Market Overview

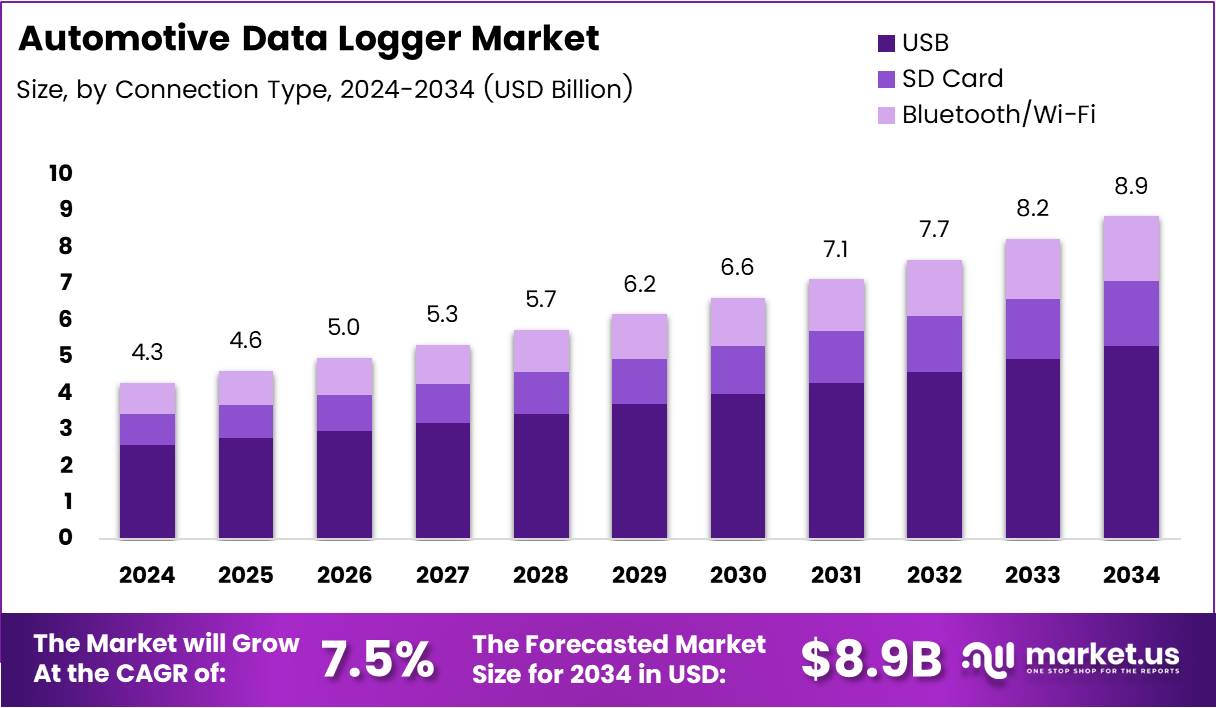

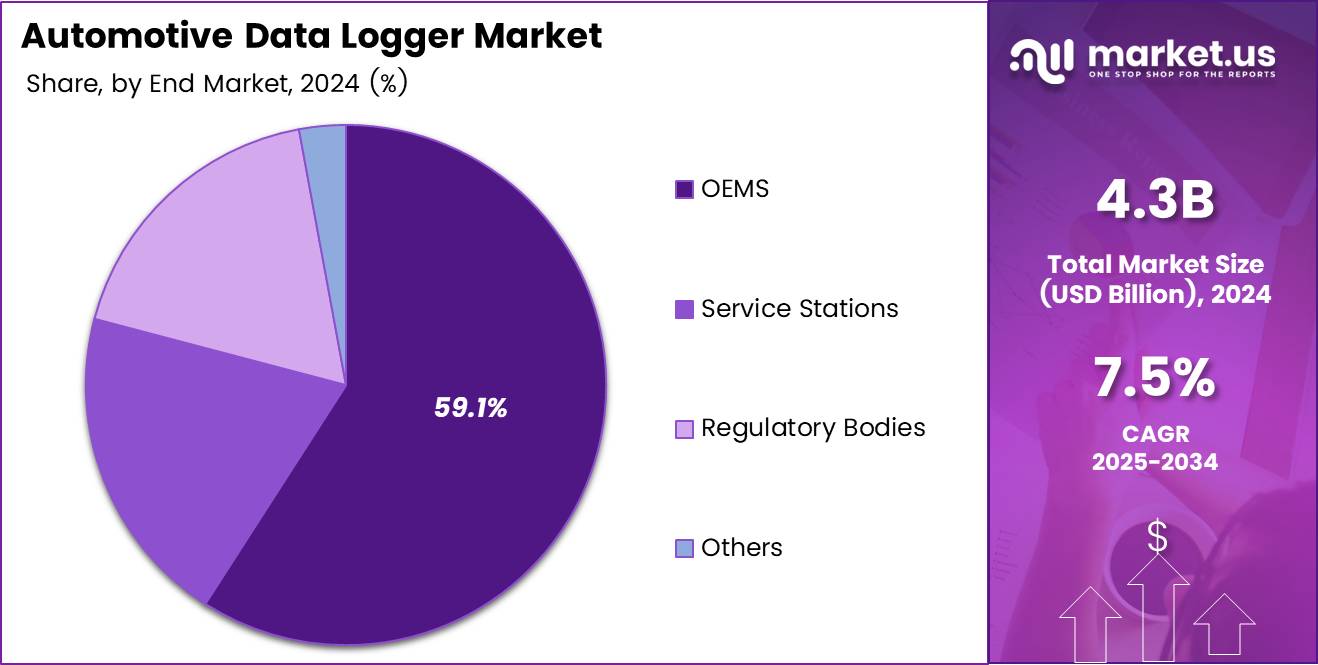

The global Automotive Data Logger Market was valued at USD 4.3 Billion in 2024 and is projected to reach USD 8.9 Billion by 2034. The market is expected to expand at a CAGR of 7.5% during 2025–2034. Rising demand for connected vehicles and vehicle diagnostics continues accelerating industry expansion across major automotive economies.

Automotive data loggers capture and store vehicle information from engines, sensors, braking systems, and telematics platforms. Manufacturers, fleet operators, and service centers use these systems for monitoring performance and maintenance conditions. Additionally, automotive companies rely on continuous data collection to improve vehicle safety, fuel efficiency, and operational reliability across commercial and passenger transportation.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Passenger vehicle manufacturers, logistics companies, and insurance providers remain major users of vehicle data recording technologies. Fleet operators use these systems for route optimization and predictive maintenance scheduling. Moreover, automotive OEMs apply recorded driving information during product testing, emissions validation, and warranty analysis to improve customer support and reduce unexpected vehicle failures.

Artificial intelligence, cloud analytics, and wireless communication technologies continue transforming automotive monitoring systems globally. Modern platforms analyze real-time vehicle information and identify performance abnormalities before mechanical breakdowns occur. Consequently, manufacturers integrate advanced software capabilities and edge computing features into automotive data logging systems to support autonomous driving development and connected mobility services.

Government agencies support market growth through vehicle safety regulations, emissions compliance rules, and telematics monitoring requirements. Commercial transport authorities increasingly require electronic vehicle tracking and driver behavior monitoring systems. Furthermore, stricter environmental policies encourage automakers to deploy advanced diagnostic solutions that improve engine efficiency and support regulatory reporting across transportation industries worldwide.

MITRE Corporation reported that 10 out of 14 advanced driver-assistance features exceeded 50% penetration in the United States during 2023. The Autopian also stated that connected vehicles can generate nearly 25 gigabytes of data every hour. These figures highlight rising demand for intelligent automotive analytics and high-capacity data logging infrastructure worldwide.

Key Takeaways

- Global Automotive Data Logger Market is projected to reach USD 8.9 Billion by 2034 from USD 4.3 Billion in 2024.

- The market is expected to grow at a CAGR of 7.5% during the forecast period from 2025 to 2034.

- USB connectivity leads the connection segment with a market share of 45.8% due to reliable data transfer capabilities.

- Hardware components dominate the market with a share of 68.9% because sensors and processors remain essential infrastructure.

- Passenger cars accounted for 52.5% market share, reflecting strong connected vehicle adoption among consumers.

- ICE vehicles captured 59.6% share due to widespread deployment and established diagnostic standards globally.

- Post-sales applications represented 66.2% share as fleet operators prioritize predictive maintenance and warranty analysis.

- OEMs held 59.1% market share through factory-installed vehicle monitoring and integrated telematics solutions.

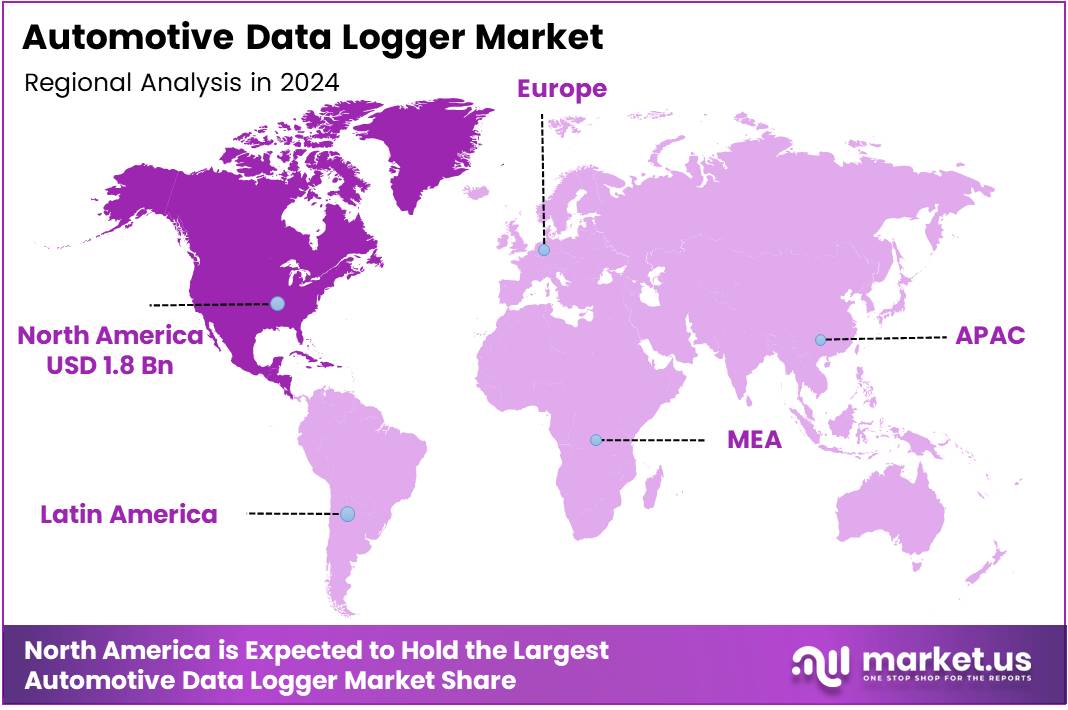

- North America led the global market with 43.70% share valued at USD 1.8 Billion.

Market Segmentation Overview

USB connectivity dominated the market with a share of 45.8% in 2024 because automotive platforms require dependable and cost-efficient data transmission. Manufacturers prefer USB interfaces due to broad compatibility with diagnostic systems and existing vehicle architectures. Consequently, automakers continue integrating USB-supported logging technologies across passenger vehicles and commercial transportation fleets worldwide.

Hardware components captured 68.9% market share because sensors, processors, and storage modules remain central to automotive data collection systems. These devices operate effectively under harsh automotive environments including vibrations and temperature changes. Additionally, miniaturization technologies improve processing capabilities and encourage wider deployment in connected mobility applications and advanced vehicle diagnostics platforms.

Passenger cars held the leading vehicle segment with 52.5% share during 2024. Consumer demand for infotainment systems, telematics services, and advanced safety features continues driving adoption across personal mobility platforms. Moreover, automakers increasingly differentiate vehicles through connected services, personalized driving analytics, and enhanced navigation capabilities supported by intelligent data monitoring systems.

ICE vehicles maintained dominance with 59.6% share, while post-sales applications accounted for 66.2% market contribution. Established combustion engine diagnostic standards support large-scale logger deployment across global transportation systems. Furthermore, aftermarket service providers and fleet operators increasingly use automotive analytics platforms for maintenance optimization, warranty management, and operational performance improvement.

Drivers

Advanced driver-assistance systems continue driving strong demand for automotive data logger technologies worldwide. Vehicle manufacturers collect high-resolution operational data from cameras, radar, and sensor systems to validate safety performance under real-world driving conditions. Consequently, stricter safety regulations encourage broader deployment of intelligent monitoring systems across passenger and commercial vehicle production programs.

Connected mobility adoption also accelerates market growth because modern vehicles generate massive operational datasets every day. Fleet operators and automakers require continuous monitoring for maintenance planning, fuel optimization, and driver behavior analysis. Additionally, cloud-integrated telematics systems enable remote diagnostics and predictive analytics that improve transportation efficiency and reduce long-term operational costs significantly.

Use Cases

Fleet management companies use automotive data loggers to monitor fuel consumption, route efficiency, and vehicle utilization in real time. Continuous diagnostics help operators schedule maintenance before costly mechanical failures occur. Therefore, logistics providers improve delivery reliability, reduce downtime, and increase operational productivity through predictive maintenance and intelligent transportation analytics systems.

Automotive manufacturers apply vehicle data logging technologies during prototype testing and quality validation programs. Engineering teams collect detailed operational information from braking systems, powertrains, and safety components under multiple driving conditions. Moreover, recorded performance insights support regulatory compliance, software calibration, and continuous improvement of autonomous driving and connected vehicle technologies.

Major Challenges

High implementation costs remain a major challenge for small fleet operators and independent service providers. Advanced automotive logging infrastructure requires significant investment in sensors, cloud platforms, and software integration services. Consequently, organizations with limited financial resources often delay technology adoption, reducing market penetration across developing transportation and logistics sectors.

Complex data management requirements also create operational difficulties for companies handling large vehicle datasets. Automotive platforms generate extensive information streams that require secure storage, advanced analytics, and cybersecurity protection measures. Furthermore, regulatory compliance related to driver privacy and data security increases maintenance expenses and technical burdens for automotive technology providers globally.

Business Opportunities

Predictive maintenance solutions create strong business opportunities as transportation companies seek lower repair costs and improved fleet efficiency. Real-time monitoring systems identify component wear patterns before critical failures occur during operations. Consequently, software developers and telematics providers can expand cloud-based analytics services supporting maintenance optimization across commercial vehicle fleets worldwide.

Usage-based insurance programs also present attractive opportunities for automotive analytics providers and connected mobility companies. Insurance firms increasingly analyze driving behavior data to personalize premium structures and improve risk assessment models. Additionally, growing adoption of electric vehicles and autonomous testing programs increases demand for intelligent data collection and vehicle performance monitoring technologies.

Regional Analysis

North America dominated the Automotive Data Logger Market with a share of 43.70% valued at USD 1.8 Billion. Strong vehicle manufacturing activity, advanced telematics adoption, and strict emissions regulations continue supporting regional leadership. Moreover, insurance telematics programs and connected vehicle deployments encourage extensive use of automotive monitoring and diagnostic systems across transportation industries.

Asia Pacific represents the fastest-growing regional market because China, Japan, and India continue expanding vehicle production and electrification programs. Government investments in intelligent transportation systems and connected mobility infrastructure accelerate automotive analytics adoption. Furthermore, growing logistics operations and commercial fleet modernization projects create strong demand for advanced vehicle data monitoring technologies.

Recent Developments

- January 2025 — NXP Semiconductors announced a USD 625 million agreement to acquire TTTech Auto, strengthening automotive software integration capabilities.

- June 2025 — NXP completed the acquisition of TTTech Auto, enhancing its safety-critical automotive systems and vehicle data management portfolio.

- January 2024 — Intrepid Control Systems launched neoVI CONNECT at CES 2024, delivering ruggedized IP67 vehicle data logging solutions for harsh environments.

Conclusion

The Automotive Data Logger Market continues demonstrating strong long-term growth supported by connected mobility adoption, regulatory compliance requirements, and expanding vehicle analytics applications. Automakers and fleet operators increasingly rely on intelligent monitoring systems for diagnostics, predictive maintenance, and safety validation. Consequently, advanced telematics technologies remain central to future transportation infrastructure development globally.

Hardware solutions, USB connectivity, passenger cars, and ICE vehicles currently dominate market demand because these segments support broad automotive deployment and established diagnostic ecosystems. North America maintains regional leadership through strong regulatory frameworks and connected vehicle penetration. Meanwhile, Asia Pacific continues emerging as a high-growth region driven by electrification and fleet modernization initiatives.

Automotive technology providers must invest in artificial intelligence, cybersecurity protection, and cloud-integrated analytics capabilities to remain competitive. Companies that develop scalable, real-time monitoring platforms will capture expanding opportunities across electric vehicles, insurance telematics, and autonomous mobility ecosystems. The market is expected to reach USD 8.9 Billion by 2034.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)