Table of Contents

Market Overview

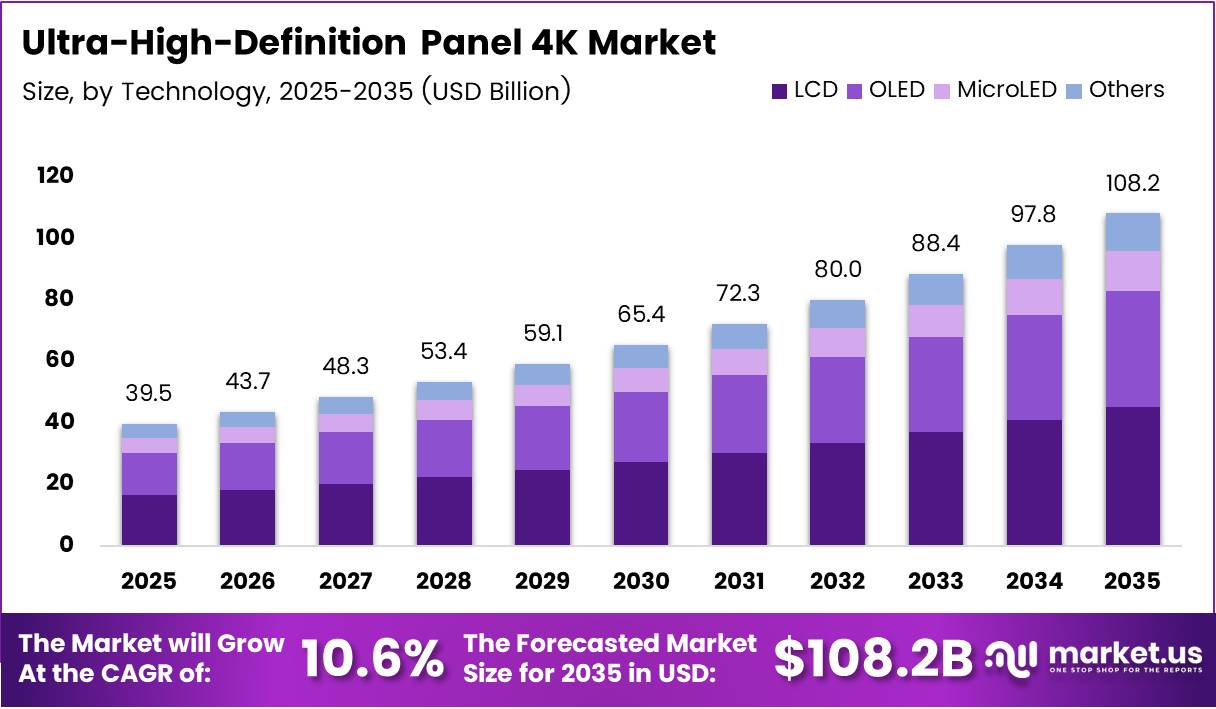

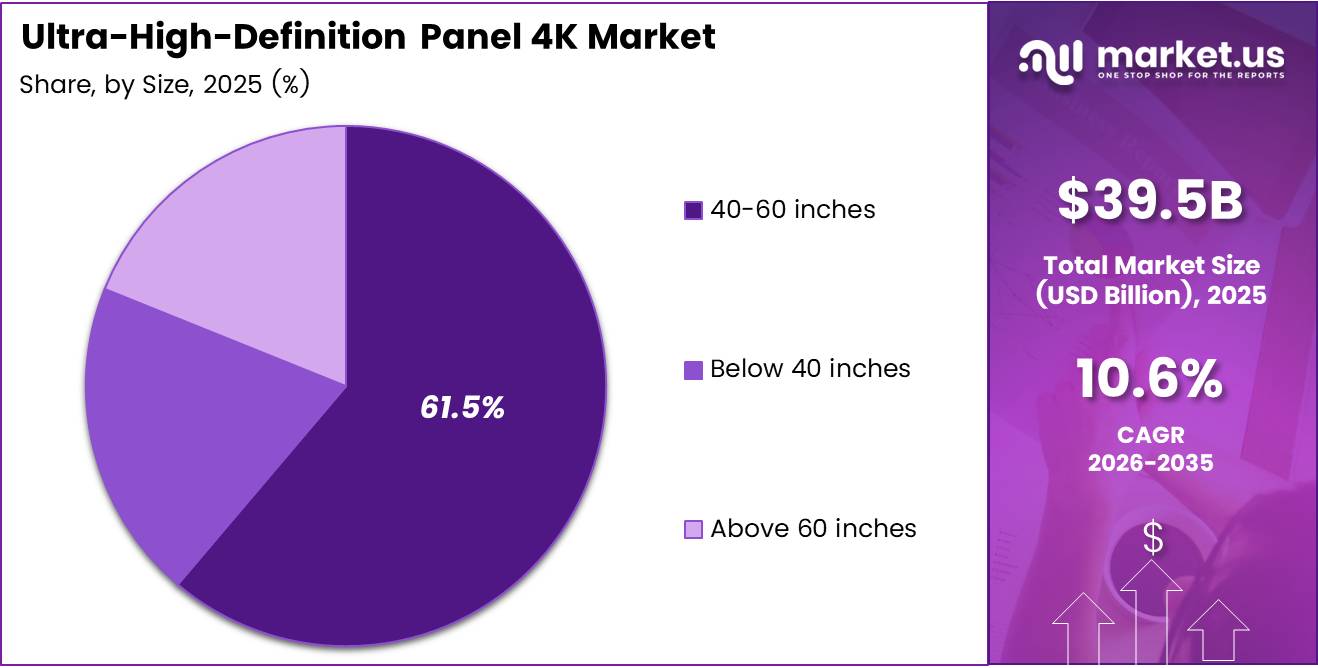

The Ultra-High-Definition Panel 4K Market was valued at USD 39.5 Billion in 2025. Analysts expect the industry to reach USD 108.2 Billion by 2035, expanding at a 10.6% CAGR between 2026 and 2035. Strong demand for higher-resolution displays across consumer electronics and commercial environments continues to accelerate global market expansion.

Ultra-high-definition 4K panels deliver a resolution of 3840 × 2160 pixels, providing sharper images and improved color accuracy. Manufacturers integrate these panels into televisions, monitors, digital signage systems, and medical displays. Consumer electronics brands, healthcare providers, and automotive manufacturers increasingly rely on this technology for visual clarity and immersive user experiences.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Consumer electronics companies drive the largest share of demand for ultra-high-definition displays. Smart TV manufacturers, gaming monitor brands, and streaming device makers use these panels to deliver premium visual experiences. Additionally, industries such as healthcare imaging, automotive infotainment, and corporate digital signage adopt high-resolution panels for professional and operational purposes.

Consumer electronics companies drive the largest share of demand for ultra-high-definition displays. Smart TV manufacturers, gaming monitor brands, and streaming device makers use these panels to deliver premium visual experiences. Additionally, industries such as healthcare imaging, automotive infotainment, and corporate digital signage adopt high-resolution panels for professional and operational purposes.

Display manufacturers continuously improve performance through innovations in OLED structures, mini-LED backlighting, and AI-powered image processing. Companies integrate intelligent upscaling engines that optimize non-4K content automatically. Consequently, these technological upgrades enhance viewing quality while extending the lifespan and efficiency of advanced display panels.

Government policies supporting advanced electronics manufacturing also contribute to market expansion. Asian countries encourage semiconductor and display production through financial incentives and infrastructure investment. These initiatives strengthen regional supply chains and ensure stable component availability, allowing manufacturers to scale panel fabrication capacity efficiently.

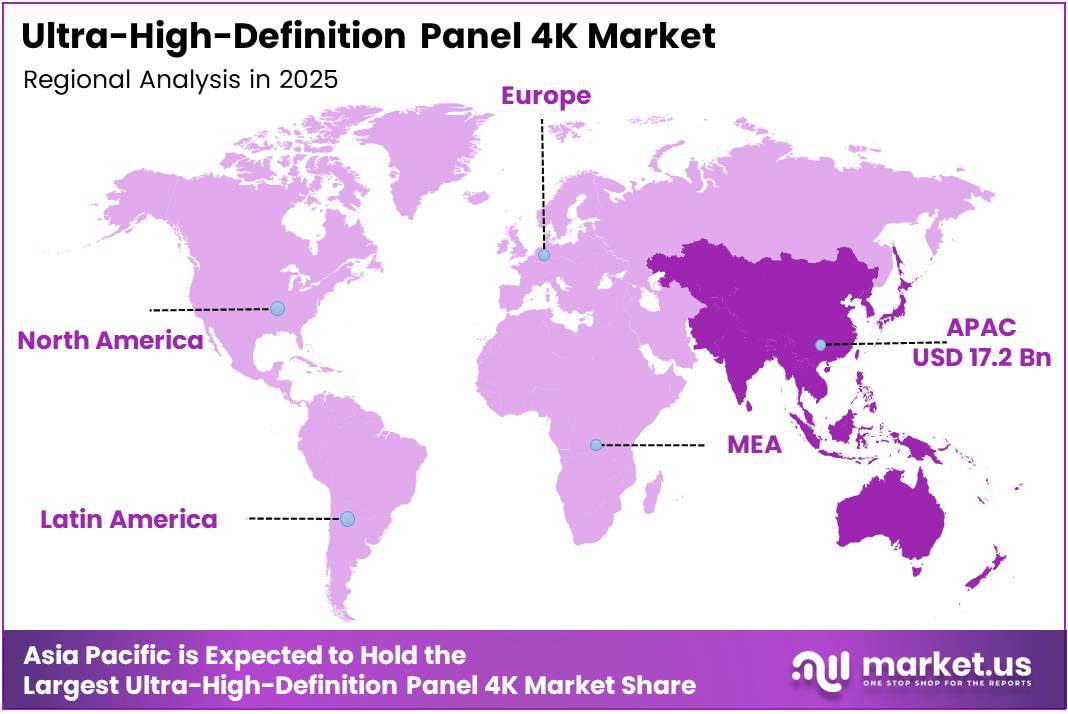

Industry statistics highlight the accelerating adoption of 4K displays. Asia Pacific accounted for 43.60% of the market, valued at USD 17.2 Billion in 2025. This dominance reflects strong manufacturing capacity and consumer electronics demand. The LCD technology segment also held 62.6% share, indicating cost-efficient production still drives mainstream display adoption globally.

Key Takeaways

- The market is valued at USD 39.5 Billion in 2025 and projected to reach USD 108.2 Billion by 2035.

- The industry is expanding at a CAGR of 10.6% during the forecast period.

- LCD technology dominates the market with 62.6% share due to mature manufacturing infrastructure.

- 4K UHD resolution holds 82.9% share because streaming platforms widely distribute native 4K content.

- The 40–60 inches panel size segment leads with 61.5% market share.

- Consumer Electronics represents 62.3% of total application revenue.

- Asia Pacific leads globally with 43.60% share valued at USD 17.2 Billion in 2025.

Market Segmentation Overview

The technology segment shows LCD displays dominating the market with a 62.6% share. This leadership results from mature manufacturing infrastructure and low production costs. Television manufacturers and commercial display providers prefer LCD panels because they deliver reliable performance while maintaining competitive pricing in high-volume display categories.

Resolution segmentation highlights the strong position of 4K UHD panels. The 4K resolution category accounts for 82.9% of market share. Streaming services, gaming platforms, and broadcast networks now produce native 4K content. Consequently, consumers upgrading from 1080p displays naturally adopt the widely available 4K ecosystem.

Panel size segmentation also shows a clear leader. The 40–60 inches category controls 61.5% of total shipments. Television manufacturers concentrate their best-selling models within this size range. Retail promotions and consumer viewing preferences reinforce its dominance across residential and commercial display installations.

Application segmentation further confirms consumer electronics as the largest revenue contributor. The segment holds 62.3% share due to global smart TV replacement cycles. Falling panel costs and improved streaming content availability motivate households to upgrade older screens to modern ultra-high-definition displays.

Drivers

Expanding availability of native 4K content strongly drives market growth. Streaming platforms, sports broadcasters, and gaming developers increasingly deliver programming in 4K resolution. The resolution segment holds 82.9% market share, confirming widespread adoption. Consequently, manufacturers accelerate production of ultra-high-definition displays to meet growing consumer demand.

Manufacturing advancements also accelerate industry expansion. Improved LCD and OLED fabrication processes reduce per-unit production costs significantly. Lower manufacturing costs allow display brands to sell 4K televisions and monitors at accessible price points. Therefore, mid-tier consumer segments increasingly adopt ultra-high-definition display technology.

Use Cases

Consumer electronics companies use 4K panels to deliver immersive entertainment experiences. Smart televisions, gaming monitors, and streaming displays integrate high-resolution panels for sharper images and vibrant color accuracy. Consequently, global households increasingly upgrade existing televisions as content platforms release more native ultra-high-definition programming.

Healthcare institutions deploy high-resolution displays for medical imaging and surgical visualization. Radiology workstations rely on precise color reproduction and high pixel density for diagnostic accuracy. Therefore, medical professionals adopt 4K panels for remote diagnostics, telemedicine consultations, and advanced surgical imaging systems.

Major Challenges

Large high-brightness displays generate significant power consumption and thermal management challenges. Panels above 60 inches require complex cooling systems and stronger backlighting components. These technical requirements increase production costs and reduce reliability in continuous-use commercial environments such as outdoor signage installations.

Supply chain volatility also affects panel production stability. Display driver integrated circuits come from a limited number of semiconductor suppliers. When component shortages occur, panel manufacturers face higher costs and delayed production schedules. Consequently, smaller display companies struggle to compete with vertically integrated manufacturers.

Business Opportunities

Automotive infotainment systems create a major growth opportunity for display manufacturers. Modern vehicles increasingly feature digital dashboards, rear-seat entertainment screens, and central infotainment displays. Automakers also sign multi-year supply agreements, providing stable demand and premium pricing opportunities for specialized panel suppliers.

Healthcare and telemedicine infrastructure also generate high-value opportunities for display producers. Hospitals require accurate, reliable screens for diagnostic imaging and remote consultation platforms. Healthcare institutions prioritize precision and durability, allowing suppliers to command higher margins compared with standard consumer electronics displays.

Regional Analysis

Asia Pacific dominates the global market with a 43.60% share valued at USD 17.2 Billion in 2025. Countries including China, Japan, South Korea, and Taiwan host most global display manufacturing facilities. This dual advantage allows regional companies to capture both production revenue and strong domestic consumer demand.

North America represents a major secondary market for high-resolution displays. Strong adoption of smart TVs and commercial digital signage drives regional demand. Established streaming infrastructure and enterprise technology investments also sustain steady replacement cycles for televisions, collaboration displays, and professional monitors.

Recent Developments

- September 2024 — TCL Group announced plans to acquire 80% stake in LG Display’s Guangzhou LCD plant through CSOT, strengthening global LCD manufacturing capacity.

- March 2025 — TCL CSOT completed the acquisition of LG Display’s Guangzhou factories, transferring high-volume 4K panel production to Chinese operations.

- June 2025 — LG Display announced investment of approximately 700 billion won (~$515 million) to expand OLED manufacturing and research capabilities.

- June 2025 — The European Investment Bank approved a €30 million financing package for OLEDWorks to expand OLED production in Germany.

- July 2025 — Sony India launched a 98-inch BRAVIA 5 Mini-LED television with 4K resolution and 120 Hz refresh rate.

Conclusion

The ultra-high-definition display industry shows strong long-term growth potential. Increasing 4K content availability and declining manufacturing costs continue to drive consumer adoption worldwide. Display manufacturers also benefit from rising demand across healthcare imaging, automotive infotainment, and digital signage infrastructure.

LCD panels remain the dominant technology with 62.6% market share due to cost efficiency and established production capacity. Consumer electronics also lead applications with 62.3% share. Meanwhile, Asia Pacific maintains global leadership with 43.60% market share supported by strong manufacturing ecosystems.

Companies seeking to capture future growth must invest in advanced panel technologies and diversified application markets. Innovations in OLED structures, mini-LED backlighting, and AI image processing will define competitive differentiation. These advancements will help the market reach approximately USD 108.2 Billion by 2035.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)