Market Overview

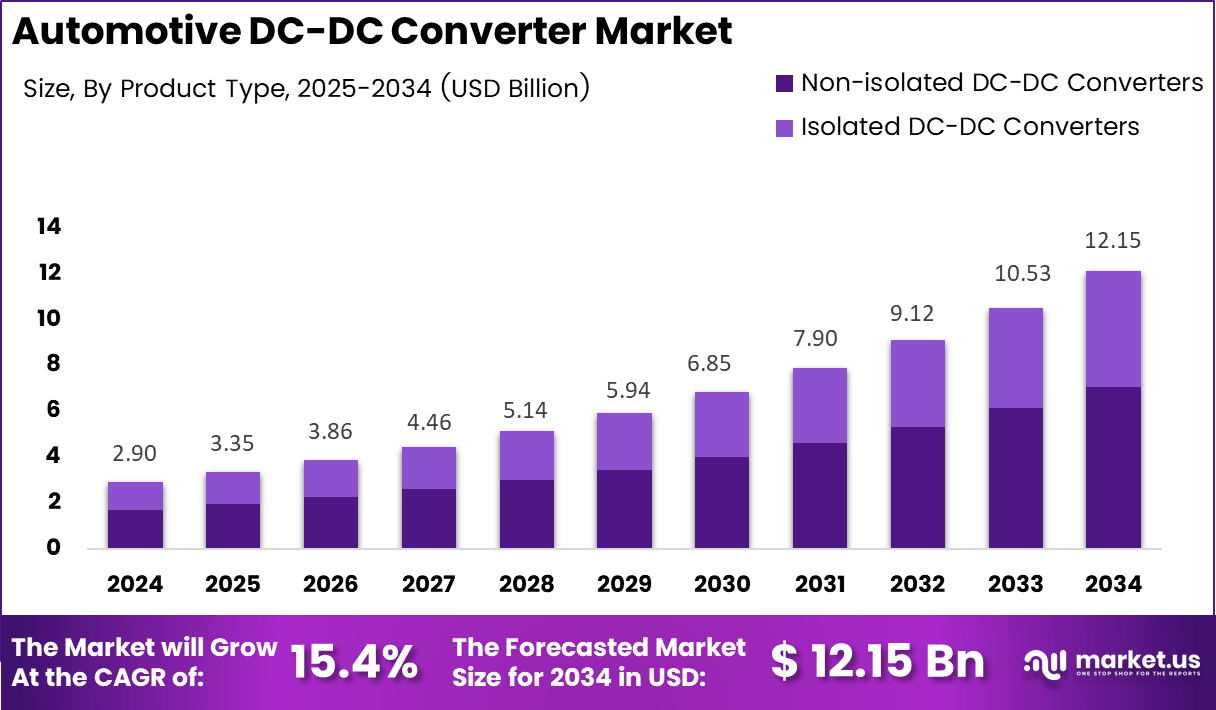

The global Automotive DC-DC Converter Market was valued at USD 2.9 billion in 2024 and is projected to reach USD 12.15 billion by 2034. The market is expected to expand at a CAGR of 15.4% during 2025–2034. Rapid electric vehicle adoption and rising integration of automotive electronics continue accelerating global market expansion significantly.

Automotive DC-DC converters regulate and transform voltage levels across electric, hybrid, and conventional vehicle systems. These converters supply stable low-voltage power for infotainment, ADAS, lighting, and battery management functions. Additionally, automakers depend on efficient power conversion systems to improve vehicle reliability, thermal stability, and electrical efficiency across modern mobility platforms.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Electric vehicle manufacturers, commercial fleet operators, and automotive suppliers remain major users of DC-DC converter technologies. Passenger vehicles require stable voltage conversion for digital clusters, sensors, and connectivity modules. Moreover, commercial fleets increasingly adopt advanced converters to support heavy electrical loads, thermal management systems, and reliable auxiliary power distribution across electrified transportation networks.

Wide-bandgap semiconductors, digital control systems, and modular converter architectures continue transforming automotive power electronics. Manufacturers increasingly use GaN- and SiC-based technologies to improve switching efficiency and reduce thermal losses. Consequently, modern converters deliver compact packaging, faster energy conversion, and improved durability for electric and hybrid vehicle applications worldwide.

Government regulations promoting low-emission transportation and vehicle electrification continue supporting market growth globally. Policymakers increasingly encourage EV production through subsidies, charging infrastructure investments, and fuel-efficiency mandates. Furthermore, automotive manufacturers deploy high-efficiency converter systems to comply with evolving environmental regulations and improve energy management across next-generation vehicle platforms.

Industry findings show that automotive DC-DC converters operate efficiently between –40°C and +80°C while exceeding 90% energy efficiency. Passenger cars commonly use 12V battery systems, while trucks rely on 24V architectures. These technical requirements increase demand for reliable voltage conversion systems supporting diverse automotive electrical environments and operational conditions.

Key Takeaways

- The global Automotive DC-DC Converter Market is projected to grow from USD 2.9 billion in 2024 to USD 12.15 billion by 2034.

- The market is expected to expand at a CAGR of 15.4% during the forecast period from 2025 to 2034.

- Isolated DC-DC Converters dominated the product type segment with a market share of 58.2% in 2024.

- Battery Electric Vehicles accounted for 66.5% share due to increasing global EV adoption.

- The 40–70V input voltage segment led the market with a contribution of 51.4%.

- The 12V output voltage segment held the largest market share at 41.9% in 2024.

- The 1–10kW output power segment dominated with a share of 49.1%.

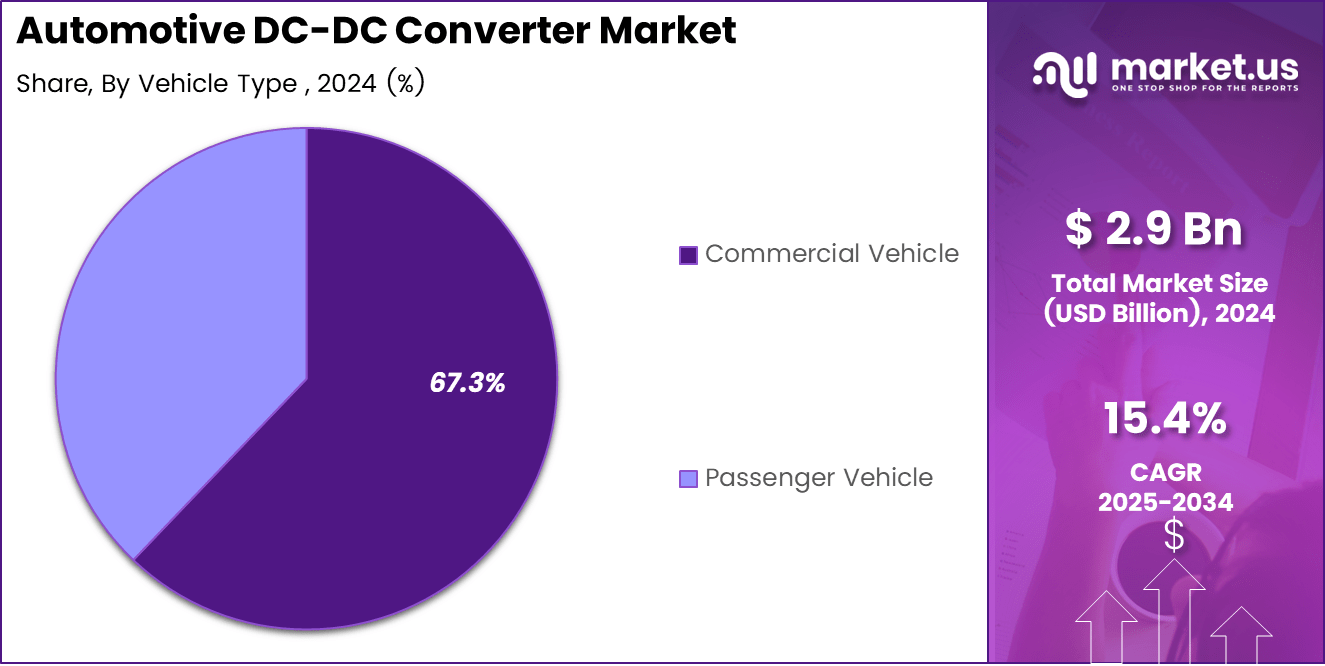

- Commercial Vehicles represented the leading vehicle type segment with a market share of 67.3%.

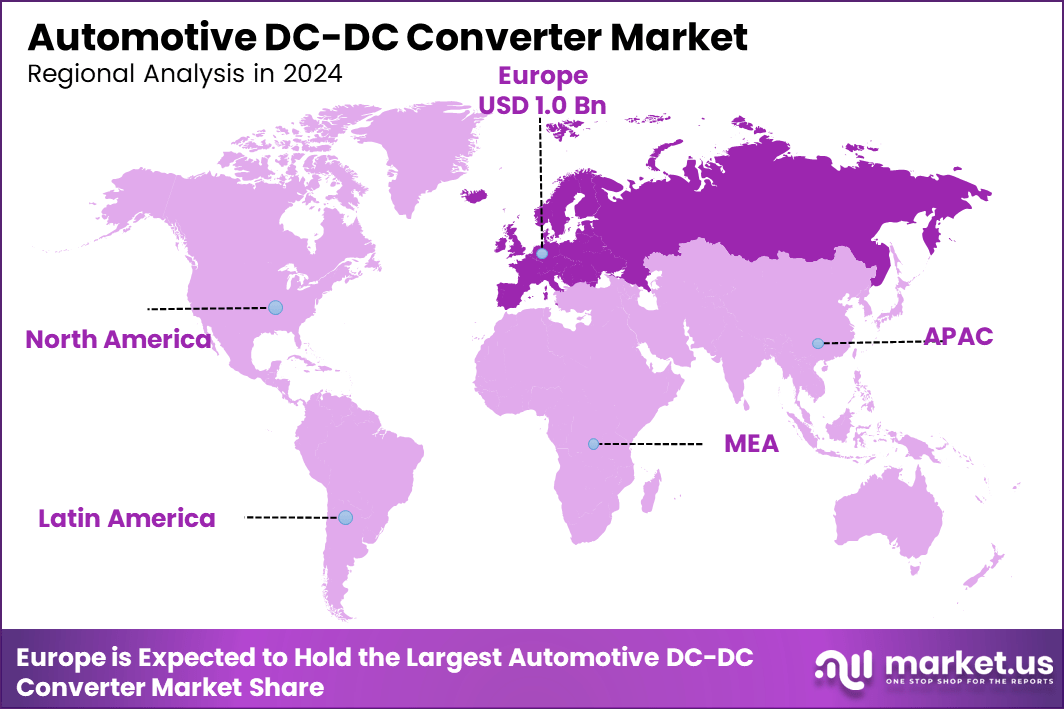

- Europe led the regional market with 37.2% share valued at USD 1 billion.

Market Segmentation Overview

Isolated DC-DC Converters dominated the product type segment with a market share of 58.2% in 2024. These systems provide galvanic isolation and improved electrical protection for high-voltage EV architectures. Consequently, automakers increasingly deploy isolated converters across electric vehicle platforms requiring safe power transfer and stable low-voltage management for sensitive electronic systems.

Battery Electric Vehicles held a dominant market position with a share of 66.5% because full-electric platforms require continuous multi-voltage power conversion. DC-DC converters support battery systems, thermal management, and auxiliary electronics within EV architectures. Additionally, rising EV production and charging infrastructure investments continue strengthening converter demand across global transportation markets.

The 40–70V input voltage segment accounted for 51.4% market share due to compatibility with mainstream EV and hybrid systems. Meanwhile, the 12V output voltage segment captured 41.9% share because modern vehicles continue relying on 12V systems for infotainment, lighting, and safety electronics. These requirements reinforce stable converter adoption globally.

The 1–10kW output power segment led with a share of 49.1%, while Commercial Vehicles dominated vehicle type demand with 67.3% contribution. Electrified buses, trucks, and logistics fleets increasingly require high-capacity converters for stable auxiliary power management. Furthermore, rising commercial fleet electrification strengthens long-term demand for advanced automotive power electronics systems.

Drivers

Growing demand for high-efficiency power conversion systems continues driving strong market expansion globally. Electric and hybrid vehicles require stable voltage regulation for sensors, battery management systems, and infotainment electronics. Consequently, automakers increasingly deploy advanced DC-DC converters that reduce energy losses while supporting reliable electrical performance across modern automotive architectures.

The rapid adoption of 48V vehicle architectures also accelerates demand for efficient converter technologies. Mild-hybrid systems improve fuel efficiency and support advanced electronic functions requiring dependable voltage transformation. Additionally, increasing integration of ADAS, digital clusters, and connected mobility features strengthens installation of compact DC-DC converters across passenger and commercial vehicle platforms worldwide.

Use Cases

Electric vehicle manufacturers use DC-DC converters to regulate voltage between high-voltage battery packs and low-voltage onboard electronics. These systems support lighting, infotainment, ADAS, and thermal management functions within EV architectures. Therefore, stable voltage conversion improves operational safety, battery efficiency, and overall driving reliability across next-generation electric mobility platforms.

Commercial fleet operators apply high-capacity DC-DC converters in buses and trucks requiring stable auxiliary power under demanding operational conditions. These converters support heavy electrical systems, connectivity modules, and advanced safety technologies. Moreover, reliable power management helps fleet operators improve energy efficiency, reduce maintenance costs, and enhance transportation performance during long-distance operations.

Major Challenges

Thermal management challenges remain a major restraint within the Automotive DC-DC Converter Market. High-power electric vehicle systems generate significant heat that can reduce semiconductor lifespan and operational reliability. Consequently, manufacturers must invest in advanced cooling technologies and protective designs, increasing production complexity and overall system costs across automotive applications.

Limited standardization across automotive power electronics architectures also slows broader market adoption. Automakers use different voltage configurations, layouts, and integration processes for EV platforms worldwide. Furthermore, converter suppliers often require customized engineering solutions for individual OEMs, reducing scalability and extending development timelines across the global automotive supply chain.

Business Opportunities

GaN- and SiC-based converter technologies create strong business opportunities due to their superior efficiency and thermal performance. Automakers increasingly adopt these materials to reduce component size while improving power density across electric vehicle systems. Consequently, semiconductor manufacturers and converter suppliers can expand next-generation power electronics portfolios supporting global EV programs.

Bidirectional charging infrastructure also creates major opportunities for advanced automotive DC-DC converters globally. Vehicle-to-grid and vehicle-to-home applications require intelligent power conversion systems capable of managing two-way energy flow efficiently. Additionally, solid-state battery development increases demand for optimized voltage regulation technologies supporting future high-capacity automotive energy storage platforms.

Regional Analysis

Europe dominated the Automotive DC-DC Converter Market with a share of 37.2% valued at USD 1 billion in 2024. Strong EV adoption, strict carbon-emission regulations, and government-backed electrification initiatives continue supporting regional market leadership. Moreover, rising deployment of 48V mild-hybrid systems strengthens demand for advanced automotive power conversion technologies across Europe.

Asia Pacific represents one of the fastest-growing regional markets because China, Japan, and South Korea continue expanding electric vehicle production and battery technology investments. Governments across the region actively support clean mobility adoption through subsidies and infrastructure development. Furthermore, rising demand for compact automotive electronics accelerates converter integration across passenger and commercial vehicles.

Recent Developments

- June 2024 — Renesas Electronics completed the acquisition of Transphorm, Inc. to strengthen GaN-based automotive power product capabilities.

- March 2025 — Vicor introduced a new DCM™ family of regulated 48V-to-12V DC-DC converters for evolving EV architectures.

Conclusion

The Automotive DC-DC Converter Market continues demonstrating strong growth due to accelerating vehicle electrification, advanced electronics integration, and global clean mobility initiatives. Automakers increasingly depend on efficient power conversion technologies to support battery systems, safety electronics, and intelligent mobility platforms. Consequently, high-performance converters remain essential within next-generation automotive electrical architectures worldwide.

Isolated converters, Battery Electric Vehicles, and commercial fleets currently dominate market demand because these segments require reliable multi-voltage power management systems. Europe maintains strong regional leadership through strict emission regulations and electrification programs. Meanwhile, Asia Pacific continues emerging as a high-growth market driven by expanding EV production and battery innovation investments.

Automotive power electronics manufacturers must prioritize thermal efficiency, modular converter platforms, and advanced semiconductor integration to remain competitive. Companies investing in bidirectional charging technologies and intelligent power management systems will capture long-term electrification opportunities globally. The market is projected to reach USD 12.15 billion by 2034.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)