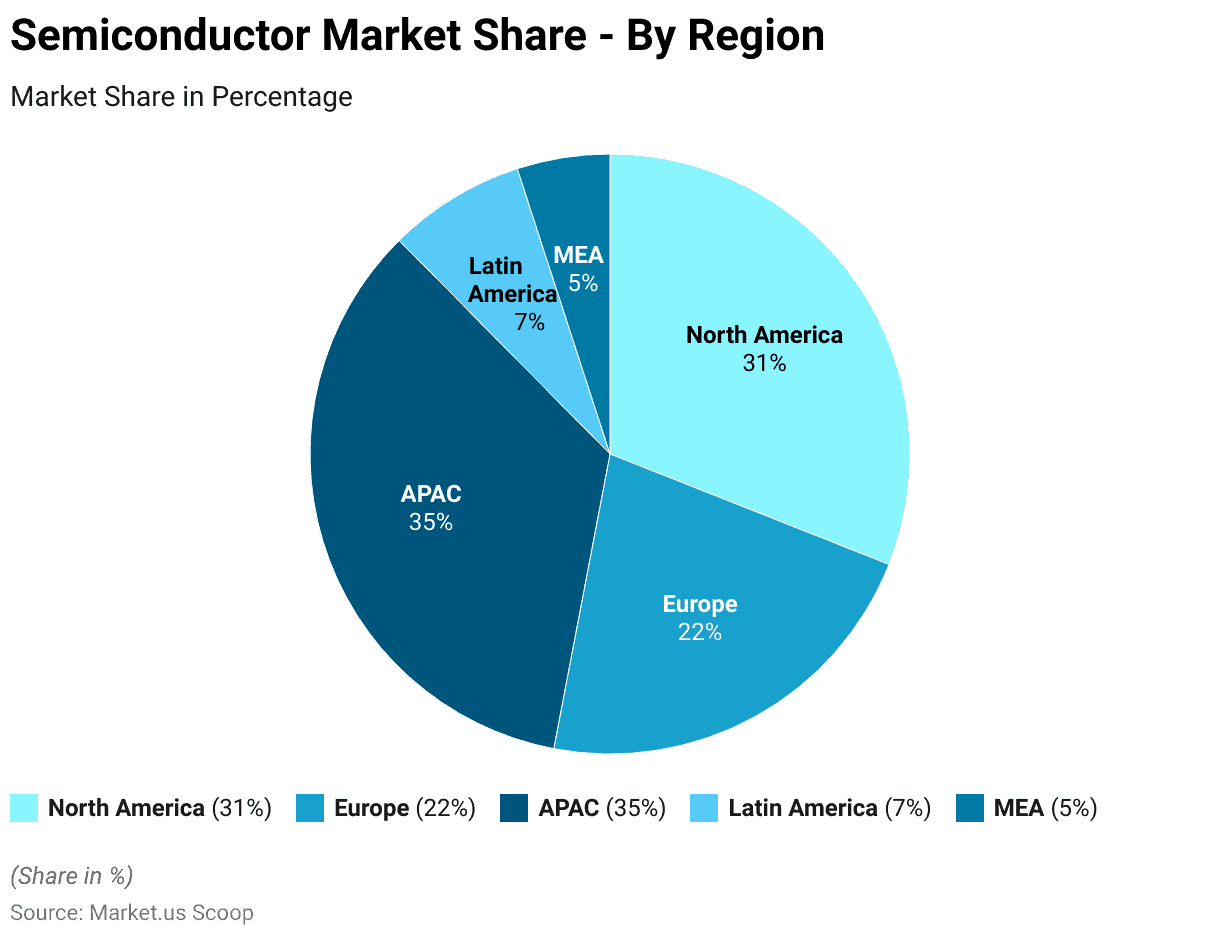

Regional Analysis of the Global Semiconductor Intellectual Property (IP) Market

- The global market for Semiconductor Intellectual Property (IP) is distributed across different regions, each contributing to its overall composition.

- North America leads the way with a substantial 31.0% market share, reflecting its prominence in the industry.

- Europe follows closely behind with a significant 22.0% market share, indicating a robust presence in the semiconductor IP sector.

- The Asia-Pacific (APAC) region commands the largest portion of the market at 34.6%, showcasing its dominance as a key hub for semiconductor IP development and consumption.

- Latin America and the Middle East & Africa (MEA) regions hold 7.4% and 5.0% market shares, respectively, contributing to the global landscape with their unique market dynamics.

Types of Semiconductor IP

Soft SIP

- Soft Semiconductor Intellectual Property (SIP) is typically provided in high-level languages like RTL, C++, Verilog, or VHDL, or sometimes as a netlist.

- Soft SIP is portable, allowing it to be moved between foundry processes, but it’s not tailored to a specific process technology.

- As a result, its power, performance, and area characteristics are uncertain until applied to a specific process and library.

- Soft SIP’s value primarily comes from its functionality, reusability, availability, and potential compliance with industry standards like USB 1.0, ARM AMBA 1.0, PCI, or IEEE 802.11.

Hard SIP

- Hard Semiconductor Intellectual Property (SIP) is typically provided in GDSII format, often with associated EDA views or models, and it’s specifically optimized for a particular foundry process.

- In some cases, it may be formatted as a “bit-stream” for FPGA use.

- Hard SIP usually includes a detailed datasheet similar to that of a standalone IC, covering aspects like power consumption, speed, and physical dimensions.

- Examples of hard SIP include processors, standard cells, memory modules, phase-locked loops (PLLs), I/O interfaces, and analog components.

Foundation SIP

- Foundation SIP typically comprises standard cell libraries, PLLs, I/Os, and compact macros.

- It’s commonly provided as hard SIP and often comes as a bundled package, rather than individual components.

- General-purpose foundation SIP might be offered for free by suppliers and foundries to attract customers, while specialized foundation SIP, like those optimized for low power or high performance, is priced based on customer requirements, customization level, and supported process technology.

Memory SIP

- Memory SIP, typically in hard SIP format, is specialized for specific process nodes and may come with memory compilers.

- It covers various memory types like SRAM, non-volatile memory (Flash, EEPROM), DRAM, and 1T-SRAM.

- High-density memory often includes redundancy for improved yield and error correction, along with integrated testing and repair capabilities.

- SRAM variants comprise single-port, dual-port, multi-port, CAMs, and customized designs focusing on area, power, or speed optimization.

- Memory can be generated using compiler tools tailored to foundry and process needs, enabling users to customize aspects like aspect ratio and power management.

Connectivity SIP

- Connectivity SIP, also called standards SIP, adheres to specific specifications like USB, PCI, IEEE1394 (known as “Firewire”), IrDA, Bluetooth, or 802.11.

- It can be provided in either soft or hard formats and is often tied to a particular version of the supported standard, which may undergo continuous updates.

- While “connectivity” typically pertains to off-chip interfaces, it can also encompass on-chip buses like AMBA or OCP.

Top Semiconductor Vendors

- According to the 2020 IPnest Semiconductor Design IP Report, Arteris IP held the 12th position among the world’s largest semiconductor IP companies.

- Notably, in the Chip Infrastructure market category, which mainly focuses on on-chip interconnect IP, Arteris IP secured 2nd place, just behind Arm Holdings.

- Arteris IP achieved remarkable year-over-year revenue growth, ranking as the second-highest in this regard among the top 15 semiconductor IP companies.

- With $34 million in revenue in 2019, Arteris IP garnered a substantial 31.3% share of the interconnect IP market.

- This growth stemmed from its success across global regions and its portfolio of products, which includes FlexNoC Interconnect, Ncore Cache Coherent Interconnect, and CodaCache Last Level Cache IP.

Recent Developments in Semiconductor IP

- Faraday introduced its LPDDR4X and LPDDR4X combo IP in June 2021, enabling speeds of up to 42Gbps.

- This IP is designed to work seamlessly with Samsung’s 14nm LPC processes and provides two pre-optimized configurations to support both in-line and corner-edge placement scenarios.

- In May 2021, Cadence Design Systems, Inc. introduced power-efficient Intellectual Property (IP) designed to comply with the PCI Express 5.0 standard.

- This IP is specifically crafted for applications in hyper-scale computing, networking, storage, and those utilizing TSMC N5 process technology.

- The complete PCIe 5.0 technology package consists of a corresponding controller, PHY, and verification IP (VIP), all strategically aimed at System-On-Chip (SoC) designs that necessitate substantial bandwidth capabilities.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)