Market Overview

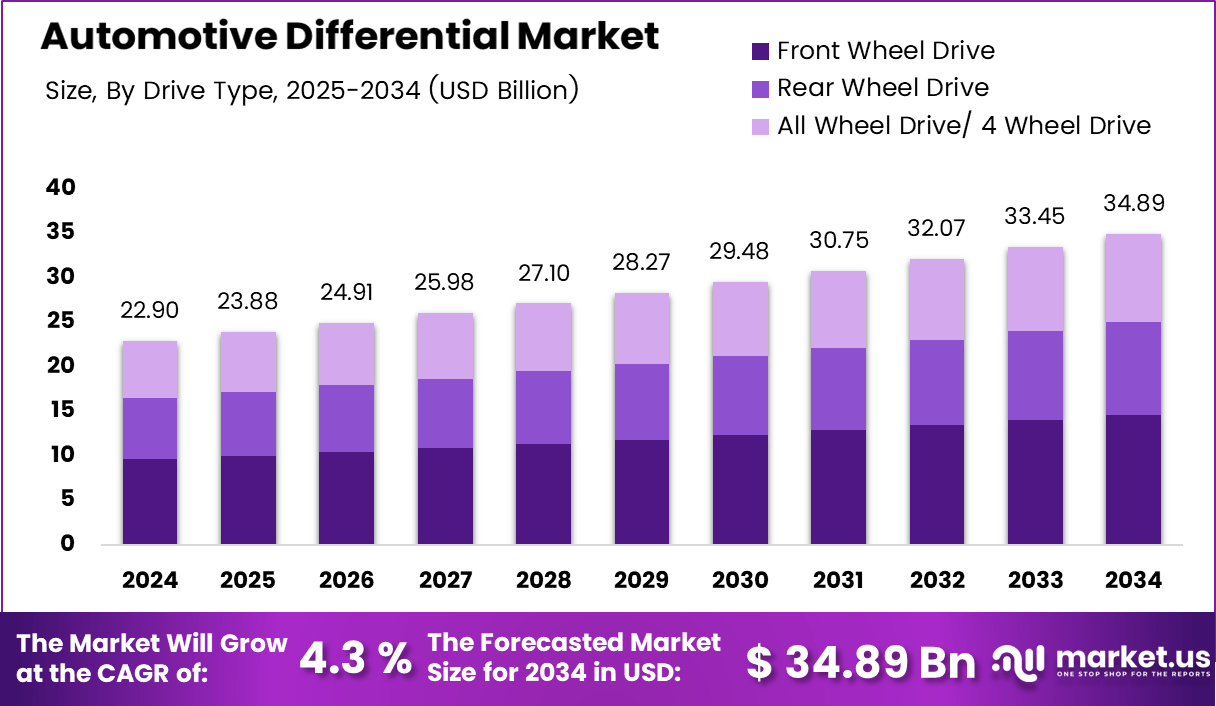

The global Automotive Differential Market was valued at USD 22.9 billion in 2024 and is projected to reach USD 34.89 billion by 2034. The market is expected to expand at a CAGR of 4.3% during 2025–2034. Growing demand for SUVs, performance vehicles, and advanced driveline systems continues strengthening industry expansion globally.

Automotive differentials distribute engine torque between wheels while allowing them to rotate at different speeds during turning. Vehicle manufacturers use these systems to improve traction, handling, and driving stability across varying road conditions. Additionally, passenger cars, trucks, and utility vehicles depend on differentials for smoother operation and reduced drivetrain stress.

Get further insight into the global trends shaping the future of the Automotive Differential industry. Request Free Sample

Passenger vehicle manufacturers, logistics companies, and agricultural equipment producers remain major users of automotive differential systems. SUVs and pickup trucks increasingly require all-wheel-drive configurations that depend on advanced torque-management components. Moreover, fleet operators use modern driveline systems to improve load handling, operational durability, and fuel-efficient transportation performance across commercial fleets.

Electronic controls, lightweight materials, and torque-vectoring technologies continue improving modern differential systems significantly. Automakers increasingly integrate intelligent driveline platforms that monitor traction and wheel speed in real time. Consequently, advanced differentials improve vehicle stability, cornering precision, and energy efficiency while supporting next-generation electric and autonomous mobility solutions worldwide.

Governments worldwide support efficient drivetrain technologies through fuel-economy regulations and emission-control programs. Automotive manufacturers increasingly adopt lightweight and electronically controlled differentials to reduce energy loss and improve vehicle performance. Furthermore, electrification policies encourage the development of e-axles and multi-motor systems requiring advanced torque-balancing capabilities for modern electric mobility platforms.

Research studies highlight the growing importance of precision-engineered differential systems in modern transportation. Industry findings show that limited-slip differentials can distribute torque from 25% to 75% between wheels under varying traction conditions. These capabilities improve acceleration stability and driving safety, reinforcing strong demand for advanced differential technologies across global automotive platforms.

Key Takeaways

- The global Automotive Differential Market is projected to grow from USD 22.9 billion in 2024 to USD 34.89 billion by 2034.

- The market is expected to register a CAGR of 4.3% during the forecast period from 2025 to 2034.

- Open Differential dominated the differential type segment with a market share of 34.7% in 2024.

- Front Wheel Drive led the drive type segment with a share of 41.8% due to fuel-efficient layouts.

- Passenger Cars accounted for 66.1% of total market installations because of strong global production volumes.

- Ring Gear emerged as the leading component segment with a contribution of 31.2% in 2024.

- Agricultural Tractors dominated the equipment type category with a market share of 59.4%.

- Asia Pacific led the regional market with 43.7% share valued at USD 10.0 billion.

- Electrification and torque-vectoring technologies continue shaping next-generation differential demand globally.

Market Segmentation Overview

Open Differential dominated the differential type segment with a market share of 34.7% in 2024. Manufacturers widely use these systems because they offer cost-efficient torque distribution and smooth cornering performance. Consequently, affordable passenger cars and mass-market vehicle platforms continue driving strong installation rates across developed and emerging automotive manufacturing economies globally.

Front Wheel Drive captured 41.8% market share due to strong production of compact cars and entry-level sedans. Automakers prefer this layout because it improves fuel economy while reducing manufacturing costs. Additionally, space-efficient drivetrain architecture supports broader adoption across urban mobility platforms and high-volume passenger vehicle categories worldwide.

Passenger Cars led the vehicle type segment with a dominant share of 66.1% during 2024. Growing urban transportation demand and rising sales of compact SUVs continue strengthening differential installations across global passenger fleets. Moreover, automakers increasingly integrate modern driveline technologies to improve handling performance, traction control, and driving comfort in consumer vehicles.

Ring Gear accounted for 31.2% market share, while Agricultural Tractors held 59.4% of the equipment segment. Ring gears remain critical for torque transfer and rotational control across automotive drivetrains. Furthermore, agricultural machinery requires durable differential systems that support heavy loads, rugged terrain operations, and stable traction under challenging field conditions.

Drivers

Growing adoption of AWD and 4WD systems continues driving strong demand for automotive differential technologies globally. SUV buyers increasingly expect improved traction, stability, and multi-terrain driving capability from modern vehicles. Consequently, automakers integrate advanced differential systems into passenger cars, pickup trucks, and commercial fleets to improve performance under varying road conditions.

Performance-oriented vehicles also accelerate market growth because modern sports cars require advanced limited-slip and torque-vectoring technologies. These systems improve acceleration control, cornering precision, and drivetrain efficiency during high-speed driving operations. Additionally, intelligent electronic differential systems support real-time torque adjustments that enhance fuel efficiency and vehicle handling across premium automotive platforms.

Use Cases

Passenger vehicle manufacturers use automotive differentials to improve stability, traction, and handling across hatchbacks, sedans, and SUVs. Advanced torque-management systems help vehicles maintain controlled movement during turning and uneven road conditions. Therefore, automakers increasingly deploy electronic differentials to deliver smoother driving experiences and higher consumer safety standards globally.

Agricultural equipment manufacturers apply heavy-duty differential systems in tractors operating across rugged and muddy terrain conditions. These components improve wheel traction and optimize torque distribution under heavy workloads. Moreover, reliable driveline performance helps agricultural operators increase productivity while reducing maintenance requirements during continuous field operations and commercial farming activities.

Major Challenges

High manufacturing costs remain a major challenge for electronically controlled differential systems. Sensors, actuators, and advanced control modules significantly increase production expenses for automakers targeting cost-sensitive vehicle categories. Consequently, entry-level and mid-range vehicle manufacturers often limit adoption of premium differential technologies to maintain affordable pricing structures in competitive markets.

Complex maintenance requirements also restrict broader deployment of advanced driveline systems across some regions. Electronic differential units require specialized servicing equipment, software calibration, and trained technicians for accurate diagnostics. Furthermore, long-term maintenance costs may discourage fleet operators and budget-conscious vehicle owners from adopting electronically optimized differential technologies despite their operational benefits.

Business Opportunities

Electric vehicle expansion creates strong opportunities for EV-specific differential systems supporting e-axles and dual-motor platforms. Automakers increasingly develop lightweight driveline technologies that improve energy efficiency and vehicle range performance. Consequently, advanced differential manufacturers can capitalize on growing global investments in electric mobility and next-generation drivetrain engineering solutions.

Torque-vectoring technologies also create major opportunities within autonomous and intelligent mobility ecosystems. Automated vehicles require highly accurate wheel torque distribution for safer lane changes and controlled emergency maneuvers. Additionally, growing aftermarket demand for off-road and performance upgrades supports rising sales of locking and limited-slip differential solutions across enthusiast communities worldwide.

Regional Analysis

Asia Pacific dominated the Automotive Differential Market with a share of 43.7% valued at USD 10.0 billion in 2024. China, Japan, India, and South Korea continue expanding automotive manufacturing and SUV production significantly. Moreover, strong electric vehicle investments and drivetrain modernization programs accelerate demand for advanced differential systems across passenger and commercial fleets.

North America demonstrated steady market expansion supported by rising production of SUVs, pickup trucks, and performance-oriented vehicles. Consumers increasingly prefer AWD-equipped models that improve traction and utility performance under diverse weather conditions. Furthermore, off-road vehicle culture and advanced driveline innovation continue supporting adoption of electronic and torque-vectoring differential technologies across the region.

Recent Developments

-

- October 2025 — BorgWarner expanded its partnership with Chery to supply advanced AWD products for next-generation intelligent vehicles.

- April 2024 — Eaton Performance launched the Detroit Truetrac differential for 2015–2024 Ford F-150 models with 8.8-inch axles.

- October 2024 — ZF Friedrichshafen AG secured a multi-year contract to supply differential gear sets for a new European EV platform.

Conclusion

The Automotive Differential Market continues expanding steadily due to rising demand for AWD systems, electric drivetrains, and advanced vehicle stability technologies. Automakers increasingly integrate intelligent torque-management systems that improve traction, handling, and fuel efficiency. Consequently, differential technologies remain essential components within modern passenger, commercial, and utility vehicle platforms globally.

Open differentials, Front Wheel Drive systems, passenger cars, and ring gears currently dominate industry demand because they support high-volume automotive production and efficient driveline performance. Asia Pacific maintains strong regional leadership through extensive vehicle manufacturing and electrification investments. Meanwhile, North America continues generating steady growth from SUVs and performance-oriented mobility segments.

Automotive component manufacturers must prioritize lightweight engineering, electronic control systems, and EV-compatible driveline innovations to remain competitive. Companies investing in torque-vectoring technologies and intelligent differential architectures will capture long-term opportunities across connected mobility and autonomous transportation ecosystems. The market is projected to reach USD 34.89 billion by 2034.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)