Market Overview

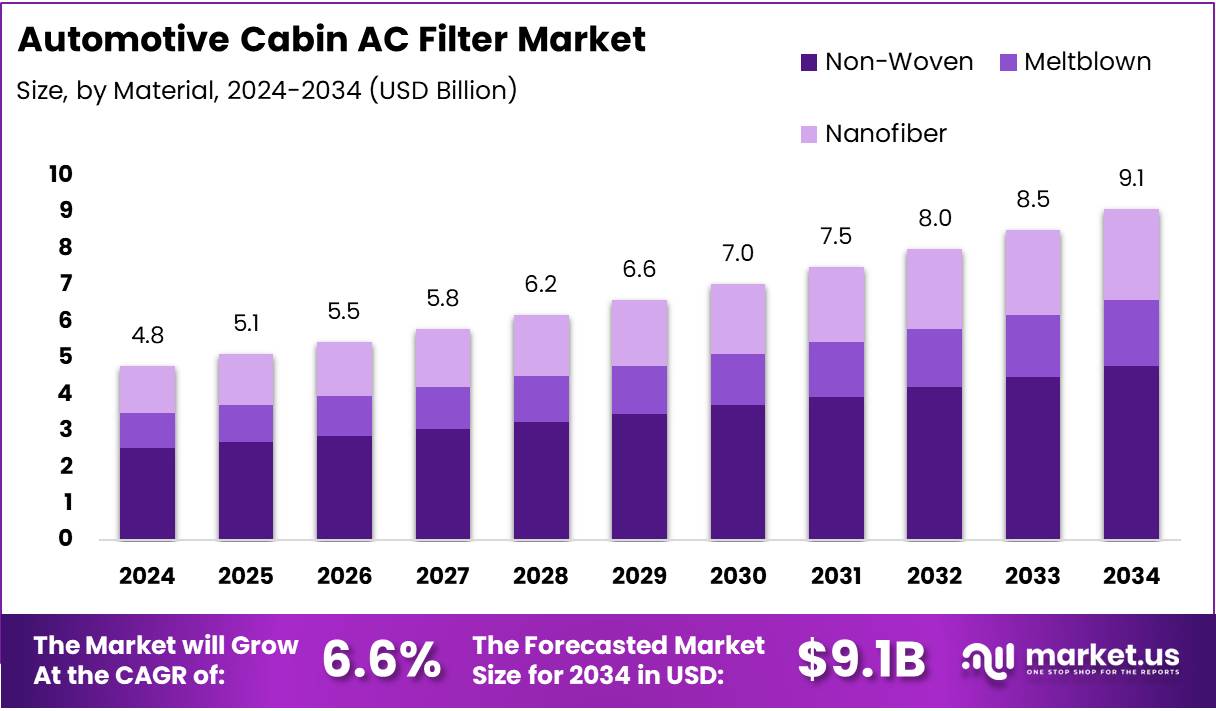

The Global Automotive Cabin AC Filter Market was valued at USD 4.8 Billion in 2024 and is projected to reach USD 9.1 Billion by 2034. The market is expected to expand at a CAGR of 6.6% during 2025–2034. Rising vehicle ownership and growing awareness about cabin air quality continue driving consistent industry demand globally.

Automotive cabin AC filters clean the air entering vehicle interiors through ventilation systems. These filters remove dust, pollen, smoke, allergens, and harmful pollutants before passengers inhale them. Passenger cars, commercial fleets, and premium mobility providers widely use these systems to improve cabin comfort and support healthier driving environments.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Automotive manufacturers across passenger vehicles, logistics fleets, ride-sharing services, and public transport systems increasingly adopt advanced filtration solutions. Passenger car makers use high-efficiency filters to improve comfort features. Commercial fleet operators install durable cabin filtration systems to support driver wellbeing during extended transportation and logistics operations.

Manufacturers integrate smart sensors, HEPA media, and activated carbon technologies into modern cabin filtration systems. These innovations improve air purification efficiency and support real-time air quality monitoring. Consequently, automakers differentiate premium and electric vehicle models through advanced in-cabin air purification and enhanced passenger protection features.

Governments worldwide enforce stricter regulations related to emissions, cabin hygiene, and in-vehicle air quality standards. Regulatory agencies encourage manufacturers to adopt cleaner filtration systems within new vehicle models. Moreover, sustainability policies and cleaner mobility initiatives continue strengthening replacement cycles for advanced automotive cabin air filtration technologies.

Industry statistics highlight strong long-term demand for cabin filtration technologies. Cabin filters generally require replacement every 12,000 miles or annually, creating recurring aftermarket opportunities. Additionally, true HEPA filters capture 99.97% of particles measuring 0.3 microns, improving passenger safety and accelerating adoption in pollution-prone urban regions.

Key Takeaways

- The global market reached USD 4.8 Billion in 2024 and is forecast to achieve USD 9.1 Billion by 2034.

- The Automotive Cabin AC Filter Market is projected to expand at a CAGR of 6.6% during 2025–2034.

- Non-Woven materials dominated the material segment with a 52.6% share in 2024 due to strong filtration performance.

- Conventional technology held a leading 59.9% market share because of affordability and widespread OEM integration.

- Activated Carbon filters accounted for 44.2% share in 2024 owing to odor and gas filtration advantages.

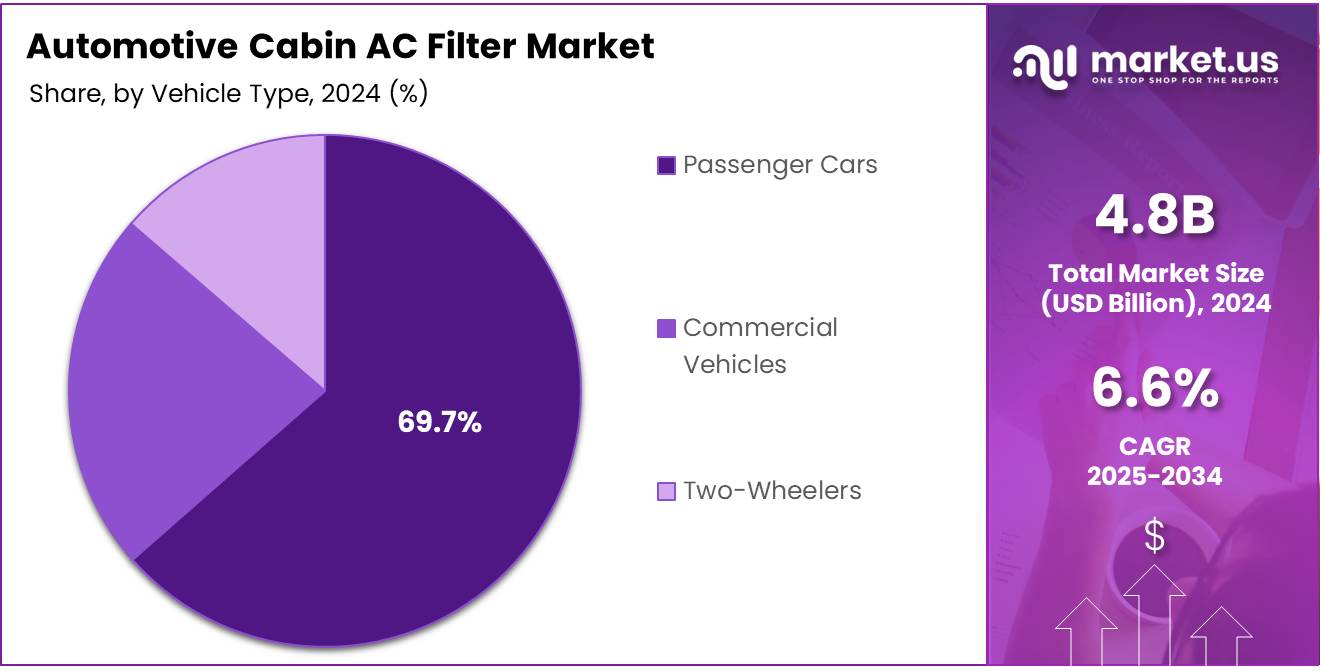

- Passenger Cars represented the largest vehicle category with a 69.7% market share in 2024.

- Aftermarket applications led the industry with a dominant 61.4% share driven by frequent replacement cycles.

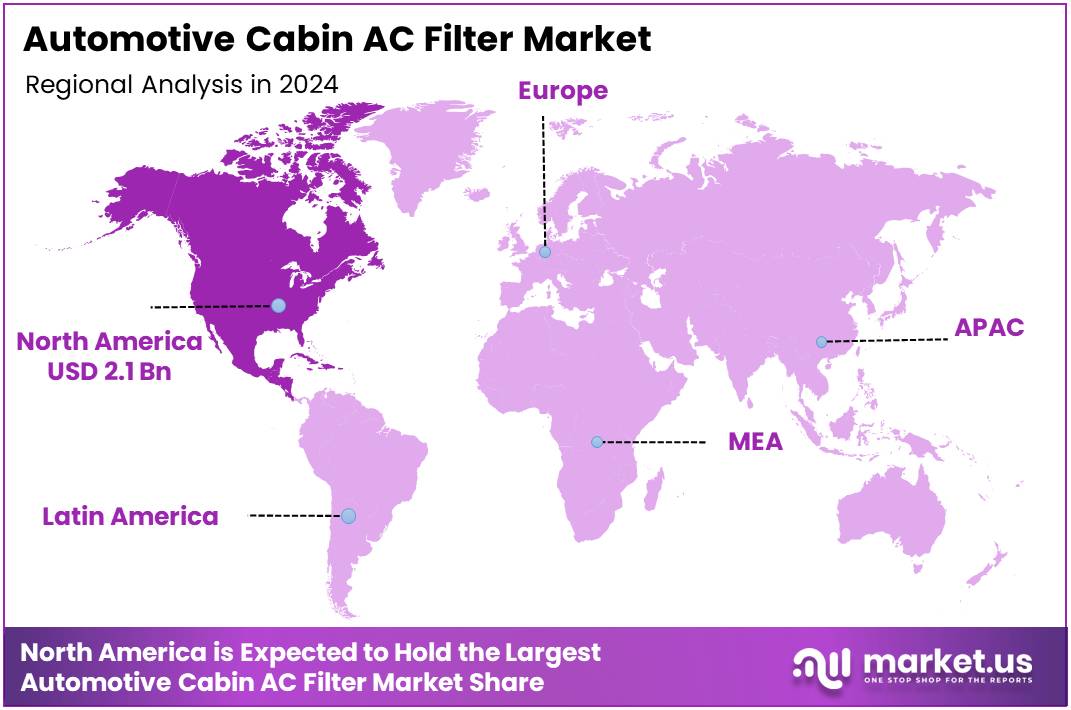

- North America captured 45.8% market share and generated USD 2.1 Billion revenue in 2024.

Market Segmentation Overview

Non-Woven materials dominated the market with a 52.6% share in 2024. Automakers preferred these materials because they balance airflow efficiency, durability, and cost-effectiveness. Consequently, manufacturers adopted Non-Woven filtration media across passenger cars and commercial vehicles to support large-scale production and maintain effective dust retention capabilities.

Meltblown and Nanofiber materials gained attention because consumers increasingly demand advanced filtration performance. Meltblown structures capture finer contaminants through dense fiber networks, while Nanofiber systems target ultrafine particles and allergens. Moreover, premium vehicle manufacturers integrate these materials to improve cabin hygiene and strengthen passenger respiratory protection.

Conventional technology led the technology segment with a 59.9% market share in 2024. Automakers widely selected these systems because they deliver reliable filtration performance without significantly increasing vehicle costs. Therefore, OEMs continued integrating conventional cabin filtration systems across mass-market vehicle categories and fleet transportation platforms.

Activated Carbon filters dominated filter type analysis with a 44.2% share due to superior odor and gas absorption performance. Passenger and commercial vehicle owners increasingly prefer these filters for improved cabin comfort. Additionally, Combination and Electrostatic filters continue gaining momentum through enhanced particulate and gaseous contaminant control.

Passenger Cars accounted for a dominant 69.7% market share in 2024. Growing personal vehicle ownership and rising consumer focus on in-cabin comfort accelerated demand across this category. Consequently, automakers integrated advanced filtration systems into passenger vehicles to support regulatory compliance and improve customer driving experiences.

Aftermarket applications led the market with a 61.4% share in 2024 because cabin filters require regular replacement. Vehicle owners increasingly choose aftermarket products for affordability and easier availability. Moreover, expanding maintenance awareness and quick installation services continue supporting recurring aftermarket revenue generation globally.

Drivers

Urban pollution and rising respiratory health concerns strongly drive the Automotive Cabin AC Filter Market. Consumers increasingly prioritize cleaner in-vehicle air environments during daily commuting. Consequently, automakers install advanced filtration systems within mid-range and premium vehicles to improve passenger protection and strengthen brand competitiveness across urban transportation markets.

Government regulations related to vehicle air quality standards continue accelerating cabin filter adoption worldwide. Regulatory authorities encourage manufacturers to integrate effective filtration technologies into new vehicle platforms. Moreover, stricter compliance requirements motivate OEMs to develop high-performance filters capable of reducing pollutants, allergens, and harmful airborne contaminants inside vehicles.

Use Cases

Passenger vehicle manufacturers use activated carbon and HEPA filtration systems to improve interior air quality and passenger comfort. These systems remove odors, allergens, and microscopic pollutants during everyday transportation. Consequently, premium automakers position advanced cabin filtration technologies as important comfort and wellness features for health-conscious consumers.

Commercial fleet operators install durable cabin AC filters to protect drivers during long-distance logistics and transportation operations. These systems reduce dust exposure and maintain ventilation efficiency in polluted urban environments. Additionally, public transport providers adopt advanced cabin filtration solutions to improve passenger safety and support healthier commuting experiences.

Major Challenges

Limited consumer awareness regarding cabin filtration health benefits continues restricting market expansion in several developing regions. Many vehicle owners delay filter replacement due to insufficient maintenance knowledge. Consequently, aftermarket suppliers face slower adoption rates for premium filtration technologies despite increasing urban pollution and growing respiratory health concerns.

Aftermarket filter compatibility issues create operational challenges for manufacturers and vehicle owners globally. Universal filter designs may not accurately fit certain vehicle models, reducing filtration efficiency and installation reliability. Moreover, manufacturers must invest additional resources into customer education and product customization to improve replacement confidence.

Business Opportunities

Smart cabin filtration systems equipped with real-time air quality sensors create strong growth opportunities for industry participants. These technologies help vehicle owners monitor cabin conditions and improve maintenance schedules. Consequently, manufacturers developing connected filtration products can strengthen customer engagement and capture premium automotive technology demand.

Eco-friendly and antimicrobial cabin filters present major business opportunities across premium and environmentally conscious vehicle segments. Manufacturers increasingly develop biodegradable filtration materials and anti-allergen solutions to address sustainability goals and passenger wellness concerns. Additionally, electric vehicle expansion supports demand for specialized filtration systems optimized for EV cabin airflow designs.

Regional Analysis

North America dominated the Automotive Cabin AC Filter Market with a 45.8% share valued at USD 2.1 Billion in 2024. Strong premium vehicle adoption, growing urban pollution concerns, and strict air quality regulations supported regional leadership. Consequently, automakers across the United States and Canada accelerated deployment of advanced cabin filtration technologies.

Asia Pacific emerged as a fast-growing regional market due to rising vehicle production and worsening urban air pollution levels. China, India, Japan, and South Korea continue investing in advanced automotive filtration technologies. Moreover, expanding electric vehicle adoption and increasing health awareness strengthen long-term regional market growth potential.

Recent Developments

- November 2025 — Atmus Filtration Technologies announced plans to acquire Koch Filter Corporation to strengthen advanced filtration product capabilities.

- February 2025 — Thermo Fisher Scientific acquired Solventum’s Purification and Filtration Business to expand high-performance filtration technology offerings.

- January 2024 — Bosch introduced the upgraded FILTER+pro cabin filter system with improved dust and allergen purification performance.

- February 2024 — Smart Parts launched washable and reusable cabin air filters focused on sustainability and long-term cost savings.

Conclusion

The Automotive Cabin AC Filter Market demonstrates strong long-term growth potential supported by rising pollution concerns, stricter regulations, and increasing vehicle ownership. Automakers continue integrating advanced filtration technologies into modern transportation platforms. Consequently, demand for HEPA, activated carbon, and sensor-enabled filtration systems will steadily expand worldwide.

Passenger Cars and Aftermarket applications continue dominating industry demand due to strong replacement cycles and growing consumer health awareness. North America maintains regional leadership through premium vehicle penetration and regulatory support. Meanwhile, Asia Pacific presents substantial growth opportunities driven by urbanization and expanding electric vehicle manufacturing activities.

Manufacturers must prioritize sustainable materials, smart sensor integration, and premium filtration performance to remain competitive in evolving automotive markets. Strategic partnerships with OEMs and aftermarket distributors will further strengthen long-term market positioning. The global Automotive Cabin AC Filter Market is projected to reach USD 9.1 Billion by 2034.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)